2022 Medical AI Industry Report: How Far Is Profitability for Healthcare AI?

From *Hyperion* to *Cyberpunk 2077*, every audiovisual work depicting the AI era meticulously portrays the technology, architecture, and daily life of the technological age, eagerly engaging with philosophical questions surrounding survival, development, and symbiosis in the cyber age.

But as AI sheds its illusory veil and truly integrates into people’s lives in a subtle, pervasive manner, it becomes even more essential to look beyond its technological manifestations and trace the driving forces behind its development.

Over the past five years, nearly RMB 100 billion has been injected into the medical artificial intelligence sector, driving unprecedented growth in sub-sectors such as AI for medical imaging, AI-driven drug discovery, robotic AI, and smart hospitals. Sustained external support has enabled AI to take root across all aspects of healthcare, becoming as pervasive as internet technology.

This is precisely where the problem lies. Over a thousand companies have entered the fray, yet few have achieved profitability. In the next five years, as the trickle of capital ceases to be forthcoming, will AI-focused enterprises be able to build mature, self-sustaining revenue models and survive on their own merits?

Guided by these questions, we engaged with over 30 companies and interviewed nearly 100 experts, conducting research across the entire industry development lifecycle to systematically address the industry’s challenging question: “How can medical AI achieve profitability?”

The initial goal and mode of action of AI lay in the “substitution” and “optimization” of past human activities, achieving cost reduction and efficiency enhancement through intelligent empowerment, which can be termed AI 1.0.

Over the past decade, this category of medical AI has matured significantly in optimizing physicians’ diagnostic and treatment efficiency as well as patients’ care pathways. A tangible indication is that outpatient halls in many Grade 3A hospitals are no longer as congested as they once were, thanks to online smart information flows that have addressed the issue.

During this process, AI technology itself has been continuously exploring the possibilities of deep integration with clinical practice, attempting to empower healthcare by optimizing clinical pathways. The resulting products are categorized as “AI 2.0” in the report.

AI 2.0 is an extension of the application scenarios covered by AI 1.0. The key distinction between AI 2.0 and AI 1.0 lies in whether knowledge and algorithms can be deeply integrated to reshape existing medical workflows. In simple terms, early-stage AI focuses on enhancing the efficiency of operational entities, whereas advanced AI has the capability to completely overhaul and reconstruct workflows, establishing a new order centered around AI capabilities.

Furthermore, the value creation model of Medical AI 2.0 differs from that of AI 1.0. The AI 1.0 era was characterized by blanket innovation, where development expanded from the lungs to other organs such as the brain, heart, and liver. In contrast, innovation in the AI 2.0 era is focused on single-point advancements built upon the achievements of AI 1.0, with companies exploring the deeper value of AI within their respective domains, rather than forming the large-scale AI product matrices seen in the AI 1.0 era.

The two types of AI empower the healthcare system in their respective ways, forming a collaborative rather than competitive relationship. Currently, there are many mature AI 2.0-style applications in the medical AI industry. Behind this trend, increasingly abundant high-quality medical data and progressively diverse algorithms provide crucial support for AI innovation.

So, what is the most critical factor in the transition from the 1.0 to the 2.0 era? Among the three key elements determining AI quality—algorithms, computing power, and data—it is ultimately algorithms and data that truly create competitive barriers.

Taking AI for assisted diagnosis as an example, during the AI 1.0 era, there was a global scarcity of open-source big medical data. AI companies had limited access to directly obtainable data, which was characterized by small volume, low standardization, low annotation success rates, and limited data types (primarily focused on pulmonary nodules).

At this stage, enterprises must collaborate with hospitals to acquire valid datasets. After obtaining de-identified data, they proceed with classification, annotation, and model training. Since the entire process relies on manual labor, the cost per data annotation ranges from 10 to 30 RMB, taking 20–40 minutes per instance. While financial investment is limited, the time commitment is substantial. In particular, achieving high-quality annotations requires the involvement of senior physicians, which significantly increases the difficulty of the annotation process.

As AI technology has become increasingly mature, since 2020, a large number of hospitals have voluntarily joined the construction of single-disease imaging databases and third-party testing databases, leading to an exponential growth in data volume. This has significantly reduced the difficulties faced by AI companies in developing new indications. Furthermore, as third-party databases have gradually achieved scale, the diversity of medical AI products has increased accordingly. Consequently, the data barriers established by AI companies have begun to weaken, while the importance of algorithmic barriers has become more prominent.

