China's Clinical Trial Digitization Unfolds: $10B Annual Market Growth and 50% Institutional Participation Signal New Era

As digitalization swept across the entire healthcare industry, the clinical trials sector stubbornly remained stuck at the informatization stage for a long time. In recent years, upgraded market demands have driven supply-side reforms, enabling digitalization to gradually permeate the field of clinical trials.

Since the release of the “Announcement on Launching Self-Inspection and Verification of Clinical Trial Data for Drugs” in 2015, the clinical trial sector has completed its informatization construction under the drive of regulatory compliance.

Subsequently, with the rapid development of innovative drugs in China, the number of clinical trial projects has surged, leading to a shortage of professionals; furthermore, the accuracy of traditional clinical trials, which heavily rely on manual processes, urgently needs improvement; additionally, increasingly stringent regulations are continuously raising clinical trial costs, making sponsors’ demand for cost reduction and efficiency enhancement more pressing. To address this series of demands from various stakeholders, digitalization offers viable solutions.

How is digitization being implemented across various stages of clinical trials? What is the current status of this digital transformation? What are the driving forces and barriers in this process? How will digital clinical trials evolve in the future? To address these questions, we conducted research involving two clinical trial centers, seven innovative enterprises, and three investment institutions, and interviewed 13 experts, company founders, and investors. This report aims to outline the current landscape of digital clinical trials and provide food for thought.

Core Views:

The market size increases by RMB 10 billion annually, with a positive growth trend.Based on the growth trend in the number of clinical trials in China in recent years and estimates of project pricing, the market size for clinical trials exceeded RMB 60 billion in 2022, expanding rapidly at an annual rate of RMB 10 billion. Driven by multiple factors including technology, market demand, policy, and capital, the digital penetration rate is expected to continue rising, potentially accounting for more than 50% of the total market share, with a favorable growth trajectory.

Clinical trial informatization has been completed, with high deployment rates of software such as EDC and intense market competition.Driven by compliance requirements, China’s clinical trials have completed the phase of informatization construction, with the deployment rate of representative software such as Electronic Data Capture (EDC) systems reaching 100%. However, due to market saturation and high product homogenization under regulatory guidance, competition within this service sector has become intensely fierce. To enhance their market competitiveness, enterprises are improving product and service performance vertically while expanding application scenarios horizontally.

Digitalization is in its early stages, with overall penetration higher in the post-launch phase than in the registration and clinical trial phase.In China, the overall level of digitalization in the pre-marketing clinical trial phase is only about 10–15%, while it is significantly higher in the post-marketing phase. The primary reasons for this disparity are the low degree of data interoperability between clinical trial institutions and sponsors, as well as the limited data-driven nature of these processes. The solution lies in supportive policies for standardized data use and the cultivation of interdisciplinary talent with expertise in both technology and medicine.

In the short term, policy drives the comprehensive digitalization of clinical trials; in the medium term, it relies on talent; and in the long term, on technology.To accelerate the digitalization of clinical trials, there is an urgent need for standardized policies governing compliant data usage to provide regulatory assurance for the digital upgrading of clinical trial centers. Furthermore, it is essential for enterprises and universities to collaborate actively in cultivating interdisciplinary talent who possess both technical expertise (such as AI, big data, and blockchain) and medical knowledge (including disease pathology, diagnostic and treatment logic, and expert guidelines). Finally, continuous technological advancements are expected to bring about disruptive innovation models to digital clinical trials, such as virtual clinical trials.

Clinical Trial Sector Completes Informatization, Entering Early Stage of Digital Transformation

Leveraging technology to reduce costs and enhance efficiency in clinical trials, achieving a win-win outcome for all stakeholders.Digitalization of Clinical Trials refers to the application of technologies such as big data, artificial intelligence (AI), and cloud computing to empower participants in clinical trials. By optimizing delivery methods or processes across all stages of clinical trials, it helps enhance the precision, safety, and efficiency of these trials. This approach reduces costs and improves efficiency throughout the entire clinical trial lifecycle—including bioequivalence (BE) studies and Phase I, II, III, and IV trials—ultimately achieving a win-win outcome for all stakeholders involved, including participants (subjects, physicians, and practitioners) and organizations (clinical trial centers, sponsor pharmaceutical companies, and contract research organizations [CROs]).

What standards must clinical trials meet during the digitalization process to be defined as digital clinical trials? Currently, there is no unified consensus within the industry. Through research and interviews, we have provided a definition of digital clinical trials from dimensions such as “optimization pathways” and “key optimization outcomes,” and have analyzed and summarized the developmental stages of clinical trials.

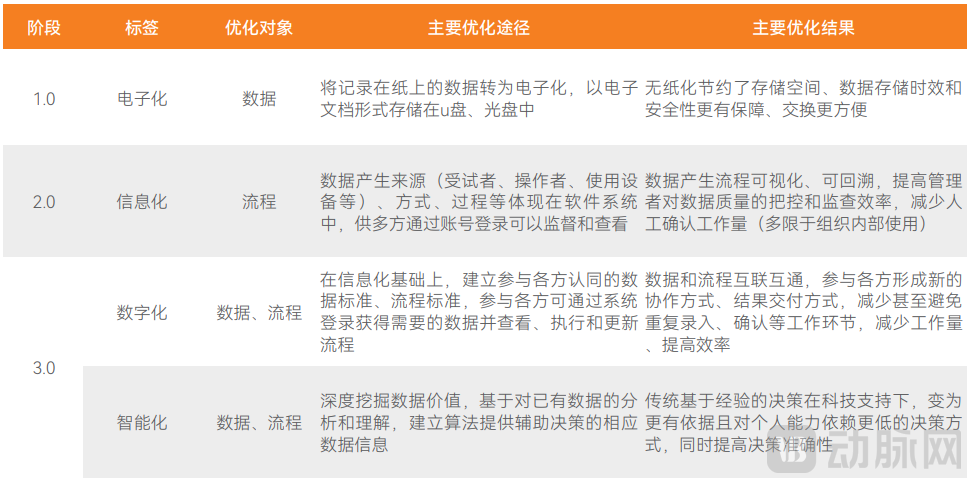

Definition and Development Stages of Digital Clinical Trials

The clinical trial industry has completed its digitalization and informatization initiatives.Around 2005, the industry began attempting to store traditional paper-based records in digital document formats, thereby completing the initial phase of digitization. While digitization enabled safer, long-term data preservation and facilitated data exchange, data authenticity and traceability remained poor, failing to meet the requirements for data accuracy verification and monitoring.

Consequently, since around 2010, informatization has taken center stage in industry upgrading. It has not only digitized experimental data but also ensured that multidimensional information surrounding the data—including instruments and consumables used, personnel involved in data collection, and collection procedures—is “traceable” within software systems, thereby providing a robust evidentiary basis for monitoring data authenticity.

On July 22, 2015, the Announcement on Launching Self-Inspection and Verification of Clinical Trial Data for Drugs, issued by the former China Food and Drug Administration (CFDA), sent shockwaves through the industry. The authenticity and traceability of data received unprecedented attention, which significantly accelerated the process of informatization within the industry.

The formation of new, more efficient collaboration models among stakeholders is a key hallmark of digitalization.There is currently no unified industry standard for the definition of digital clinical trials, but a clear consensus exists that they “establish new, more efficient modes of collaboration among all stakeholders.”

The informatization phase has brought data "online." The next step is to leverage this data effectively, enabling participants in clinical trials (subjects, physicians, and practitioners) and participating organizations (clinical trial sites, sponsor pharmaceutical companies, or CROs) to establish more effective connections. This will foster a more efficient and convenient collaboration model, yielding mutual benefits and better outcomes and returns. Based on this definition, the digital transformation of the industry is still in its early stages.

Intelligence Empowers Decision-Making in Digital Clinical Trials.In the course of informatization and digitalization, the industry has established extensive databases. By leveraging technologies such as artificial intelligence to achieve in-depth data understanding and develop algorithms, clinical trial decision-making can rely less on empirical experience and become more “intelligent” through data-driven support.

Overall, informatization serves as the foundation for digitalization, while digitalization represents an upgrade of informatization. Currently, the clinical trial sector, having established its informatization infrastructure, is undergoing a digital transformation aimed at fostering more efficient connectivity among all stakeholders. Furthermore, intelligence enhances the “smart” capabilities of decision-making within digital clinical trials. Characterized by data-driven approaches, it replaces empirical experience with algorithmic outputs to provide auxiliary decision support across multiple stages of digital clinical trials.

