InnoCare Pharma Successfully Lists on STAR Market, Pioneering A+H Dual-Listing Trend for Innovative Biotechs

InnoCare

Innovative Drug Developer

On September 21, InnoCare successfully listed on the STAR Market of the Shanghai Stock Exchange, with an issue price of RMB 11.03 per share. The stock closed at RMB 9.33 on its first day of trading, representing a decline of 15.41%. Following its listing in Hong Kong in March 2020, InnoCare has officially embarked on a new “H+A” journey, becoming the largest IPO by fundraising scale among global biotechnology companies returning to the A-share market in 2022.

InnoCare, founded in 2015, focuses its product portfolio on oncology and autoimmune diseases. Driven by factors such as population aging, the demand in InnoCare’s therapeutic areas is substantial. According to Frost & Sullivan, the global oncology drug market reached $150.3 billion in 2020 and is projected to grow to $482.5 billion by 2030; the global autoimmune disease drug market totaled $120.6 billion in 2020 and is expected to reach $175.2 billion by 2030.

In the face of this vast and rapidly growing market, only enterprises with strong R&D capabilities can reap the benefits of development. Capital, in turn, serves as a solid backbone for R&D.

The STAR Market’s agglomeration effect on hard-tech companies continues to strengthen, with an increasing number of high-quality red-chip companies embarking on their “return to A-shares” journey. InnoCare’s listing on the STAR Market is poised to kick off a trend of dual H+A capital platform operations, which may represent a new direction for Chinese biotech companies exploring the capital markets in the future.

Shi Yigong, a highly renowned figure in the industry, is one of the co-founders of InnoCare.

Shi Yigong holds titles including Academician of the Chinese Academy of Sciences, Chair Professor at the School of Life Sciences, Tsinghua University, Foreign Associate of the American Academy of Arts and Sciences, Foreign Associate of the U.S. National Academy of Sciences, and Foreign Member of the European Molecular Biology Organization (EMBO). According to InnoCare’s introduction, Shi Yigong participates in the company’s operations as Co-founder and Chairman of the Scientific Advisory Board, providing assistance and guidance for its R&D activities.

Another co-founder, Cui Jisong, is also a prominent figure in the global pharmaceutical R&D community.

Cui Jisong worked at Merck for 14 years and also served as CEO and Chief Scientist of BioDuro, a PPD company. During his tenure as Chairman of the Sino-American Pharmaceutical Professionals Association (SAPA), he invited Shi Yigong to deliver a keynote speech at an international conference organized by the association, through which they became acquainted. By 2015, as the domestic environment for innovative drugs in China gradually improved, Cui Jisong and Shi Yigong decided to jointly establish an innovative pharmaceutical company, bringing advanced overseas expertise back to China.

In addition to the two co-founders, most members of the company’s management team come from multinational pharmaceutical giants such as Pfizer, GlaxoSmithKline, Bristol-Myers Squibb, and Johnson & Johnson. Among them, Zhao Renbin, wife of Shi Yigong, previously worked at Johnson & Johnson, serving as a Senior Scientist and later as Chief Scientist. She subsequently served as Director of Pharmaceutical Research Biology at Biodel, where she was a colleague of Cui Jisong. Zhao Renbin currently serves as an Executive Director at InnoCare.

Although 2015 marked a trough in the development of innovative drug companies, with pharmaceutical regulatory reforms only just beginning, and despite the Chinese pharmaceutical market being dominated by generic drugs and few new drugs being approved at that time, InnoCare swiftly secured financing from investment institutions, bolstered by the prestige of its star-studded team. Between 2016 and 2019, InnoCare raised approximately USD 300 million in cumulative financing.

Thanks to its strong R&D progress, InnoCare was listed on the Hong Kong Stock Exchange in March 2020, raising approximately HK$2 billion to fund plant construction, sales team establishment, and subsequent R&D investment.

Generally, it often takes more than 10 years for an innovative drug to go from research and development to market launch, whereas InnoCare launched its first product in just five years.

At the end of 2020, when InnoCare was listed on the Hong Kong Stock Exchange, its flagship product, orelabrutinib (Yinuokai®), received conditional approval for marketing from the National Medical Products Administration. Currently, InnoCare’s second commercialized product, tafasitamab, has been approved for use as an urgently needed clinical imported drug at Boao Super Hospital. In addition, 12 products are in Phase I/II/III clinical trials, and four products are in the preclinical stage.

