Dingdang Health Lists on HKEX, Marking a New Milestone for Internet Healthcare

Another Internet Healthcare Company Goes Public in 2022! Today, Dingdang Health Successfully Listed on the Hong Kong Stock Exchange. Dingdang Health’s IPO Price Was HK$12 per Share, with a Slight 2% Increase at Opening, Reaching a Market Capitalization of HK$16.3 Billion.

Over the past eight years, Dingdang Health’s development path has been far from easy. In the pharmaceutical O2O sector, a number of peers collapsed after their initial business models were proven unviable; major platforms such as Meituan and Ele.me entered the market leveraging their online traffic and delivery resources, while chain retail enterprises rapidly expanded into O2O by capitalizing on their offline pharmacy advantages...

Through the Dingdang Kuaiyao app, Dingdang Health has successively provided medicine delivery and comprehensive healthcare services, established offline smart pharmacies and an internet hospital, and later launched its “DTP to Home” service. The company’s self-positioning has evolved from an O2O platform, to a new-retail pharmaceutical enterprise, then to an internet-based pharmaceutical and healthcare company, followed by an internet “medical care + pharmaceuticals” home-based health service platform, and finally to a digital medical and healthcare home-service provider.

Breaking through the competition via a self-operated model and achieving a successful IPO marks a new starting point in Dingdang Health’s development journey, and further signals the beginning of a new phase in the landscape of the pharmaceutical O2O market.

The emergence of the O2O (Online-to-Offline) trend in the pharmaceutical sector stems from the success of the internet in other consumer domains, particularly the rapid growth of O2O penetration in food delivery services. In the trillion-yuan pharmaceutical retail market, there is room for improvement in the convenience of medication purchases for users, and the service radius of physical pharmacies needs to be expanded. Drawing on O2O experiences in other sectors, it undoubtedly serves as a powerful tool to address these challenges.

With this mindset, a wave of O2O platforms was established between 2013 and 2014, with some securing backing from renowned investment firms. Dingdang Health was among the companies founded during this period.

However, the idealized bubble was quickly burst by reality; within just two to three years, a large number of platforms ceased operations. According to statistics from VCBeat, more than 30 platforms were focusing on developing pharmaceutical O2O services in 2013; by 2016, over half of these platforms had either shut down or pivoted their business models.

The reasons for failure are roughly as follows:

First, purchasing medication is a low-frequency need; particularly at that time, when smartphone users were predominantly middle-aged and young adults, the demand for buying medicine was even less frequent.

Second, a key feature of the O2O model is rapid medication delivery. To meet the demand for timely delivery of orders that are low-frequency and dispersed in both time and location, substantial logistics costs must be incurred, necessitating a mature logistics system.

Third, online platforms and offline pharmacies maintain a cooperative relationship, resulting in limited control over the pharmacies; in particular, the fixed operating hours of offline pharmacies cannot meet the 24-hour delivery demands of online platforms.

The capabilities of the founding team and capital investment are also critical factors determining the success or failure of a project.

Dingdang Health has been able to break through the industry’s predicament primarily by finding breakthroughs to address the aforementioned challenges. The background support from the founding team and capital infusion is evident, exemplified by Yang Wenlong, Chairman of Renhe Pharmaceutical, embarking on a “second entrepreneurial venture,” and securing over RMB 3 billion in financing across five rounds. Since 2016, Dingdang Health has also established its own pharmacy network to ensure 24-hour operations; built a standardized delivery team to guarantee medication delivery speed and brand recognition; and continuously expanded the number and coverage of its pharmacies, leveraging economies of scale to overcome the challenge of low purchase frequency and reduce delivery costs.

In recent years, the rapid growth in the number of Dingdang Health’s smart pharmacies and the volume of medication orders has driven overall revenue growth, with total income rising from RMB 580 million in 2018 to RMB 3.68 billion in 2021. Under Dingdang Health’s business model, the high costs associated with building offline pharmacies and delivery networks have meant that profitability has not yet been achieved despite the rapid revenue growth. However, the loss ratio is gradually narrowing: the adjusted net loss ratio decreased from 11.9% in 2018 to 8.9% in 2021, and further declined to 4.5% in the first quarter of 2022.

