Surgical Robot Sector in Peril: Industry-Wide Shakeout Looms?

Bosscom

High-end Medical Device Developer

On September 20, 2022, the Hunan Provincial Healthcare Security Administration issued a document titled “Notice on Regulating the Use and Charging of Surgical Robot-Assisted Operating Systems” (hereinafter referred to as the “Notice”), cooling down the surgical robotics sector, which had been the hottest track this year.

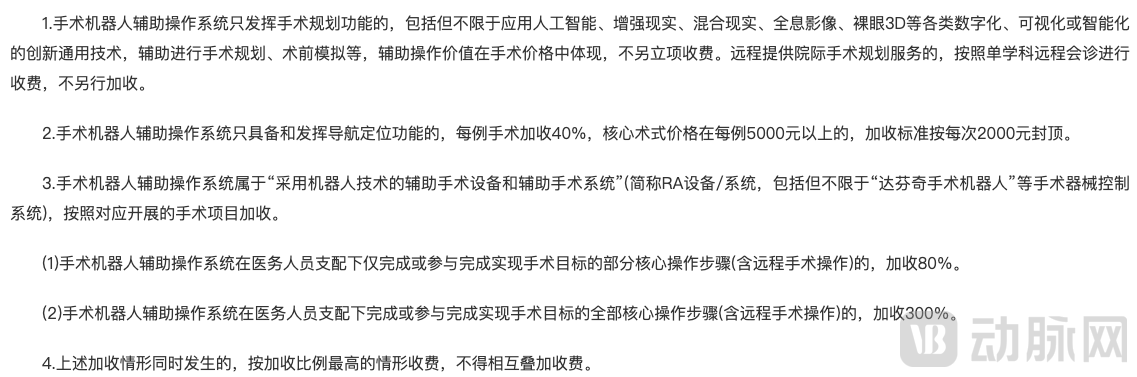

The Notice classifies surgical robots for the first time, encompassing all forms under the concept of “surgical robots” and re-categorizing them into three types: those that “only provide surgical planning functions,” those that “only possess and provide navigation and positioning functions,” and “robotic-assisted surgical devices and systems.” Software and hardware falling outside these three categories are not eligible for separate billing.

The introduction of pricing standards has sent shockwaves through the surgical robotics industry. Although the “Notice” is a local policy, it hangs like the Sword of Damocles, with the potential to be implemented nationwide at any time. When that happens, the valuations of many surgical robotics companies could plummet by half overnight.

Reactions to the “Notice” have been mixed. Some argue that the policy stifles enthusiasm for medical device innovation and overlooks the risk value associated with the development of cutting-edge technologies; others contend that all medical devices should be priced rationally, rather than focusing efforts on “innovating” billable items.

No consensus has yet been reached on who is right and who is wrong, but the National Healthcare Security Administration had already begun pricing and adjusting various surgical robots several years ago.

“Surgical robots” is originally a loanword. In China’s medical device classification catalog, surgical robots are categorized as active surgical devices, primarily divided into two types: “surgical navigation” and “control systems.”

“Surgical navigation” is used in conjunction with pre-generated surgical plans or for formulating surgical plans, to assist in surgical navigation. Navigation systems equipped with robotic arms can be utilized for minimally invasive procedures during surgery, providing support for more precise and refined surgical skills and maneuvers; the “control system” consists of a surgeon’s console, a patient-side surgical platform, a stereoscopic endoscope system, and dedicated instruments for the image processing platform, serving as equipment to help precisely control surgical operations during endoluminal procedures.

In simple terms, “surgical navigation” is primarily software-based and serves to assist in procedures; both surgical planning and navigation localization mentioned in the “Notice” fall into this category. In contrast, a “control system” requires an integration of hardware and software, functions to control procedural operations, and emphasizes the use of “robotic operative techniques.”

