Lu Gang: A New Journey and Mission Beyond the Capital Winter

Recently, during the 2022 China International Fair for Trade in Services, the Ministry of Industry and Information Technology, the National Health Commission, and the Beijing Municipal People’s Government co-hosted the “Conference on Healthcare and Industrial Technological Innovation Services” at the China National Convention Center. Mr. Lu Gang, Partner at Legend Star, attended the Investment and Financing Forum and delivered a keynote speech titled “New Journey and New Mission in the Post-Capital Winter Era.”

From 2021 to 2022, the once-booming healthcare investment sector cooled rapidly to a winter-like state within just over a year, with numerous flagship projects either breaking their issue price upon IPO or facing delays. Venture capital firms, which had previously flocked to the healthcare sector—viewing it as a “long slope with thick snow” and treating it as a core portfolio allocation—have demonstrated considerable risk aversion and adopted a cautious, wait-and-see approach.

Lu Gang believes that, despite being at a cyclical low point, as long as investors remain convinced that the healthcare industry still offers a long runway with substantial returns, investment firms can fully adopt a more proactive mindset to seize opportunities and engage in innovation. This is a“Issues of Faith”; and whether one can persist in shaping long-term value and endure short-term hardships, this is a"Strategic" Issues. A long-termist needs to have sufficient “faith in what they believe in.”Underlying Rationaleand adopt appropriate “flexible strategies” to make sound choices and engage effectively. As for Legend Star, its understanding of the future is that “China’s new healthcare ecosystem is rapidly taking shape. If we can align with long-term trends and clearly recognize the historical stage in which we find ourselves, we will inevitably have the confidence to uphold our new mission and embark on a new journey.”

Below is the edited transcript of Lu Gang’s speech, shared for your reference:

From Boom to Winter in Healthcare Investment: How to Reassess the Former “Faith”?

Hello everyone. The topic I am sharing today is “A New Journey and New Mission in the Post-Capital Winter Era.” There are two key phrases here. The first is “in the post-capital winter era.” It is widely acknowledged that healthcare investment and financing are currently in a downturn. So, where do the future development opportunities for the healthcare industry lie? What will be the logic and opportunities for innovation? This brings me to the second key phrase, “a new journey and new mission,” which will be the focus of my presentation today.

Let me first introduce Legend Star. Since 2008, we have focused on investing in and incubating science and technology innovation projects, primarily engaging in angel investment and non-profit entrepreneurial incubation. Over the past decade-plus, we have invested in more than 400 companies, covering numerous sectors such as intelligent technology, healthcare, chips, and new materials, among which several standout enterprises have emerged. In the past ten years, we have consistently achieved strong rankings in major industry evaluations. Additionally, the Legend Star Entrepreneurial CEO Training Program has been running for 14 years, cultivating over 1,100 entrepreneurial CEOs through a combination of public welfare initiatives and practical training. While striving to excel in entrepreneurial incubation, we have also drawn valuable practical experience from the entrepreneurial journeys of many “Star Friends.”

Drawing on over a decade of accumulated investment experience and observations of cyclical shifts, we have gradually developed our own understanding and strategic approach to the symbiotic relationship between venture capital and entrepreneurship, as well as strategies for navigating market bubbles and downturns.

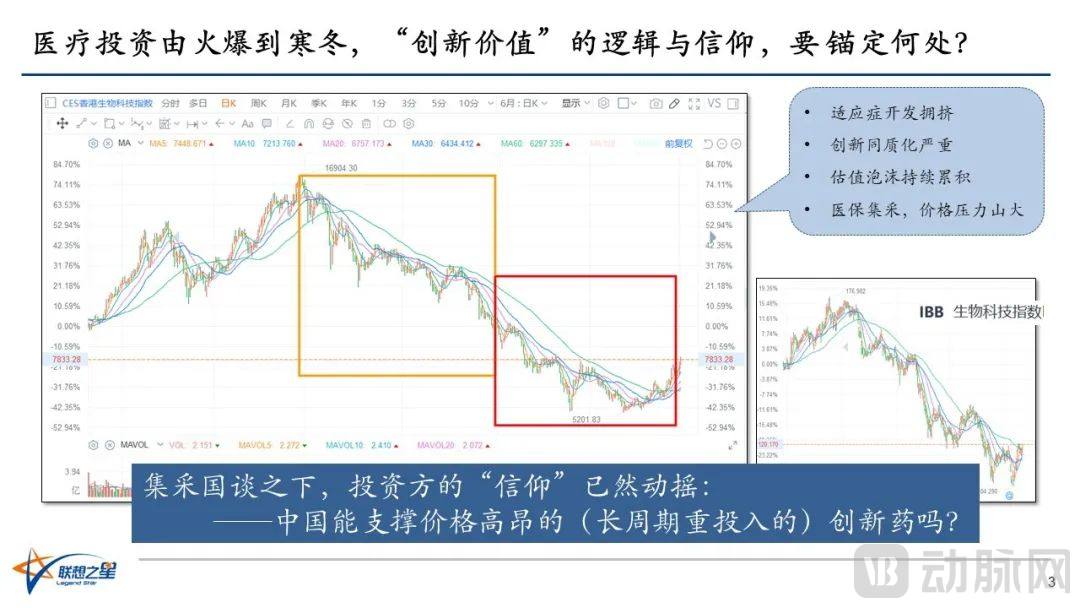

Reviewing the changes in investment, financing, and market valuations within the healthcare sector over the past year, with the HKEX Biotech Index as a reference, reveals that after reaching a peak in July 2021, the index experienced two significant downturns, as highlighted by the boxed areas in the chart. At their lowest point, the stock prices of most leading companies had fallen to 30% of their previous highs. The systemic, deep declines and weak rebounds indicate an exceptionally harsh winter. The breadth of this impact has spread from the secondary market to the early stages of the primary market, affecting nearly the entire healthcare sector, ranging from biopharmaceuticals to medical devices and healthcare services.