The pharmaceutical O2O industry is evolving through growing pains, while Dingdang Health has built a model distinct from traditional O2O, establishing a self-operated O2O model.

Meanwhile, platform-based and chain enterprises have also made significant inroads into the pharmaceutical O2O market. The former includes companies such as Meituan, Ele.me, and JD Health, while the latter mainly consists of chain pharmacies like Laobaixing, Dashenlin, and Yifeng.

In the platform-based and chain-based models, there are numerous listed companies with substantial direct financial and resource support; these enterprises either possess advantages in online and offline traffic or benefit from large-scale pharmacy operations. The self-operated O2O model, akin to “starting from scratch,” has also produced a listed company, Dingdang Health. As the development paths of these three models become increasingly distinct, the market landscape shaped by the three major “camps” has entered a new phase.

Currently, there are too many voices in the industry directly comparing typical enterprises within the aforementioned models. In VCBeat’s view, while commercial competition among various models and companies is inevitable, a mutually integrated industry ecosystem is more conducive to expanding the market under the new landscape.

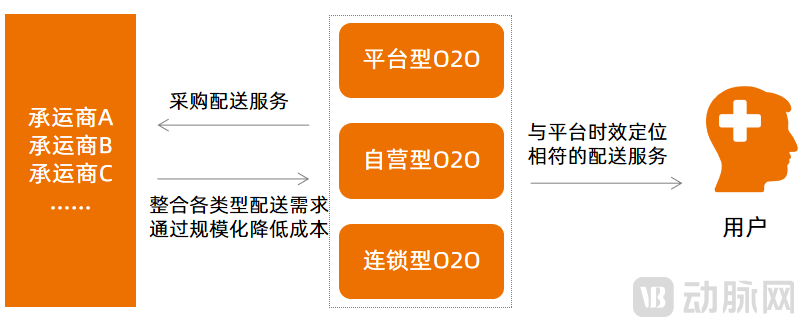

“Sharing” of Delivery Resources

One-hour delivery, 30-minute delivery, 28-minute delivery... The aggressive promotion of delivery timeframes by various companies highlights that delivery speed is a key dimension of corporate competition.

The Internet-based “sharing economy” has exerted tremendous influence among consumer-end (C-end) users, while for business-end (B-end) enterprises in the online-to-offline (O2O) sector, “shared delivery” has also evolved into an industry norm.

Various pharmaceutical O2O models achieve overall industry cost reduction through "shared" delivery. Chart by VCBeat

Taking Dingdang Health as an example, its prospectus reveals that as of March 2022, rapid medicine delivery was primarily provided by 2,600 riders, who were engaged through outsourcing arrangements with delivery partners. Dingdang Health enters into service outsourcing agreements with these delivery partners, and the engaged riders provide exclusive delivery services to Dingdang Health.

To handle increased order volumes requiring additional manpower, Dingdang Health partners with third-party carriers to provide non-exclusive delivery services. As of March 2022, Dingdang Health had collaborated with five delivery partners and 21 third-party carriers.

In the chain-store model, enterprises also collaborate with third-party carriers, whose partners dispatch riders to accept orders, thereby meeting the timely delivery needs of individual stores. For instance, Dada Now has partnered with Laobaixing Pharmacy to provide its stores with a range of delivery services, including instant delivery, scheduled delivery, and citywide delivery. It also offers delivery services to other retail enterprises such as Neptune Star, Quanyuantang, Shuyu Civilian Pharmacy, and Yifeng Pharmacy.

Notably, Dada Now also serves as the logistics provider for JD Daojia’s O2O home-delivery pharmacy service and JD Health’s O2O urgent medicine delivery service; in addition to Dada Now, JD Health’s O2O urgent medicine delivery service also utilizes Meituan riders for distribution.

Clearly, in the aforementioned model, O2O enterprises may collaborate with multiple carriers, while carriers (including those affiliated with the platform) provide delivery support to multiple enterprises, thereby achieving “shared” delivery services.