The Clinical Trial Market Exceeds RMB 60 Billion, with the Digital Segment Accounting for 15–50%

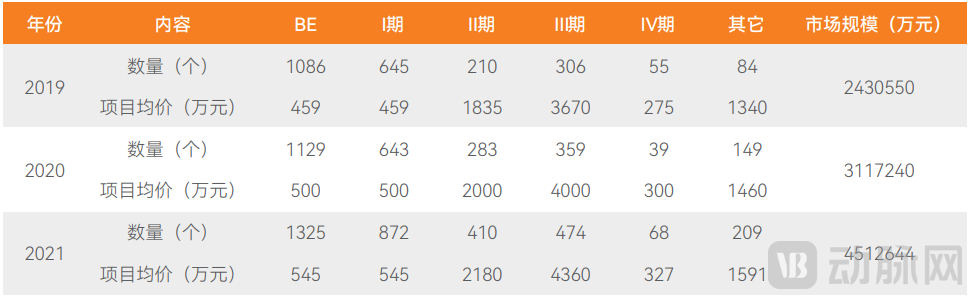

The clinical trial market is growing by tens of billions annually.Due to significant variations in the number of trials and pricing across Bioequivalence (BE) studies and Phase I, II, III, and IV clinical trials, we calculated the market size for each category separately and then summed them to estimate the total market size. Trials that could not be clearly classified into a specific category were grouped under “Other,” with the average price per trial for this group determined by taking the mean of the average prices across all other categories. The estimated overall market size for clinical trials is as follows.

Market Size Estimation for Clinical Trials, 2019–2021

Data Sources: Center for Drug Evaluation, National Medical Products Administration; Sinovation Ventures; VCBeat.

From 2019 to 2021, the clinical trial market size grew by approximately RMB 10 billion annually, increasing from RMB 24.3 billion in 2019 to RMB 45.1 billion in 2021, with an average annual growth rate of up to 36.51%.

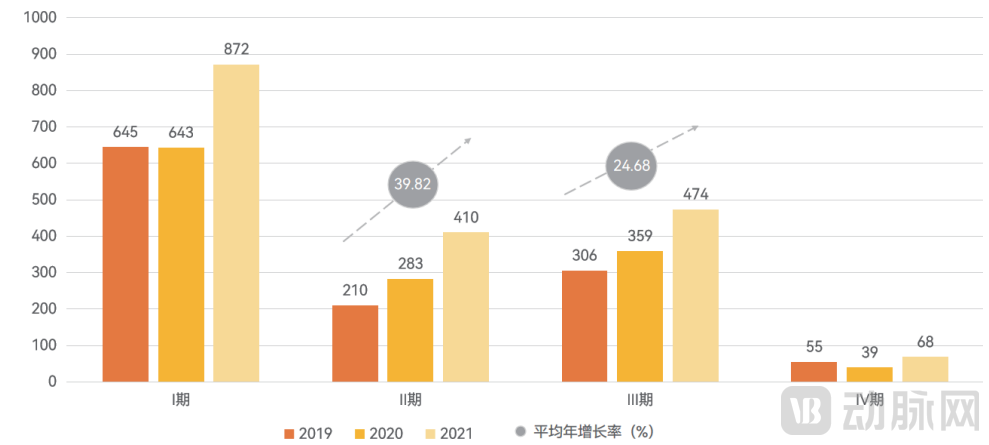

II. The increase in the total number of Phase II and III clinical trials has further expanded the market size.In clinical trials, Phase III projects incur the highest costs, followed by Phase II. According to statistics from VCBeat, the average costs for Phase II and Phase III clinical trial projects reach as high as RMB 20 million and RMB 40 million, respectively—5 to over 10 times those of bioequivalence (BE), Phase I, and Phase IV projects—and are growing at an annual rate of 9%.

From 2019 to 2021, the average annual growth rates for the total number of “high-value” Phase II and Phase III clinical trials reached 39.82% and 24.68%, respectively, significantly higher than those of other phases. Based on this trend, the overall market size of clinical trials in 2022 is expected to exceed RMB 60 billion.

Changes in the Total Number of Clinical Trials by Phase for New Drugs, 2019–2021

Data Source: Center for Drug Evaluation, National Medical Products Administration; Sinovation Ventures; Produced by VCBeat

Digital clinical trials are poised to capture half of the market by offering more comprehensive services.Interview-based research indicates that the costs incurred to “digitize” a project vary from approximately 15% to 50% of the total project budget, depending on the extent and format of digitalization. This implies that the market size for companies providing digital clinical trial services in China was poised to exceed RMB 30 billion in 2022.

Policy Guidance Steers the Direction of Digitalization, While Capital Investment Accelerates the Digital Transformation Process

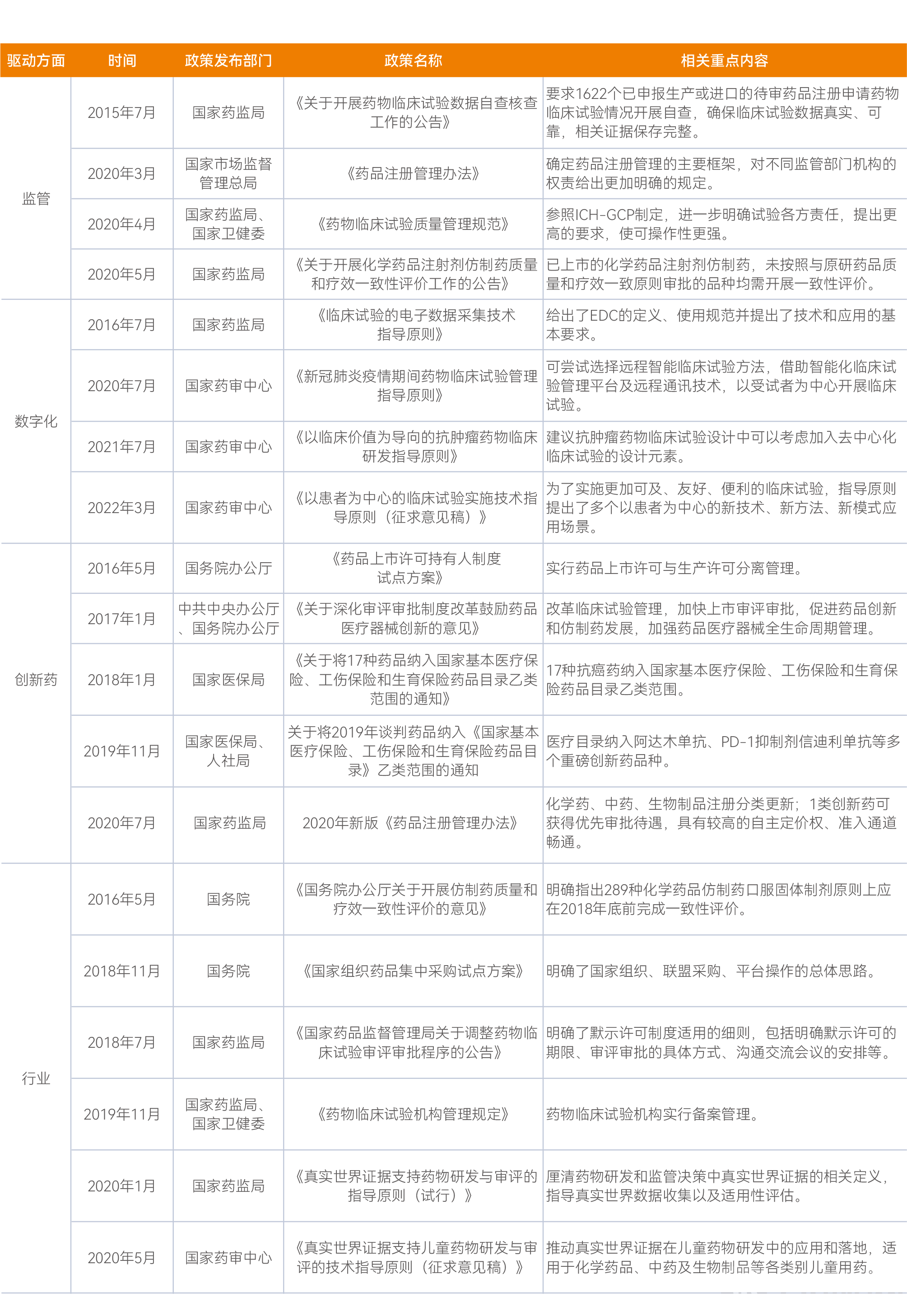

# Tightening Regulatory Policies: Detailed Guidelines Steer the Direction of Digitalization. Clinical trials are a highly regulated field. In recent years, regulatory oversight of clinical trials, particularly concerning the authenticity and reliability of data, has become increasingly stringent, with continuously emerging higher and more rigorous requirements.

However, on the flip side, the more explicit and detailed requirements set forth by relevant policies have also led to a more unified and clear market demand for digitalization in certain segments of clinical trials, thereby providing product developers with clearer guidelines and making it easier to meet market needs.

A Review of Policies Driving the Development of the Digital Clinical Trials Sector

Source: Arterial Orange Database, prepared by VCBeat.