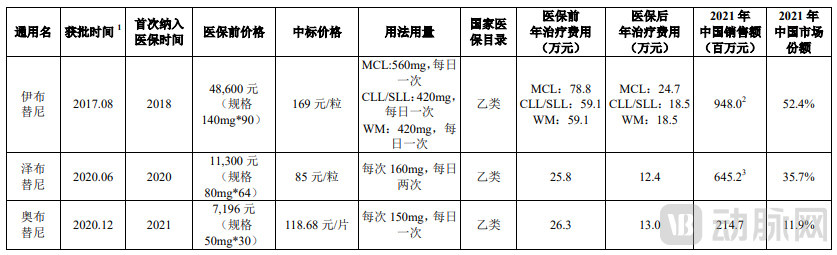

Market Share of Orelabrutinib and Its Major Domestic Competitors, Source: Prospectus

Orelabrutinib is the third BTK inhibitor to be launched in China, following ibrutinib and zanubrutinib. As commercial expansion only began in 2021, orelabrutinib generated sales revenue of RMB 215 million for the full year, capturing a market share of 11.9%. Following its inclusion in the National Reimbursement Drug List at the end of 2021, orelabrutinib’s sales revenue reached RMB 217 million in the first half of 2022, according to the interim report, representing a year-on-year increase of 115%.

During the roadshow, Jin Xiaodong, Chief Commercial Officer of InnoCare, stated that as of September 1, 2022, orelabrutinib had been included in the “dual-channel” drug management scope across 28 provinces, municipalities directly under the central government, and autonomous regions, with unified medical insurance reimbursement policies implemented at designated medical institutions and designated retail pharmacies. This will strongly ensure patient access to orelabrutinib and significantly enhance its market competitiveness.

InnoCare remains in a loss-making position. According to the prospectus, the company’s net profit attributable to shareholders was RMB -2.141 billion, RMB -391 million, and RMB -64.546 million in 2019, 2020, and 2021, respectively. As of December 31, 2021, the accumulated balance of uncovered losses amounted to RMB 3.562 billion. In the first half of this year, the company’s net loss widened from RMB 209 million in the same period last year to RMB 441 million, representing a year-on-year increase of 110.75%.

Like all innovative pharmaceutical companies, InnoCare faces the challenges of lengthy R&D cycles and high investment. The prospectus shows that InnoCare’s R&D expenses for the past three years were RMB 234 million, RMB 423 million, and RMB 733 million, respectively. R&D expenses in the first half of this year amounted to RMB 274 million, higher than RMB 185 million in the same period last year. Sustained R&D investment is the primary cause of its losses.

For innovative pharmaceutical companies, the advantage of independent R&D lies in the ability to select targets autonomously and optimize compound development, thereby securing international rights while controlling costs; however, the drawback is the prolonged R&D cycle. To boost revenue, InnoCare has licensed in the new drug Tafasitamab within its core therapeutic area of hematologic malignancies, aiming to explore combination therapy opportunities with its existing product pipeline in future promotions.

For a biotech company, product development is merely the first step toward success; the next challenge it must confront is how to clear the hurdles of commercialization.

Whether losses continue to widen depends largely on whether InnoCare’s commercialized product sales can meet expectations.

To accelerate commercialization, the Guangzhou pharmaceutical production base has officially received approval for commercial manufacturing. Constructed in accordance with GMP standards of China, the United States, the European Union, and Japan, the facility is expected to achieve an annual production capacity of up to 1 billion tablets. Starting June 30 this year, it will be utilized for the production of orelabrutinib tablets, marking InnoCare’s entry into independent manufacturing.

In terms of commercial sales, the prospectus reveals that InnoCare has established a commercialization team of more than 230 members to comprehensively drive the market expansion of orelabrutinib. In the future, with the launch of its second product, tafasitamab, the team will further expand.

Despite the significant revenue growth driven by sales of orelabrutinib, InnoCare still has a long way to go before it can achieve profitability with a single product.

