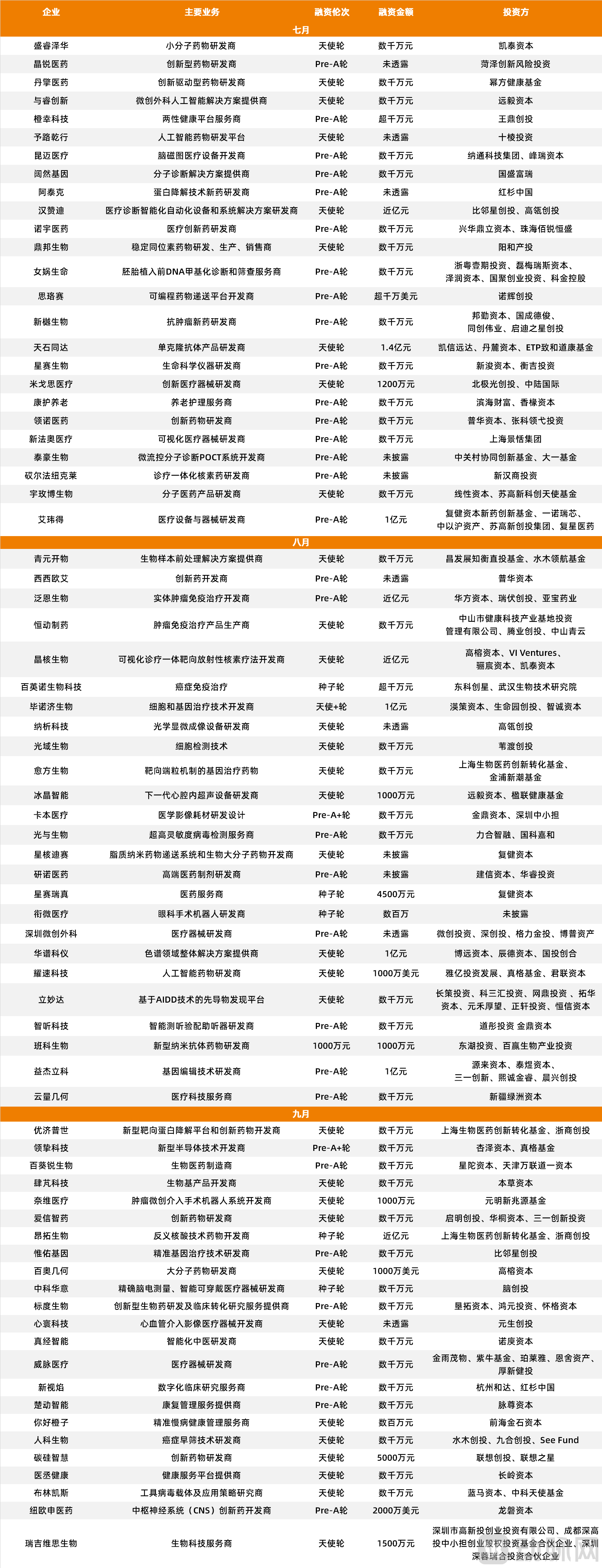

73 Early-Stage Fundraisings Totaling Over RMB 4.7 Billion: What Is Q3's Healthcare Investment Focus?

From 2021 to 2022, the once-booming healthcare market rapidly cooled to a winter-like state within just over a year, with many leading companies’ IPOs either breaking their issue price or being postponed.

However, the jittery sentiment in the secondary market has not dampened the fervor surrounding early-stage healthcare investments.

2022YearQ3Overview of Early-Stage Healthcare Financing

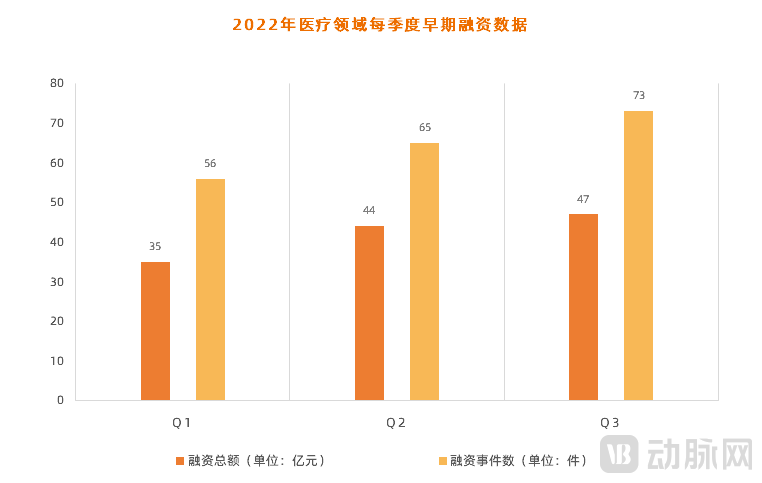

According to incomplete statistics from VCBeat’s Orange Bureau, China’s healthcare sector in 2022Q3 saw 73 early-stage financing events, with a total funding amount of RMB 4.7 billion。