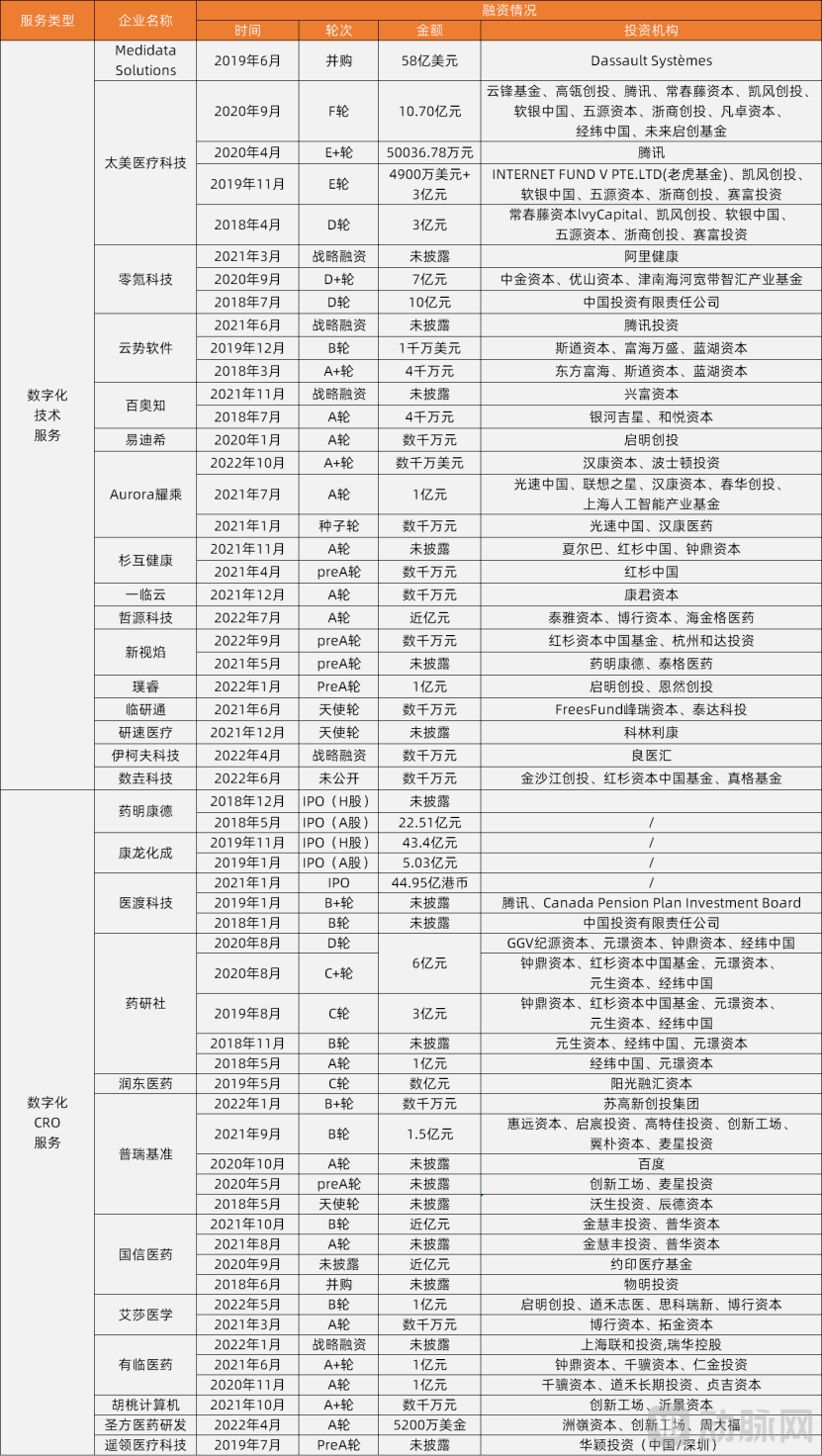

Capital Fuels the Rapid Development of Digital Clinical Trials.In recent years, amidst the wave of digitalization, leading traditional CROs such as WuXi AppTec and Pharmaron have actively deployed digital pipelines covering drug discovery, clinical trials, and manufacturing. Meanwhile, a number of digital CROs focused specifically on digitalizing clinical trial processes have emerged in China, including Yidu Cloud (a subsidiary of Yidu Tech), Aishai Medical, DrugDev Club (parent company: Miaoyi Biotech), Yaoling Medical Technology, and Youlin Pharma.

An analysis of financing events in this field over the past five years reveals that CRO companies providing digital clinical trial solutions have performed well in the capital market during the last two years. In addition to digital CROs, technology service providers such as BioKnow, Taimei Medical Technology, Linyantong, and Yansu Medical play a crucial role in the digital transformation of clinical trials, which has sustained strong investor enthusiasm for this sector.

Financing Status of Companies Providing Digital Clinical Trial Technologies and Services Since 2018

Source: Artery Orange Database, prepared by VCBeat.

Capital’s strong interest in and investment in CRO companies with digital capabilities, digital CROs specializing in clinical trials, and providers of digital technical services for various stages of clinical trials have been a major driving force behind industry development in the early stages of digitalization.

Analysis of the Current Development Status of the Three Main Business Models for Technical Service Enterprises

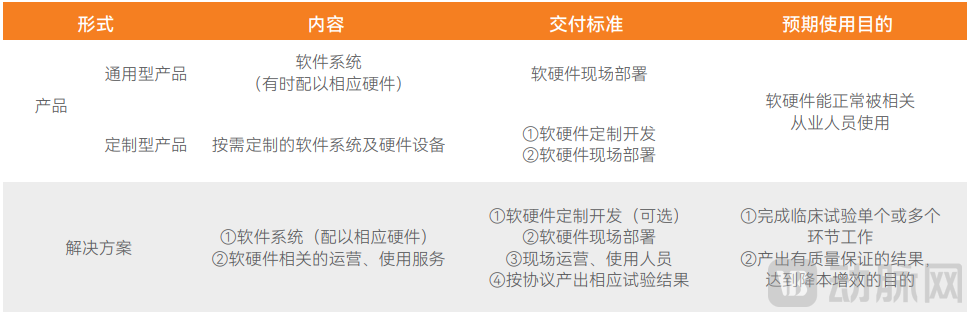

The development of technology service enterprises is the most mature, with products and solutions coexisting.Driven by capital and market demand, upstream technical service providers in the industry chain have achieved the most mature development, serving as a key driver for the growth of the digital clinical trial sector. These enterprises not only undertake the development of digital technology infrastructure but also play the role of market educators.

Technical service providers offer a high degree of product flexibility to the market, delivering modular combinations of software, hardware, and services with varying levels of customization tailored to the specific phase, scale, and requirements of clinical trials.

Currently, product types can be broadly categorized into two groups. The first group consists of products that offer only hardware and software, which are further divided into general-purpose and customized solutions. The primary distinction between them lies in the ownership of the data storage servers: customized products utilize private servers owned by the client, whereas general-purpose products typically rely on the vendor’s servers. The second group comprises comprehensive solutions that include hardware, software, and related operational services. These two categories differ in terms of content, delivery standards, and intended use cases.

Comparison of the Two Main Product Categories Offered by Technical Service Enterprises

Different Forms Give Rise to Three Major Business Models.Differences in product types also give rise to distinct business models. According to research, the aforementioned product forms can be broadly mapped to the current mainstream business models: SaaS, private customization, and solutions-based models.

Comparison of the Three Major Business Models

SaaS offers promotional advantages, but the overall market size is relatively small.SaaS is a business model widely adopted by most technology service providers, typically featuring usage-based pricing and low unit prices. Currently, apart from a few industry giants, clinical CRO companies are mostly small in scale and highly fragmented.

Therefore, the low cost barrier of the SaaS model offers certain advantages for market expansion during the early stages of product launch. However, this low entry cost also limits the overall market size of SaaS services. According to research, software and hardware products account for only about 15% of the total costs in clinical trials.

Solutions expand market size, but entail greater accountability for outcomes.To capture larger markets, the “product + service” solution-based business model has gradually emerged. In addition to providing software and hardware products within the SaaS model, companies also deploy specialized operational and user personnel, enabling clients to bypass the learning curve associated with using tools to generate results on their own, and instead directly delivering outcomes at lower costs or higher quality.

As a result, the addressable market for technology service providers is set to expand from 15% of the overall clinical trial market to nearly 50%. However, alongside this broader market opportunity, companies bear greater responsibility for trial outcomes, with projects typically structured around milestone-based deliverables and payments. Currently, many enterprises offer both SaaS and solution-based models, with the latter generally accounting for a larger share of their business.