The da Vinci surgical robot, which is associated with endoscopic procedures, is a typical "master-slave" surgical robot. Its domestic registration name is "Endoscopic Surgical Instrument Control System." In contrast, surgical robots used in domestic neurosurgery, orthopedics, and other fields primarily serve as auxiliary tools, and their registration certificates are mostly labeled as "Surgical Navigation Systems."

Although the two types of surgical robots differ in function, market positioning, and price, the current policy impacts both, albeit to varying degrees.

Prior to the issuance of the “Notice,” surgical navigation robots had been gradually included in the price catalogs of multiple provinces and municipalities over the preceding two years. However, due to the lack of unified policy guidance, charging standards for surgical navigation varied widely across regions, ranging from as low as RMB 800 in some provinces and municipalities to as high as RMB 5,000 in others, with inconsistent classifications of surgical robots across different catalogs.

The convoluted pricing structure has created a chaotic market for surgical navigation robots, causing their value to become increasingly decoupled from their clinical utility.

“Although different surgical robots have clear conceptual distinctions during registration, some companies obscure the roles they play in assisting surgical procedures when applying for pricing approvals. Many manufacturers of orthopedic and neurosurgical surgical navigation systems have only completed R&D in ‘surgical navigation,’ but by purchasing hardware such as robotic arms and control consoles to assemble a so-called ‘control system,’ they enjoy pricing access at the level of control systems. This actually disrupts the equivalence between innovation value and revenue,” Yu Lang, founder of Shengxing Technology, told VCBeat.

Now, the "Notice" has made a breakthrough by classifying surgical robots as Class III medical devices. While establishing the roles of various types of surgical robots, it also clearly delineates their market segments. In other words, companies focusing on operational control should dedicate themselves to perfecting control technologies, while those specializing in navigation and positioning should build competitive barriers around these capabilities.

The policy’s classification and pricing of surgical robots have both advantages and disadvantages for the industry. Nevertheless, it is undeniable that while the Notice curbs the unchecked expansion of surgical navigation robots, it also offers them significant opportunities for growth and innovation.

For lightweight surgical navigation systems, the “Notice” has established their status through pricing regulations, eliminated information asymmetry between medical institutions and enterprises, and enabled hospitals to procure equipment based on their actual needs.

“Previously, hospitals invested over RMB 10 million in expensive equipment with limited functionality and high fees, making widespread clinical adoption difficult. With the introduction of new guidelines, hospitals purchasing surgical robots must now calculate the equipment’s service life, depreciation period, and the number of patients served annually during depreciation to determine the break-even point. Under these circumstances, it is difficult for hospitals to recoup the acquisition costs, leading them to abandon plans to purchase expensive surgical robots and instead opt for more practical surgical navigation products,” Xia Guifeng, founder of Bosscom, told VCBeat.

At the same time, to compete directly in the market with manufacturers of operative control surgical robots, companies specializing in surgical navigation must also deliver products of genuine value.

For most surgical planning robots, the range of surgical procedures they can assist with is quite limited. For instance, current orthopedic surgery robots can only perform incision positioning and point marking, failing to provide full-process coverage of the core surgical steps.

In other words, despite the high R&D costs incurred by manufacturers and the substantial surgical fees paid by patients, the singular value demonstrated by surgical robots appears insufficient to justify the significant expenditures across all stages of their lifecycle.

Against this backdrop, policy mandates that hospitals may only charge additional fees based on the number of core steps completed in a surgical procedure. One of the objectives is to control overall costs, enabling broader patient access to new technologies while fostering innovation in surgical techniques and core procedural steps within the surgical robotics industry.

To emerge as the leader in this new classification, companies must explore the development of diverse surgical techniques and core procedural steps, striving to achieve comprehensive coverage across all procedures and stages. After all, only such innovation in surgical robotics can truly meet clinical needs.

Compared with surgical planning robots, “control-and-operation” surgical robots face more severe challenges.