ForReasons for the Decline, a consensus has been reached that the primary cause is none other thanCrowded Indication Development, Severe Homogenization of Innovation, and High Valuation Bubbles. Since the establishment of the National Healthcare Security Administration, successive rounds of centralized procurement and national price negotiations have not only lowered drug prices and promoted more efficient use of healthcare insurance funds, but also imposed significant market and financing pressures on pharmaceutical and medical device companies.

This raises a soul-searching question: Can the Chinese market support high-priced innovative drugs that require long development cycles and substantial investment?In the healthcare sector, can investing in high-risk innovations still yield commensurate returns? The once-unshakable faith in long-term, high-resilience sectors has, inUncertain Outlook, Lack of Confidenceamid the decline in valuations, has already begun to waver.

Standing at the present moment, we are already in the midst of a harsh winter; it is of little value to merely proclaim its arrival. Instead, it may be more meaningful to look back at the trend-based signals that foreshadowed the onset of this winter.

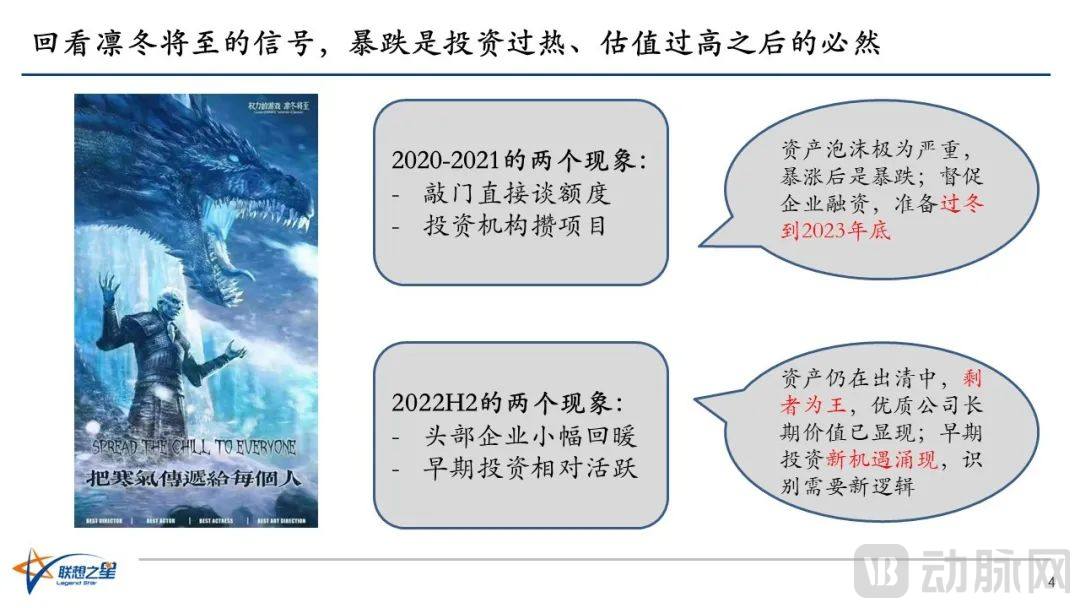

In 2020 and 2021, we observed two phenomenaFirst, investment fervor is running high. Institutions are knocking on doors to directly inquire about remaining investment quotas, driven more by the fear of missing out than the fear of making wrong bets; securing an allocation brings peace of mind. This phenomenon is not limited to pre-IPO projects; early-stage ventures with attractive profiles are also heavily sought after, making fundraising relatively easy. Second, there is a rising trend of “project packaging,” particularly in sectors benchmarked against hot tracks in the United States—such as ophthalmology, gene therapy, cell therapy, and brain science—where competition is relatively less intense. By assembling a team with impressive credentials and creating a polished pitch deck, it becomes easy to secure financing. Notably, well-known investment firms are often among the participants in these packaged deals.

What does this indicate? The frenzied rush for projects will inevitably lead toRapid Expansion of Asset Bubbles, chasing trends and assembling teams will inevitably lead toSpeculative Entrepreneurshipthe emergence. This often indicates that market highs are difficult to sustain.Plummeting valuations and a harsh winter are the inevitable aftermath of excessive valuations and rampant speculation, a cyclical shift that has occurred repeatedly in other sectors.

At the end of 2020, we began urging our portfolio companies to accelerate their fundraising efforts, emphasizing that valuation levels were secondary. What mattered more was securing sufficient capital while the financing window remained favorable, thereby ensuring adequate resources for wintering-over strategies. A sharp surge is highly likely to be followed by a steep decline; although we could not predict when or how it would occur, its arrival was inevitable. At that time, our preliminary assessment indicated that companies should prepare enough cash reserves to last until at least the end of 2023.

In the second half of 2022, two phenomena gradually re-emerged.: First, valuations of leading enterprises have shown a slight rebound; second, early-stage investment has demonstrated relatively higher activity compared to mid- and late-stage investments, with many large late-stage funds establishing dedicated early-stage funds.