Quarterly Early-Stage Financing Data in the Healthcare Sector, 2022

A cross-sectional comparison reveals that both the number of early-stage financing deals and the total financing amount remained at high levels in 2022, showing a continuous upward trend. Compared with Q2, Q3The number of financing events increased by 3, with the total financing amount rising by RMB 800 million, representing an increase of over 18%.。

In fact, many industry insiders believe that healthcare financing and investment are facing a capital "winter," yet the early-stage healthcare market is moving against this trend and continues to heat up.

What trends can be observed from early-stage financing and investment data in Q3? Which early-stage sectors have attracted significant capital attention? After a period of market consolidation, what new investment logics have emerged among institutional investors? To address these questions, VBInsight has conducted an in-depth analysis of early-stage financing and investment activities in Q3.

Which sectors are viewed favorably?

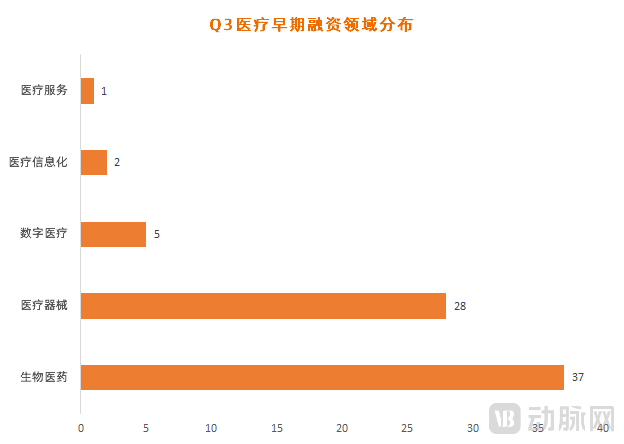

According to statistics from Chengguo Bureau, among the 73 companies that completed early-stage financing in Q3,Biopharmaceutical companies dominate the landscape, with a total of 38 firms, accounting for 52%.;Medical device companies followed closely, with a total of 27 firms, accounting for 37%.; other medical sectors account for approximately 10% of the share, but within this 10%,There are five companies engaged in digital healthcare.。

Q3 Distribution of Early-Stage Financing in the Healthcare Sector

Such allocation across financing sectors is, in fact, a long-standing pattern for early-stage healthcare projects.

Currently, the wave of domestic substitution in China’s healthcare sector is accelerating, with significant strides even being made toward first-in-class (FIC) innovations. The high barriers to entry and innovative nature of “hard tech” will undoubtedly enhance the long-term vitality and growth potential of China’s medical industry. Consequently, the biopharmaceutical and medical device sectors, infused with “hard tech” DNA, are naturally attracting substantial capital attention.

As Dr. He Weiwu, Founding Partner of the ETP Zhihe Daokang Fund, stated: “Technological capability is one of our golden criteria for selecting portfolio companies.”

Based on this, VCBeat has summarized the current core businesses of healthcare companies that secured early-stage financing in Q3, identifying three hot sectors for early-stage healthcare projects.

Q3 Small-Molecule Drug Companies That Completed Early-Stage Financing

According to statistics, among the 37 pharmaceutical companies that secured early-stage financing in Q3,Ten companies are engaged in small-molecule drug R&D, accounting for over 27%。

Compared with large-molecule biologics, small-molecule drugs offer distinct advantages in drug development, including low molecular weight, lack of immunogenicity, high absorbability, mature manufacturing processes, the ability to penetrate cell membranes, and ease of storage and transportation.

It is reported that 10 small-molecule drug R&D companies completed financing in Q3,All focused on undruggable targets or novel targets, focusing on four key areas: protein degrader drugs, nanomedicines, antisense nucleic acid drugs, and AI-driven drug R&D, among whichFour companies are focused on protein degradation drugs., highly favored by capital.

