Billion-Dollar Asset Repatriation: Is the Medical IPO Sector Poised for a Comeback?

Delisting is virtually the Sword of Damocles hanging over all Chinese concept stocks.

Over the past two months, entities ranging from the “first listed internet medical aesthetics company” to the “largest IPO in precision cancer diagnosis and treatment” have been swept into a public opinion whirlwind surrounding delisting. Their brief journey on the U.S. stock market appears not to have served as the anticipated accelerator for growth, but instead has left behind widespread damage. Recently, VCBeat reviewed the 27 Chinese healthcare companies still listed on U.S. capital markets, finding that 25 of them face various delisting risks. Their combined market capitalization of nearly $30 billion has effectively become high-risk assets.

So, what kind of crisis does the delisting turmoil sweeping through Chinese concept stocks pose to healthcare innovation companies? And does this crisis also harbor new opportunities? We attempt to provide answers.

What triggered the panic over the collective delisting of Chinese concept stocks was the once widely discussed “Provisional Delisting List.”

Since early March, the U.S. Securities and Exchange Commission (SEC) has successively released nine batches of companies identified for potential delisting, covering nearly half of all China-concept stocks. Industry analysts note that after these China-concept stocks sequentially released their financial reports, they were all included on the provisional delisting list.

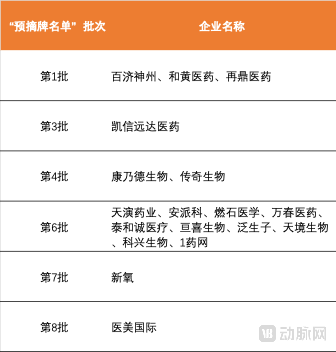

Specifically, on March 8, 23, and 30, the U.S. Securities and Exchange Commission (SEC) successively released three batches of the provisional delisting list, which included 11 Chinese concept stocks, such as four domestic innovative pharmaceutical companies: BeiGene, Zai Lab, Hutchmed, and CStone Pharmaceuticals. On April 13 and 21, 29 Chinese concept stocks were added to the SEC’s provisional delisting list, including Conatus Biosciences and Legend Biotech. On May 4, 9, and 30, the SEC issued three more lists of companies identified for potential delisting, covering 107 Chinese concept stocks. Healthcare-related enterprises on these lists included Burning Rock Biotech, Vascure Pharmaceutical, Cancer Care China, Gracell Biotechnologies, Genetron Holdings, I-Mab, Sinovac Biotech, 111, Inc., So-Young, and Peng Ai Aesthetic Medicine. By the end of July, the SEC released its latest ninth batch, adding six more Chinese concept stocks.

Healthcare Companies on the Pre-Delisting List

The release of the provisional delisting list triggered immediate declines in the share prices of the affected companies. In March, following the announcement of the first batch of companies included in the “provisional delisting list,” BeiGene’s stock price fell for three consecutive days, wiping out nearly one-third of its market capitalization. Similarly, the shares of Hutchmed and Zai Lab, also on the list, plummeted for three straight days. Admittedly, the prospect of delisting deterred investors, prompting them to hastily offload their holdings, which in turn accelerated the delisting of Chinese concept stocks. The NASDAQ’s mandatory delisting rules will be discussed later.

The rationale behind the provisional delisting list stems from the implementation of the U.S. Holding Foreign Companies Accountable Act (HFCAA). Officially enacted in 2020, the HFCAA laid the groundwork for this year’s provisional delisting list. Under the HFCAA, foreign companies listed in the United States may face mandatory delisting if they fail to allow U.S. regulators to inspect their audit working papers for three consecutive years. Typically, once a company is placed on the provisional delisting list, it has a 15-day window to demonstrate to the U.S. Securities and Exchange Commission (SEC) that it does not meet the criteria for delisting; otherwise, it will be moved to the confirmed delisting list.

