Amid Industry Crackdown, Domestic Photonic Aesthetic Medical Devices Surge with Backing from Top-Tier VCs

Huadong Medicine

Large Comprehensive Pharmaceutical Product Developer

Solta Medical

R&D Manufacturer of Beauty Medical Devices

Haohai Biological Technology

Medical Biomaterials R&D and Manufacturer

Fumeilei Medical

R&D Developer of Medical Aesthetic Devices

Candela

Medical Aesthetic Device Developer

Under the tailwind of the “appearance economy,” the medical aesthetics industry has remained hot for years, but it has recently encountered significant challenges: reports indicate that relevant authorities will conduct inspections across the upstream, midstream, and downstream segments of the sector. In response, the share prices of leading companies Imeik and Bloomage Biotech dropped by more than 10%.

Nevertheless, the medical aesthetics industry continues to attract significant attention from investors amid pressure, driven by the sustained growth in demand. Reports from third-party platforms such as So-Young and Gengmei indicate that not only are an increasing number of women opting for cosmetic surgery and anti-aging treatments, but men are also actively engaging in medical aesthetic procedures. Moreover, younger generations, particularly those born in the 1990s and 2000s, have become a key force propelling the rapid expansion of the medical aesthetics market.

Sustained growth on the demand side has naturally bolstered development on the supply side. VCBeat’s statistics reveal that since last year, more than 30 upstream companies in the medical aesthetics sector have secured financing, attracting over RMB 2 billion in investment. Top-tier institutions—including Tencent, Xiaomi, SoftBank, IDG Capital, Northern Light Venture Capital, Goldman Sachs, Hillhouse Capital, ZhenFund, and Yunfeng Capital—have consecutively invested in these enterprises. Among them,Photoelectric medical aesthetics is one of the key niche sectors attracting significant capital investment, and it remains a vibrant segment despite the overall pressure facing the medical aesthetics industry.

“Currently, photoelectric medical aesthetic devices in China are predominantly imported, leaving substantial room for domestic brands to capture market share,” Wang Xingchun (a pseudonym), a senior investor in consumer healthcare, told VCBeat. “From the evolution of the global market, photoelectric medical aesthetic companies demonstrate strong profitability. For instance, Solta Medical, the maker of Thermage and currently pursuing an IPO, generated annual revenue exceeding $200 million.”

More importantly, a cohort of high-quality innovative enterprises is gradually emerging in the mid-to-high-end medical device sector, offering investors a broader range of investment targets compared to a few years ago.Data from the VCBeat database shows that photoelectric medical aesthetics companies, including Fumeilei Medical, Nanjing Baifu, Yaguang Medical, Chongqing Jingyu, Viora, High Technology Products, and Alma Lasers, have recently secured financing.