Even platform-based enterprises such as Meituan and Ele.me, despite maintaining large-scale rider teams, still operate their delivery services on a “shared” model—sharing delivery resources with online-to-offline (O2O) services for food delivery, supermarkets, and convenience stores.

Consequently, the division of labor within the O2O sector has become increasingly specialized, making carriers an indispensable component. For a single enterprise, growth in order volume helps reduce delivery costs. Across multiple enterprises, carriers consolidate delivery orders from various platforms, thereby helping to further transform the low-frequency nature of medication purchases into high-frequency interactions, ultimately achieving reduced delivery costs at the industry level.

Flow and Entities Are Interdependent

Among the three major models of pharmaceutical O2O, platform-based models boast large-scale online traffic, chain-store models have extensive offline traffic entry points, and self-operated models combine both online traffic and offline entry points. Currently, the industry predominantly recognizes the traffic advantages of platform-based models. In fact, the integration of online and offline channels in pharmaceutical retail is deepening, and in the context of O2O, these various models are mutually dependent.

On one hand, chain-operated and self-operated enterprises have entered the pharmaceutical O2O segments of platforms such as Meituan, Ele.me, and JD Health to acquire online traffic from public domains. They also generate revenue beyond their own O2O platforms—i.e., outside private-domain traffic—with this income even accounting for a certain proportion of their overall O2O business.

Shuyu Civilian Pharmacy revealed in its first-half 2022 financial report that its online business generated over RMB 360 million in revenue, with third-party O2O platforms accounting for 53% and its self-operated platform contributing 8%. Dingdang Health also noted in its prospectus that the proportion of revenue from third-party platforms within its direct-to-consumer online business has been steadily increasing, reaching 72.6% in the first quarter of 2022.

On the other hand, platform-based O2O models need to cover a large number and wide variety of retail pharmacies to provide more robust fulfillment support; otherwise, with only online traffic and no offline physical entities as a foundation, the fundamental logic of O2O would not hold.

JD Health noted in its financial report that Yaojisong, by co-building a grid-based operational ecosystem with merchants and employing diverse fulfillment methods, provides all-channel, round-the-clock services to users in over 400 cities through partnerships with more than 60,000 merchants. As of March 2022, Meituan Maiyao had partnered with nearly 200,000 offline physical chain pharmacies, which constitute an important component of Meituan’s O2O ecosystem.

If we must discuss the “dependence” among various business models and enterprises, such “dependence” is invariably bidirectional, rather than being merely a unidirectional reliance of other types on platform-based models.

Moreover, from the consumer’s perspective, it is inevitably more convenient to download fewer apps—such as Taobao, JD.com, Meituan, and Ele.me—to access a wider range of daily life services, including shopping, dining, and purchasing medications, than to install multiple vertical-specific apps. On the surface, platform-type apps indeed offer greater convenience.

However, this does not mean that proprietary platforms of chain and self-operated enterprises have lost their significance. In its 2022 annual report, Yixintang revealed that the average transaction value of its self-operated O2O business was 4.17 times that of its third-party O2O business. The differences between self-operated and third-party O2O businesses in terms of drug categories and pricing, user positioning, and delivery timeliness enable the two models to complement each other.

Technological Capabilities Complement Traditional Channels

It must be acknowledged that brick-and-mortar pharmacies remain one of the primary channels for pharmaceutical retail today. Their widespread distribution and proximity to communities facilitate patient management, and over the course of industry development, they have cultivated a base of relatively loyal customers. These are advantages that chain-based O2O models find difficult to replace. At the same time, issues such as low levels of digitalization and the need for improvement in service efficiency and quality at brick-and-mortar pharmacies are equally evident.

Self-operated O2O enterprises like Dingdang Health have applied technological capabilities to pharmacy construction and operations during their development, addressing the shortcomings of traditional brick-and-mortar pharmacies. For instance, they leverage big data and proprietary geo-fencing technology to select locations for smart pharmacies, optimizing network coverage efficiency. They employ intelligent medication selection systems to seamlessly connect user orders with medication pickup and delivery. Furthermore, by using an intelligent order dispatching system that tracks order volumes and workforce availability, they schedule deliveries based on a balance of cost and time, while accounting for complex factors such as weather conditions, thereby ensuring timely medication delivery at lower costs.

