Vascular Interventional Robotics: A High-Growth Frontier with CAGR Exceeding 90% in China

If we were to name the buzzwords in the healthcare industry in 2022, vascular interventional surgical robots would definitely be one of them.

As a “rising star” in the field of surgical robotics, the vascular interventional surgical robot sector is experiencing rapid development, with the compound annual growth rate (CAGR) of the Chinese market expected to exceed 90%. Industry giants such as Siemens and MicroPort have entered the fray. Capital is also fueling this growth, with multiple financing rounds exceeding RMB 100 million injected into the sector.

In the field of vascular interventional surgical robots, domestic and international companies are essentially on a level playing field. With no standardized benchmarks in the market yet, product development remains highly diverse. In this capital-intensive market, what types of products truly meet clinical needs? And which companies will survive the competition?

Guided by these questions, VCBeat Research Institute conducted surveys across multiple enterprises to provide a comprehensive analysis of the vascular interventional surgical robotics industry from dimensions including industry overview, technical challenges, current market status, and future trends, aiming to deliver valuable industry insights to stakeholders and participants.

Vascular interventional surgical robots serve as the eyes, hands, and brain of physicians. Vascular intervention refers to diagnostic and therapeutic procedures performed via the vascular route using instruments such as puncture needles, guidewires, and catheters under the guidance of medical imaging. The workflow of vascular interventional surgery primarily consists of the following steps: puncture, access establishment, angiography, balloon predilation, stent deployment, and withdrawal of guidewires and catheters. Currently, except for trivial tasks such as puncture and replacement of guidewires and catheters, vascular interventional surgical robots can assist in completing most procedural steps.

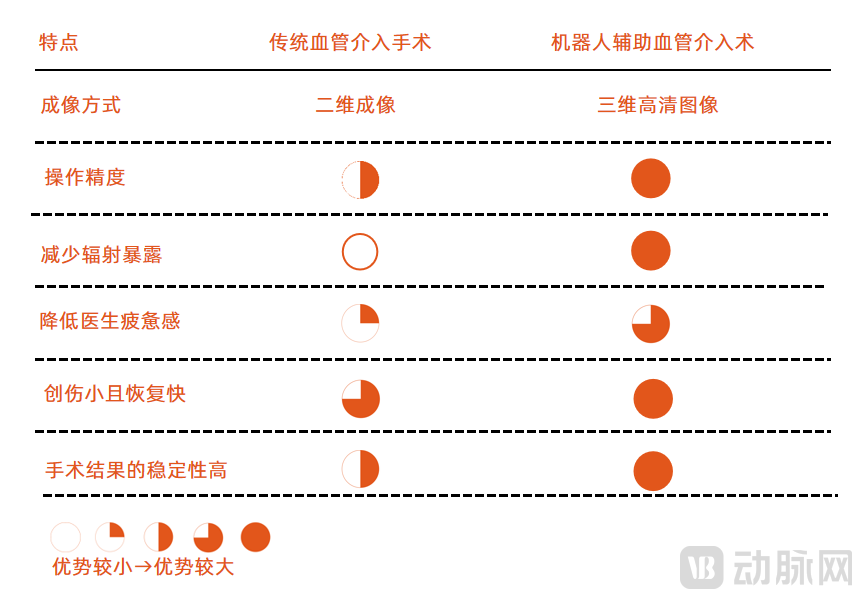

Traditional Vascular Interventional Surgery vs. Robot-Assisted Vascular Interventional Surgery Source: MicroPort MedBot’s Prospectus, Interviews

Based on functional classification, vascular interventional surgical robots can be divided into two categories: one assists physicians in performing vascular interventional electrophysiological examinations or treatments, while the other assists physicians in completing angioplasty. The former requires the use of dedicated vascular interventional instruments to manipulate active mapping catheters and electrode catheters under magnetic navigation guidance, but cannot perform various endoluminal procedures such as balloon or stent delivery. The latter is compatible with conventional interventional devices, such as small-diameter catheters and guidewires, enabling the completion of most procedures in vascular intervention without the need for customized dedicated instruments.