To maintain ample liquidity during its development, InnoCare, like most biotech companies, has secured substantial cash flow through equity financing on one hand, and leveraged its robust business development (BD) capabilities to establish commercialization and development partnerships with large pharmaceutical companies on the other.

In July 2021, InnoCare entered into a license and collaboration agreement with Biogen, granting Biogen exclusive global rights to orelabrutinib in the field of multiple sclerosis, as well as exclusive rights in certain autoimmune disease fields outside of China, for an upfront payment of $125 million.

InnoCare will receive a $125 million upfront payment, as well as up to $812.5 million in potential payments for clinical development, commercial, and sales milestones, and will also be eligible to receive tiered royalties based on net sales.

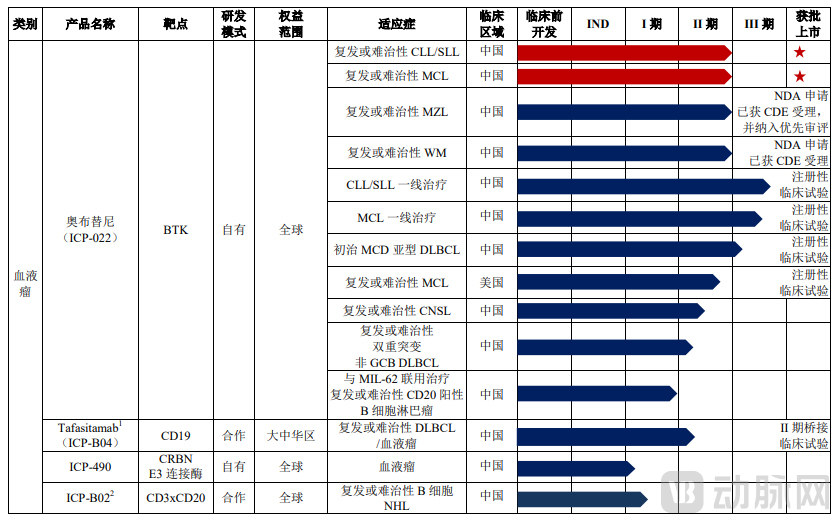

R&D Progress of the Flagship Product, Orelabrutinib; Image Source: Prospectus

The 2022 interim report shows that as of June 30, 2022, InnoCare’s cash and cash equivalents amounted to RMB 6.519 billion, indicating no immediate liquidity concerns on paper. However, funding requirements will rise as clinical research progresses. InnoCare is advancing multiple clinical trials for its pipeline products globally, continuously expanding its product portfolio and broadening the indications under investigation. This also means that InnoCare’s R&D expenses will remain at a high level.

In this scenario, only by maintaining a sufficient capital reserve to ensure the company’s sustainable development and prevent R&D disruptions due to funding shortages can it potentially achieve the commercialization of multiple products, rapid revenue growth, and high-speed corporate expansion in the future.

One year after its listing on the Hong Kong Stock Exchange, InnoCare completed a private placement of 210 million shares to institutional investors in February 2021, securing approximately HK$3.042 billion in investments from Hillhouse Capital and Vivo Capital. In August 2021, Hillhouse’s secondary market team increased its stake in InnoCare by 637,000 shares; in November, Hillhouse further acquired an additional 10.914 million shares at a cost of HK$194 million.

Hillhouse’s continued support has provided significant assistance to InnoCare, but this alone is insufficient. For InnoCare, which is already listed in Hong Kong, a return to the A-share market has become an inevitable choice.

Although InnoCare has begun to adopt the license-in model to introduce drugs, its self-developed products remain its core competitiveness. Cui Jisong once stated publicly: “Choosing to list on the STAR Market during a period of unfavorable market conditions was still a strategic decision. Raising more capital allows us to advance more clinical projects. It is difficult to control external developments; what matters more is strengthening our own moat.”

China previously lacked capabilities in novel drug development, as the industry was in its nascent stages and the broader sector had only a superficial understanding of the process. Given the substantial risks inherent in novel drug development, truly innovative companies must possess core competencies and establish their own technological barriers. This necessitates that enterprises define clear objectives and execute their plans in a structured and strategic manner.