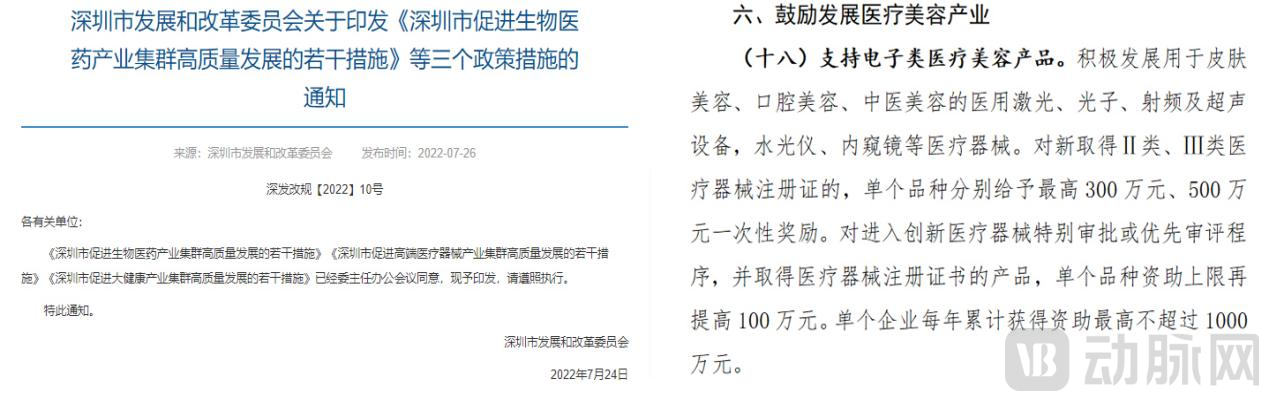

On the policy front, support is also being intensified. Taking Shenzhen as an example, the "Several Measures to Promote High-Quality Development of the Big Health Industry Cluster in Shenzhen," issued by the Shenzhen Municipal Development and Reform Commission this July, explicitly states that support will be provided for electronic medical aesthetic products, with active development encouraged for medical devices such as medical lasers, photon, radiofrequency, and ultrasound equipment used in dermatological aesthetics, dental aesthetics, and traditional Chinese medicine (TCM) aesthetics. The release of these policies is beneficial to the development of domestically produced photoelectric medical aesthetic devices.

(Image source: Official website of the Shenzhen Municipal Development and Reform Commission)

(Image source: Official website of the Shenzhen Municipal Development and Reform Commission)

Amidst the immense popularity, why has energy-based aesthetic medicine risen so prominently? What are the underlying reasons? And what are the future evolutionary trends? To address these questions, VCBeat has analyzed industry data and interviewed multiple experts to shed light on the answers.

The Pursuit of Beauty Is Universal. In recent years, as public acceptance of medical aesthetics has grown, "light medical aesthetics"—a non-surgical category of aesthetic treatments—has gained immense popularity among young people due to its inherent advantages, including minimal invasiveness, rapid recovery, and low risk.

According to the “2021 China Medical Aesthetics Anti-Aging Consumption Trends Report” released by Xinhua Finance in collaboration with SoYoung,In the light medical aesthetics market, energy-based device procedures are the most favored, with 86.23% of consumers seeking anti-aging treatments opting for such procedures.From the perspective of market growth, the consumer market size for energy-based medical aesthetics is projected to reach RMB 50.812 billion in 2025 (as estimated by Gaohe Investment Research Center), with a CAGR (Compound Annual Growth Rate) of 13.61%.

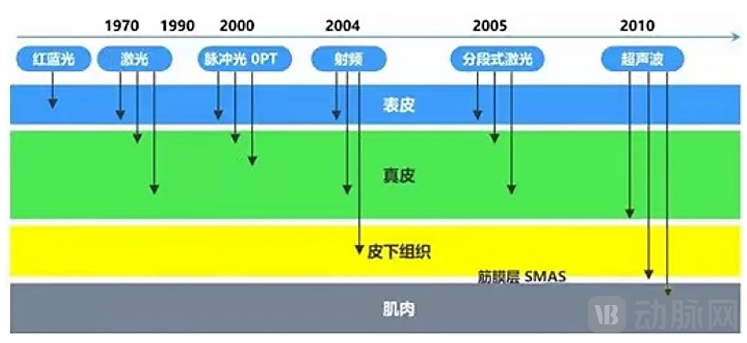

“Energy-based aesthetic medicine, as a key branch of the medical aesthetics industry, primarily refers to energy-source-based medical aesthetic procedures/products,” said Wang Xingchun, a senior investor in consumer healthcare.Photoelectric medical aesthetic devices deliver energy in the form of lasers, radiofrequency, and ultrasound to the skin, with the aim of improving the skin condition of individuals seeking aesthetic enhancement.

(Schematic diagram of skin layers penetrable and affected by different devices. Image source: Zhongtai Securities Research Institute)

(Schematic diagram of skin layers penetrable and affected by different devices. Image source: Zhongtai Securities Research Institute)

Specifically, when photoelectric energy acts on different skin layers, it can address corresponding skin concerns. For instance, acting on the epidermis, it can achieve effects such as acne treatment, spot removal, and skin whitening; acting on the dermis, it can stimulate collagen regeneration, thereby achieving skin tightening and anti-aging benefits; and when acting on the subcutaneous tissue, it can facilitate fat reduction and body contouring.