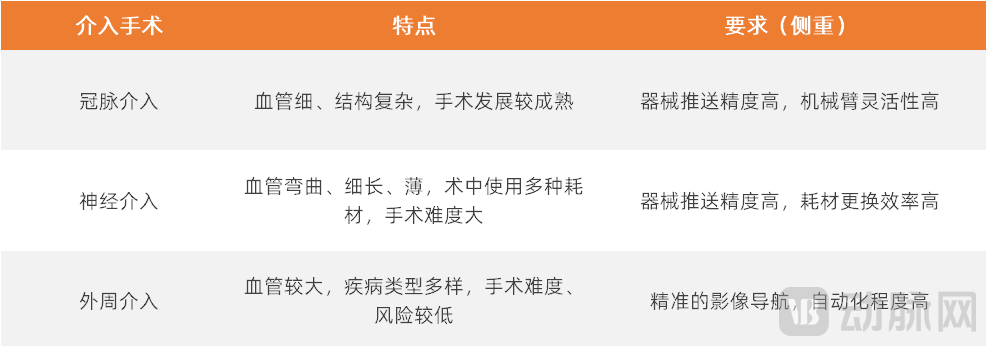

Classified by procedural technique, vascular interventional surgical robots are primarily divided into three categories: coronary intervention, neurointervention, and peripheral intervention (including aortic intervention). Globally, coronary intervention is the most mature field, with a high annual volume of percutaneous coronary intervention (PCI) procedures. Consequently, most companies developing vascular interventional surgical robots have initially focused on applying their technology to PCI procedures.

With the development of the vascular interventional surgical robot market, some companies have begun to develop pan-vascular interventional surgical robots. Relying on the design of multiple technical modules, these robots are suitable for various types of vascular interventional surgeries.

Coronary intervention is the primary target application for vascular interventional surgical robots. The coronary intervention market represents the most mature segment within the broader field of vascular interventions, with an annual volume of percutaneous coronary intervention (PCI) procedures exceeding one million. Vascular interventional surgical robots will further promote the widespread adoption of coronary interventions and drive the development of consumables such as stents and balloons. Furthermore, these robots can reduce intraoperative waste and improve the utilization rate of consumables through precise instrument delivery.

Neurointervention represents a critical bottleneck in the development of surgical robots, while peripheral intervention serves as the key to penetrating primary healthcare markets. Neurointerventional procedures are technically demanding and carry higher risks; the long navigation paths within neurovasculature and the diverse range of materials used require surgical robots to be compatible with various consumables. Although peripheral interventions are less technically challenging, they necessitate multi-disciplinary collaboration. Patients are predominantly distributed across primary care settings, where awareness of disease treatment remains low.

Despite continuous innovations in vascular interventional devices—such as the evolution from conventional balloons to drug-coated balloons, and further to stent-mounted drug-coated balloons—these advancements represent optimizations of therapeutic tools rather than changes to the overall interventional workflow. In vascular interventional procedures, operators still need to perform steps such as puncture, predilation, angiography, and stent placement under X-ray fluoroscopy in the catheterization laboratory, thereby being exposed to radiation for extended periods. The emergence of vascular interventional surgical robots has fundamentally transformed the operational paradigm for interventional physicians without altering their manual techniques. Instead of directly manipulating instruments within human blood vessels, operators now achieve remote control through a master-slave robotic system.