In fact, small-molecule drugs have evolved from the era of compound development (e.g., penicillin and norfloxacin) into the targeted therapy era.In 2021, the global market size for innovative small-molecule drugs was approximately $180 billion, with China’s market accounting for about $40 billion, representing over 20% of the global market., future market expectations may be even higher, so focusing on specific targets is a goal driven by both technology and the market.

Protein degradation technology has garnered significant enthusiasm in the small-molecule drug sector because it overcomes limitations such as target restrictions and poor resistance to traditional small molecules, making it particularly promising for tackling the challenge of “undruggable targets.”

As of May 2022, more than 100 protein degrader projects worldwide had completed proof-of-concept studies and were in the preclinical stage, with 31 having entered clinical trials. In China, 20 to 30 companies have actively established their presence in the protein degrader field.

Next, let’s look at protein degrader companies that completed financing in Q3, such as the one led by Sequoia China in July.Atek, is one of the few startups focusing on ATTEC protein degradation technology; it also raised tens of millions of yuan in financing in September.Uji Pushi, its in-house protein degradation pipeline is dedicated to expanding the development of PROTACs and molecular glue drugs for autoimmune diseases and cancer.

It is reasonable to believe that, as the latest frontier breakthrough in small-molecule drugs, protein degraders will usher in the next golden age of small-molecule therapeutics.

Q3 CGT Companies That Completed Early-Stage Financing

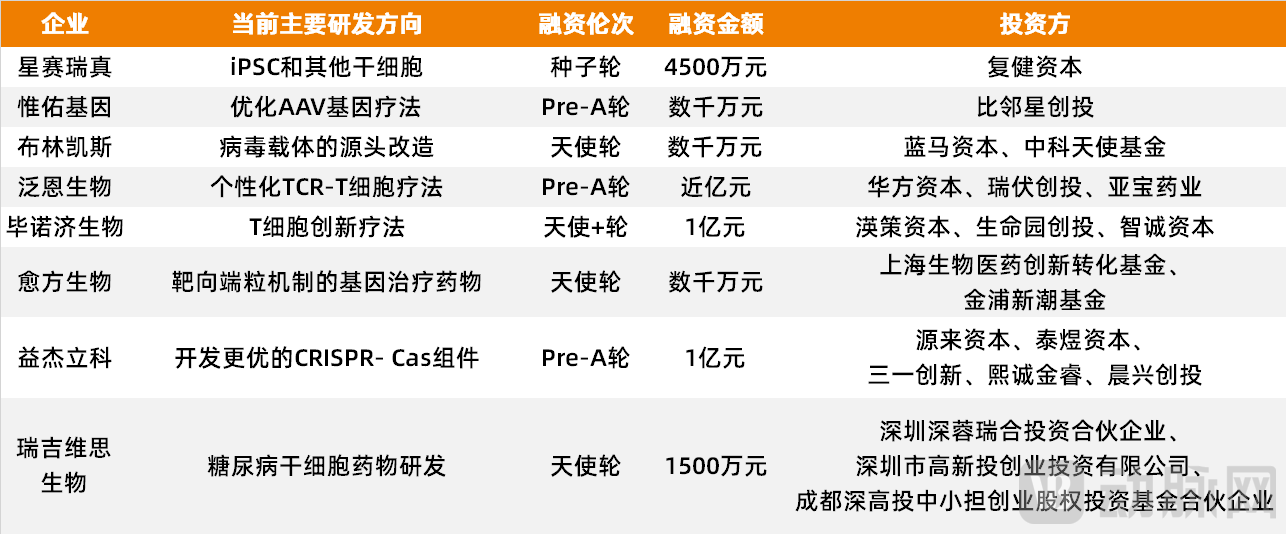

CGT is a niche sector that has garnered significant attention in the biopharmaceutical industry in Q3. According to statistics, in Q3, early-stage financing was completed byThere are 8 CGT companies, accounting for nearly 22%.。

Compared to the fields of large-molecule and small-molecule therapeutics, cell and gene therapy (CGT), as an emerging modality for drug development, centers on gene therapy vectors. It offers durable efficacy after a single administration, targets a broad range of indications, and can address refractory diseases, thereby providing incremental growth to China’s rare disease market.

Of the eight CGT companies that secured financing in Q3,Half of the companies are focusing on stem cells, particularly innovative T-cell therapies.。

In recent years, while cell therapies involving stem cells (including T cells) have achieved significant breakthroughs, their clinical application still faces a series of challenges: the traditional ex vivo manufacturing processes for CAR-T and TCR-T cells are complex, entail high treatment costs, and cannot support large-scale production; furthermore, the insufficient specificity of cultured stem cells results in suboptimal therapeutic efficacy and compromised safety.