Private customization ensures that "data remains within the institution," but it presents a higher barrier to entry for customers.Furthermore, a private customization business model has emerged in the industry. In terms of market size, this model continues to target the software and hardware segments of the clinical trial market, with a fee structure similar to that of Hospital Information Systems (HIS).

This model more directly addresses clients’ need to keep data within their own institutions. Therefore, it is a favorable option for pharmaceutical companies and CROs seeking solely to purchase hardware and software technologies. However, due to the private configuration of servers and customization of hardware and software, the initial cost threshold is relatively high; the starting fee for customized solutions is often 20 times that of the SaaS model or even higher. This implies that, from a cost perspective alone, the SaaS model is more suitable for enterprises with fewer than 20 projects per year on average.

Three Major Models Await Market Validation.Given the distinct characteristics of each business model, the key challenges to be addressed vary accordingly. For the SaaS model, increasing the average revenue per user (ARPU) or innovating pricing structures may be effective strategies for expanding the overall market size. For companies offering private customization services, lowering barriers to entry to attract a broader customer base is a critical consideration. In the solution-based business model, although integrated solutions are more favored by the market than standalone hardware or software products, it is essential to effectively manage the accompanying profitability challenges. This requires reasonable control over trial costs—particularly labor costs and additional expenses arising from project delays—while ensuring high-quality compliance with delivery standards.

Currently, industry perspectives on the development of the three business models vary, and the future trajectory of each model remains to be validated by the market over a longer period.

Analysis of the Development Status of CRO Companies Providing Digital Clinical Trial Services

To clarify the current development status of clinical trial CRO enterprises, we broadly categorize companies capable of providing digital clinical trial CRO services into three types.

Classification of Companies Providing Clinical Trial CRO Services

Traditional CRO companies require a lengthy transition period for digital transformation.For traditional CRO companies, digital transformation requires in-depth communication and integration between business departments and the digital transformation team, which is not an easy process.

On the one hand, the digitalization team needs to learn business processes to design corresponding digital solutions; on the other hand, the business team’s work habits will change as a result of digital upgrades. Both the learning and adaptation processes require a considerable transition period.

Furthermore, traditional CRO giants often operate across numerous stages spanning both preclinical and post-clinical phases. In contrast to these other stages, clinical trials exhibit weaker standardization, greater reliance on human resources, and higher demands for personnel competency, thereby making expansion in this segment more challenging. Consequently, it is difficult for clinical trials to serve as the core focus of digital transformation for major CRO enterprises, which in turn limits the strategic priority assigned to their digital upgrading.

Innovative Digital CRO Companies Demonstrate Strong Fundraising Performance.Companies providing clinical trial CRO services with a focus on “digitalization” can be divided into two categories: technology-driven service providers, whose offerings may range from standalone technical solutions to comprehensive CRO services; and companies dedicated exclusively to providing CRO services.

Both are favored by investors. When assembling their founding teams, such digital enterprises typically prioritize “possession of digital expertise” and “a track record of successful digital projects” as key criteria. This grants them an “inherent advantage” in digital technology and mindset. Coupled with their focused engagement in clinical trial processes, they exhibit heightened sensitivity to digitalization needs and respond more rapidly.

Compliance and cost-efficiency demands drive higher product penetration, with EDC reaching 100%

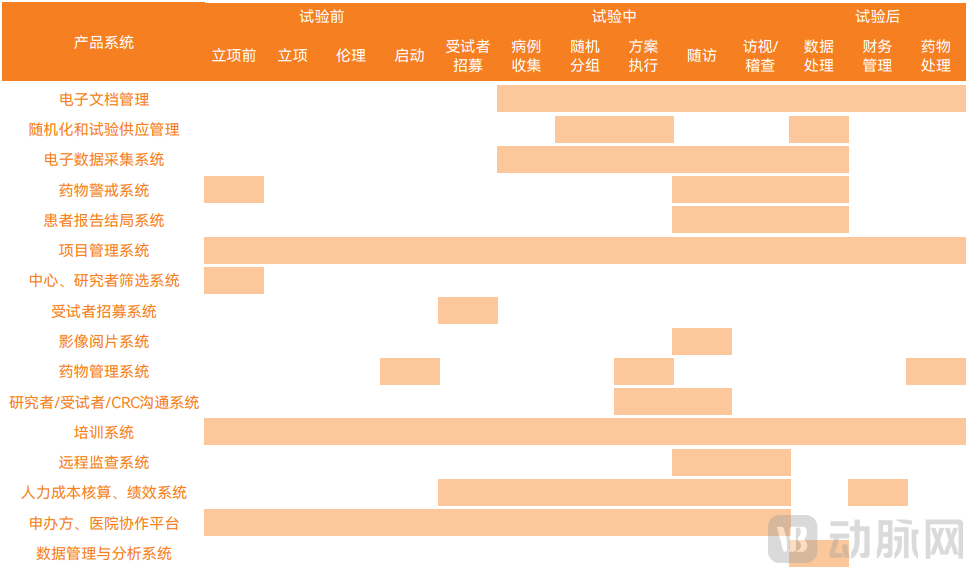

The digital product pipeline continues to expand, with progressive coverage of all stages of clinical trials.We have reviewed the current major digital products for clinical trials and their primary application stages. Notably, as various products continue to upgrade and iterate, there is a growing trend toward integration (mutual inclusion) among them. Consequently, similar products from different companies are gradually becoming more differentiated.

An Inventory of Application Stages for Software Systems in Digital Clinical Trials

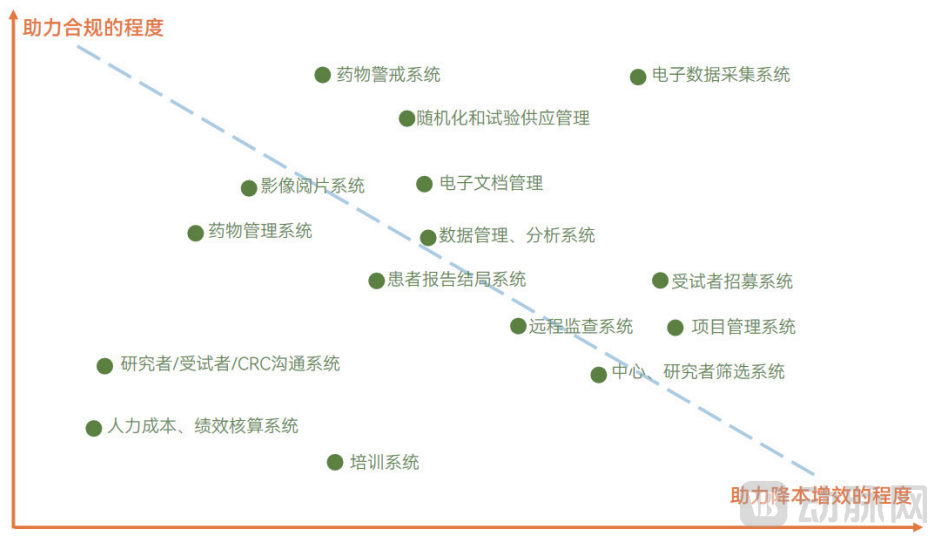

Compliance and cost reduction with efficiency enhancement are key drivers of product market penetration.Compliance is the foundation of clinical trials and holds “veto power” over their conduct and outcomes. Therefore, as regulatory requirements become increasingly stringent, products that facilitate greater compliance in clinical trials have achieved the highest market penetration rates. Examples include Electronic Data Capture (EDC) systems, Randomization and Trial Supply Management (RTSM), and Pharmacovigilance (PV). According to surveys, the adoption rate of such products at trial sites reaches 90–100%, essentially achieving full market coverage.

Furthermore, cost reduction and efficiency enhancement constitute the second core driver. The major cost drivers in clinical trials include data capture and recording, project collaboration management, and data monitoring. Therefore, from the perspective of cost reduction and efficiency enhancement, Electronic Data Capture (EDC) systems remain the primary driver for increased penetration rates. Meanwhile, related products such as Clinical Trial Management Systems (CTMS), Electronic Trial Master File (eTMF) solutions, and remote monitoring tools also demonstrate favorable market penetration, reaching approximately 50%.

The Extent to Which Various Products Support Compliance, Cost Reduction, and Efficiency Enhancement

Focusing on the two dimensions of “compliance” and “cost reduction and efficiency enhancement,” we have evaluated the extent to which each product contributes in these areas, as illustrated in the chart. It is evident that products positioned above the blue dashed line generally exhibit higher market penetration rates.

As the penetration rate of EDC systems rises, the market is becoming saturated with players. Under the guidance and requirements of detailed regulatory frameworks, product homogenization has become severe, making it crucial for enterprises to identify and cultivate their differentiated competitive advantages in this landscape.