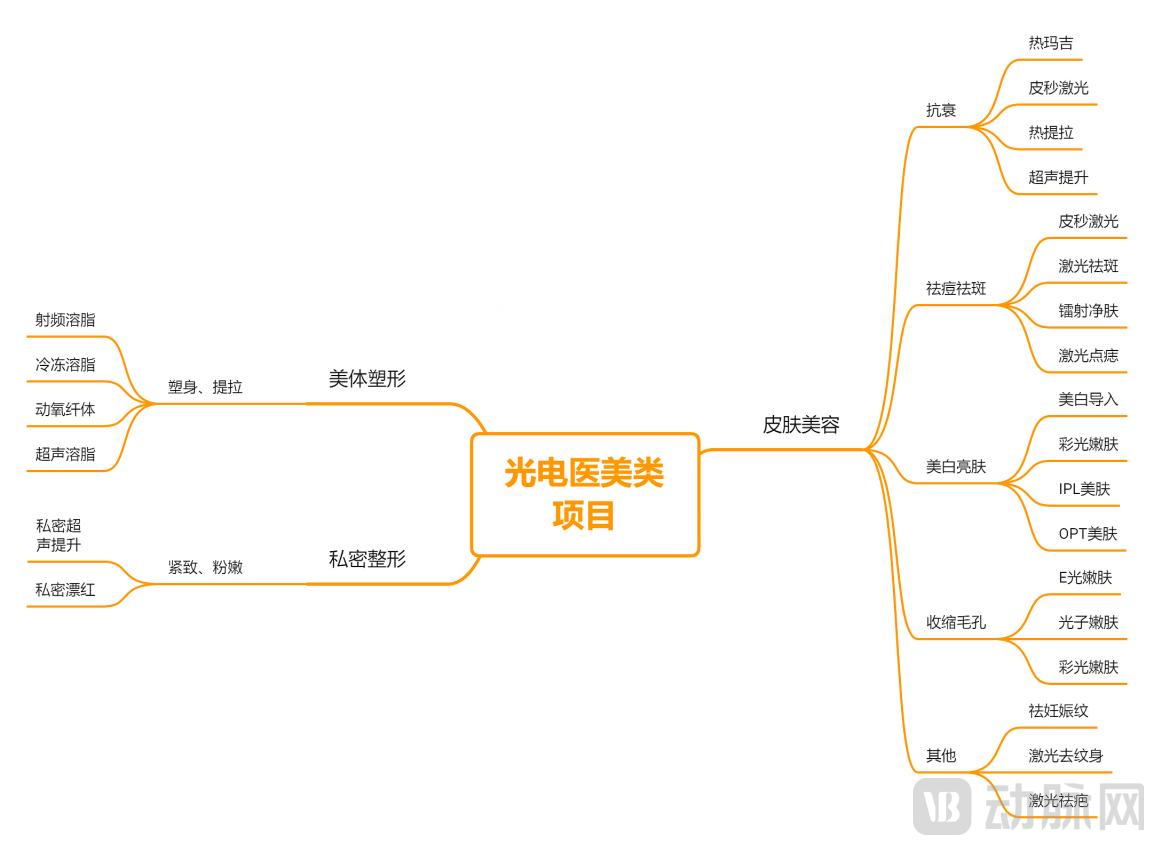

“Currently, the mainstream optoelectronic devices on the market include Thermage, intense pulsed light (IPL) skin rejuvenation, ultrasound lifting, and laser pigmentation removal, primarily covering three major application scenarios: facial aesthetic medicine, body contouring, and intimate plastic surgery.“Huang Feng, a senior practitioner in the medical aesthetics industry, told VCBeat that energy-based medical aesthetic procedures have become highly popular among beauty seekers due to their rapid efficacy, short post-operative recovery time, and long-lasting results.”

(Mainstream photoelectric medical aesthetic procedures on the market; graphic by VCBeat)

(Mainstream photoelectric medical aesthetic procedures on the market; graphic by VCBeat)

For instance, in April this year, data from Yimei Cha and the SoYoung Data Yanjiuyuan showed that two photoelectric treatments—skin tightening and lifting, and intense pulsed light (IPL) skin rejuvenation—ranked first and second, respectively, in terms of consumption scale, accounting for 11.33% and 5.38% of all medical aesthetic procedures that month.

(April Ranking of Consumer Spending on Medical Aesthetics Procedures. Image source: SoYoung Data Research Institute)

“From the operational perspective of our institution, skin tightening and anti-aging have become ‘essential demands’ for aesthetic seekers in recent years. Aesthetic seekers have demonstrated greater acceptance and openness to related treatments, particularly energy-based anti-aging procedures,” said Huang Feng, a senior practitioner in the medical aesthetics industry. He noted that skin-tightening and lifting treatments, including those using devices such as the Ultrasound Cannon (Chao Sheng Pao), have become important strategies for many medical aesthetics institutions to acquire and convert customers.