In this regard, the majority of CGT companies that secured financing in Q3 have targeted the pain points of stem cell therapy, offering unique solutions.

For instance, those that have secured nearly RMB 100 million in Pre-A round financingFanen Biotech, comprehensively optimized the manufacturing process for personalized TCR-T cells and completed the development of GMP-compliant production processes, enabling the preparation of personalized polyclonal TCR-T cells simultaneously targeting multiple tumor antigens for patients within approximately six weeks.

and those that have secured RMB 100 million in Angel+ round financingBinoji Bio, deeply committed to innovative T-cell therapies, has established proprietary platforms for the development of targets regulating T-cell fate and for T-cell engineering, dedicated to developing cell therapies based on multiple T-cell types.

In addition to stem cell therapies (ex vivo edited cell products), CGT also encompasses product categories such as viral vectors, plasmids, bacterial vectors, and gene editing systems, each of which currently faces its own clinical challenges.

However, the challenge is also the “blue ocean.” According to data from Frost & Sullivan,In 2022, the market size of China’s cell and gene therapy (CGT) sector is projected to increase by 1,025.21% year-on-year, and it is expected to maintain a high growth rate of over 100% in the following years. By 2025, the market size of China’s CGT sector is anticipated to reach RMB 17.885 billion.。

Therefore, from the perspective of industrial development, the CGT market is both new and large, with the potential to become a golden track in the next decade.

Q3 IVD Companies That Completed Early-Stage Financing

In the medical device sector, capital continues to focus on the evergreen track of IVD (in vitro diagnostics). According to statistics, among the 28 medical device companies that secured early-stage financing in Q3,There are 11 IVD companies, accounting for nearly 40%.。

The IVD sector encompasses numerous subfields. Based on differences in test indicators, specimen types, and underlying principles, the IVD market has evolved into a tripartite structure dominated by clinical chemistry diagnostics, immunoassay diagnostics, and molecular diagnostics.

Among IVD companies that completed early-stage financing in Q3,There are six companies engaged in molecular diagnostics.。

For example, those that have secured tens of millions of yuan in Pre-A round financingLight and Biology, our independently developed ultra-bright rare-earth upconversion nanoparticle fluorescent probes, whose single-molecule immunoassay performance is highly suitable for the discovery and detection of novel biomarkers for various diseases; having secured tens of millions of yuan in Pre-A round financingKuoRan Genomics, pioneering a unique "NGP (Next-Generation Pathology) + NGS (Next-Generation Sequencing)" model. It provides a one-stop molecular diagnostics solution for multiple application scenarios.

Molecular diagnostics is a quintessential example of personalized medicine. It employs molecular biology techniques to detect changes in the structure or expression levels of genetic material, and is primarily used in the detection of infectious diseases, eugenics screening, sexually transmitted disease (STD) screening, cancer screening, and genetic disorder screening. It is characterized by its precision, speed, and simplicity.

Unfortunately, China’s molecular diagnostics industry started relatively late, and the mid-to-high-end segments of its supply chain have long been dominated by leading foreign companies. Leveraging their technological and brand advantages, firms such as Roche and Abbott have captured the majority share of the domestic mid-to-high-end market.

However, against the backdrop of precision medicine, and driven by factors such as advancements in domestic molecular diagnostic technologies, policy support, and strong investor interest, domestically produced molecular diagnostic instruments are transitioning from the introduction stage to the growth stage, with numerous Chinese companies vying for market share in the molecular diagnostics sector.The market size of molecular diagnostics in China increased from RMB 2.54 billion in 2013 to approximately RMB 13.2 billion in 2019, with an average annual growth rate roughly twice the global average.。

Thus, it is evident that the technological boundaries of molecular diagnostics in China will be gradually expanded, positioning it as one of the most promising segments within the IVD industry.

Invest in People or Technology?

Choosing the right track is only the first step; to ensure long-term competitiveness in a prime sector, startups must return to focusing on team composition and technological R&D.

The debate over whether to invest in people or in technology has long persisted in the early-stage investment and financing market.

From an investment perspective, high-quality founding teams with interdisciplinary backgrounds and composite R&D experience can provide multi-faceted, high-caliber solutions during the company’s growth phase. Such teams are better equipped to mitigate startup risks, while their profound scientific research accumulation lays a solid foundation for future technological breakthroughs.

that secured nearly RMB 100 million in angel financing in AugustJinghe Biotechas an example, it is a biopharmaceutical company focused on the development of theranostic targeted radionuclide therapy (TRT).