From a macro perspective, under the new environment characterized by the strong synergy of domestic policies and the global upcycle in innovative drugs, China’s innovative drug market is gradually entering a phase of stable expansion. An analysis of historical National Reimbursement Drug List (NRDL) negotiation results shows that the innovativeness of pharmaceutical products has been continuously improving. Varieties with high clinical value have achieved significant sales growth after price reductions through NRDL negotiations; orelabrutinib serves as a typical case in point.

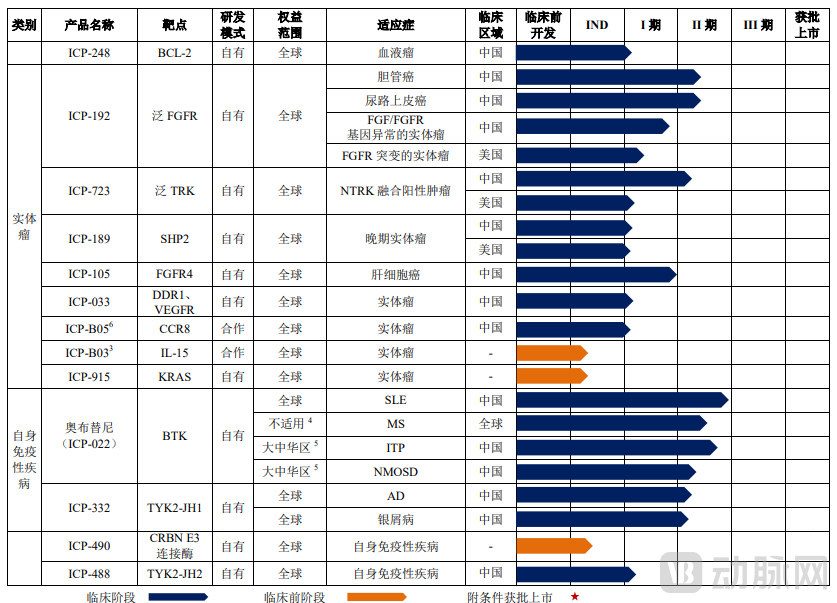

R&D Progress of InnoCare’s Product Pipeline, Source: Prospectus

InnoCare has a clear development goal: to continuously advance its product pipeline in hematologic malignancies, autoimmune diseases, and solid tumors, secure approvals for multiple products over the next three to five years, and establish a commercial portfolio of blockbusters, thereby demonstrating the company’s sustained capacity for value generation. This strategy aims to accelerate InnoCare’s transformation from a biotech firm into an integrated biopharma enterprise encompassing innovative drug R&D, manufacturing, and commercialization.

How Much Does It Really Cost to Develop an Innovative Drug? This Question Is Difficult to Answer Definitively.

However, we can draw a general conclusion from Deloitte’s report titled “2021 Pharmaceutical Innovation ROI Evaluation.” Deloitte analyzed the R&D return on investment trends of 15 leading global biopharmaceutical companies in 2021, and the data showed that the R&D cost for a single innovative drug at these companies amounted to USD 2.006 billion. This means that bringing an innovative drug from the laboratory to the market requires nearly RMB 14 billion.

In other words, InnoCare’s RMB 6 billion in cash on hand appears ample but is, in fact, insufficient to bolster the company’s competitiveness in the market.

Therefore, InnoCare’s return to the A-share market is driven by both tactical needs and strategic imperatives.

Previously, it was difficult for unprofitable companies to list on the A-share market, as listing requirements primarily focused on metrics such as revenue and profitability. True innovative drug companies typically incur substantial upfront investments, making it challenging for them to meet traditional listing standards. Subsequently, Chapter 18A of the Hong Kong Stock Exchange’s Listing Rules allowed pre-revenue, unprofitable biotechnology companies to file for listing on the HKEX, thereby becoming the preferred listing venue for many unprofitable biotech firms.

Subsequently, the China Securities Regulatory Commission (CSRC) issued a relevant announcement, adjusting the market capitalization requirements for overseas-listed red-chip companies to an “either-or” criterion: either “a market capitalization of no less than RMB 200 billion,” or “a market capitalization exceeding RMB 20 billion, coupled with independently developed, internationally leading technologies, strong technological innovation capabilities, and a relatively competitive position within the industry.” This effectively lowered the threshold for the return of overseas-listed red-chip companies to the domestic market.