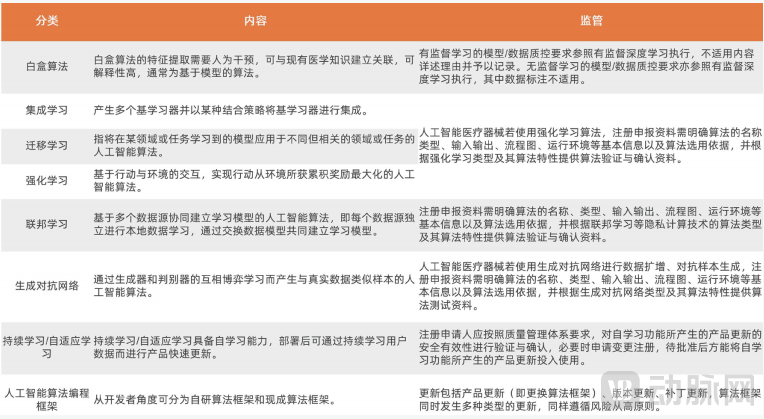

On the other hand, on March 7, 2022, the Center for Medical Device Evaluation of the National Medical Products Administration (NMPA) issued the "Guiding Principles for Registration Review of Artificial Intelligence Medical Devices" (hereinafter referred to as the "Guiding Principles"), which redefined concepts such as AI medical devices, basic registration principles, lifecycle processes for AI medical devices, and technical considerations. Notably, this policy refined the algorithms applicable to AI approval by expanding beyond deep learning to include transfer learning, ensemble learning, federated learning, reinforcement learning, generative adversarial networks, and adaptive learning.

Content and Regulation of Various AI Algorithms (Data Source: VCBeat)

Following the release of the document and the confirmation of review and approval processes for more innovative algorithms, the barriers in medical AI are gradually shifting toward algorithmic capabilities. A richer variety of algorithms will enter the market, empowering diagnostic and treatment workflows in a more effective manner.

Overall, whether in the AI 1.0 or AI 2.0 era, the value of medical AI lies in reshaping digital healthcare through intelligence, a gradual and continuous process. Currently, mainstream AI products such as AI-assisted diagnosis and AI-driven new drug discovery are in a transitional phase of commercialization. They possess highly accurate and replicable models, National Medical Products Administration (NMPA) medical device certifications, comprehensive knowledge graphs, and stable partnerships—key components for commercialization. However, due to the market’s lag in accepting new technologies, most target hospitals and pharmaceutical companies remain skeptical about the benefits of intelligent products and the operational sustainability of startups, leaving room for improvement in payment conversion rates. As market recognition of AI’s value continues to grow, the commercial capabilities of medical AI enterprises will gradually strengthen, potentially achieving profitability within a few years.

Although AI at different stages has its own value, capital's preference for certain tracks can still be intuitively reflected through data.

Globally, computer vision-based AI-assisted diagnosis and NLP-based medical knowledge graph construction are the two fastest-growing sectors in medical AI. In particular, during the period from 2015 to 2020, hundreds of companies entered the field of AI-assisted diagnosis, with more than a hundred securing financing from the primary market.

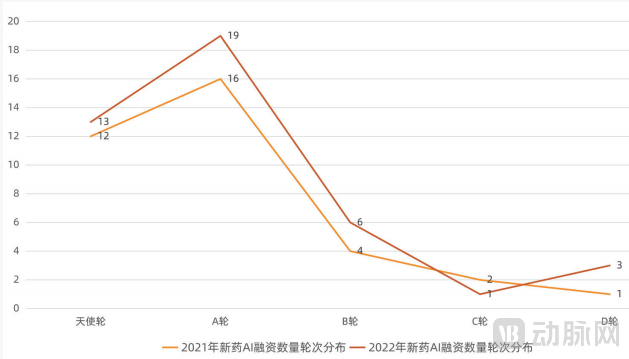

But in 2022, AI for new drug development emerged as a standout, becoming the hottest sector across the entire field.

During the 2021 statistical year (September 1, 2020–August 31, 2021), early-stage projects (pre-Series B, excluding Series B) accounted for 80% of the 35 disclosed AI-driven new drug financing rounds. In the 2022 statistical year (September 1, 2021–August 31, 2022), the total number of such rounds increased from 28 to 32, with early-stage projects maintaining a 76% share.