Crystal Core Biologics was co-founded in 2021 by four founders, including Dr. Yu Haihua and Dr. Wang Yu. Dr. Yu previously worked at GSK, where he engaged in new drug R&D for over a decade, and later joined Huayi Technology to lead the Molecular Imaging and Drug Research Institute. Dr. Wang has more than 20 years of experience in the development of various targeted conjugate drugs, such as small-molecule radiopharmaceuticals, at internationally renowned pharmaceutical companies including Endocyte and Eli Lilly, and possesses extensive experience in new drug development with multiple US NDAs and INDs.

The proceeds from this round of financing will be primarily used to accelerate the clinical development of Crystal Nuclear Biopharma’s multiple innovative targeted radiopharmaceuticals in the pipeline and to upgrade its radiopharmaceutical R&D platform.

The lead investor, Gaorong Capital, believes that Jinghe Biologics'The founding team hails from multiple leading companies in the industry and possesses R&D experience with internationally marketed radiopharmaceuticals,This will provide strong innovative momentum and competitive advantages for its later-stage research and development.

From an investment perspective, innovative technologies are essential for the iteration of the healthcare industry. Adopting new technologies offers the potential to enter untapped markets and secure market share at an early stage.

which secured tens of millions of yuan in angel financing in AugustOptical Domain Biologyas an example, it has developed the world’s first in vivo flow cytometry (IVFC) technology. Unlike traditional ex vivo detection methods, this technique enables non-invasive, real-time, dynamic, continuous, and quantitative detection/monitoring of target substances such as cells, molecules, and nanoparticles in the circulatory system of humans or animals, without the need for blood sampling. It directly reflects the true molecular, physiological, metabolic, and pharmacological parameters and status within the internal environment of humans or experimental animals.

The innovation, feasibility, and application value of this technology have been recognized by peers and experts both domestically and internationally. Related research findings have been published in prestigious international journals such as Nature, Nature Medicine, Cell, Blood, Light: Science & Applications, Cancer Research, and ACS Nano. To date, more than 100 academic papers have been published, with a cumulative impact factor of 887, including over 30 articles with an impact factor greater than 10.

Weidu Ventures, the exclusive investor, has taken an interest inGiven its high academic standing and technological advantages in the field of biomedical photonics, its research achievements are believed to have the potential to disrupt traditional in vitro cell detection methods.It is reported that the IVFC-1000 series of research instruments, soon to be launched by Guangyu Biology, will pioneer a novel method for in vivo cytological detection and represent the world’s first commercial instrument based on IVFC technology.

Overall, investing in people and investing in technology each have their own advantages, and cannot be generalized.

In the early stages of a project’s growth, high-quality founding teams bring extensive expertise in R&D and commercialization; however, their core technologies may still be under development or require prolonged validation. While nascent innovative technologies can serve as the core competitiveness of startups, it remains uncertain whether subsequent R&D advancement and commercialization will proceed smoothly.

“No one is perfect.” This saying also applies to early-stage projects in the medical field.

When making investment decisions, investors should carefully consider whether they can effectively leverage the “strengths” of startups and whether they have the capability to help address their “weaknesses.”

Meanwhile, it is crucial to recognize that supporting early-stage projects in the healthcare sector is inherently a journey marked by both risks and rewards, with no one-size-fits-all roadmap. Understanding the logic of industry development and seizing future market share in healthcare are essential competencies that both startups and investment institutions must continually refine.

Investment Institutions in Fierce Competition

According to statistics from VCBeat’s Orange Fruit Bureau, among the 73 early-stage medical financing deals completed in Q3,A total of 132 investment institutions participated, with no investors demonstrating sustained activity.。

In addition to top-tier firms such as Sequoia Capital and Hillhouse Capital, as well as early-stage-focused investors like Northern Light Venture Capital and Proxima Ventures, which led early-stage deals, VCBeat’s Orange Data Bureau observed several noteworthy investment trends in the early-stage financing market during Q3:

One is that large pharmaceutical companies are personally investing in early-stage companies.

WithYabao PharmaceuticalFor example, as a developer, manufacturer, and distributor of pharmaceuticals and general health products, its patented flagship product, Dinggui Erqitie (Pediatric Umbilical Patch), along with renowned products such as Honghua Injection and Zhenju Jiangya Tablets, have long enjoyed nationwide acclaim in China.