As reforms and opening-up in China’s domestic capital market deepen, the listing regime has become more inclusive, and pathways for red-chip companies to return to the A-share market are continuously expanding. Coupled with external capital market factors, such as the U.S. Holding Foreign Companies Accountable Act, a significant number of companies are expected to choose to list on the A-share market in pursuit of a more stable capital and operating environment. On the other hand, Chinese concept stocks listed on Nasdaq are severely undervalued, significantly strengthening the incentive for innovative technology enterprises to return to the A-share market.

Competition is fierce in any industry undergoing capitalization, and this serves as the driving force behind industrial transformation and development. Meanwhile, the capital market evolves dynamically; it looks beyond the present to focus on the future. Only enterprises with sustained innovation capabilities are better positioned to embrace what lies ahead.

An increasing number of listed companies are opting to integrate their “A+H” dual financing platforms. According to data from East Money Choice, 146 companies have already established access to both financing platforms.

“A+H” dual listing comprises three models: “H-share first, then A-share,” “A-share first, then H-share,” and “simultaneous A+H listing.”

Listing H shares first and A shares later can be interpreted as indicating a company’s substantial capital needs, prompting it to choose H shares for rapid listing and financing to address urgent funding requirements. Subsequently, when its financial performance improves, the company returns to list A shares to secure higher valuations and greater access to capital. Conversely, listing A shares first and H shares later suggests that the company has international expansion objectives and requires H shares as an overseas financing platform.

FromFinancing EnvironmentTo speak of, the opening of the "A+H" dual financing model trend is inseparable from the deepening reforms of a series of listing systems in the two major capital markets of A-shares and H-shares in recent years, which have brought about continuously improving inclusiveness and openness.

FromCorporate DevelopmentFrom this perspective, establishing “A+H” dual listing platforms enables companies to avoid reliance on a single market for subsequent fundraising. The diversified funding channels provided by these dual platforms will significantly enhance corporate financing capabilities. Integrating the “A+H” dual financing platforms not only strengthens the close linkage between enterprises in both international and domestic markets but also further broadens their financing channels.

In addition to raising capital, companies pursuing an “A-share first, H-share second” listing can leverage the internationalized regulatory environment of the Hong Kong market to enhance corporate governance and promote market-oriented and standardized operations; meanwhile, those adopting an “H-share first, A-share second” approach can better harness the strength of China’s domestic capital markets to diversify and optimize their capital structure, thereby bolstering financial reserves for sustainable development strategies.

FromImpact PerspectiveFor companies with a global business footprint, establishing an “A+H” dual-listing platform can better meet the needs of international investors. Furthermore, H-shares can provide more options for future mergers and acquisitions, thereby further enhancing the company’s international brand value.

Typically, the Hong Kong market exhibits lower liquidity and price-to-earnings (P/E) valuations than the mainland China market. Integrating the “A+H” dual financing platform is conducive to valuation recovery for enterprises and enhancing secondary market liquidity.

As a pre-profit innovative pharmaceutical company, InnoCare has already had one blockbuster product approved for market launch. Compared with many pre-profit biotech companies listed on the Hong Kong Stock Exchange, its performance certainty is relatively higher. However, the company’s other products are still in early-stage clinical trials, requiring continuous high R&D investment. With this return to list on the A-share market and another round of substantial capital raising, how InnoCare will develop in the future remains to be seen.

In the recent period, a number of innovative drug companies listed on the Hong Kong Stock Exchange, including Junshi Biosciences, CanSino Biologics, and BeiGene, have successively listed on the STAR Market, initiating the “A+H” dual-listing model. Companies’ choice of listing venue is primarily driven by factors such as the ease of listing, the liquidity of exit channels for early-stage investors, valuation levels, internationalization needs, and the regulatory environment. Given that many enterprises have business expansion and diversified financing requirements, the H-share market remains a highly important listing destination.

The STAR Market has a clear positioning in China, establishing explicit institutional safeguards for the listing and financing of innovative biopharmaceutical enterprises, thereby carrying significant strategic importance. Currently, the STAR Market has gathered a cohort of science and technology-driven pharmaceutical companies that align with national strategies, possess key core technologies, and demonstrate outstanding technological innovation capabilities. Therefore, in the near future, the dual-listing model of “STAR Market + H shares” may become the preferred option for innovative pharmaceutical companies.