Prior to 2021, capital tended to concentrate on leading enterprises such as XtalPi, with very limited financing opportunities for AI-driven new drug startups. However, the performance of the primary market for AI in new drug development over the past two years indicates that this sector has become the most investable track within AI technology. A large number of investment institutions have flocked into the field, expanding the application scenarios of AI from crystal discovery and clinical patient screening to every aspect of the pharmaceutical process.

New Drugs in 2021 and 2022AIFinancing Rounds (Data Source: VCBeat)

Furthermore, within the realm of software development, AI-driven new drug discovery ventures command significantly higher valuations than other AI-enabled sectors. Statistical data indicate that projects at the angel round typically require funding of over RMB 10 million, while more than half of enterprises in Series A (including Pre-A and A+ rounds) have raised over RMB 100 million. Investors remain highly optimistic about the AI-driven new drug discovery sector. The substantial late-stage single-round fundraising of RMB 300–400 million by XtalPi, the RMB 500 million Series A+ financing of Xinhe Bio, and the USD 100 million Series A funding of BioMap all clearly demonstrate that the primary market holds a positive outlook on the future prospects of AI in new drug development.

Let’s examine the field of imaging AI, which boasts the most mature commercialization. Following the wave of IPOs in the medical AI sector in 2021, imaging-related companies such as Keya Medical, LinkDoc Technology, Infervision, and Shukun Technology successively filed their prospectuses; in November of the same year, Airdoc successfully went public.

However, this momentum came to an abrupt halt in 2022. Most leading AI companies maintained relatively stable cash flows and ample capital reserves. Driven by concerns about post-IPO stock price declines amid economic downturn pressures, only Botong Medical had submitted its prospectus in China as of September 15. Notably, the company focuses primarily on precision diagnosis for coronary intervention, with AI-supported QFR being just one component of its product portfolio.

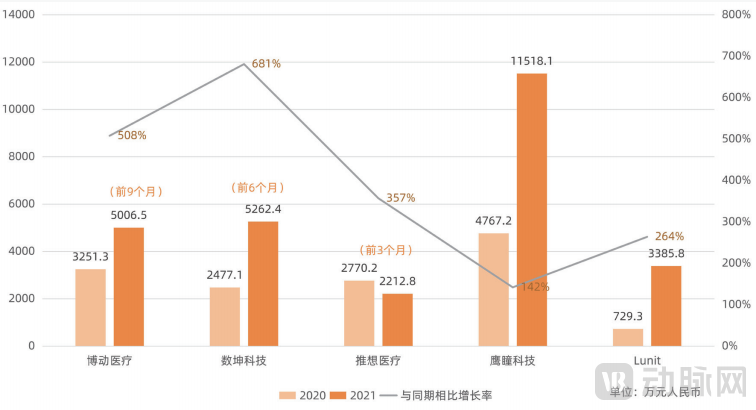

Following their IPOs, several companies delivered strong performances. All reported positive revenue growth to varying degrees, indicating further market expansion. Notably, Shukun Technology achieved a year-on-year growth rate of 681% in the first half of 2021, while Airdoc, which already had revenues at scale, still recorded a 142% increase, with its full-year 2021 revenue surpassing RMB 100 million.

Analysis of Main Business Revenue of Companies Filing for IPO (Data Source: Prospectuses and Annual Reports of Each Company, VCBeat)

Nevertheless, negative net profit is an unavoidable reality for every enterprise. VCBeat Research Institute believes that AI companies are still in a stage of rapid development, requiring substantial investment in research and development to maintain competitiveness and ensure exploration of frontier markets. On the other hand, while economies of scale in profitability are beginning to emerge, their scale still needs to be expanded. Under high R&D expenditures, current limited revenue is insufficient to support significant growth in net profit.