As self-operated platforms transition from online to offline operations and are founded on the premise of technology empowerment, they are able to facilitate the deep integration of technological applications and pharmaceutical retail through top-level design.

For traditional chain pharmacies, O2O is merely one aspect of their digital transformation aimed at improving quality and efficiency. Further technological support is required to enhance the services of chain-based O2O models. In this process, platform-based O2O has played a significant role.

Since 2021, Ele.me’s “Little Blue Light” initiative and Meituan’s “Little Yellow Light” initiative have been key measures by these platforms to accelerate the online integration of brick-and-mortar pharmacies. Through strategies such as prioritized traffic allocation and nighttime delivery fee subsidies, these programs partner with physical pharmacies to support 24-hour operations and enable nighttime delivery services.

Soon, “unmanned pharmacies” have become an upgraded version of platforms’ technological empowerment for brick-and-mortar pharmacies. For example, Meituan has partnered with chain pharmacies to create 24-hour smart pharmacies, embedding “unmanned pharmacy” systems into traditional stores. By adopting technologies such as visual recognition and automated control, these pharmacies achieve fully automated management of the entire process from order picking, order consolidation, packaging, to handover, enable end-to-end monitoring of the picking and outbound workflow, and ensure medication safety through systematic verification functions.

For users, these “unmanned pharmacies” enable both in-store self-service medication purchases and O2O delivery. For platforms, they establish a more extensive 24-hour delivery network. For brick-and-mortar pharmacies, they address the challenge of high labor costs associated with nighttime operations. This model exemplifies the complementarity between the technological capabilities of platform-based enterprises and the traditional distribution channels of chain-store enterprises.

Overall, the trend toward deeper integration among the three models is becoming increasingly pronounced, with their distribution systems, channel development, traffic entry points, and technological capabilities exhibiting a state of mutual interdependence.

According to statistics from Menet, by the end of 2021, approximately 200,000 pharmacies had joined O2O platforms, accounting for one-third of the total number of retail pharmacies in China. It is projected that by 2030, the share of O2O sales in the overall brick-and-mortar pharmacy market will rise to 19.2%, with the market size reaching RMB 144.4 billion.

Amid the digitalization trend, omni-channel deployment has become an imperative for retail entities such as brick-and-mortar pharmacies and pharmaceutical e-commerce platforms. The integration and complementarity of various O2O models will further facilitate the overall scale expansion of the pharmaceutical O2O sector.

In a landscape characterized by both integration and competition, what trends will the pharmaceutical O2O sector exhibit in the future? Based on the strategic planning directions of various platforms, the key trends are as follows.

First, expand from pharmaceutical O2O to service-oriented O2O.

In fact, platform-based O2O models have already established such a business structure, integrating offline services such as health checkups and vaccinations into online platforms.

Dingdang Health also stated in its prospectus that, in addition to opening more than 300 new smart pharmacies and hiring thousands of additional riders over the next few years, it plans to invest in and acquire chain pharmacies, testing institutions, and healthcare service providers. This includes investing in or acquiring companies specializing in routine disease screening and rapid diagnostic technologies, on-demand real-time testing service providers, and firms focused on testing facilities and instruments, thereby further expanding its portfolio of healthcare products and services.

Secondly, patient management has truly become a competitive dimension.

Currently, companies are offering services such as internet healthcare, pharmaceutical care, chronic disease management, and health management.

However, from both the supply and demand sides, the true value of these services has yet to be fully realized (except for online consultations and prescriptions aimed at promoting prescription drug sales). In other words, service providers are more focused on driving direct sales conversions, while users have a relatively low perception of the value added by services such as medication reminders and online prescription issuance.

How to Truly Manage Patients and Maintain Long-Term Engagement? Companies Must Not Only Focus on Effectively Building Their Service Processes but Also Transform Them into Competitive Advantages.

