CVS Health Acquires Signify Health for $8 Billion to Accelerate Home-Based Care Strategy

CVS Health

Pharmaceutical Retailers

On September 6, CVS Health (hereinafter referred to as “CVS”), renowned for its chain pharmacies, announced the acquisition of Signify Health at $30.5 per share in cash, with a total transaction value reaching $8 billion (approximately RMB 55.8 billion), emerging as the ultimate winner of this acquisition battle. This represents a significant premium over Signify Health’s previous market capitalization, which stood at just $6.6 billion in late August.

The bidding war was fierce—CVS’s rivals at the table included giants such as Amazon and UnitedHealth. In late August, insiders revealed that UnitedHealth had submitted the highest bid, offering more than $30 per share, with Amazon close behind. Unexpectedly, it was CVS that ultimately emerged victorious.

This marks the second clash between CVS and Amazon in a short period. Of course, Amazon emerged victorious last time—acquiring One Medical for $3.9 billion in July, with CVS as one of its rivals.

With this acquisition, CVS Health has not only scored a strategic victory but also enhanced its user reach through the home care network provided by Signify Health. After years of effort, the once-familiar label of “chain pharmacy” may no longer be apt for CVS Health, as a vast healthcare empire has begun to take shape.

CVS’s latest acquisition target, Signify Health, is a healthcare services company. In February 2021, Signify Health went public on the New York Stock Exchange, with its stock price surging on the first day of trading and its market capitalization reaching $7 billion. However, just one year later, its market value had dropped by more than half.

Signify’s core competitiveness lies in its nationwide healthcare service network, which spans all 50 U.S. states and comprises approximately 10,000 physicians, nurses, and physician assistants. These primary care providers regularly conduct home visits to enrolled patients, delivering comprehensive medical and health services.

Beyond medical care, these service providers also address patients’ social and behavioral needs by connecting them with appropriate follow-up care and community resources, thereby tackling the social determinants of health at their root. Issues such as food insecurity, transportation barriers, social isolation, and poverty fall within their scope of focus. Statistics show that Signify Health has established partnerships with more than 600 medical and social care organizations and 200 community-based organizations.

According to the financial report, in 2021, Signify provided approximately 1.9 million home service visits to customers.

To mitigate the impact of the COVID-19 pandemic on in-home visits, Signify Health introduced virtual visits, primarily conducted via video, in 2020. Statistics show that these virtual visits accounted for more than 38% of total visits in 2020. However, as social distancing restrictions were eased, the proportion of virtual visits gradually declined to 17% in 2021.

Delivering value-based healthcare is Signify’s original vision, with data serving as the critical foundation. According to its introduction, each visit can generate a comprehensive report capturing up to 240 data points. As of 2021, its database contained data on approximately 40 million members.

These data, in turn, form Signify’s proprietary decision support and analytics tools, providing guidance on a range of care plans—including clinical workflows and home-based diagnostic screening—to partner physicians and customers (such as healthcare providers, governments, and health management programs), while helping them manage services throughout the patient care journey.

From Signify’s business perspective, this represents a natural “traffic gateway.” It not only helps CVS Health achieve its goals in home care and managed health management, but also enables it to reach more users through differentiated services, establish broader and deeper connections with community resources, and organically integrate these efforts with its nearly 10,000 stores across the United States, thereby forming a robust grassroots service network.

This serves as an excellent complement to the CVS HealthHUB innovative business model proposed by CVS in 2019. The essence of this initiative is to bundle CVS’s existing business formats and service capabilities, establishing diversified brick-and-mortar stores that integrate convenient medical care, chronic disease management, health management, and the sale and services of traditional pharmacy products. This approach aims to enhance user stickiness and drive further service engagement.

This concept has expanded rapidly since its launch. The 2021 annual report revealed that CVS converted approximately 300 stores into CVS HealthHUBs in that year alone, providing integrated services to users within their coverage areas.

Signify will leverage CVS’s resources to achieve more rapid expansion. As planned, Signify aims to increase its annual home visits from 1.9 million to 2.5 million this year. CVS’s resources will clearly help it better accomplish this goal.

Emerging victorious in fierce M&A competition is no easy feat, especially when the rival is a deep-pocketed giant like Amazon, which is determined to make significant inroads into the healthcare sector. Not long ago, reports emerged that Amazon plans to partner with local small and medium-sized pharmacies in Japan to establish a prescription drug sales platform, following the legalization of electronic prescriptions in the country next year. Patients will be able to obtain prescriptions and purchase medications online through participating pharmacies, with Amazon providing delivery services. Additionally, the platform will offer patients online guidance on proper medication usage.