Do these two phenomena indicate that the adjustment has been fully realized and an inflection point is imminent? I believe that leading companies in certain niche sectors now offer long-term investment potential, as their valuations are attractive relative to their intrinsic value; however, on the whole, “Do Not Mistake a Rebound for a Reversal”. The accumulated homogenized assets from the previous period remain severely oversupplied, and clearing this excess will still take time. When a significant number of companies are forced into “liquidity paralysis,” or when frequent fire-sale disposals of pipeline assets—a rather “bloodthirsty” phenomenon—become commonplace, that may well mark the turning point. High-quality companies that survive the winter can relatively easily achieveThe Last Man Standing。

History always repeats the same logic in different forms: high-quality companies and opportunities often emerge from harsh winters, and this time should be no exception. China’s healthcare industry is also nurturing a new journey amid the current downturn.

China’s “Long Slope with Thick Snow” Track Cannot Be Simply Benchmarked Against Europe and the United States

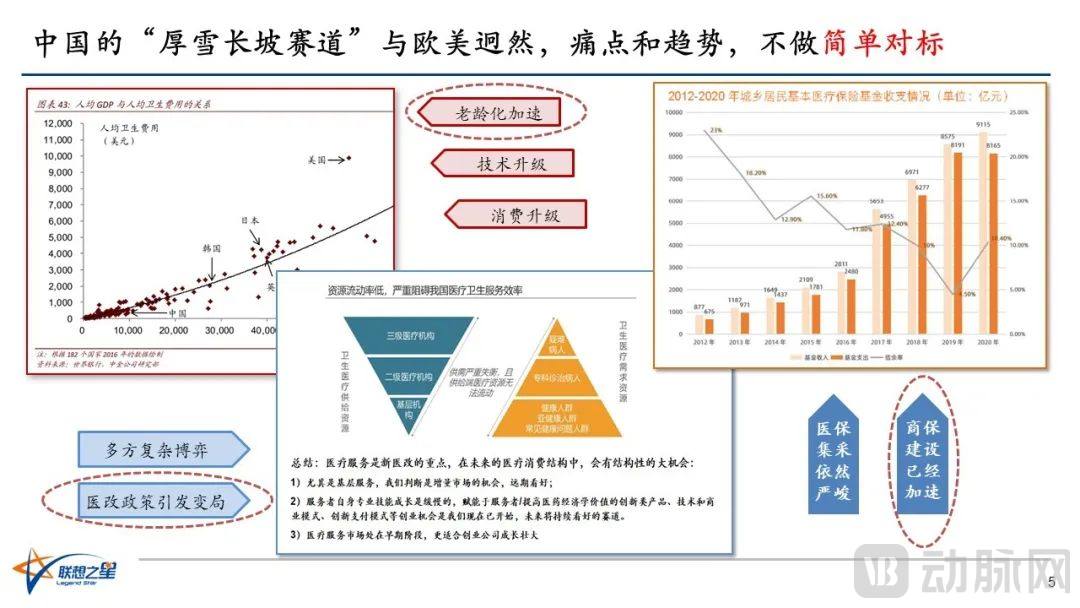

To look ahead to the new journey, we must understand the past and grasp the characteristics of China’s industrial environment.Unique Underlying CharacteristicsI have reviewed numerous business plans from startups that frequently benchmark themselves against technological advancements and market trends in Europe, the United States, and Japan. However, I believe that while China’s healthcare sector is indeed a “thick-snow, long-slope” track, its underlying characteristics give rise to pain points and trends that are markedly different from those in Western markets. Simple benchmarking may lead to predicaments. In the past, certain sectors fell into traps of inflated valuations, severe homogenization, and difficulties in commercial implementation precisely due to such simplistic benchmarking.

First,China Faces Three Major Realities: Accelerating Aging, Technological Upgrading, and Consumption Upgrading. Take the accelerated aging of the population as an example. The aging challenge faced by a country with 1.4 billion people, particularly the urgent pressure stemming from the “accelerated” aging trend following decades of the one-child policy, is unprecedented in any other nation. Is it highly feasible to emulate the European and American systems to address this issue? It may be quite difficult.

Second,China’s Healthcare Ecosystem Faces Multifaceted and Complex Strategic Interactions, including insufficient supply and uneven distribution of medical resources, particularly the previously existing distorted practice of "subsidizing healthcare with drug profits."Healthcare Reform Policies Are Triggering a Paradigm Shift, which is also a unique challenge faced by China.

Third,Payment resources are insufficient and unhealthy, or have yet to achieve a virtuous cycle., is one of the challenges facing China. Public health insurance accounts for 90%–95% of healthcare payments in China; while this dominant share underscores its overwhelming predominance, the relative scarcity of public insurance resources is an indisputable fact. Although the development of commercial health insurance is accelerating, its absolute base remains small, making it difficult to shoulder significant responsibility in the short term. In this regard, China’s situation differs markedly from that of Europe and the United States.

Therefore, by avoiding simplistic benchmarking, we are compelled to delve deeper into this issue and recognize that the fundamental characteristics of China’s “long-slope, thick-snow” sectors differ significantly from those in Europe and the United States. Consequently, when addressing pain points and assessing trends, we must naturally develop our own logical frameworks and understanding.