On one hand, photoelectric procedures offer product advantages such as high efficacy and low risk; on the other, there is a surge in demand from aesthetic seekers. This has naturally drawn capital’s favorable outlook toward photoelectric projects, leading to frequent investments and infusions of hundreds of millions of yuan in recent times.

“Against the backdrop of rising living standards and deepening population aging in China, consumers’ demand for anti-aging treatments has become increasingly strong.” In the view of Wang Xingchun, a senior investor in consumer healthcare, the rapid growth of the medical aesthetics market over the past decade, along with the emergence of numerous publicly listed companies with market capitalizations exceeding RMB 10 billion, amply demonstrates the broad prospects for the future of the energy-based device (EBD) segment in medical aesthetics.

Of course,In addition to the high growth potential of the sector, the robust gross profit margins of medical aesthetics companies specializing in optoelectronic technologies are also a significant factor attracting capital.An overview of the entire medical aesthetics industry chain reveals that the upstream sector, represented by pharmaceuticals and medical devices, boasts the highest gross profit margins. Specifically, companies in the medical device segment report gross profit margins ranging from 50% to 60%. For instance, Qizhi Laser and Furui Medical Technology, representative enterprises in the field of photoelectric medical aesthetics, have gross profit margins of 55.8% and 55.7%, respectively. In contrast, the downstream sector, dominated by service providers, typically sees gross profit margins between 30% and 50%. Representative companies such as Huahan Plastic Surgery and Langzi Shares report gross profit margins of 50.6% and 47.8%, respectively.

Additionally,We are currently in a window of opportunity for the domestic substitution of photoelectric medical aesthetic devices.It is worth noting that over 80% of optoelectronic devices in China are imported brands, primarily sourced from advanced manufacturing countries such as the United States, Israel, and Germany (iResearch data), indicating substantial potential for domestic substitution.

It is precisely on this basis that photoelectric medical aesthetics has risen strongly.

“In the field of photoelectric medical aesthetics, particularly in the segment of high-end devices, China still faces a shortage of relevant talent, and its core technologies remain in a catch-up phase,” said Wang Xingchun, a senior investor in consumer healthcare.The R&D of high-end optoelectronic medical aesthetic devices in China faces two major “mountains.”

· First, China remains relatively weak in basic theoretical research; for instance, further academic studies are needed to elucidate the specific mechanisms and effects of various energy-based technologies in cosmetic dermatology.

·Second, in terms of application development, the industry requires more interdisciplinary talent, as photoelectric medical aesthetics involves the intersection of multiple disciplines, including physics, engineering, and medicine. An excellent photoelectric device must not only address technical issues such as laser sources and wavelengths but also resolve challenges related to product design and clinical efficacy.

“This presents both challenges and opportunities,” Wang Xingchun added. In China, there is a large number of small-scale optoelectronic medical aesthetics companies. Their products suffer from serious homogenization and low technological value-added, resulting in low market concentration. Furthermore, these companies rank low in terms of safety and efficacy.

Amidst market consolidation and substitution opportunities, an increasing number of enterprises, capital investors, and R&D and management professionals are entering the field of photoelectric medical aesthetics, having already achieved certain breakthroughs.

From the perspective of industry path evolution, there are currently two main approaches to entering the photoelectric medical aesthetics sector: mergers and acquisitions, and independent research and development.

For instance, Huadong Medicine, Haohai Biological Technology, Fosun Pharma, and Sihuan Pharmaceutical have chosen to rapidly enter the market through mergers and acquisitions; whereas Fumeilei Medical, Lifotronic Technology, Yaguang Medical, Chirz Laser, Peninsula Medical, and Baifu Medical are pursuing a path of independent research and development.

Most of the companies implementing mergers and acquisitions strategies are leading enterprises in the pharmaceutical sector, which are entering the medical aesthetics market primarily to seek second and third growth curves for their businesses.Taking Huadong Medicine as an example, as a pharmaceutical R&D enterprise, it acquired a 26.6% equity stake in the U.S.-based company R2 in 2019, thereby securing exclusive Asia-Pacific distribution rights for the F1 (cryotherapy for spot removal) and F2 (full-body skin whitening) aesthetic light-based devices, and formally entering the field of photoelectric medical aesthetics.