Amazon has been seeking breakthroughs in the healthcare sector in recent years, sequentially launching Amazon Care and Care Medical, which primarily provided home-based services to employer clients. However, the response to these services fell short of expectations, leading to the announcement of their closure at the end of August this year. This may well be a key reason behind Amazon’s interest in acquiring Signify Health.

Amazon also acquired PillPack and built Amazon Pharmacy on that foundation, creating direct competition with CVS, which originated as a chain pharmacy. Furthermore, Amazon recently completed its acquisition of One Medical, once again outmaneuvering CVS. The competitive pressure Amazon is exerting on CVS is evident.

With the acquisition of Signify Health, CVS has finally scored a win. To cope with intense competition, CVS is also seeking breakthroughs in other areas. During its second-quarter earnings conference call, CVS executives stated that primary care would be the focus of its future expansion efforts.

Perhaps it won’t be long before we see giants like CVS Health and Amazon lock horns again.

If you still view CVS as merely a chain pharmacy, it may be time to reconsider. In fact, CVS has undergone a significant transformation to stay competitive. Today, CVS has evolved into a multi-sector health solutions provider.

According to the latest financial report, CVS currently employs up to 300,000 people. In addition to its 9,900 brick-and-mortar pharmacies, it operates nearly 1,200 MinuteClinic convenient care clinics, solidifying its status as an undisputed giant in the chain pharmacy industry. Furthermore, CVS serves approximately 110 million PBM (Pharmacy Benefit Management) members and provides professional services to over 1 million patients annually. The company also has an insurance business that covers around 35 million people nationwide, including participation in public programs such as Medicare Advantage and Medicare Part D prescription drug plans.

Based on different business lines, CVS is internally divided into four major segments: Health Care Benefits, Pharmacy Services, Retail and Long-Term Care (LTC) Pharmacies, and Corporate/Other.

Healthcare Benefits is the youngest division of CVS, primarily providing comprehensive insurance-integrated services to a diverse clientele that includes employers, individuals, college students, part-time workers, health plans and healthcare providers, government entities, and labor organizations.

These services are divided into commercial insurance and government-sponsored insurance. The commercial insurance segment covers a range of health plans, including Point-of-Service (POS) plans, Preferred Provider Organizations (PPOs), Health Maintenance Organizations (HMOs), indemnity benefits, and Health Savings Accounts (HSAs). The government-sponsored insurance segment offers Medicare Advantage, Medicare Supplement, and prescription drug plans in select regions, and participates in various public insurance programs such as Medicaid and the subsidized Children’s Health Insurance Program (CHIP).

The Pharmacy Services division provides clients with comprehensive PBM solutions, broadly categorized into three types: solution-based services, value-added services, and management services. Solution-based services involve the design and management of PBM programs. Value-added services include prescription management, mail-order pharmacy services, specialized pharmaceutical services for rare and complex diseases, infusion therapy, and clinical medical services. Management services primarily offer administrative support for Medicare Part D plans and retail pharmacy networks, while also providing prescription management, disease management, and healthcare expenditure management services.

According to CVS Health's financial report, in 2021, the company's PBM business issued or managed as many as 2.2 billion prescriptions, demonstrating its strong operational capabilities.

The Retail and Long-Term Care Pharmacy segment is CVS’s traditional core business. The retail division primarily sells prescription medications, a wide range of health and wellness products, and general merchandise, while also providing patients with services such as diagnostic testing, flu management, and vaccinations for infectious diseases—including COVID-19—through its conveniently located MinuteClinic walk-in clinics. The long-term care pharmacy focuses on distributing prescription drugs and delivering pharmacy consultation and other supportive services for long-term care facilities. In 2021, this business segment filled as many as 1.6 billion prescriptions, accounting for 26.4% of the total prescription volume across all retail pharmacies in the United States.