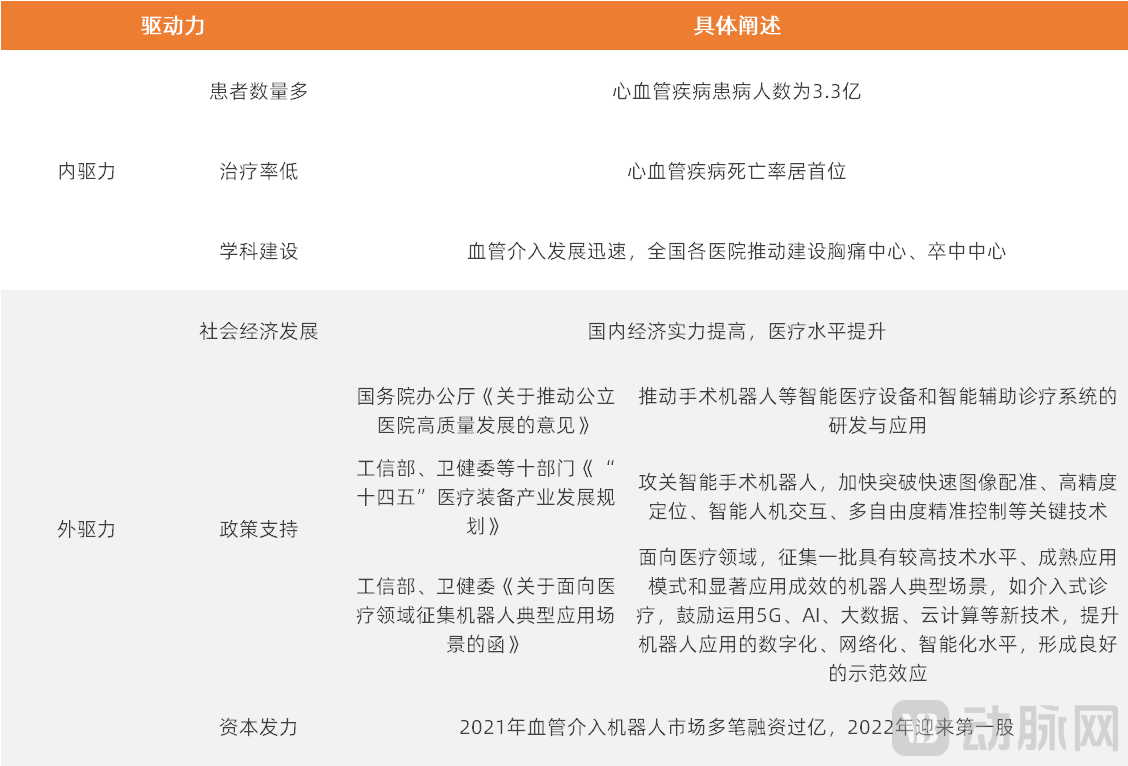

The market for vascular interventional surgical robots is a hot spot, characterized by substantial clinical demand, significant market gaps, and diverse development directions. China’s healthcare landscape has shifted from focusing on the treatment of life-threatening diseases to improving quality of life and well-being, accompanied by rising healthcare expenditures; in 2021, total national health spending exceeded RMB 7.55 trillion. This trend has laid the foundation for the application of high-end vascular interventional surgical robots.

The rapid development of China’s vascular interventional surgical robot market is driven by two main factors: first, the large patient population and the uneven distribution of medical resources between doctors and patients are promoting new clinical solutions; second, socioeconomic conditions, policies, capital, and other factors are driving corporate innovation.

Market Drivers for the Development of China’s Vascular Interventional Surgical Robotics SectorSource: VBInsight

Capital has also shown strong confidence in the development logic of the vascular interventional surgical robot market. Between 2021 and 2022, financing in China’s vascular interventional surgical robot sector was highly active, with multiple large funding rounds exceeding RMB 100 million flowing into the field.

Financing Status of Vascular Interventional Surgical Robot Companies in ChinaSource: VBInsight

From a clinical perspective, the pain points of vascular interventional procedures urgently need to be addressed. These procedures have a high threshold and significant technical difficulty, resulting in a steep learning curve for physicians. Taking neurointervention as an example, cerebral blood vessels are fragile and tortuous, requiring the use of various types and sizes of surgical instruments during complex operations. Moreover, proficiency in interventional surgery relies heavily on “practice makes perfect”; physicians must engage in long-term training to develop tactile sensitivity, leading to high initial training costs and unpredictable outcomes. Statistics show that there are only 6.48 interventional physicians per hospital on average in China.

Moreover, the uneven distribution of medical resources in China makes it difficult to achieve “homogenization” of interventional procedures. Variations in physicians’ skill levels across different regions hinder standardization, and prolonged procedural durations can impair physicians’ performance, potentially leading to human errors that result in poor patient outcomes. Meanwhile, during interventional operations in the catheterization laboratory, physicians are exposed to radiation, and wearing lead aprons can cause joint and spinal damage.

By operating vascular interventional surgical robots, physicians can access vascular regions that are difficult to reach with manual techniques, thereby enabling more complex procedures. In addition to promoting the standardization of interventional procedures and enhancing safety, vascular interventional surgical robots offer a distinct advantage by shielding physicians from radiation exposure, which naturally facilitates greater physician acceptance.