Looking back, we began monitoring the sector in 2008 and embarked on early-stage healthcare investments in 2010, establishing a broad portfolio by today. A review of our early-stage investment logic and practices offers insights into the trends of healthcare innovation in China, and provides an opportunity to share our perspectives and recommendations on future developments.

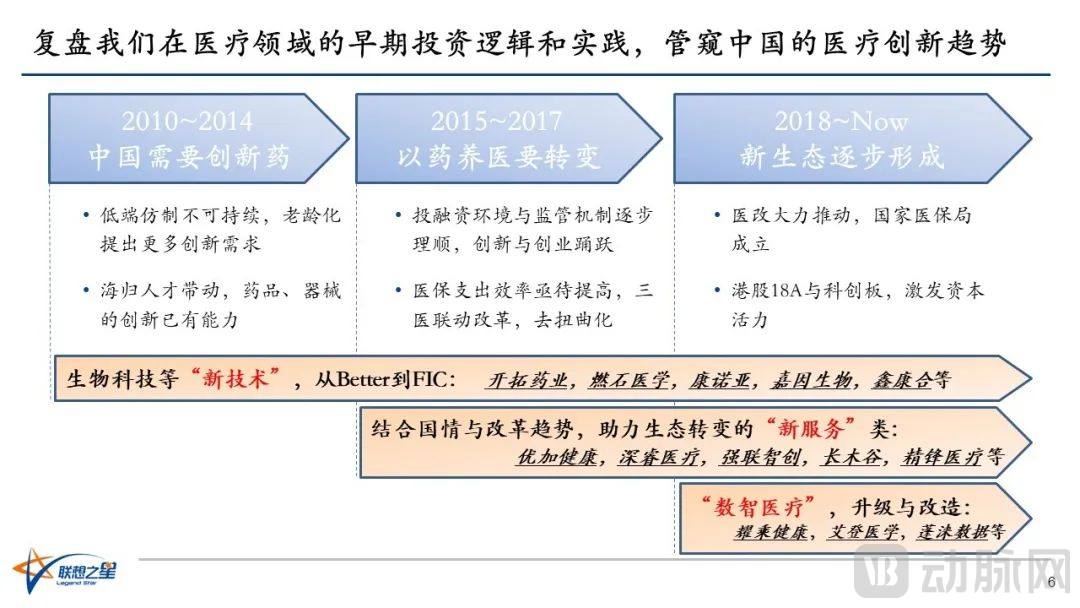

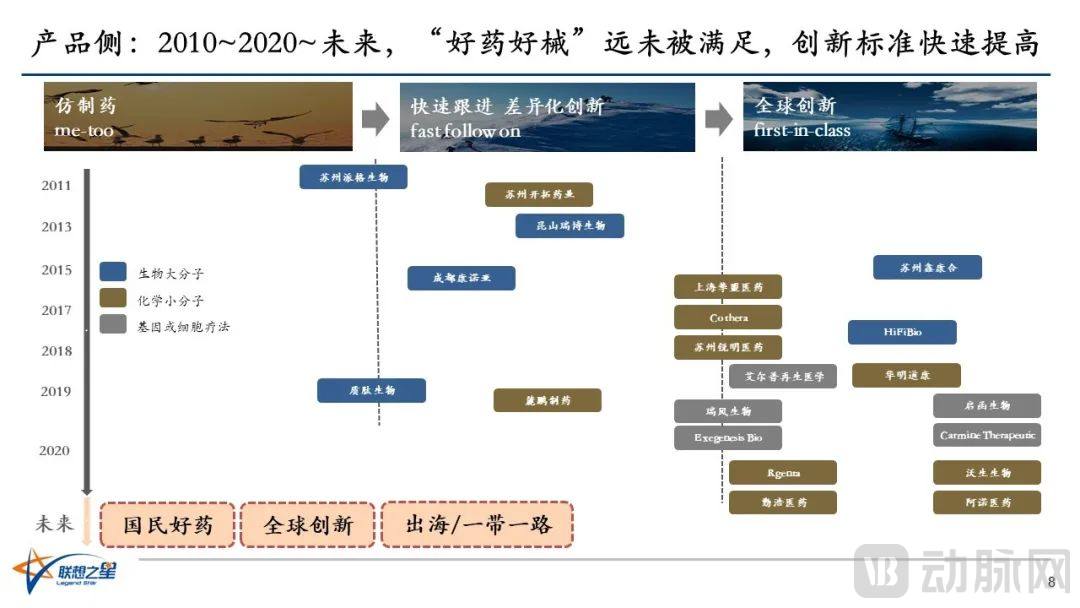

2010–2014In China, low-end generic drugs are ubiquitous and highly profitable. However, relying solely on low-end generics is unsustainable. The accelerating aging population has also created greater demand for product innovation, at a time when the supply of innovative drugs is severely insufficient, necessitating new variables to drive change. What are these new variables based on? They stem from the pioneering efforts of a cohort of highly skilled overseas-returnee pharmaceutical professionals who embarked on arduous entrepreneurial journeys, enabling us to begin achieving upgrade-oriented innovations in drugs and medical devices. Consequently, our strategy at the time was centered around “new technologies,” starting with me-better approaches, including innovative drugs, novel diagnostic technologies, and new medical devices. Over time, the requirements for new technologies have gradually escalated from me-better standards to best-in-class and first-in-class levels. Among the dozens of companies we invested in over several years, three to five have successfully gone public. Our investment strategy in the “new technology” sector has continued to this day, constantly evolving alongside industrial advancements.