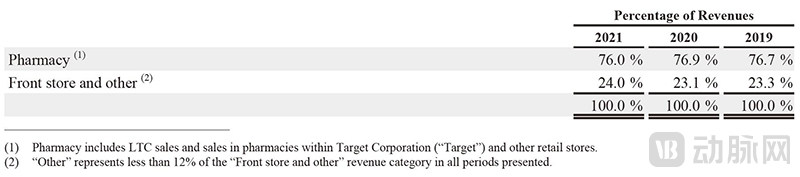

CVS Health’s Retail and Long-Term Care Pharmacy segment has, in recent years, further broken down its revenue into two specific business categories: pharmacy and front-end store operations, along with other businesses (screenshot from CVS financial report)

As CVS stores do not exclusively sell pharmaceuticals, the annual report further breaks down the operations of the Retail and Long-Term Care Pharmacy segment into two categories: Pharmacy and Front Store & Other. The Pharmacy segment primarily consists of prescription drug retail operations. The Front Store & Other segment includes front store operations (such as ExtraCare loyalty cards and prepaid cards, as well as CVS Health-branded health and beauty products), MinuteClinic walk-in clinics, on-site pharmacies, medical diagnostic testing, and long-term care pharmacy operations.

In terms of sales proportion, the retail prescription drug business accounts for an absolute share, maintaining a level close to 80% for several years.

Finally, there is the Corporate and Other segment. This segment primarily comprises components not included in the core business segments, mainly consisting of legacy pension and long-term care insurance businesses that are being maintained without new business development, as well as management and administrative expenses supporting the company’s overall internal operations. Based on historical revenue figures for this segment, its contribution is virtually negligible.

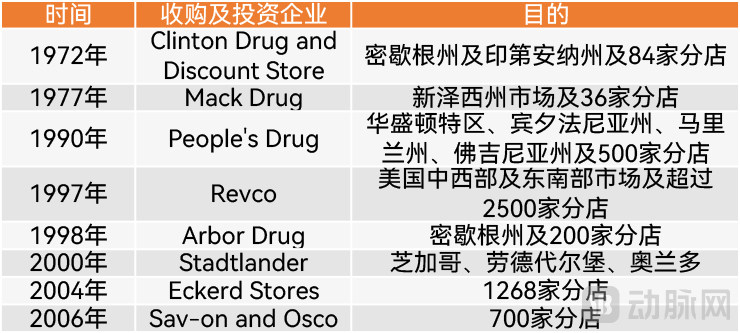

Since its founding in 1963, CVS has become the leading pharmacy chain in the United States through decades of aggressive expansion, including both organic growth and mergers and acquisitions. In 1999, CVS acquired the online pharmacy Soma.com and rebranded it as CVS.com. By 2005, CVS had surpassed its largest competitor, Walgreens, to become the nation’s largest pharmacy chain with more than 5,400 brick-and-mortar stores, a significant increase from approximately 1,000 stores in 1994.

CVS’s Major Early Mergers and Acquisitions in the Expansion of Its Chain Pharmacy Business

Subsequently, CVS embarked on a development path distinct from that of its primary competitor, Walgreens. The latter primarily pursued horizontal expansion, scaling its market presence through internationalization. This approach is fundamentally akin to domestic market consolidation, allowing the company to leverage its existing expertise to rapidly replicate its product portfolio, supply chain, and operational capabilities in international markets. Furthermore, it facilitates mutual synergy and integration, thereby reducing overall group costs and maximizing efficiency.

In contrast, after becoming the largest pharmacy chain in the United States, CVS did not pursue horizontal international expansion but instead adopted a vertical development strategy, extending its reach upstream and downstream within the industry. The 2006 acquisition of MinuteClinic, a walk-in retail clinic provider, marked a milestone in CVS’s vertical expansion. Through this acquisition, CVS began to penetrate upstream into healthcare services.

MinuteClinic’s nurse practitioners and physician assistants are all licensed to provide primary healthcare services to the community, including various laboratory and diagnostic tests, chronic disease management, and minor in-clinic procedures. They also offer common vaccination services to the surrounding communities and maintain close coordination with higher-level medical institutions within the community.

This notion is hardly surprising—statistics show that 70% of Americans live within five kilometers of at least one CVS pharmacy. The widespread presence of these community stores provides physical locations for CVS’s various community services, home-based care, and convenient clinics. Therefore, by effectively coordinating these diverse business formats to deliver more comprehensive services, CVS can enhance customer stickiness, achieving a “1+1>2” effect.

PBM represents CVS’s second avenue of expansion. As early as 1994, CVS began exploring the PBM business, aiming to establish a dual-core development strategy anchored by its brick-and-mortar retail pharmacies and driven by PBM services. However, this cross-industry endeavor proved challenging, and the revenue contribution from its PBM segment has remained minimal.

Even after acquiring Eckerd Stores’ PBM business in 2005 and generating $3.683 billion in revenue from it in 2006, this figure accounted for only 8.3% of the company’s total annual revenue of $43.8 billion.