Vascular interventional surgical robots present extremely high technical barriers, integrating multidisciplinary knowledge from artificial intelligence, mechanics, electrical engineering, bionic simulation, and image-guided navigation. From an application perspective, companies adopt different entry points: some focus on standardizing coronary angiography, others prioritize the precise positioning and deployment of stents and balloons, while some emphasize comprehensive coverage of the entire surgical workflow.

Force feedback and precise motion control are the technical focal points of vascular interventional surgical robots. Robot-assisted vascular intervention leads to a loss of sensory information, creating a strong demand for force feedback. Leveraging force feedback technology, surgical robots can accurately perceive the forces exerted on instruments during the procedure and transmit the resistance encountered by the instruments in real time to the physician’s console, thereby enhancing the surgeon’s haptic sense of “presence.” However, current force feedback technologies still fail to meet the high-precision requirements of vascular interventions and largely remain at the experimental stage.

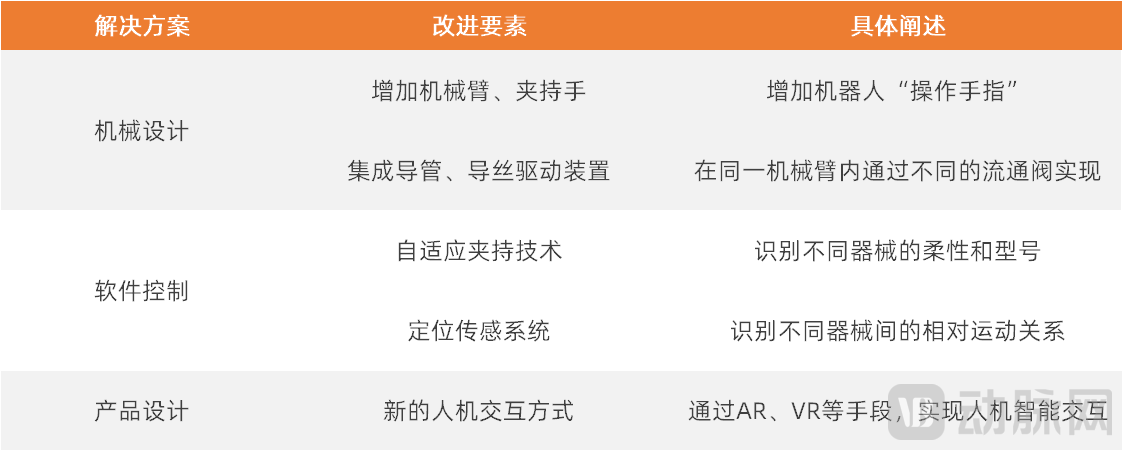

Meanwhile, throughout the entire process of endovascular intervention, operators need to use various devices such as catheters, guidewires, balloons, and stents. In certain steps, catheters and guidewires must be manipulated collaboratively within a relatively narrow space. Therefore, to cover more aspects of endovascular interventions, surgical robots must support multi-device coordination.

To achieve multi-device coordination, vascular interventional surgical robots integrate catheter and guidewire driving mechanisms into their mechanical structure. Furthermore, robotic arm designs can be optimized by incorporating grippers and increasing degrees of freedom. In terms of control software, these robots employ adaptive gripping and positioning sensing technologies to accommodate various models of catheters and guidewires, taking into account the inherent flexibility of the instruments, the relative motion between different devices, and the diversity of interventional tools. Moreover, multi-device coordination is not merely a matter of mechanical design and software control; the robots must also provide robust force feedback and multimodal image fusion, necessitating the development of novel human-machine interaction methods or operational interfaces.