In 2015,We have observed shifts in two environmental factors that present new opportunities. First, the financing and investment landscape and regulatory mechanisms have been progressively streamlined, fostering vigorous innovation and entrepreneurship. Second, the coordinated reform of healthcare, medical insurance, and pharmaceuticals (the “Three-Medical Linkage”) has clarified its direction and begun to correct market distortions. In this context, we believe that to meet the demands of an aging population, China’s healthcare industry requires not only new technologies but also innovative medical services. Given China’s unique national conditions, challenges, and reform trends, a significant opportunity distinct from those in Europe and the United States is emerging: namely, new service-oriented opportunities that facilitate the transformation of the healthcare industry ecosystem. Accordingly, we defined and established a strategic focus on “New Healthcare Services,” and began investing in a portfolio of related companies. To this day, this sub-sector remains a key area for our innovation-driven growth.

So2018 to presentWhat stage is the healthcare industry in? I believe it isThe Stage of Gradual Formation of the New Ecosystem, that isFrom an ecosystem of “funding healthcare through drug sales” to one of “sustaining healthcare through service provision”. The landmark event was the establishment of the National Healthcare Security Administration in May 2018, which tackled entrenched industry problems by starting from the payment side and lowering drug prices through centralized procurement. In addition, the launch of Chapter 18A of the Hong Kong Stock Exchange and the STAR Market fully stimulated the vitality of capital and innovation-driven entrepreneurship. In this context, we have become more bold in our investments. In the area of new services, we have further increased our commitment to the development of digital-intelligent healthcare and the upgrading and transformation of traditional industries, while also investing in a batch of technology enterprises that align with development trends and possess strong innovative capabilities.