In contrast, CTMS software, which is designed to enhance operational efficiency, has not yet received explicit policy support. Furthermore, due to variations in workflows across different projects and enterprises, its level of standardization is lower than that of EDC systems. Therefore, to further increase the market penetration of such products, it is necessary to strengthen market education on one hand, while enterprises must continuously hone their ability to rapidly respond to non-standard market demands on the other.

Next, from a product perspective, this report will summarize the research findings on the development of various products (and companies), driven by two key factors: “compliance” and “cost reduction and efficiency improvement.”

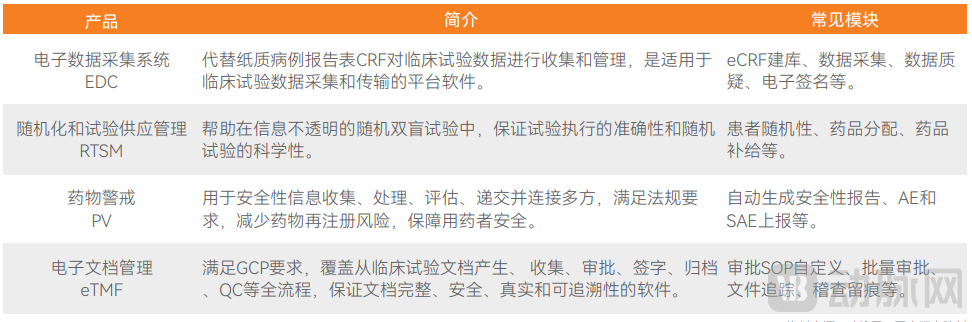

Stringent Regulatory Requirements Drive the Development of Healthcare IT Software, Achieving 100% Coverage

Software such as EDC, RTSM, and PV has become an essential requirement.Drug clinical trials are a heavily regulated industry, particularly for bioequivalence (BE) studies and Phase I–III registration trials. Driven by years of compliance requirements, software systems involved in informatization, such as Electronic Data Capture (EDC) and Randomization and Trial Supply Management (RTSM), have become essential for conducting clinical trials and are now nearly universally adopted by sponsors (pharmaceutical companies or CROs) and clinical trial sites.

Software and Main Functions Involved in Information Technology Construction

“Essential” Software Suffers from Severe Homogenization: Three Pathways Offer a Way Out of the Rat Race

Software Performance Convergence: Companies Embark on a Path to Break Free from Hyper-Competition.Policy-driven rapid industry growth is a double-edged sword: while it boosts demand-side acceptance, it also leads to an increase in the number of supply-side enterprises. Furthermore, as regulatory details become increasingly clear, software performance is gradually converging.

For technology service providers offering software related to EDC-based informatization, the market is becoming increasingly saturated and homogeneous. To avoid being trapped in a race to the bottom through price wars, these companies are actively exploring their own paths to break free from this intense competition.

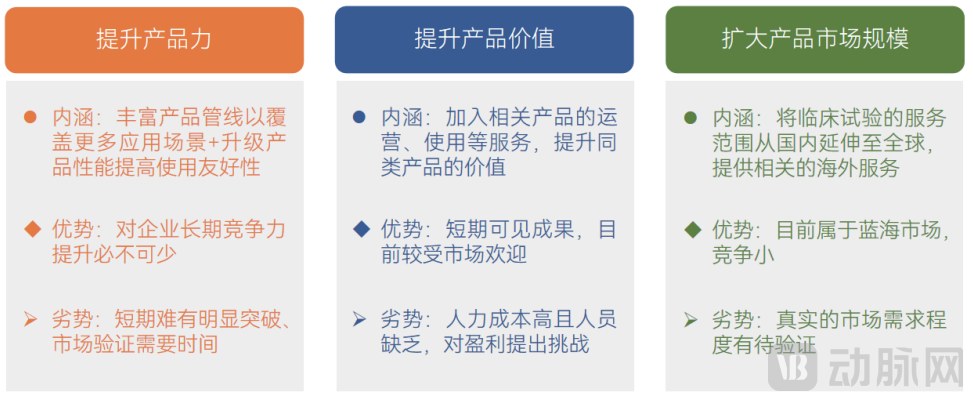

Three Major Pathways for Enterprises to Enhance Market Competitiveness

Expanding the Pipeline and Upgrading Performance in Tandem to Enhance Product Competitiveness.In the pursuit of enhancing product competitiveness, companies often simultaneously pursue horizontal expansion of their product pipelines to accommodate a broader range of application scenarios in clinical trials, and vertical upgrades to the performance of existing products to deliver a more user-friendly experience. Determining the optimal balance between these two strategic avenues poses a significant challenge to corporate leaders’ market judgment and strategic planning capabilities.

Furthermore, in the digital clinical trial arena, where stagnation equates to regression, enhancing product competitiveness is not merely a strategy for breaking through intense market competition, but an indispensable “foundation for survival” for enterprises.

Service Enhancement and Global Service Expansion Offer New Strategies to Break Through Market Saturation.According to research, incorporating services to enhance product value—specifically by providing services for single or multiple stages of clinical trials—has garnered favorable market feedback. However, the associated rise in labor costs poses new challenges to corporate profitability. Furthermore, amid the growing trend of innovative pharmaceutical companies expanding globally, tapping into overseas service markets has emerged as a strategic move to break free from intense domestic competition.

Dual Drivers of Compliance and Cost Efficiency: Data Acquisition Achieves New Breakthroughs

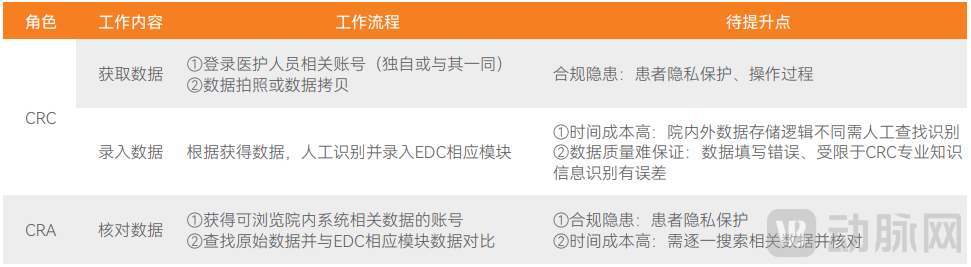

Data Collection: The Key to Digitalization Lies in Replacing Manual Labor.During the phase of information technology infrastructure development, the most critical software is undoubtedly the Electronic Data Capture (EDC) system. In addition to meeting regulatory compliance requirements for electronic data storage and audit trails, EDC represents one of the major costs in clinical trials. This is because the process of “transferring” data into the EDC system still relies heavily on manual operations, which not only poses risks of data entry errors but also incurs substantial labor costs, including those for Clinical Research Coordinators (CRCs) during data entry and Clinical Research Associates (CRAs) during monitoring. According to surveys, the costs associated with data entry and monitoring account for approximately 25% and 10% of the total project budget, respectively.

CRC and CRA Responsibilities in the Data Collection Process and Areas for Improvement

It is evident that the key to addressing compliance risks in data collection and reducing the significant cost burden lies in replacing manual labor with technology. For Clinical Research Coordinators (CRCs), technology can facilitate direct integration between hospital systems and Electronic Data Capture (EDC) systems, enabling automatic population of required data fields. Consequently, CRCs are only required to review and sign off on the data.

Implementing this step is expected to improve data collection efficiency by approximately 90%, thereby yielding corresponding savings in labor costs. However, the digital clinical trials sector has yet to fully overcome this pain point—is this due to regulatory constraints or technological limitations?

Technological Breakthroughs Make Data-Secure Discharges Possible.Out of concern for patient privacy and responsibility for data security, clinical trial centers have always adhered to the principle of “data staying within the hospital,” which is undoubtedly a major obstacle to data interoperability. However, at its core, what these centers seek to control during the clinical trial process is:

What data are included at discharge? ---- Must not contain patient privacy information or data unrelated to the clinical trial.

Are there any risks in the data discharge pathway? ---- It must not impact existing systems.

Final Data Ownership? ---- Data copied from discharge records should be appropriately destroyed after use in clinical trials.

These concerns have been addressed with corresponding solutions driven by technological breakthroughs, such as patient data de-identification, secure data interfaces, firewall configurations, and audit trails for data extraction processes. Currently, companies including BioKnow, DrugDev Club, Yaoling Medical Technology, LinYanTong, and Yansu Medical all offer relevant solutions, which can be delivered in various forms such as SaaS, private customization, and comprehensive solution packages.

Precise application of data requires deep integration of technology and medicine.Obtaining data interfaces is merely the first step; the subsequent phases of identification and application require not only technical expertise but also deep integration with medical knowledge and clinical diagnostic and treatment logic.

To replace manual labor with automated systems by populating the corresponding fields in the Electronic Data Capture (EDC) system with hospital data via interfaces, three stages are required: data extraction, data processing (including de-identification, archiving, and format conversion), and data application (matching and entry). The efficiency and accuracy of each step are closely tied to the degree of integration between technology, medical knowledge, and clinical logic.