Multi-Device Collaborative Solutions Source: VBInsight, Corporate Interviews

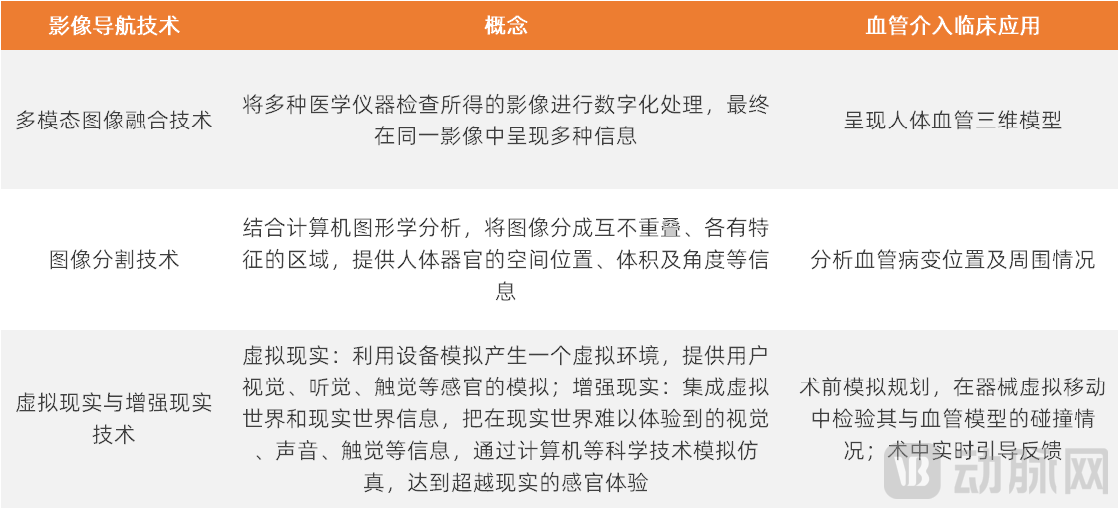

Furthermore, surgical image navigation serves as the eyes and brain of vascular interventional surgical robots. By integrating multiple types of medical imaging, such as CTA and MRI, it reconstructs three-dimensional vascular models of patients, enabling physicians to observe the overall morphology of lesions and their relationship with surrounding structures from multiple angles. Meanwhile, image navigation facilitates lesion localization and surgical path planning; it achieves real-time navigation by aligning original medical imaging data with the real-time motion information of medical devices.

Image-Guided Navigation Technology | Source: VBInsight

However, from an overall perspective, breakthroughs in individual technologies are merely a matter of time; the pace of product iteration and clinical adaptability constitute critical barriers. Vascular interventional surgical robots are the product of multidisciplinary integration, requiring consideration of technical module integration and overall system coordination. Technologies such as force feedback and multi-instrument coordination are not isolated issues pertaining to single technical modules; rather, they must be integrated into a unified system to ensure the overall safety and stability of vascular interventional surgical robots.

Current vascular interventional surgical robot products are still undergoing continuous iteration, with no standardized benchmarks yet established. Based on industry trends, we have identified five major development directions for the future:

1. Covering the entire workflow of vascular interventional surgery, breaking through the homogenization dilemma of surgical robot products.Some companies focus on intravascular procedures, leading to severe product homogenization. Intravascular manipulation is a core component of percutaneous coronary intervention (PCI). Existing surgical robots may only be actively engaged for a few minutes during the procedure, while preliminary steps such as puncture, angiography, and diagnosis still rely heavily on physicians’ individual experience and technical skills. In interventional surgeries, angiography and diagnostic processes account for 70%–80% of the total operative time. Although these tasks are fragmented and difficult to standardize, they significantly impact subsequent disease diagnosis and treatment.

To cover a broader range of surgical procedures, vascular interventional surgical robots must address compatibility with different product models and flexibility, enable sterile operations, and complete the entire workflow including unpacking, switching catheters and guidewires, and retrieval. Meanwhile, as vascular interventional surgical robot products evolve, consumables such as catheters and guidewires are advancing toward intelligence and multifunctional integration. A single catheter can perform multiple functions, eliminating the need for exchanges during surgery, thereby improving efficiency while conserving resources.

2. Suitable for various procedures including coronary, peripheral, and neuro-interventions, the pan-vascular surgical robot reduces hospital procurement costs.Due to the high cost of vascular interventional surgical robots and expensive startup fees, ideal products should adopt a modular design capable of performing coronary, neuro, and peripheral interventional procedures simultaneously. The pan-vascular interventional surgical robot is equipped with a multifunctional platform, allowing operators to select the appropriate technical modules as needed. This approach enables hospitals to save on procurement costs. The surgical robot is compatible with most commercially available guidewires, stents, and balloons, ensuring compatibility with existing catheterization laboratories without the need for customized medical devices. This facilitates in-hospital use and strengthens hospitals’ willingness to purchase.