It is evident that the companies faced preliminary delisting due to regulatory issues, rather than operational problems. In fact, while submitting audit working papers to regulators is technically feasible, it conflicts with domestic regulations. According to China’s Securities Law, documents and materials related to securities business activities must not be disclosed overseas without the permission of the China Securities Regulatory Commission (CSRC). Furthermore, data security regulations issued in June 2021 also imposed relevant restrictions. However, by late August, the CSRC and the Ministry of Finance officially announced that they had reached an audit regulatory cooperation agreement with the Public Company Accounting Oversight Board (PCAOB). In mid-September, media reports indicated that the PCAOB had selected accounting firms and would dispatch staff to Hong Kong to participate in the review process. This development has, to some extent, mitigated the external pressure for a large-scale delisting of Chinese concept stocks from U.S. stock exchanges.

In contrast, Chinese-listed stocks face another, more concrete challenge: the continued listing review standards of the Nasdaq market.

This standard comprises two mandatory criteria and three optional criteria. The two mandatory criteria are the $1 minimum bid price delisting rule (where a listed company receives a delisting warning if its closing share price falls below $1 for 30 consecutive trading days) and the rule requiring delisting if the total number of shareholders is fewer than 400. The three optional criteria include a market capitalization exceeding $50 million, annual revenue exceeding $50 million, and shareholders’ equity exceeding $10 million.

If calculated based on the “$1 Listing Rule,” numerous Chinese healthcare stocks listed in the U.S. also face delisting risks. This potential delisting list includes former industry leaders in various niche sectors, such as Nature’s Sunshine Products and So-Young. Of course, with a 30-trading-day grace period, most companies on this list still have an opportunity to turn the tide; however, a few have already received delisting warnings due to their stock prices.

For example, Ampio Pharmaceuticals, which appears on this list, previously received a warning from Nasdaq. Under the listing rules, the market value of Ampio’s listed securities fell below the $50 million minimum required for continued listing over 30 consecutive trading days. On September 24, 2021, Nasdaq notified the company of this deficiency, and the company failed to regain compliance within the prescribed 180-day period. Consequently, Nasdaq informed the company that its securities would be delisted from the Nasdaq Global Market at the market open on April 4, 2022. SoYoung has also received similar warnings.

It is evident that, regardless of the underlying reasons, Chinese concept stocks are collectively entering their darkest hour in overseas markets, and the practice of listing in the United States may become a thing of the past.

Although Chinese concept stocks have only recently become a phenomenal presence in overseas capital markets, they have already undergone three waves of relisting.

For a long time, due to relatively low barriers, faster processes, and ample capital availability, listing in the U.S. was an important milestone that many domestic innovative enterprises included in their agendas from inception. To this end, most of them established red-chip structures suitable for the U.S. stock market during the early stages of equity financing, and would file prospectuses with NASDAQ or the NYSE once the timing was ripe.

By March 2022, when the “Pre-Delisting List” began to be disclosed, more than 260 Chinese companies had gone public in the United States over the previous two decades, forming a substantial cohort with a combined market capitalization of $1.3 trillion. The term “Chinese concept stocks” has thus become widely recognized.

However, driven by factors such as regulatory constraints, costs, and the rapid maturation of global financial markets, the past two decades have also witnessed a dramatic contraction in the U.S. stock market. Since 1996, an increasing number of U.S. companies have chosen not to list domestically, while delistings have surged, causing the number of publicly traded companies on U.S. exchanges to nearly halve. Meanwhile, emerging capital markets, including Hong Kong stocks and A-shares, have experienced rapid growth.

Generally, there are three options for Chinese companies listed in the U.S. to return home: privatization and delisting from the U.S. stock market, followed by a new listing on the A-share or Hong Kong stock market; maintaining their U.S. listing status while pursuing a dual primary listing on the A-share or Hong Kong stock market; and maintaining their U.S. listing status while seeking a secondary listing on the A-share or Hong Kong stock market.