In August, it participated in an investment focused on personalized TCR-T cell preparation.PanEnbio。

Looking again at China's largest R&D, manufacturing, sales, and operational platform provider in orthopedics—Naton Medical Group, after two decades of rapid development, it has completed a systematic layout across the entire industry chain in the field of orthopedic implants, encompassing independent R&D, industrialized production, large-scale marketing, and application in medical services.

Its July assistance for a novel magnetoencephalography system based on quantum sensing technologyKunmai MedicalCompleted the Pre-A round of financing.

As a well-established enterprise in the pharmaceutical sector, why does it proactively engage in investing in early-stage healthcare projects?

This move, on the one hand, demonstrates major pharmaceutical companies’ recognition of early-stage innovative technologies and their development prospects, reflecting a broad industry consensus on investing early and in small-scale ventures; on the other hand, it may stem from the fact that these companies have reached the growth ceiling in their existing therapeutic areas, necessitating the exploration of new business lines to stimulate corporate development and iteration.

Moreover, the abundant R&D resources and comprehensive product pipelines of large pharmaceutical companies can provide startups with a “beginner’s guide,” meaning their role is far more complex than that of mere investors.

Second, research institutes’ own “funding pools” have begun to provide “fresh capital.”

For example, providing Qingyuan Kaiwu with tens of millions of yuan in angel-round financing in AugustShuimu Linghang FundandChangfa Zhan Zhiheng Direct Investment Fund, all affiliated with the Beijing Tsinghua Industrial Development Institute; andWuhan Institute of Biotechnologydirectly participated in the seed funding round of Baiyingnuo Biotechnology, which exceeded RMB 10 million.

Currently, as the incubation systems of research institutes become more refined, comprehensive “software” and “hardware” support have gradually become the “standard configuration” for early-stage projects originating from these institutions.

Third, a large number of government-backed fund-of-funds have been actively entering the early-stage market.

Among the institutions participating in the early-stage financing round in Q3, there appearedHai Bio-Pharmaceutical Innovation and Commercialization Fund, Life Science Park Investment Fund, Zhangjiang Lingyi Investment, SDIC Chuanghe, Zheshang Venture Capitaland other figures.

The entry of state-owned capital institutions and funds reflects the policy orientation of national and local governments, highlighting their emphasis on early-stage healthcare projects.

In addition to participating in early-stage investment, various regions have also provided multifaceted “support” for the development of early-stage medical projects. For instance, provinces and municipalities across China have actively established industrial parks and incubators to offer comprehensive strategic guidance for the commercialization of innovative technologies.

In summary, while various investment institutions and funds are scrambling to secure a first-mover advantage in early-stage investments, gaining such an advantage does not necessitate frequent deal-making or excessive capital infusion.

Unlike the standout performance in the first half of the year, when Sequoia China made 12 investments and Qiming Venture Partners made eight, the early-stage investment and financing market in Q3 saw no clear leader.

In fact, after a period of consolidation, investment institutions have developed a deeper understanding of the development logic behind early-stage projects and have gradually established a set of optimal investment models and processes.

HillhouseRecently Announced the Official Launch of“Aseed+” Seed ProgramIt serves as an excellent reference.

“Aseed+” Seed Program aims to invest in approximately 100 seed-stage enterprises over a three-year period, focusing on integrating pre-investment, investment, and post-investment stages to deliver integrated services encompassing startup incubation, market validation, acceleration, industry matchmaking, and follow-on financing.

As Li Liang, Founding Partner of Hillhouse Capital, stated, “We aim to provide entrepreneurs with ample confidence at the early stage, enabling them to navigate through the ‘valley of death.’”

Previously, Hillhouse helped BayOmics translate its vision from concept to reality, providing support in company registration, team recruitment, integration of upstream and downstream industrial resources, and the establishment of strategic partnerships with renowned pharmaceutical companies both domestically and internationally. Thus, a cutting-edge biotech startup was born.

As early as August,Sequoia's Startup Accelerator: YU, providing Chinese entrepreneurs from angel round to Series A with systematic entrepreneurship courses and resource services exclusively developed by Sequoia.

YU is regarded as a significant transformation for Sequoia, from a “capital investor” to a “service partner.”

The strategic adjustments made by leading investment firms undoubtedly do not prove that early-stage investing is the right choice, butAfter making the investment, it is essential to provide robust “post-investment services” and serve as a “deeply engaged companion” to startups; this is the key to unlocking the value of early-stage projects.。