Degree of Demand for Technical and Medical Expertise Across Data Collection Stages

In the data scraping phase, a thorough understanding of the storage and management logic of hospital information systems enables rapid identification of the information required for clinical trial Case Report Form (CRF) tables, thereby facilitating efficient data extraction and reducing the need for post-keyword-search filtering.

After processing, the information proceeds to the data application phase. The matching process relies heavily on an understanding of clinical diagnosis and treatment logic, establishing corresponding data mappings, and achieving accurate matching and entry through continuous optimization of AI algorithms. As a result, Clinical Research Coordinators (CRCs) only need to verify and sign off on the final results.

Finally, by leveraging blockchain technology, the entire data flow from within to outside the hospital—including operational personnel and timestamps—is fully traceable. This helps Clinical Research Associates (CRAs) improve monitoring efficiency by eliminating the need for manual searches for source data, making the data’s provenance clear at a glance and laying a critical foundation for remote monitoring.

Driven by Cost Reduction and Efficiency Enhancement, New Business Models Are Urgently Needed

Digitalization drives cost reduction through more efficient collaboration models.Digitalization in the clinical trial sector is still in its early stages, with the primary objectives being cost reduction and efficiency improvement. The focus of upgrades is shifting from “compliance”-related processes to those characterized by high costs and low efficiency in traditional models, such as:

Insufficient overall project management led to project delays.

Difficulties in patient recruitment lead to project delays or closures.

The selection of investigators and sites is time-consuming and labor-intensive.

High Labor Costs for CRA Monitoring.

The market penetration rate of related software systems has also increased.

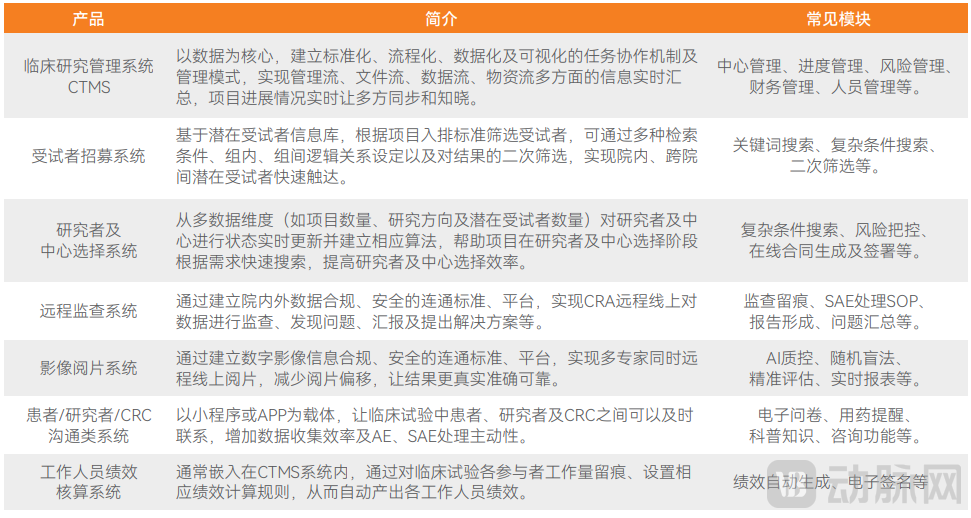

Software Involved in Digitalization Initiatives and Key Functionalities

Digitalization must build upon informatization by leveraging data mining and application to establish standards and rules, thereby enabling all stakeholders in clinical trials to form new, more efficient collaboration models driven by data, ultimately resulting in significant improvements in efficiency and reductions in cost.

How Have the High-Cost, Low-Efficiency Stages of Clinical Trials Changed with the Aid of Various Software, Supporting Services, and Solutions? We Will Now Analyze the Findings from Our Survey One by One.

Project management penetration rate is approximately 50%, with local tertiary A hospitals developing at a faster pace

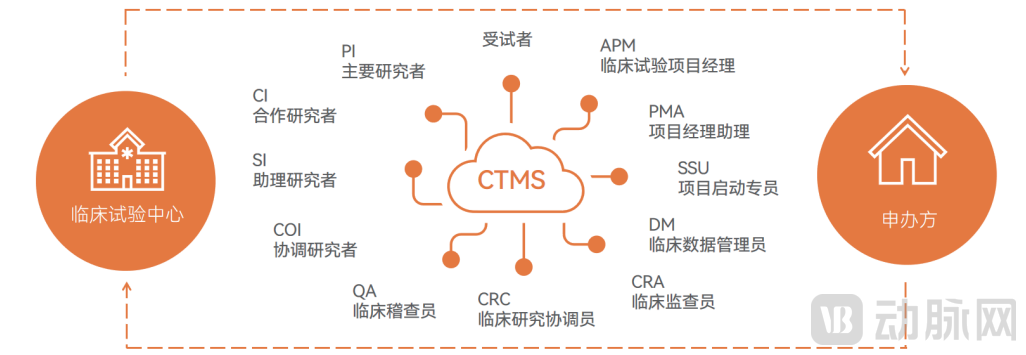

The foundation of project management requires data interoperability.Clinical trials involve numerous participants from both clinical trial centers and sponsors, categorized into three groups: subjects, investigators, and staff.

CTMS Connectivity Involves Institutions and Participants in Clinical Trials

Approximately 50% of clinical trial centers have joined the digital initiative for “interconnectivity.”Depending on the deploying institution, a Clinical Trial Management System (CTMS) can be categorized into the clinical trial site side and the sponsor side. Digitalization efforts focus on achieving interconnectivity between these two ends, thereby reshaping the traditional mode of collaboration between them.

Taking the PI signature phase in clinical trials as an example, traditional clinical trial CRCs typically accumulate a certain number of documents and have them signed in batches when the PI is available. This process has strong uncertainty in its time cycle; if there are two PIs involved in the trial, the uncertainty further increases, consuming CRC time and making progress difficult to control. Additionally, if there are errors or non-compliance in the signed documents, extra time is required for re-signing.

In digital clinical trials, Principal Investigators (PIs) and Clinical Research Coordinators (CRCs) at both the investigative sites and the sponsor end can leverage a Clinical Trial Management System (CTMS) to streamline this frequent and time-consuming process. First, since all data and workflows are “online,” most documents requiring signatures can be automatically generated and categorized. CRCs only need to review the relevant information and confirm submission, while PIs can log into their accounts to view pending documents and complete signatures during fragmented downtime. Additionally, the system can prioritize documents based on their validity deadlines and provide timely reminders to prevent delays in document signing from impacting overall project progress.

As a result, document error rates and preparation time are significantly reduced, while CRCs and PIs can also complete the signing process flexibly and efficiently.

Although end-to-end management of interoperability projects between in-hospital and out-of-hospital settings is a key link in cost reduction and efficiency improvement, as mentioned in the previous chapter, due to security concerns regarding “data not leaving the hospital,” although many enterprises have solutions for connectivity based on CTMS software both inside and outside hospitals, only about 400-500 clinical trial centers, accounting for approximately 50%, have actually attempted to achieve “connectivity.”

Local Grade 3A hospitals have a stronger willingness to develop in “connectivity” than national large-scale Grade 3A hospitals.According to research, the initial pioneers in adopting digital upgrades for interoperability were not national top-tier tertiary hospitals with a high concentration of clinical trials, such as Huashan Hospital and Tiantan Hospital, but rather local tertiary hospitals, such as Guizhou Cancer Hospital.

For clinical trial institutions, national top-tier (Grade 3A) hospitals lack the motivation for digital transformation due to an abundance of clinical trials. In contrast, while local Grade 3A hospitals possess strong capacity to undertake clinical trials, their annual number of accepted clinical trial projects is not saturated, whether in terms of available investigator resources, patient population base, or clinical trial conduct capabilities.

Digital transformation not only enhances the competitiveness of healthcare institutions but also, through digital interconnectivity, increases their visibility to sponsors, thereby enabling them to secure more clinical trial projects. Wendy, an investment manager at Sinovation Ventures, stated that it is estimated that around 2020, nationwide top-tier tertiary hospitals (Grade A Class III), such as Ruijin Hospital, had cash flows exceeding RMB 1 billion, while local tertiary hospitals had less than half of that amount.

Annual revenue from clinical trials for the former ranges from tens of millions to hundreds of millions of yuan. This scale does not significantly impact its operations, and it has never been “absent” from this sector. However, if clinical trial revenue of a similar magnitude were generated by a local Grade A tertiary hospital, it would constitute a “pivotal” source of income. Of course, for local Grade A tertiary hospitals, beyond this most direct incentive, other important drivers include the hospital’s academic standing and researchers’ scientific needs.