Historically, the pricing of surgical robots has been determined by the cost of their utilization. Generally, the cost for hospitals to acquire surgical robots falls into two categories: one is the cost of hardware equipment and routine maintenance, and the other is the cost of consumables such as scalpels, robotic arms, and laser generators.

Taking the da Vinci Surgical System as an example, the purchase cost per unit is approximately RMB 20–25 million, with annual maintenance costs ranging from RMB 1.5 to 2 million, and robotic arms priced at RMB 100,000 each. Southwest Securities previously estimated the surgical cost for procedures using the da Vinci system, finding the average expense to be as high as RMB 44,000 per case.

Taking radical prostatectomy for prostate cancer in urology as an example, the total cost for patients undergoing robotic-assisted surgery amounts to nearly RMB 60,000. In contrast, if laparoscopic surgery is adopted, hospital charges are estimated at RMB 5,000–8,000. According to the Notice, which caps additional fees at 300%, the maximum revenue a hospital can generate from one such procedure is RMB 32,000, which does not even cover the cost incurred by the hospital for a single system startup.

The Hunan Provincial Healthcare Security Administration was undoubtedly aware of the costs and current fee structures associated with surgical robots when establishing pricing standards. With this context, the issuance of the "Notice" serves two primary purposes: first, to encourage hospitals to make rational decisions regarding the use of surgical robots, ensuring they are not employed merely as tools for profit generation; and second, to incentivize domestic manufacturers to reduce the cost of surgical robots, thereby making them accessible to patients who genuinely require high-precision surgical interventions.

However, it is also important to note that, according to the transmission pathway outlined in the “Notice” (National Healthcare Security Administration–Hospitals–Enterprises), although the ultimate goal is to enable enterprises at the end of the chain to achieve cost control and technological innovation, if hospitals in the intermediate position fail to derive benefits from equipment innovation and consequently cease using surgical robots, this technology will lose its application scenarios, thereby eliminating any possibility for further innovation.

Therefore, Hunan Province’s pioneering issuance of the “Notice” is a response to the National Healthcare Security Administration’s policy released in March. However, due to the regional nature of the policy, current pricing standards may still be in the pilot phase and subject to adjustment during nationwide implementation. Given the inherent potential value of surgical robots, pricing standards will continue to evolve through ongoing adjustments involving medical insurance authorities, hospitals, enterprises, and patients, ultimately achieving a win-win outcome for all four parties.

Although the price access guidelines issued in the “Notice” have not yet been implemented nationwide, for companies operating in this sector, seeking new pathways is no longer merely a precautionary measure. After all, the challenges facing various types of surgical robots are real and tangible; it is only a matter of time before the National Health Commission and the National Healthcare Security Administration impose regulatory oversight on the industry.

In this context, companies that have entered the surgical robotics sector relatively recently must re-examine the issue from the perspective of hospitals. Specifically, they should assess the profitability potential of niche segments based on the overall demand for surgical robots in Chinese hospitals, calculate the payback period for their R&D products from the hospital’s standpoint, and determine whether it remains necessary to deepen their involvement in this sector.

For companies that have already made in-depth investments in surgical navigation robots, they are facing a market that is fairer and more focused on clinical value. In this context, refining the development of surgical procedures and core steps, and accelerating the layout of full-procedure and full-step coverage have become inevitable for corporate growth. Throughout this process, companies must also control R&D costs to avoid falling into the trap of “high investment, low clinical value.”

For the few domestic companies that have completed the R&D of surgical robot control systems, although they are currently facing the dual pressures of market education and shrinking scale, if they can achieve a breakthrough in R&D costs and effectively reduce the usage cost of surgical robots, these companies are expected to seize the opportunity for overtaking on bends amidst challenges and capture market share from overseas enterprises.

The policy implications extend beyond surgical robots, offering valuable insights for the entire medtech sector. In summary, the era of “muscle-flexing” development in medical technology—relying merely on the accumulation of technologies and conceptual packaging—is over. To achieve long-term sustainability within hospital settings, products must never deviate from their essential clinical value at any stage.