Forging a New Ecosystem for the Future of Healthcare

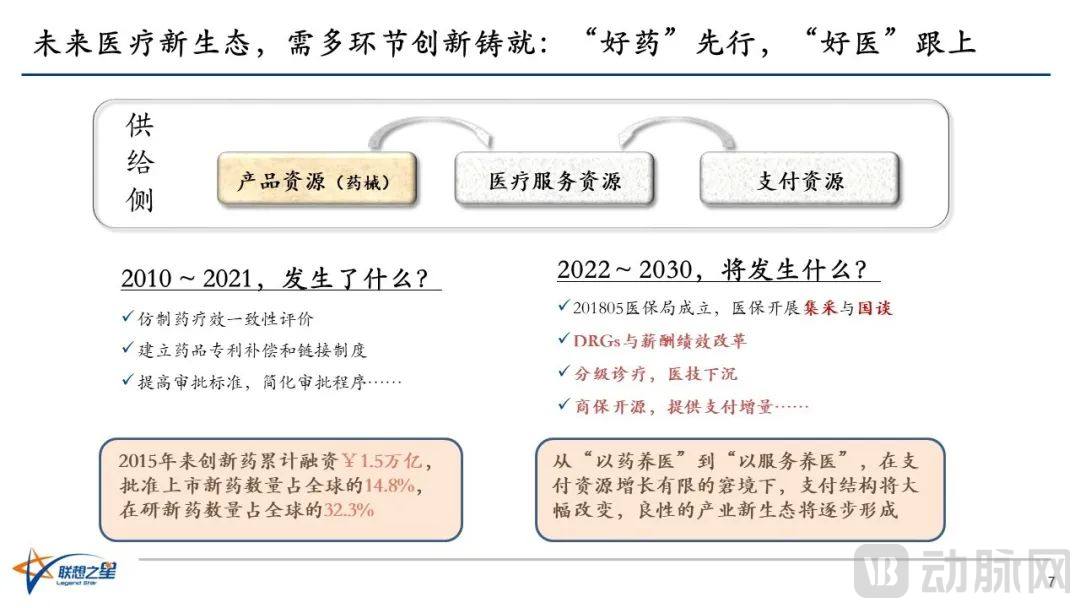

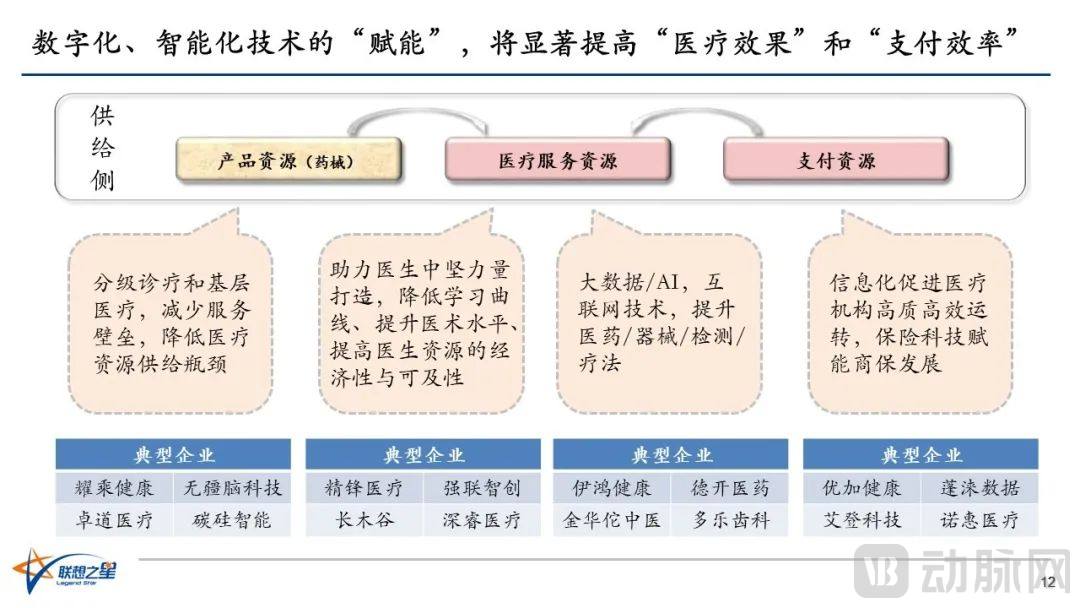

Building on the case study of Legend Star’s evolving investment strategy, let us zoom out further to explore the core issues within China’s healthcare ecosystem.For a long time, the core pain point of China’s healthcare system has not lain on the demand side, but rather on the supply side—where insufficient resources and low efficiency have constrained its capacity to meet the robust demands of society and the public.

Let us examine the key components of the supply side, which essentially consist of three major stakeholders: products, payment, and medical services. Product resources include pharmaceuticals and medical devices; payment resources encompass basic medical insurance and commercial health insurance; and medical service resources comprise hospitals, physicians, and various healthcare institutions. Product and payment resources reach end-users to meet their needs through the core link of medical services. This fundamental relationship enables the healthcare industry to achieve a complete cycle and sustainable development.

2010 to 2021, what has happened? In terms of policy, regulatory measures favorable to the rapid enrichment of product resources have been intensively introduced and advanced. These include the consistency evaluation of therapeutic efficacy for generic drugs, the establishment of a drug patent compensation and linkage system, the raising of approval standards, the simplification of approval procedures, and the accelerated market launch of high-quality drugs and medical devices. As a result, since 2015, China’s innovative drug sector has accumulated RMB 1.5 trillion in financing; approved innovative drugs account for 14.8% of the global total, while drugs under development represent 32.3% of the global pipeline—a significant breakthrough and achievement.

Today, we are witnessing significant price reductions for many pharmaceuticals and medical device consumables. Volume-based procurement negotiations have delivered tangible benefits to the public, enabling payers to purchase more cost-effective drugs and devices with greater efficiency. An important backdrop to this trend is that over the past decade, vigorous entrepreneurial activity and substantial capital investment have spurred high levels of innovation among enterprises, leading to marked improvements in the quality and sophistication of pharmaceutical and medical device products, a continuous expansion of product categories, and even “excessive crowding” in certain segments. In short, the efforts of the past decade have prioritized the availability of high-quality medicines, initially addressing constraints in product supply and alleviating the relative strain on medical insurance fund resources.

Then2020 to 2030What Will Happen? Looking back at the establishment of the National Healthcare Security Administration (NHSA) in 2018, which launched centralized volume-based procurement and national reimbursement drug price negotiations, this served as a significant signal indicating China’s commitment to improving efficiency throughout the payment process. This necessitates reforms in hospital compensation and performance management, implementation of tiered diagnosis and treatment systems, and the decentralization of medical technical resources. While effectively managing existing resources, it is essential to expand new sources; commercial health insurance must assume responsibility for revenue generation by providing incremental sources of payment funding.

ThereforeIn the transition from “subsidizing healthcare with pharmaceuticals” to “sustaining healthcare through services,” payment structures will undergo significant adjustments amid the constraint of limited growth in payment resources, gradually fostering a healthy new industrial ecosystem.To truly keep pace with the “acceleration” of aging among 1.4 billion people and avoid major mishaps, this “gradual formation” must inevitably also have an “acceleration.”

To achieve acceleration, the enthusiasm and creativity of doctors and hospitals are essential prerequisites. Therefore, “good physicians” must keep pace; otherwise, even the best drugs will have limited significance. “Good physicians” not only refers to cultivating skilled doctors capable of addressing complex and refractory diseases, but also entails optimizing the distribution of healthcare resources, enabling high-quality medical care and expertise to reach grassroots levels, thereby benefiting a broader population. Of course, among theseHow to protect and incentivize the enthusiasm of doctors and hospitals will be the top priority and the decisive factor determining the success or failure of healthcare reform.。

Guided by these trend assessments and strategic rationales, Legend Star has made continuous investments on the product side over the past decade. Taking innovative pharmaceuticals as an example, its investment focus has gradually expanded from “Better” and “Fast” to “Best” and “First,” reflecting a steady increase in the degree of innovation. The continuous iteration of strategies and standards is underpinned by industrial development and the evolution of market opportunities.

From the perspective of today’s so-called “winter moment,” China’s demand for high-quality drugs and medical devices remains far from satisfied. The need to rapidly raise innovation standards is not about pursuing innovation for its own sake, but rather because only innovation can meet these demands. The current “winter” has been primarily driven by homogeneous overcrowding, excessive capital bubbles, and the passive position imposed by volume-based procurement. However, these cyclical factors have not altered the fundamental long-term trend characterized by a “long slope and thick snow.” How, then, should we understand future opportunities? I have identified three key words:

First,National Trusted Medicine, namely cost-effective, high-efficacy drugs suitable for the Chinese population, represents a significant opportunity; second,Global InnovationIt is also a major opportunity; third, going global, especially similar toBelt and Road InitiativeYes, expanding into middle- and lower-income countries. Since China has developed high-quality medicines capable of serving its 1.4 billion people, why not export them to nations with similar healthcare scenarios or consumption levels, thereby improving their medical and public health environments? China’s pharmaceutical industry is ready to go global. These represent three opportunities on the product side.