Finally, O2O will become a digital marketing channel for specific pharmaceutical products.

Amid the rapid development of B2C pharmaceutical e-commerce, O2O has been able to capture and expand its market share primarily because it meets users’ urgent medication needs. Consequently, O2O drug categories exhibit distinct corresponding characteristics.

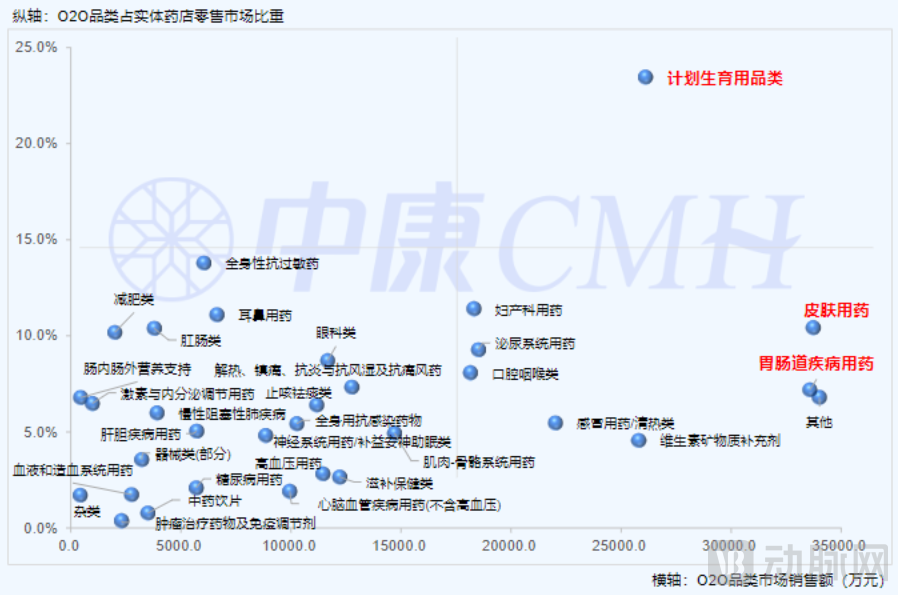

According to pharmaceutical O2O data released by Zhongkang CMH, dermatological medications, gastrointestinal drugs, and family planning products were the three categories with the highest market shares in the second quarter of 2022. In addition, seven categories—including systemic antihistamines, otolaryngological medications, and proctological drugs—accounted for more than 10% of the brick-and-mortar pharmacy retail market. In terms of O2O’s contribution to the brick-and-mortar pharmacy retail market, urgency and privacy remain the primary characteristics of consumer medication behavior.

O2O Pharmaceutical Category Share and Contribution, Source: Zhongkang CMH

O2O platforms have brought varying levels of online exposure to brick-and-mortar pharmacies, while also creating more visibility opportunities for pharmaceutical products and even pharmaceutical companies themselves, thus becoming an important channel for digital marketing by pharma companies. In particular, O2O pharmaceutical categories have distinct characteristics, and when combined with more detailed transaction data, pharmaceutical companies can leverage O2O platforms to conduct more precise digital marketing.

In 2022, Zhiyun Health, which operates in the same internet healthcare sector as Dingdang Health, also went public. Both companies have undergone a similar trajectory in their respective niche markets: a frenzy of startups entering the space, followed by the collapse of early movers after their business models were proven unsustainable, and then iterative refinement of their own models amidst uncertainty until they persisted long enough to reach an IPO and embark on a new phase.

In the view of Jiang Min, a partner at SoftBank China Capital, China’s digital healthcare sector as a whole is still in the early stages of commercialization. Dingdang Health has broader market potential, and there are high expectations for it to serve a wider population with superior digital healthcare products and services.

As part of digital healthcare, the positioning and value of the three major O2O industry models have become increasingly clear. Compared with the uncertainties of the past, the current market demonstrates greater certainty in terms of policy, competitive landscape, and technological application. Stakeholders across these three models need to foster the overall growth of the industry through a dynamic of competition and cooperation.