Vascular interventional diseases share common pathologies, primarily including occlusion, stenosis, thrombosis, and reflux. The main interventional devices include catheters, guidewires, stents, and balloons. In coronary interventions, vascular interventional surgical robots must offer high precision and flexibility. In neurointerventions, in addition to achieving high precision, surgical robots must facilitate rapid and sterile replacement of consumables. In peripheral interventions, since peripheral vessels are larger, the requirements for precision are relatively lower, while the demands for image navigation technology are higher. Meanwhile, peripheral interventional treatments are less technically challenging and can be performed locally at primary healthcare institutions; therefore, there is a high demand for robot automation, aiming for balanced and consistent surgical quality, along with multidisciplinary collaboration within hospitals.

Characteristics and Requirements of Different Interventional Procedures Source: VBInsight

3. Semi-automated or even fully automated vascular interventional surgical robots represent the ultimate form, further enhancing surgical efficiency and alleviating physician fatigue.The primary information sources for automated surgery are medical images and case data, with deep learning and feedback mechanisms serving as the core technologies. Capabilities such as image processing, high precision, and rapid response are indispensable. Currently, as image segmentation and fusion technologies as well as feedback mechanisms remain immature, enterprises may begin by developing automated modules.

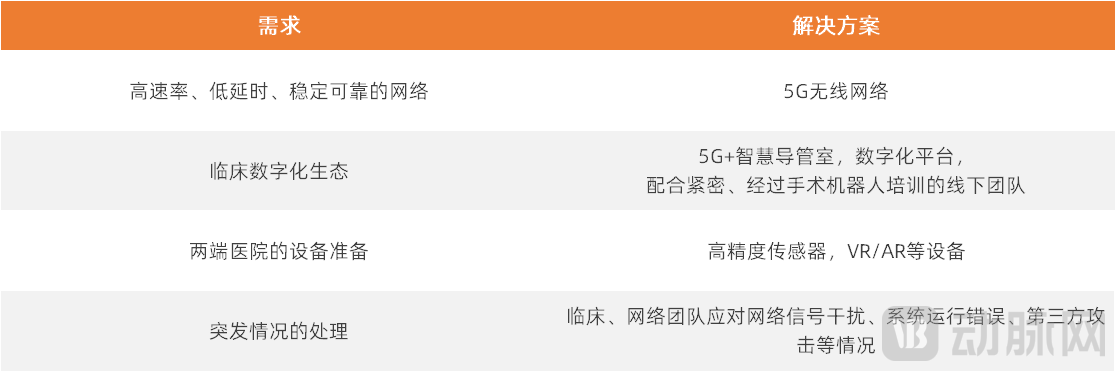

4. 5G-enabled remote acceleration is driving the widespread adoption of robotic surgery, representing a unique advantage for Chinese enterprises.“Real-time interconnectivity” is the key to remote surgery, requiring ultra-low-latency transmission of commands and imaging. In addition to relying on 5G technology with high bandwidth and low latency, hospitals need to build a high-quality 5G smart ecosystem. The safety and stability of 5G remote surgery are paramount; beyond network transmission issues such as latency and stuttering, attention must also be paid to exceptional circumstances including operational errors in online systems and third-party cyberattacks.

5G Remote Robotic Surgery Support ResourcesSource: VBInsight

In clinical applications, a significant use case for 5G remote surgery is emergency procedures. Currently, 5G remote surgery remains in the phase of clinical trials. To implement it in routine clinical settings, the issue of liability attribution must be resolved. The implementation of 5G-enabled surgeries involves three primary liable parties: hospitals, surgical robot manufacturers, and network service providers. In the event of unconventional incidents other than network latency or robotic malfunctions, determining liability proves challenging.

5. Lightweight and compact designs help reduce robot costs and improve accessibility.In addition to achieving lightweight and miniaturized designs for existing robotic products through modifications in design and materials, disposable vascular interventional surgical robots represent an alternative approach. Given the high purchase and maintenance costs associated with surgical robots, the emergence of disposable robots may also reshape their premium market positioning.

The Future of Vascular Interventional Surgical Robots: Systematization or Specialization?Vascular interventional surgical robots are still in an exploratory phase. The aforementioned technological directions can develop concurrently and are not entirely isolated. The market for these robots is flourishing, with no standardized path forward. Companies may choose to break through in niche areas by enhancing the precision and standardization of procedures such as angiography and guidewire/catheter advancement, thereby addressing complex lesions like calcified plaques and chronic total occlusions. Alternatively, they may adopt a holistic product approach to develop pan-vascular surgical robots that integrate more advanced capabilities.