Digital Intelligence Empowers the New Healthcare Ecosystem

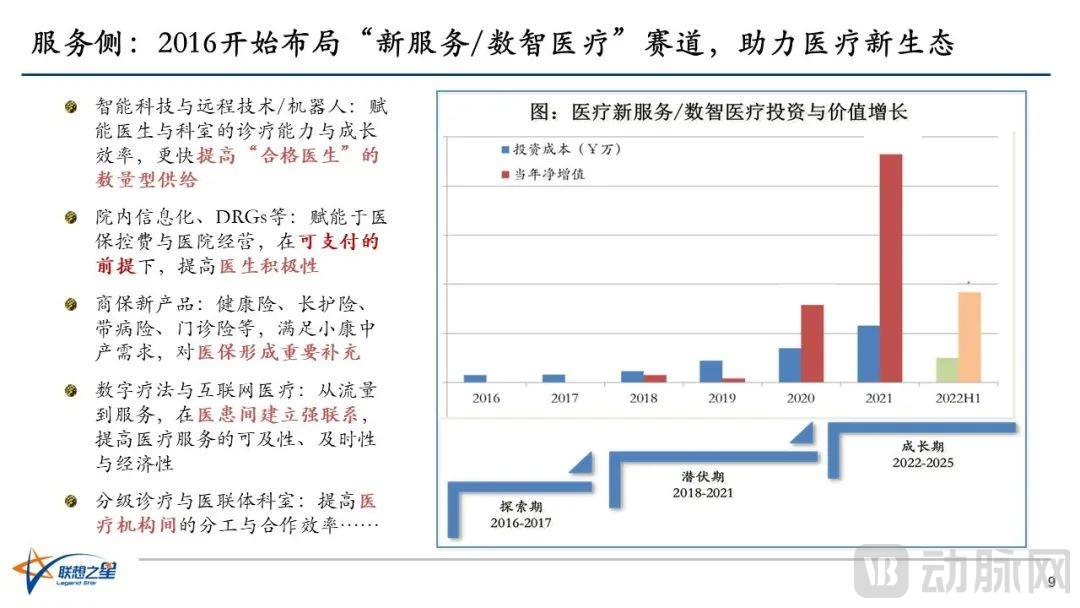

On the service side, it is even more important to highlight China’s opportunities and distinctive characteristics.Legend Star made it clear in its investment strategy as early as 2016 to begin positioning itself in, or exploring, the new services/digital-intelligent healthcare sector., we recognize that China’s future medical ecosystem must feature not only high-quality drugs but also superior healthcare services. Key pain points and critical needs we focus on include how to increase the number of qualified physicians, how to enhance physician motivation within limited payment resources, and how to establish strong, positive connections between doctors and patients. Our early-stage investment strategies and portfolio allocations in these areas have progressed through phases of exploration and incubation, and are now gradually entering a growth stage.

The blue bars in the chart above represent our annual investment amount in the new healthcare services and digital-intelligent healthcare sector, while the red bars indicate the net value added in each respective year. Can this sector truly deliver high-growth returns? Although I have omitted the specific figures, it is evident that the value addition is gradually accelerating. To illustrate our confidence and conviction, let us examine case data from our investment portfolio: After a period of earlier impetuousness and hype, digital-intelligent healthcare and new healthcare services have begun to achieve commercial implementation, with service scenarios continuously expanding and their empowerment of the new industrial ecosystem starting to drive progress. Even amid the current “financing winter” sweeping the entire healthcare industry, the enterprise value within this sector continues to grow rapidly, and an increasing number of investment institutions that share our consensus are stepping up their efforts.