2007 marked a turning point. By merging with Caremark Rx, then the leading PBM in the United States, CVS achieved a leap forward in its PBM business. That year, its PBM segment generated $43.45 billion in revenue, nearly matching the $45.09 billion in revenue from its retail pharmacy chain. Total revenue reached a new high of $76.33 billion, representing a substantial 74% increase from the previous year.

It is not difficult to understand why CVS Health had long been eager to enter the PBM business.

Leveraging its robust retail network, the PBM business saw rapid revenue growth in the following years, surpassing the retail pharmacy segment for the first time in 2012. Since then, the Pharmacy Services segment, represented by the PBM business, has remained CVS Health’s largest revenue-generating division.

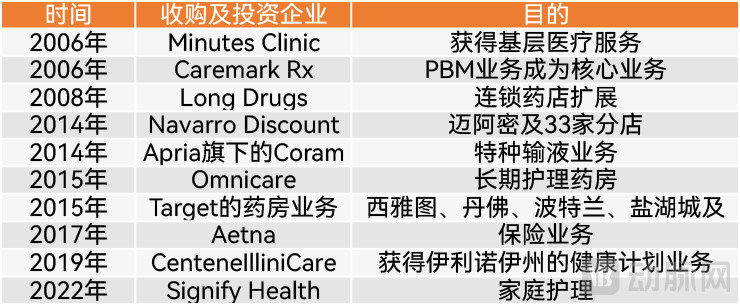

Certainly, during this period, CVS did not relax its efforts to consolidate its store-based operations. By acquiring Coram Specialty Infusion Services, the long-term care pharmacy Omnicare, and more than 1,600 pharmacies and clinics under Target, the retail giant, CVS has built a denser network capable of offering a broader range of services.

Notably, CVS Health’s appetite for acquisitions grew stronger during this period: it spent $12.7 billion to acquire Omnicare and $19 billion to purchase Target’s pharmacy business, successfully integrating both.

With this foundation in place, CVS began strategizing its entry into the trillion-dollar insurance business. In 2010, CVS acquired the Medicare prescription drug services division of UAM, marking its initial foray into the sector.

In 2017, CVS Health received approval from the U.S. Department of Justice to acquire Aetna for $69 billion, shocking the world.

Key M&A Events in CVS Health’s Vertical Expansion

Aetna is one of the oldest health insurance companies in the world and was the third-largest medical insurance company in the United States at that time, ranking 154th on the 2018 Fortune Global 500 list. At that time, Aetna provided medical insurance plans and other insurance services to a population of 22.2 million, particularly leading in the fields of medical, dental, pharmaceutical, life, and group disability insurance.

Following the merger, Aetna’s 23 million members will become a “traffic source” for CVS Health, while Aetna will benefit from more refined pharmacy benefit management and cost-control measures provided by CVS. More importantly, the combination will create a powerful bargaining alliance, strengthening their negotiating power against pharmaceutical companies and healthcare providers, thereby helping to further reduce operational costs.

During its third-quarter earnings call that year, CVS projected that the acquisition would help achieve at least $750 million in cost savings within two years.

The significant impact of Aetna’s acquisition on CVS is evident from the revenue performance of CVS Health’s pharmacy benefits management segment. In 2017, the newly formed division generated $3.59 billion in revenue. By 2018, this figure more than doubled, reaching $8.96 billion—a remarkable achievement for a nascent business unit.

However, this pales in comparison to Aetna. In 2019, Aetna’s revenue was consolidated into the financial statements, driving the segment’s revenue directly up to $69.6 billion. CVS Health’s total revenue also surged by 30% year-over-year, reaching $256.78 billion and breaking through the $200 billion mark.

In the latest financial report, the revenue of the healthcare benefits segment has reached $82 billion. Although it still ranks last among the major segments, it is not far behind the pharmacy business, which generated $100 billion. Based on the recent growth trends of these two business lines, the healthcare benefits segment is expected to surpass retail pharmacy within a few years, barring any unforeseen circumstances.

CVS Health’s Annual Revenue by Business Segment (Bolded years reflect the financial statement impact of major PBM and insurance acquisitions)

Thus, CVS Health has completed its vertical industry chain layout. By acquiring outstanding companies and even leading enterprises upstream and downstream in the supply chain, it has successfully expanded into the upstream healthcare services sector and the downstream payment services sector (including PBM and insurance services).

Although the healthcare systems of China and the United States differ, CVS’s growth trajectory clearly offers valuable reference points for China. First, the trend toward industry consolidation will become increasingly pronounced.