Reshaping the “Outreach” Phase of Subject Recruitment Based on In-Hospital and Out-of-Hospital Health Big Data

Digitally transform the outreach process to improve efficiency in reaching potential participants.Subject recruitment has consistently ranked high on the “pain point list” for clinical trials, with one of the key challenges being the difficulty in efficiently reaching precisely targeted participants. Traditional recruitment processes primarily rely on purely manual methods—such as leveraging patient populations from collaborating investigators, referrals among researchers, and CRCs conducting case-by-case “manual searches” in hospital wards—all of which suffer from low efficiency and precision.

During the process of digital transformation, the outreach phase of subject recruitment has ushered in new models and methodologies, underpinned by ample data and algorithms aligned with medical logic. Sponsors need only input the inclusion and exclusion criteria into the corresponding software system, which can then precisely search the database for suitable subjects.

Comparison of Patient Reach in Subject Recruitment Before and After Digitalization

For subject recruitment software, the scale and data integrity of the system’s information repository are crucial. In specific disease areas, a larger pool of potential subjects and more comprehensive multi-dimensional health data collection provide a solid foundation for algorithms; the former ensures the quantity of screening candidates, while the latter enhances the quality of screening.

The database for digital subject recruitment draws information from two primary sources: electronic medical records of in-hospital patients and partnerships with platforms that possess substantial internet traffic resources. Currently, oncology drugs account for more than 50% of approved innovative drug clinical trials in China, making oncology the most favored niche sector for digital subject recruitment.

Digitalization Empowers the Educational Component of the Subject Conversion Process.In the patient conversion phase, it is not yet possible to reshape collaboration models within the outreach phase to significantly enhance efficiency. However, the digital upgrade of the outreach phase enables more precise screening of subjects, which can directly improve the conversion rate in the conversion phase. Additionally, a large number of easy-to-understand scientific popularization products, presented in various formats such as text and video, have emerged. These resources assist Clinical Research Coordinators (CRCs) and other professionals in conducting subject education more efficiently, thereby increasing conversion rates.

Phase IV Clinical Trial Digitalization Remains a Blue Ocean, with Urgent Demand for Cost Reduction and Efficiency Improvement

From the perspective of definitional scope, Phase IV clinical trials are a form of post-marketing clinical validation; post-marketing clinical validation, in turn, is a type of Real World Study (RWS). Although these three categories differ in deliverables and study objectives, their trial design methodologies and execution processes are similar. Therefore, when surveying the digitalization needs and current status of Phase IV clinical trials, we also included companies providing digital solutions for post-marketing clinical validation and RWS. The following analysis of the survey results is presented with RWS as the primary focus.

Real-world studies have a more urgent need for cost reduction and efficiency improvement.Real-World Studies (RWS) differ significantly from registration clinical trials in terms of regulatory requirements, study design, sample size requirements, and data collection dimensions; therefore, the digitalization process and needs for RWS also differ from those for registration clinical trials.

Some Differences Between Registered Clinical Trials and Real-World Studies

The primary objectives of Real-World Studies (RWS) for pharmaceuticals include identifying rare adverse effects, discovering new indications, and facilitating reimbursement listing. Achieving these objectives relies on large sample sizes, which are typically tenfold or greater than those in registration clinical trials. Larger sample sizes entail higher labor costs for data collection, a major cost component.

Furthermore, from a statistical perspective, the increased sample size reduces the impact of individual data errors on overall results. Coupled with the less stringent regulatory requirements for Real-World Studies (RWS) compared to those for registration clinical trials, the pursuit of cost reduction and efficiency improvement in RWS is more direct and urgent.

Digital data collection is the foundation for conducting large-sample real-world studies (RWS).The labor cost of data collection increases linearly with the sample size, i.e., total data collection cost = sample size × (time per data point collected × labor cost per unit time). Therefore, as labor costs continue to rise, shortening the time required to collect each data point has become a critical bottleneck to address if we are to expand the sample size and obtain higher-quality real-world study (RWS) results while controlling or even reducing costs. This makes digital data collection increasingly important for RWS.

RWS involves more centers and a larger volume of subject data, which is not necessarily generated entirely within hospitals or fully captured by hospital information systems. Therefore, the key focus of digital upgrading in the data collection phase of RWS is on leveraging machines to more accurately identify data fields and automate data entry in accordance with medical logic.

In-depth data mining unlocks greater value for RWS.In addition to differing requirements for the digitalization of data collection methods, RWS also presents distinct needs in terms of data analysis and in-depth mining, necessitating more intelligent data analytics.

In registrational clinical trials, data analysis is largely driven by the trial design, with corresponding data calculated along predefined dimensions to yield binary (“yes/no”) results, following established analytical frameworks.

Real-world studies (RWS) are more strongly data-driven, requiring iterative and in-depth data mining to generate “new leads” with guiding value. For example, RWS can uncover new indications for marketed drugs beyond those originally approved—insights that may not be pre-specified before conducting the RWS but are instead derived through data mining.

Therefore, the digitalization of data analysis in Real-World Studies (RWS) needs to be more “intelligent” to fulfill its dual mission of “validation” and “discovery.” In digital clinical trials, there are more aspects that can be enhanced through intelligence, which we will discuss separately in the next chapter (please scan the QR code at the end of the article to access the full report).

Digital Sector Sees Expanded Market, Facilitating Decentralization and Site Diversification in Clinical Trials

The Boom in New Drug Development Expands the Digital Clinical Trial Market.With strong national support for innovative drugs in recent years, the number of innovative drug R&D enterprises in China has increased, with an accelerating growth trend year by year. Furthermore, the “4+7” volume-based procurement policy is compelling capable domestic generic drug manufacturers to shift their focus toward R&D and innovation. Consequently, the number of innovative drugs approved for clinical trials in China will continue to grow rapidly.

Faced with rapidly growing demand for clinical trials, traditional approaches are clearly inadequate. Digital clinical trials can reshape collaboration among stakeholders to enable more efficient and cost-effective trial execution, delivering greater volumes of higher-precision results within the same human, material, and time resources.

Amid the rapid growth in the total number of clinical trials, while the number of clinical trial sites, potential participants, and industry practitioners cannot expand at a comparable pace, the market size of the digital clinical trial sector has experienced rapid growth. On the other hand, increasingly stringent regulatory policies, along with rising compliance requirements and costs, are making digitalization an essential necessity in the field of clinical trials, which will further expand the market size of digital clinical trials.

Digital clinical trials enable interconnectivity of information and more rational allocation and utilization of resources.Digital infrastructure has laid the foundational platform for the interconnectivity of industry information. First, key details of clinical trial centers—such as accreditation certificates, experience in clinical trial projects, and investigator profiles—are made transparent and updated in real time. By eliminating information asymmetry, sponsors gain broader options, enabling more precise site selection and higher success rates in site screening. Meanwhile, thanks to this interconnected platform, centers with underutilized capacity relative to their operational capabilities also have opportunities to secure more projects. This process helps alleviate the current imbalance where leading clinical trial centers are overloaded with projects while other centers remain underutilized.

Secondly, digitalization facilitates the conduct of multicenter clinical trials. Traditional clinical trials, which rely heavily on manual labor, are constrained in the number of participating sites due to limitations in manpower and cost. This is a key reason why many trials are concentrated in a few dozen leading large centers with substantial patient populations.

In digital clinical trials, the assistance of digital products reduces the deployment and execution costs for single sites. Furthermore, digitization enables remote operations in multiple processes, such as data monitoring, thereby enhancing the capability to implement projects simultaneously across multiple clinical trial sites. Consequently, the upper limit on the number of selectable trial sites has been raised. This provides sponsors with more numerous and flexible options for site selection, further promoting the decentralization and dispersal of clinical trial projects.

Finally, with the implementation of DRGs and tiered diagnosis and treatment, patients are gradually shifting to primary care facilities, whose capabilities are being enhanced. Coupled with deepening digital penetration, remote and decentralized clinical trial operations will have greater scope in the future, further promoting the rational allocation and utilization of clinical trial resources.

Corporate positioning is becoming increasingly clear, with multiple business models validated by the market.

Technical Service Enterprises: Broadening Product Connotations, “Solutions” Gain Market Recognition.In the early stages of the digital clinical trial industry, companies entered the market by leveraging their respective team strengths. For instance, among technology service providers, some hospital informatics companies have transformed or expanded into the digital clinical trial sector by building on their existing data integration capabilities and hospital resource bases; meanwhile, companies specializing in SaaS or software technical services have entered the clinical trial field by capitalizing on their technological advantages to provide digital solutions across various stages of the process.