Data shows that between 1996 and 2019, the number of listed companies in mainland China grew from 524 to 3,777, marking the second-highest growth rate globally, while the number of listed companies in Hong Kong increased from 561 to 2,272. In 2019, Hong Kong’s IPO fundraising reached $314.2 billion, not only setting a new high since 2011 but also securing its position as the world’s largest IPO market for the second consecutive year after 2018.

In fact, the delisting turmoil involving Chinese concept stocks that began in March 2022 was not the first large-scale exodus for this group.

Between 2013 and 2016, Chinese concept stocks embarked on their first wave of intensive relisting. The underlying reason was straightforward: undervalued market capitalization.

During this period, a cohort of companies that had previously listed in the United States—including Focus Media, WuXi AppTec, Qihoo 360, Mindray Medical, Giant Network, Perfect World, and Shanda Games—returned to the Chinese market. In the first wave of such returns, these China-concept stocks made their re-entry into the domestic capital markets, where they were enthusiastically embraced by investors. Notably, WuXi AppTec and Mindray Medical opted for a decisive path: delisting from the U.S. stock exchanges through privatization and subsequently relisting on China’s A-share market. This strategic move proved pivotal for their subsequent development.

At the end of 2015, WuXi AppTec, which had been listed on the U.S. stock market for nine years, was delisted with a market capitalization of $3.3 billion. Two years later, WuXi AppTec was split into three entities—WuXi AppTec, WuXi Biologics, and Pharmaron (formerly known as WuXi STA)—which were subsequently listed on the Shanghai Stock Exchange (A-shares), the National Equities Exchange and Quotations (NEEQ), and the Hong Kong Stock Exchange, respectively. The combined market capitalization of these three companies approached RMB 100 billion, nearly ten times the value at the time of delisting. In 2021, WuXi AppTec’s share price reached an all-time high of RMB 172, giving this single entity a market capitalization of RMB 500 billion. Even amid the current broad decline in pharmaceutical stock prices, the total market capitalization of the WuXi-affiliated listed companies remains close to RMB 500 billion, a figure that was difficult for WuXi AppTec to achieve when it was listed in the United States.

In most cases, the widespread undervaluation of Chinese concept stocks in the U.S. market, relative to domestic companies, is often not attributable to their operational performance per se; rather, it stems from cultural differences in perception and divergent preferences for business models.

For instance, WuXi AppTec has maintained an aggressive investment stance since 2014, focusing primarily on gene science, biological operations including cell therapy, and mobile health. However, Wall Street investors, who prioritize cash flow, have been skeptical of such large-scale M&A investments. A clear example occurred in March 2014: after releasing its full-year 2014 financial results, WuXi AppTec announced the construction of a new CAR-T facility in Philadelphia. This move triggered a stock sell-off by investors, causing WuXi AppTec’s share price to drop from around $40 in early March to $34.39 on March 13, a decline of over 16%. In contrast, the Hong Kong Stock Exchange and the STAR Market exhibit greater tolerance for cash flow considerations, as evidenced by the numerous innovative pharmaceutical star companies that have emerged in these markets.

Around 2019, Chinese concept stocks once again experienced a concentrated wave of homecomings. The second wave of collective returns by these companies was driven not only by valuation disparities but also by emerging political and commercial factors, leading to a significant increase in the number of firms returning compared to two or three years earlier.

In 2018, two hard-tech companies, JA Solar and Montage Technology, went private from the U.S. stock market and returned to the A-share market, marking the start of the second wave of Chinese concept stocks returning home. In November of the following year, Alibaba held a secondary listing in Hong Kong, becoming the first Chinese concept stock to do so. After 2020, seven Chinese concept stocks, including NetEase, JD.com, Yum China, ZTO Express, and Huazhu Group, completed secondary listings in Hong Kong. They were warmly received by investors and drove a new round of prosperity for the Hong Kong Stock Exchange as an offshore financial market. Subsequently, seven other Chinese concept stocks—Jumei International, Changyou, 58.com, Yixin, Sogou, Sina, and DouYu—completed privatization, with some planning to relist on the A-share market in the future.