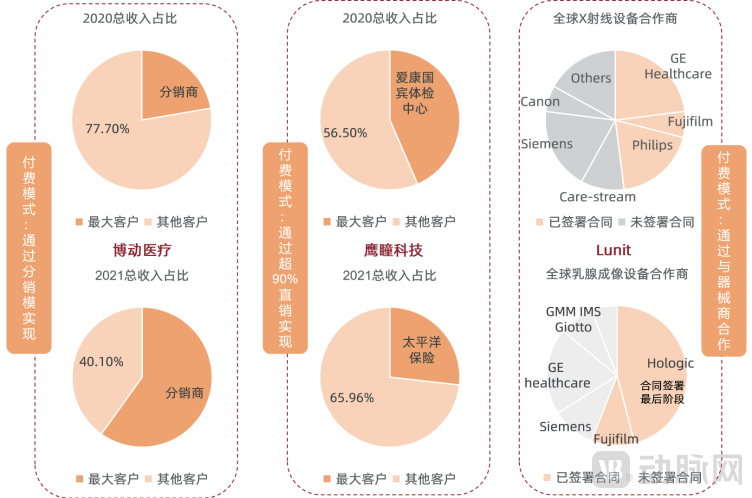

Notably, the risk resilience of the vast majority of medical AI companies is steadily strengthening. It is evident that the proportion of revenue derived from the top five customers as a share of total revenue is continuously declining for many enterprises, reflecting increasingly diversified and decentralized commercialization pathways. Under this trend, AI companies with billions in cash flow have ample time to refine their market positioning and gradually achieve profitability.

Analysis of Largest Customers (Data Sources: Company Prospectuses, Annual Reports, Lunit BP, VCBeat)

Analysis of Largest Customers (Data Sources: Company Prospectuses, Annual Reports, Lunit BP, VCBeat)

Corporate IPO data reflects the current state of commercialization for the most mature AI technologies; however, these commercially deployed technologies may not necessarily hold the greatest potential, and the resulting revenue does not accurately predict a company’s future profitability. This report provides a comprehensive analysis of the four primary application scenarios where medical AI currently plays a significant role, exploring the development status and profitability of the AI industry beyond the scope of IPOs. This article uses AI-enabled medical imaging as a case study for illustrative analysis.

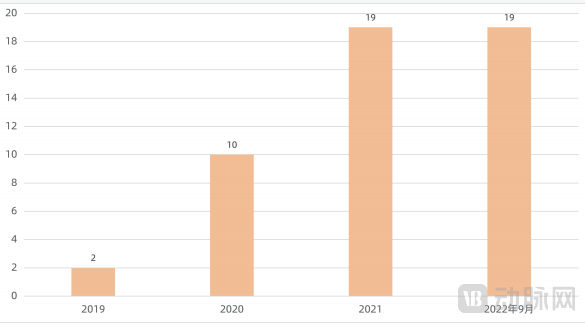

As a bellwether for the development of the medical AI industry, a total of 49 AI products from 28 companies had obtained Class III Medical Device Registration Certificates by September 1, including 29 software products powered by deep learning algorithms. Overall, the National Medical Products Administration (NMPA) has been accelerating the approval of Class III certifications for AI medical devices, thereby hastening the commercialization of medical AI.

Number of Certifications by Year (Source: VCBeat)

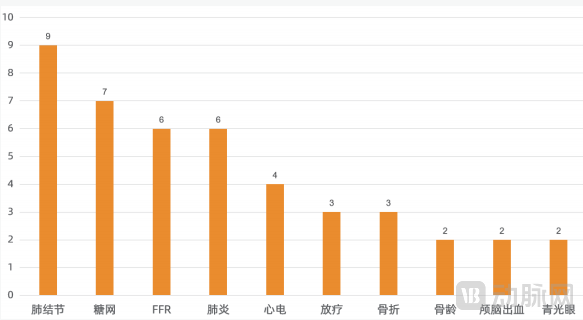

The total number of Class III medical device certificates has been steadily increasing over time, accompanied by intensifying product homogenization. A total of 49 AI products cover 15 auxiliary diagnosis scenarios. Among these, there are nine AI solutions for pulmonary nodule detection based on CT imaging, followed by seven AI products for diabetic retinopathy diagnosis using fundus cameras, with seven companies having obtained market access approval. CT-FFR and CT-based pneumonia diagnosis follow closely, each with six Class III certificates. In the field of AI-enabled ECG analysis, Lepu Medical uniquely holds four Class III certificates. Additionally, in the five scenarios of radiotherapy, fracture detection, bone age assessment, intracranial hemorrhage, and glaucoma, AI products from more than one company have passed regulatory review and approval.

Class III Medical Device Certifications by Disease Category (Source: VCBeat)

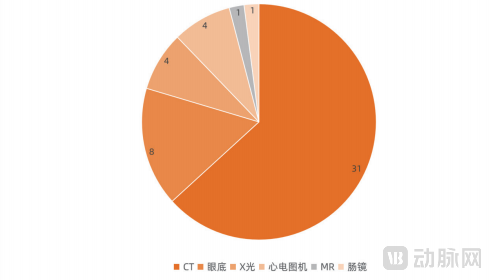

Further Discussion on Devices for Medical AI Applications. Currently, data used by all approved products are derived from six types of devices: CT scanners, fundus cameras, X-ray machines, electrocardiogram (ECG) machines, MRI scanners, and colonoscopes. The CT imaging scenario offers a broad scope of application, high clinical value, a large patient population, and substantial volumes of standardized data, making it the preferred choice for AI companies’ R&D efforts. Consequently, AI solutions for CT, with 31 approved products, far outnumber those for other devices. In contrast, MR images are more complex and available data volumes are relatively limited, while standardization of colonoscopy images remains challenging; as a result, only one AI product has been approved for each of these two modalities.