In February 2021, Huadong Medicine acquired a 100% equity stake in High Tech, securing its cryolipolysis products (Cooltech, Cooltech Define, Crystile) and laser hair removal products (Elysion, Primelase). This February, Huadong Medicine announced that its wholly-owned subsidiary, Sinclair, would acquire a 100% equity stake in Viora, an Israeli energy-based medical aesthetics device company.

Turning to Fosun Pharma, it established its subsidiary Sisram Medical in Israel in 2013 and acquired a 95.2% stake in Alma Lasers, an Israeli aesthetic medical device company.

As a leading enterprise in the hyaluronic acid sector, Haohai Biological Technology has gradually shifted its resources toward the medical aesthetics and energy-based device sector. Last year, it formally acquired a 63.64% equity stake in Ouhua Meike, fully integrating Ouhua Meike’s radiofrequency and laser medical aesthetic devices into its medical aesthetics division. Furthermore, Haohai Biological Technology holds equity interests in EndyMed, an Israeli giant in medical aesthetics and energy-based devices, as well as exclusive distribution rights for its products in China.

Those opting for in-house R&D are primarily innovative enterprises with relatively short operating histories.Take Nanjing Baifu, which secured Series A financing in July this year, as an example. The company has independently developed a series of laser products, including ND:YAG Q-switched lasers, 1064 nm long-pulse lasers, 755 nm alexandrite long-pulse lasers, 2940 nm erbium lasers, and 1064/532 nm picosecond lasers.

Shenzhen Lifotronic Technology Co., Ltd., a company listed on the STAR Market, currently offers a main product portfolio that includes pulsed laser treatment systems, Q-switched Nd:YAG laser treatment devices, ultraviolet therapy systems, semiconductor laser treatment devices, intense pulsed light (IPL) therapy devices, phototherapy devices, and red-blue light therapy devices.

Fumeilei Medical, which secured tens of millions of yuan in angel financing this April, focuses on the independent research and development of high-end products such as picosecond laser therapeutic devices, photoacoustic imaging skin detectors, and photoacoustic-guided picosecond laser therapeutic devices.

In September, Yaguang Medical, having completed its Series B financing, launched the “Shuiyingji” (Water Baby Skin) product series. This device is a non-invasive, transdermal drug delivery medical device classified as a Class II medical device and holds an NMPA registration certificate as a non-invasive transdermal drug delivery system. Specifically, it applies medium-frequency pulses to the skin to induce temporary disruption of the stratum corneum structure, creating reversible “electropores” that facilitate drug penetration. The electric field applied to the cells increases cell membrane permeability, allowing nutritional components to penetrate into the dermis.

It is not difficult to observe that numerous innovative optoelectronic enterprises in China are progressively deepening their engagement, achieving certain progress in both research and development and commercialization.

“Domestic acoustic, optical, and electrical products are riding the wave of import substitution, presenting significant opportunities; however, ultimate success hinges on pricing and product quality.“Wang Xingchun, a senior investor in consumer healthcare, stated.

The robust demand on the consumer end and the buoyancy of the primary market indicate that the photoelectric medical aesthetics sector has entered a phase of accelerated growth.

In this opportunity, how to seize the window period and take off has also become a must-answer question for innovative enterprises. In response to this, Wang Xingchun, a senior investor in consumer healthcare, believes thatFirst, pursue a blockbuster product strategy; second, evolve toward a platform-based model.

"Blockbuster-product companies" refer to firms that own a single hit product, such as Thermage; "platform-based companies" refer to those with diversified product lines, encompassing several mainstream categories of optoelectronic devices and achieving product synergy.

“There is no absolute superiority or inferiority between the two; companies pursuing a blockbuster product strategy and those adopting a platform-based model require different capabilities—the former emphasizes product strength, while the latter focuses on channel marketing,” said Wang Xingchun, a senior investor in the consumer healthcare sector.Companies centered on blockbuster products will gradually evolve into platform-based enterprises, while platform-based companies may also increasingly focus on becoming blockbuster-product-centric firms due to the emergence of a specific blockbuster product.

Currently, a typical representative of single-product powerhouse companies is Solta Medical Corporation, which is gearing up for an IPO this year. Leveraging its strong product capabilities, its flagship device, Thermage, enjoys robust sales worldwide. To enhance profitability, Solta Medical Corporation has adopted the classic “razor and blades” business model.