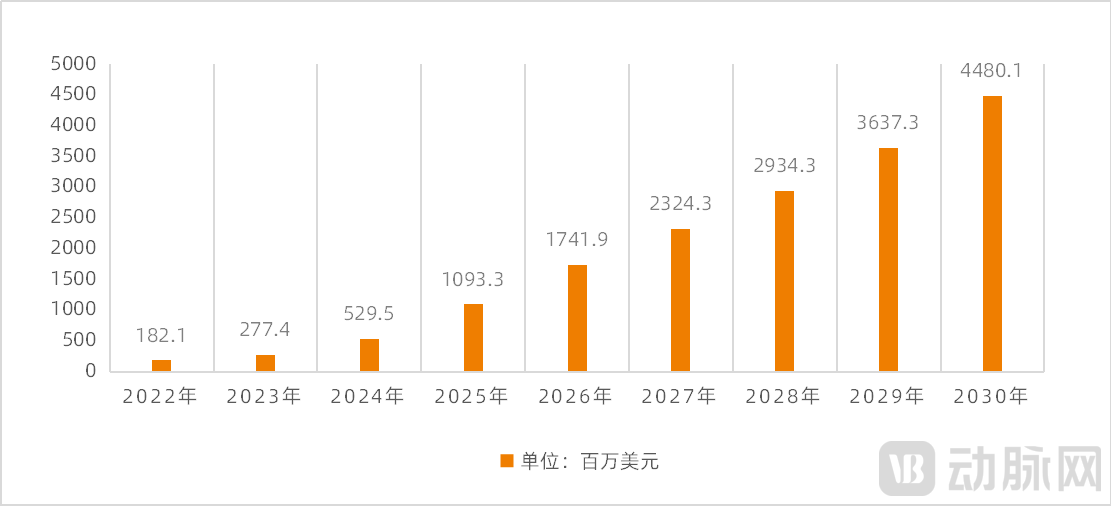

Driven by the benchmark demonstration of the da Vinci Surgical System, as well as advancements in technology, capital investment, and market demand, the global development of vascular interventional surgical robots has accelerated, leading to rapid market expansion. According to data from Frost & Sullivan: the global market size for vascular interventional surgical robots is projected to reach USD 180 million in 2022 and grow to USD 4.48 billion by 2030, representing a compound annual growth rate (CAGR) of 49.2% from 2022 to 2030.

Global Market Size of Vascular Interventional Surgical Robots, 2022–2030 (Estimated) Source: CIC Consulting

Currently, developed regions such as the United States and Europe constitute the primary markets for vascular interventional surgical robots. Globally, only a few models of vascular interventional surgical robots have received regulatory approval, predominantly in the United States or Europe. For instance, Siemens’ CorPath GRX has obtained both CE marking and FDA clearance; Robocath’s R-One has received CE marking; and Stereotaxis’ Genesis RMN and Johnson & Johnson’s Sensei X2 have secured FDA clearance.

Overview of Overseas Vascular Interventional Surgical Robotics Companies | Source: VBInsight