Statistical Classification of Medical AI-Enabled Devices (Data Source: VCBeat)

Ultrasound is a key sector where AI companies may soon achieve breakthroughs in regulatory review and approval. Ultrasound data adds a temporal dimension to the two-dimensional data generated by CT and DR. Moreover, ultrasound examinations often produce a large number of frames with no diagnostic value. AI must therefore identify the value of each frame in a dynamic environment, compare them against one another, and extract the responsible view at specific moments to enable effective image analysis.

The landscape for pathology AI is relatively challenging, facing obstacles beyond the regulatory review and approval system. As imaging-assisted diagnosis occupies the midstream of the industry chain, it relies on the standardization of upstream imaging equipment. However, mainstream domestic electron microscope manufacturers have not established unified data standards, nor do they have sufficient incentive to modify their devices in accordance with industry-specified data standards, leading to certain issues with data interoperability. In this context, some pathology companies, such as Diyingjia, Kunyuan Fangqing, and DeepThinking, have obtained Class II medical device certifications, enabling them to conduct AI sales at a certain scale.

Overall, as the regulatory approval process becomes increasingly mature, the development costs of medical AI are gradually becoming more controllable, and more imaging AI solutions targeting niche scenarios are progressively obtaining Class III medical device certificates issued by the Center for Medical Device Evaluation (CMDE). For instance, MicroVision Medical’s research on colorectal polyps and Siemens’ work on thoracic spine imaging have both secured Class III medical device certifications. In the future, application scenarios for medical AI will continue to expand alongside the maturation of the review and approval processes, enabling medical AI companies to better mitigate risks and effectively reduce R&D costs.

AI solutions that have achieved market access can pursue commercialization while simultaneously navigating pricing approval and national medical insurance reimbursement processes. Currently, companies are actively promoting provincial and municipal pricing approvals. For instance, Keya Medical’s “DeepVessel FFR” has completed pricing procedures in 11 provinces and municipalities, including Beijing, Hebei, Shandong, Zhejiang, and Jiangsu. PulseMed’s QFR has obtained pricing approval in 11 provinces and municipalities. Airdoc’s fundus AI has secured pricing access in five provinces and municipalities. Regarding medical insurance coverage, in April 2021, the Shanghai Healthcare Security Administration included 28 new items, such as “AI-assisted therapeutic technologies,” within the scope of Shanghai’s basic medical insurance coverage. The reimbursable scope for “AI-assisted therapy” is limited to radical prostatectomy, partial nephrectomy, total hysterectomy, and radical resection of rectal cancer.

Although there have been certain breakthroughs in pricing approval and national medical insurance reimbursement inclusion, these achievements have not yet reached scale. We believe that while domestic AI companies aspire to maintain their independence by leveraging both tendering/bidding and direct sales models, it may be more conducive to the rapid development of imaging AI in the future to delegate channel management to medical imaging equipment manufacturers and PACS vendors, thereby allowing AI firms to focus on R&D within their respective niche segments and fostering a more refined industry division of labor.

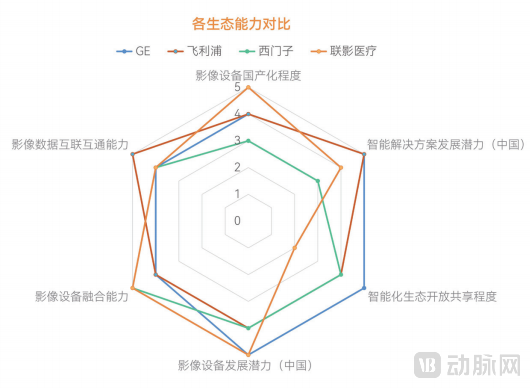

Currently, the relatively mature medical imaging ecosystem in China is primarily built by four companies: GE Healthcare, Philips Healthcare, Siemens Healthineers, and United Imaging Healthcare. Each company has its own strengths in terms of the localization level of imaging equipment, the development potential of intelligent solutions (in China), the openness and sharing level of the intelligent ecosystem, the development potential of imaging equipment (in China), the integration capability of imaging equipment, and the interoperability of imaging data.