Regardless of the entry strategy, most companies initially explore their business model through Software-as-a-Service (SaaS) offerings. SaaS represents a viable initial go-to-market strategy due to its advantages, including rapid deployment, convenient updates and iterations, and low cost barriers. However, as enterprises mature, the limitations of SaaS—particularly its relatively small total addressable market—become apparent. Consequently, the industry has seen the emergence of diverse business models, such as custom development and deployment for sponsors and trial sites, or enhancing product portfolios with value-added services to provide comprehensive solutions (including partial Clinical Research Organization [CRO] services) or full-scale CRO services. Research indicates that among companies offering both SaaS platforms and integrated solutions, clients predominantly prefer the latter.

CRO Companies: Entering the Market with Their Respective Strengths, Digital Firms Are Favored by Capital.Clinical trial CRO companies can also be broadly categorized into two digitalization pathways. The first comprises traditional CRO firms that leverage their domain expertise to integrate digital elements through in-house development or partnerships, thereby undergoing digital transformation and entering the digital clinical trial space. The second consists of companies that enter the market with a digital-first mindset, providing innovative clinical trial CRO services.

Research indicates that traditional CROs possess abundant industry resources, and the key to their upgrade lies in whether decision-makers attach sufficient strategic importance to digital transformation. Digital clinical trial companies, leveraging their advantage in digital mindset, are more sensitive to the digital upgrade needs across various stages of clinical trials. Furthermore, their focused business lines and lean startup teams often enable them to meet clinical trial demands more quickly and flexibly.

Currently, various business models remain to be further validated by the market. In the future, as technology service providers enhance their capability to deliver solutions and digital CROs continue to capture a larger share of the clinical trial market, digital clinical trials are likely to yield solutions and products with absolute competitiveness in certain segments—particularly those involving intelligence-driven processes. Meanwhile, digital CROs will also extend their services upstream or downstream, covering stages beyond clinical trials, such as drug discovery and post-marketing studies.

The Digital Evolution of Clinical Trials: Driven by Policy in the Short Term, Talent in the Medium Term, and Technology in the Long Term

The technology is “sufficient”; what is urgently needed are guidelines and security safeguards for data usage to facilitate its implementation.Currently, the field of digital clinical trials is in its early stages of development. According to research, less than 15% of registered clinical trials are digitized, while the digitization rate for post-marketing clinical trials stands at approximately 30%. However, from a technological perspective, the achievable level of digitization extends far beyond these figures. Technologies such as artificial intelligence (AI), big data, blockchain, and the Internet of Things (IoT) are now nearly capable of reshaping traditional labor-intensive models, giving rise to new data-driven online and remote delivery models.

Multiple factors hinder technology from realizing its true value, with the lack of direct data interoperability being a primary one. A persistent and difficult-to-bridge gap exists between clinical trial institutions and sponsors. At its core, this gap stems from concerns over data security. Although digital health companies are continuously promoting market education by emphasizing the security features of their products, there remains a lack of industry-wide standards for data security safeguards and application rules. Currently, the industry urgently requires policy support to standardize data application rules. With such regulatory guidance and robust security assurances, digital technologies can fully realize their true value across all stages of clinical trials.

To optimize traditional clinical trial processes and maximize cost reduction and efficiency gains, talent is the key.Guided and safeguarded by standardized rules for data application, related digital products can be more widely adopted in clinical trials, garnering rich and valuable user feedback that drives continuous performance improvements. This, in turn, helps traditional clinical trial processes achieve maximal cost reduction and efficiency gains during their digital transformation.

Translating user feedback (clinical trial needs) into digital solutions and presenting them as corresponding technical products is not a simple process. It requires an organic and deep integration of technology (AI, big data, IoT, VR, etc.) with medical knowledge (pathology, diagnostic and treatment habits and logic, industry guidelines, expert consensus, etc.). In this process, interdisciplinary talents with backgrounds in both technology and medical knowledge are crucial. Currently, most companies address this challenge by building teams with composite capabilities.

However, due to the distinct professional training systems and divergent problem-solving mindsets adopted by these two types of professionals, coupled with the high entry barriers in both industries, it remains challenging to foster deep integration that leverages their respective expertise to address industry-specific pain points.

Nevertheless, stakeholders across the industry are actively intensifying efforts to cultivate this type of interdisciplinary talent. For instance, enterprises are facilitating talent exchange and development by establishing various platforms, universities are proactively training relevant professionals, and numerous attempts have been made to implement joint training programs between enterprises and academic institutions. In summary, driven by supportive domestic policies, capital investment, and robust market demand, resolving the talent bottleneck is merely a matter of time. This will, in turn, elevate the cost-reduction and efficiency-enhancing capabilities of digital clinical trials to new heights.

Technology Redefines the Horizon of Possibilities, Empowering Disruptive Clinical Trials with Infinite Potential.The “endgame” of digital clinical trials may lie not merely in replacing traditional trial steps with automated systems or establishing new online and remote delivery models, but rather in introducing disruptive trial paradigms that fundamentally reshape clinical trial processes. Examples include the already-emerging decentralized clinical trials (DCTs) and the virtual clinical trials that companies are actively exploring and strategically deploying. Looking ahead, as technologies continue to advance while ensuring the reliability of results, what further disruptive clinical trial models will emerge remains a space rich with possibilities for imagination.

The above is an excerpt of the main content of the report. The complete framework of the report is as follows:

Chapter 1: Dual Drivers of Policy and Capital, Digital Clinical Trials Market Exceeds RMB 30 Billion

1.1 Completion of Information Technology Infrastructure in Clinical Trials, Entering the Early Stage of Digital Transformation

1.2 The clinical trial market exceeds RMB 60 billion, with the digital segment accounting for 15–50%

1.3 Policy Guidance Steers the Direction of Digitalization, While Capital Investment Accelerates the Digital Transformation Process

Chapter 2: Rising Penetration of Digital Products, Business Models Await Market Validation

2.1 Analysis of the Current Development Status of the Three Major Business Models of Technical Service Enterprises

2.2 Analysis of the Development Status of CRO Enterprises Providing Digital Clinical Trial Services

2.3 Compliance and Cost-Efficiency Needs Drive Higher Product Penetration, Achieving 100% EDC Adoption

Chapter 3: Compliance-Driven Completion of Industry-Wide Information Technology Infrastructure

3.1 Demand for Strict Regulatory Oversight Drives the Development of Healthcare Informatics Software, Achieving 100% Coverage

3.2 “Must-Have” Software Suffers from Severe Homogenization: Three Pathways Offer a Way Out of the Rat Race

3.3 Dual Drivers of Compliance and Cost Reduction with Efficiency Gains Lead to New Breakthroughs in Data Collection

Chapter 4: In the Early Stages of Digital Transformation, Upgrades Begin with High-Cost, Low-Efficiency Processes

4.1 Driven by the Imperative to Reduce Costs and Enhance Efficiency, New Business Models Are Urgently Needed

4.2 Project management penetration rate is approximately 50%, with local tertiary A hospitals developing at a faster pace

4.3 Reshaping the “Outreach” Phase of Subject Recruitment Based on In-Hospital and Out-of-Hospital Health Big Data

4.4 The digitalization of Phase IV clinical trials remains a blue ocean, with an urgent need for cost reduction and efficiency improvement

Chapter 5: Artificial Intelligence Enables Smarter Decision-Making in Digital Clinical Trials

5.1 Intelligent Assistance Enables Faster and Better Decision-Making Across Multiple Stages of Clinical Trials

5.2 Data Interconnectivity and Multidisciplinary Talent Are Key to Driving Intelligence

Chapter 6 Future Trends

6.1 The Digital Sector Sees a Larger Market, Facilitating the Decentralization and Dispersion of Clinical Trials

6.2 Corporate positioning has become increasingly clear, with multiple business models validated by the market

6.3 The digital evolution of clinical trials: driven by policy in the short term, talent in the medium term, and technology in the long term

Chapter 7 Corporate Case Studies

7.1 YaoYanShe (Parent Company: Miaoyi Biotechnology) – An Innovative CRO Technology Platform in the Field of Pharmaceutical R&D

7.2 BioKnow - Innovative Digital Solutions for Pharmaceutical R&D

7.3 Linyantong - Private Deployment of the Intelligent Clinical Trial Detection System

7.4 Yaoling Medical Technology: AI Empowers RWS to Uncover Post-Marketing Medical Value

7.5 Yansu Medical: AI-Driven Direct Data Acquisition, Efficiently and Compliantly Reshaping Clinical Trials

Scan the QR code below to get the full report for free.

Special Acknowledgments (in order of research interviews):

Mr. Zhang Hongwei, Vice President of Taimei Medical Technology; Wendy, Investment Manager at Sinovation Ventures; Dr. Zhuang Yonglong, Founder and Chairman of BioKnow; Mr. Duan Zhongcheng, Founder of Linyantong; Mr. Peng Yitian, Co-founder of Drug Research Society; Mr. Hu Qitong, Technical Director of Yaoling Medical Technology; and Mr. Wang Taifeng, Founder and CEO of Yansu Medical.