How to Understand This Model? It locks in customers by leveraging a low-frequency product, thereby raising barriers to entry for new competitors, and generates profitability through associated derivative products or services, thus securing sustainable and stable revenue.

Specifically, Solta Medical Corporation’s “razor” is the Thermage device, and its “blade” is the Thermage tip. In other words, the Thermage device requires only a one-time purchase, whereas the Thermage tips necessitate ongoing paid replacements.

The rationale behind this design is that during Thermage treatment, the temperature of the heated tissue can reach 60–70°C, posing a risk of burns. To address this, Solta Medical Corporation employs a specialized Kapton-coated membrane to ensure uniform energy distribution. However, this specialized Kapton coating is highly prone to damage after repeated use. Consequently, the Thermage handpiece is designed as a single-use disposable, requiring a new handpiece for each patient undergoing the procedure.

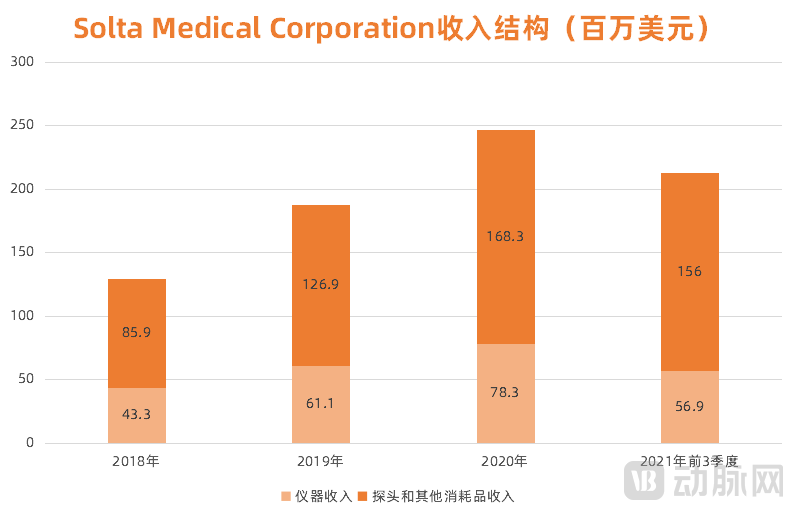

Benefiting from the “razor and blades” business model, Solta Medical Corporation has demonstrated strong profitability. According to its prospectus, Thermage tips and consumables accounted for over 70% of Solta Medical Corporation’s revenue in the first three quarters of 2021. The increased proportion of consumables revenue was the primary driver behind the company’s gross margin growth.

(Graphic by VCBeat; Data source: company prospectus)

(Graphic by VCBeat; Data source: company prospectus)

Representative platform-based enterprises include Candela, which was founded in 1970. Its product portfolio features PicoSure, E-light, CoolTouch CO2 fractional laser, Alexandrite laser hair removal, and PicoWay picosecond laser. This diverse range of products enables the company to provide comprehensive solutions for scenarios such as scar treatment, facial rejuvenation, wrinkle reduction, body contouring, tattoo removal, and hair removal.

“Platform-based enterprises have significant potential for leveraging synergies in branding, R&D, and distribution channels, which facilitates the sharing of successful product strategies and domestic and international channel resources, thereby accelerating product development and cross-selling across different product lines and markets,” said Wang Xingchun, a senior investor in the consumer healthcare sector.

However, it is important to note that regulatory authorities have intensified enforcement in response to the frequent irregularities plaguing the medical aesthetics industry in recent years. In March this year, the National Medical Products Administration (NMPA) issued an announcement adjusting the content of the “Medical Device Classification Catalog” concerning 27 categories of medical devices. Among these, radiofrequency treatment (non-ablative) devices, such as radiofrequency therapeutic instruments and radiofrequency skin treatment instruments, are now regulated as Class III medical devices. This signifies a further elevation of market entry thresholds.

Amid the overarching trends of technological iteration and increasingly stringent regulations, the photoelectric medical aesthetics industry is undergoing accelerated consolidation. Companies plagued by severe product homogenization and low technological value-added will be eliminated, while a cohort of enterprises daring to innovate and continuously break through will ultimately rise to the forefront of industry development.