In April 2018, the Hong Kong Stock Exchange (HKEX) unveiled the latest version of its Listing Rules, introducing three major initiatives to attract new-economy companies to list in Hong Kong. These measures included allowing companies with their primary business focus in the Greater China region to pursue secondary listings in Hong Kong, significantly lowering the thresholds for shareholding structure and market capitalization for such secondary listings. Since then, the HKEX has welcomed more than 20 returning Chinese concept stocks within just a few years. The initial public offering (IPO) market capitalizations of these Chinese concept stocks on the HKEX have continually broken trading volume records in the market, largely continuing the remarkable trend of Chinese concept stocks returning to mainland China’s A-share market.

The third wave of capital repatriation, which began in March this year, has been driven by more complex factors than the previous two rounds and involves a larger number of companies. What changes their return will trigger in the capital market is an even more complex proposition.

For most Chinese companies listed in the U.S., delisting from American stock exchanges will not mark the end of their journey in the capital markets. If the first wave of relistings nearly a decade ago helped create A-share stars such as WuXi AppTec and Mindray Medical, and the second wave three years ago forged the Hong Kong Stock Exchange legends of innovative pharmaceutical companies like BeiGene and Zai Lab, then a distinct feature of the current third wave of relistings is dual or multiple listings.

It is necessary to distinguish between two concepts: secondary listing and multiple listing. The latter can, to a certain extent, broaden its shareholder base and enhance its influence in the global market.

During the first two waves of Chinese concept stocks returning to their home markets, listed companies predominantly chose the A-share market or the Hong Kong Stock Exchange (HKEX) as their secondary listing venue. While secondary listings entail fewer regulatory requirements and lower costs, they are clearly disadvantaged by their susceptibility to volatility in the primary listing market. Consequently, an increasing number of enterprises are opting for dual or multiple listings. Although this approach involves a more complex listing process and incurs greater time and financial costs, stock pricing across different markets remains relatively independent, and shares are more readily included in indices on the new capital markets.

BeiGene is the first innovative pharmaceutical company in China to adopt a multiple-listing strategy. In 2016, BeiGene listed on the NASDAQ, reaching a market capitalization of nearly $10 billion after three follow-on offerings. In 2018, it achieved a dual primary listing on the Hong Kong Stock Exchange. Two years later, it was included in the Stock Connect program, and the following year, it further expanded its multiple-listing structure with a formal listing on the Shanghai Stock Exchange. Cumulatively, the company has raised nearly $50 billion across these three markets, providing robust support for the research and development of innovative drugs.

Data shows that BeiGene’s planned or ongoing clinical trials have covered nearly 50 countries and regions worldwide, with more than 14,000 participants enrolled. Among the nearly 100 clinical trials, dozens are Phase III studies or potential registration-enabling trials, with overseas patients accounting for nearly half of the enrollment. As is well known, clinical trials represent the most capital-intensive stage of new drug development. Such substantial financial demands indicate that relying solely on fundraising in a single capital market is insufficient to sustain these efforts.

Furthermore, in June this year, Zai Lab converted its listing status on the Hong Kong Stock Exchange (HKEX) from a secondary listing to a primary listing, becoming another company with a multi-listing structure. Hutchmed, upon its return to the Hong Kong stock market, initially opted for a multi-listing approach, with its share price surging 50% on the first day of trading. Meanwhile, InnoCare Pharma, which just listed on the STAR Market last week, chose a dual-listing strategy on both the HKEX and China’s A-share market.

As an increasing number of healthcare innovation companies opt for dual or multiple listings across different capital markets, the performance and conditions in any single market no longer hold veto power. For healthcare innovation enterprises, the need for external funding remains constant; beyond the U.S. stock market, pursuing multiple listings in other capital markets may prove to be a more favorable strategy.