Comparison of Ecosystem Capabilities (Data Source: VCBeat)

Beyond the four industry leaders mentioned above, medical imaging equipment manufacturers such as Neusoft Medical and SynoVision are also promoting the coordinated development of software and hardware, while IT giants like Fujifilm (China) and Winning Health are striving to expand their ecosystems. The competition between these ecosystems will be a long-term endeavor, during which AI medical imaging companies may achieve profitability at a faster pace.

Like cross-disciplinary technologies such as the internet and 5G, AI is one of the few technologies in this era capable of independently forming a comprehensive product ecosystem. However, its application within the healthcare sector remains relatively limited. Currently, hospitals are gradually developing a systematic understanding of medical AI, regulatory frameworks are being progressively refined, and the range of applicable scenarios for AI products offered by enterprises continues to expand.

Under the new circumstances, medical “AI+” is continuously evolving into medical “+AI,” with its application scenarios expanding from diagnosis and treatment to research, insurance, and other areas, thereby creating new market growth.

Expanding outward from medical institutions as the initial point of deployment is not only an effective strategy for AI to tap into incremental markets, but also a passive response to the cautious regulatory review and approval processes governing medical devices. In summary, the development of relatively mature incremental AI products in healthcare is currently concentrated in the consumer (C-end) sector and among insurers and pharmaceutical companies within the business (B-end) sector. Imaging AI has downplayed the classification of AI as a medical device, while knowledge graphs based on Natural Language Processing (NLP) have incorporated multi-dimensional data extending beyond the traditional healthcare domain.

“Going Global” is another pathway for AI companies to seek incremental market growth. Currently, enterprises with overseas expansion plans include those specializing in AI-driven drug discovery and AI-based medical imaging. AI companies in the drug discovery sector primarily collaborate with overseas pharmaceutical firms to assist in R&D, leveraging AI capabilities to optimize and accelerate certain stages of the new drug development process. The situation for AI-based medical imaging companies is relatively more complex. Market access, as the starting point for commercialization, serves to some extent as a measure of an AI company’s capability in overseas expansion.

Statistics on CE, FDA, and PMDA Certifications

Statistics on CE, FDA, and PMDA Certifications

(Excluding medical imaging equipment manufacturers; Source: VCBeat Research Institute)

Furthermore, the public-welfare pathway, initially adopted as a transitional strategy when medical imaging AI struggled to navigate the National Medical Products Administration’s (NMPA) review and approval landscape prior to 2020, has now become a significant avenue for AI companies seeking new growth opportunities. By implementing solutions through public-welfare initiatives, medical imaging AI enterprises can not only support national efforts in early screening for diseases such as cancer and ophthalmic conditions but also help their AI products gain early market adaptation.

The above is an excerpt from the main content of the report. The complete framework of the report is as follows:Scan the QR code to download the full report for free。

Chapter 1: The Core Value of Medical AI: The Foundation for Cost Reduction and Efficiency Enhancement, and the Potential to Reshape the Healthcare System

1.1 Initial AI: Cost Reduction and Efficiency Enhancement Empowered by Intelligence

1.2 Advanced AI: Disruptive Value Creation

1.3 High Barriers, Long Accumulation: Great Potential for Medical AI

Chapter 2: Multi-fold Revenue Growth, Just One Step Away from Profitability

2.1 Imaging Companies Successively Go Public; New Drug R&D Becomes the Primary Target in the Primary Market

2.2 Multiple Companies Enter the Secondary Market, with AI Imaging Remaining the Mainstream

Chapter 3 Beyond the IPO: Multiple Factors Influence Commercial Monetization, and Profitability Requires Overcoming These Hurdles

3.1 Current Status of AI Development in Medical Imaging and Factors Influencing Commercialization

3.2 Current Status of AI Development in Hospital Information Systems and Factors Influencing Commercialization

3.3 Current Status of AI Development in New Drug R&D and Factors Influencing Commercialization

3.4 Current Status of AI Development in Medical Robots and Factors Influencing Commercialization

Chapter 4: New Scenarios, New Models—Opening a New Chapter in the Development of Medical AI

4.1 Seeking New Blue Oceans in AI

4.2 The Future Form of Medical AI Enterprises

4.3 Venturing Overseas to Seek Market Growth

4.4 Leveraging Public Welfare as a Nexus: Integrating Social Value with Commercial Value

Chapter 5 Corporate Case Studies