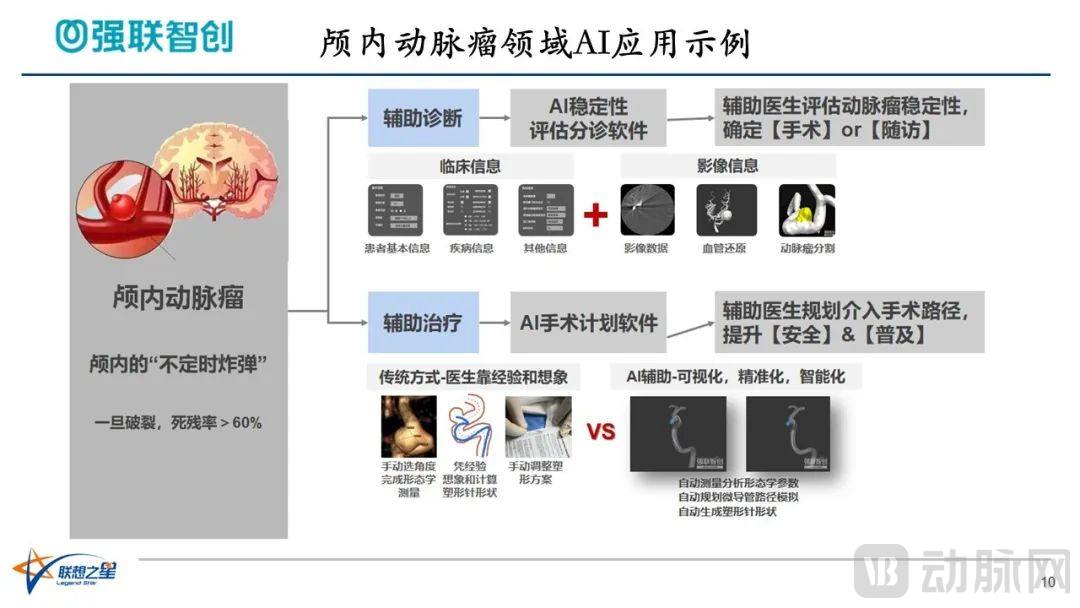

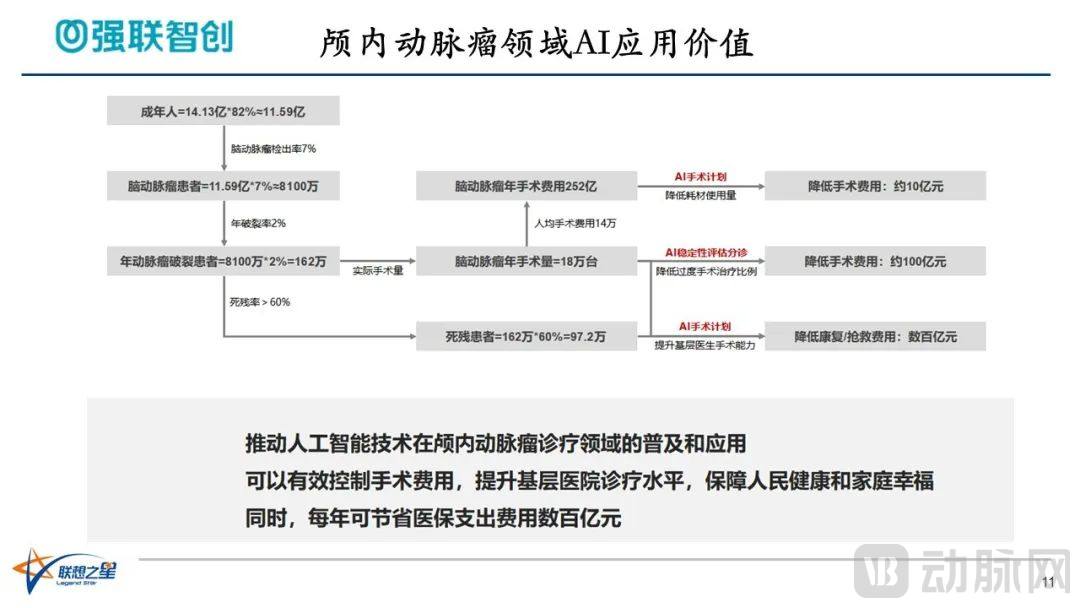

Regarding how to adapt to the Chinese context and demands to explore innovative pathways, let us take our portfolio company, Qianglian Zhichuang, as an example. The incidence of stroke in China is rising, particularly strokes caused by aneurysms—often referred to as “ticking time bombs”—where there remains a significant unmet need. With a disability and mortality rate as high as 60%, each stroke patient requires intensive care from one or even half a family member, severely impacting the family’s quality of life and substantially increasing their financial burden. Qianglian Zhichuang leverages AI technology to enhance the industry’s intelligence level from two perspectives. First, it assists in diagnosis, helping physicians evaluate whether surgical intervention is necessary and enabling early elimination of this “ticking time bomb.” Second, it supports treatment by assisting physicians in planning interventional surgical pathways to reduce operative risks. In essence, it helps more mid- and primary-level physicians master surgical techniques, thereby benefiting a larger patient population and preventing the disease before it manifests. This aligns with one of ourUniversal Innovation Logic, which is to increase the supply of qualified physicians and improve access to high-quality medical care.

What is the actual magnitude of the “commercial value” and “social value” generated by Qianglian Zhichuang? A simple calculation provides some perspective: China has approximately 1.159 billion adults, among whom up to 1.62 million patients suffer from ruptured aneurysms each year. By leveraging AI, direct medical expenditures can be reduced by tens of billions of yuan. Given the relatively limited resources of the national healthcare insurance system, the early application of such technologies in these areas can not only lower public health system costs but also significantly alleviate the non-medical burdens on families and society. From this more comprehensive perspective, it becomes clear that innovative digital-intelligent healthcare does more than just capture commercial value; more importantly, it creates positive spillover effects that generate substantial social value. For initiatives that benefit patients’ families, mid-level physicians and healthcare institutions, and healthcare insurance payers—and even help governments improve local health standards—is there really a need to worry about market demand or volume-based procurement?

There are many more such technologies and companies. Today,The “empowerment” of digital and intelligent technologies will significantly improve “medical outcomes” and “payment efficiency.”. Over the course of many years of investment, we have evolved from “shooting in the dark” to “aiming with precision,” and today, we have further consolidated our investment themes. We have invested in several typical high-growth projects across three key areas: product resources, medical service resources, and payment resources, thereby forming a clearer understanding of innovation opportunities with Chinese characteristics. Our steadfast belief in long-duration, high-resilience sectors stems from this experience.

Looking back on the past fifteen years, China’s healthcare industry has focused relatively more on product-side development, thereby providing greater access to high-quality pharmaceuticals and medical devices today. Moving forward, we aim to build a new healthcare ecosystem that is better suited to China’s unique characteristics and supports healthy, sustainable growth. We have gained valuable insights in this field and are eager to share them today, with the hope of collaborating with all stakeholders to jointly realize this new ecosystem. Amidst the current capital winter, we see not only challenges but also renewed mission and hope.

That concludes my presentation today. Thank you all!