As early as 2018, the concentration of chain pharmacies in the United States had already exceeded 40%. In China, however, according to the latest annual reports, the six largest listed pharmacy chains collectively serve only over 260 million people out of a national population of 1.4 billion. Even the most extensive among them has yet to achieve coverage across all provinces in mainland China, excluding Hong Kong, Macao, and Taiwan.

According to data from the Ministry of Commerce, in 2021, the chain affiliation rate of pharmaceutical retail enterprises across China reached 57.2%, representing a significant increase from 34.3% in 2011. However, the total sales of the top 10 players in the industry amounted to RMB 114.7 billion, accounting for only 21.1% of the national retail market. In contrast, the top three companies in the United States hold more than 80% of the total market share. This indicates that there is still substantial room for improvement in market concentration in China.

Therefore, the early expansion and land-grab strategy of CVS Health has undoubtedly become a consensus within China’s chain pharmacy industry. In recent years, major chain pharmacies have intensified industry consolidation. Driven by large-scale mergers and acquisitions, the chain affiliation rate in China’s pharmaceutical retail sector is poised to rise rapidly, with market share concentration among leading enterprises accelerating significantly.

It is worth noting that, with the changing times, it is not only chain pharmacies themselves that are striving to increase industry concentration; new players such as professional investment firms and pharmaceutical companies are also actively engaging in investments and mergers and acquisitions within the pharmaceutical retail sector. Furthermore, internet giants represented by JD Health and Ali Health are entering the market from the online sphere, seeking to create an integrated online-to-offline (O2O) closed-loop ecosystem.

A seasoned veteran of the pharmaceutical e-commerce industry believes that the trend toward online-offline integration is irreversible. Particularly since the onset of the COVID-19 pandemic, a growing number of users have been exposed to online models for purchasing medications and seeking medical consultations out of necessity, thereby recognizing their convenience. Consequently, even as pandemic control measures have been relaxed, these users continue to opt for online services, and overall industry data continues to show an upward trend.

Driven by these favorable factors, companies will inevitably prioritize online-offline integration in their future strategies once they reach a certain stage of development. Depending on their respective strategic layouts, online giants may choose to either build their own offline stores or establish them through mergers and acquisitions (M&A). Relatively speaking, M&A is clearly a faster and more convenient path.

Of course, even with the rise of online healthcare, the importance of brick-and-mortar pharmacies should not be underestimated. A key factor behind this is the unique nature of medical services. In traditional retail, e-commerce platforms have gained a dominant advantage over offline retailers through their convenience and efficiency. However, the case of CVS Health demonstrates that pharmacies are more than just retail outlets; they can serve as critical nodes delivering primary care services to local communities, thereby enhancing accessibility for patients.

Through sustained efforts, CVS stores have evolved into integrated hubs offering convenient medical care, chronic disease management, health management, and the sale and services of traditional pharmacy products. Following its recent acquisition of Signify Health, CVS can even provide in-home nursing care to users in surrounding communities.

In China, the industry has also recognized that pharmacies can play a more significant role by shifting from a drug-centric to a patient-centric model, transforming simple medication sales into a comprehensive chronic disease management system that covers patients’ entire life cycles. In addition to dispensing medications, pharmacies can provide surrounding communities with a range of services, including maintaining chronic disease health records, conducting tests, offering safe medication information, providing medication guidance and follow-up, and managing complications.

Meanwhile, major pharmacy chains in China are also drawing on international experience to explore integration with a wider range of business formats. For instance, they are expanding their product offerings from purely pharmaceuticals to include health and beauty products. Alternatively, they are partnering with commercial insurance providers to build a multi-tiered healthcare payment system and service model that combines “basic medical insurance + commercial insurance.”

With continuous advancements in policy and the industrial environment—such as the ongoing promotion of the separation of prescribing and dispensing, the establishment of hospital-pharmacy prescription sharing platforms based on electronic prescriptions, and the further development of commercial health insurance—the industry is poised for even greater growth.

So, will we see a domestic “CVS” in the future? Let’s wait and see.

References:

Ministry of Commerce: "Statistical Analysis Report on the Operation of the Pharmaceutical Distribution Industry in 2021"

Fred Pennic,hitconsultant.net:CVS Health to Acquire Signify Health for $8B

Paige Minemyer,fiercehealthcare.com:How Signify Health fits into CVS' healthcare strategy

Marissa Plescia,Medcitynews.com:Analyzing CVS Health’s $8B buy: There’s no place like home