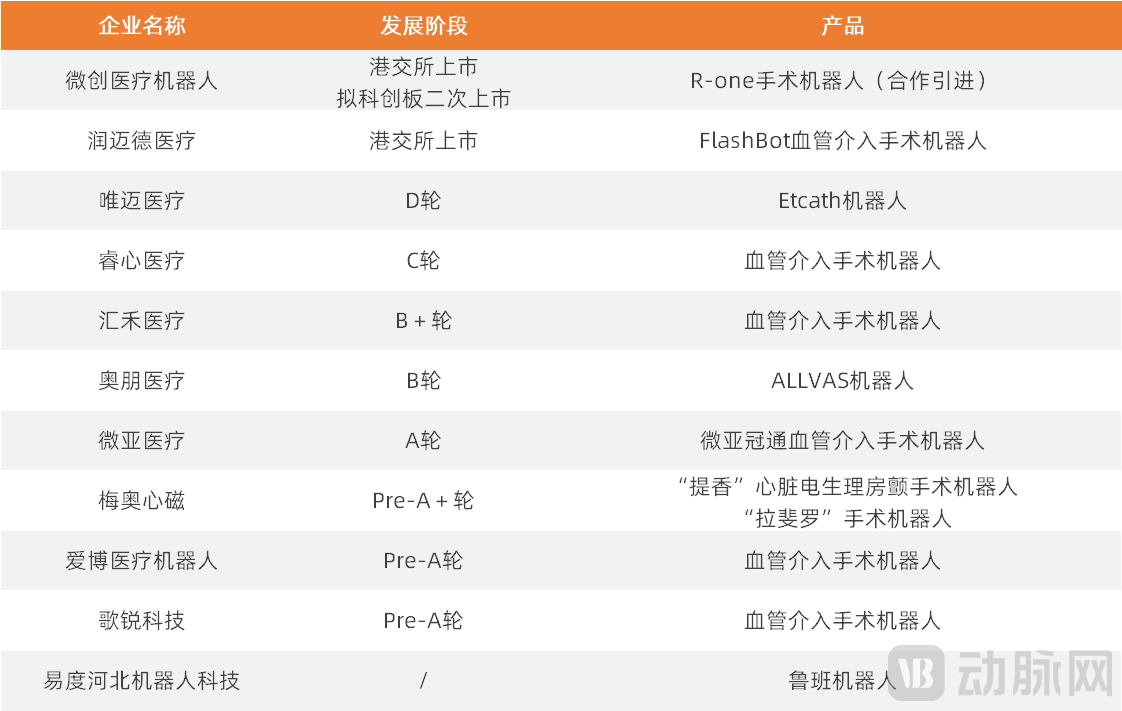

China’s vascular interventional surgical robot market is in its early stages of development, with no products yet approved. Currently, domestic companies such as MicroPort MedBot, Runmai Medical, Realsim Medical, Weimai Medical, Huihe Medical, Allvas Medical, Weiya Medical, Mayo Magnetics, and Aibo Medical Robot have entered the field of vascular interventional surgical robots, with their products primarily in the animal testing or clinical trial phases. Frost & Sullivan projects that China’s vascular interventional surgical robot market will reach RMB 33.9 million in 2022 and grow to RMB 5.824 billion by 2030, representing a compound annual growth rate (CAGR) of 90.3% from 2022 to 2030.

Overview of Chinese Vascular Interventional Surgical Robotics CompaniesSource: VBInsight

In the global market, each regional market has its own characteristics. To successfully penetrate a local market, one must first understand and comprehend its specific features; otherwise, it is difficult to simply “copy and paste” strategies from other regions. Compared with overseas markets, catheterization laboratories in China are extremely busy and operate under significant time constraints. Under volume-based procurement (VBP) and Diagnosis-Related Groups (DRG) payment systems, cost constraints are more stringent. Furthermore, clinical adoption of new technologies tends to be conservative.

Unlike the “domestic substitution” development path seen in medical devices such as coronary stents, coils, endoscopes, and staplers, domestically produced vascular interventional surgical robots are poised to follow a path of “indigenous innovation.” Chinese companies are well-positioned to enter the global market and compete with their overseas counterparts.

Currently, overseas vascular interventional surgical robotics companies such as Siemens, Robocath, and Stereotaxis are accelerating their entry into China. Among them, Siemens is directly entering the Chinese market based on a localization strategy, while the French company Robocath and Stereotaxis are both entering China through collaborations with local enterprises.

In comparison, these overseas companies enjoy the following advantages: their vascular interventional surgical robot products were developed earlier, have already received regulatory approval abroad, and their safety and efficacy have been clinically validated. However, domestic companies also possess many unique advantages: they hold core patents, thereby avoiding patent blockades; they apply cutting-edge technologies such as 5G, computational fluid dynamics, and image-guided navigation to vascular interventional surgical robots; they benefit from localization advantages through close collaboration with domestic clinical institutions; and they achieve rapid product iteration.

As previously mentioned, vascular interventional surgical robots will cover the entire surgical procedure, expand the range of indications, and enable coordinated operation with a wider array of vascular interventional devices, while evolving toward remote operation, intelligence, miniaturization, portability, and cost-effectiveness.

As the penetration rate of vascular interventional surgical robots continues to rise, vascular interventional devices will also evolve into robot-specific versions. Some device manufacturers may develop stent delivery handles and balloon dilation catheter handles that are better suited for operation by vascular interventional surgical robots; they may also innovate new devices to address current pain points in robotic vascular interventions, such as all-in-one catheters and intelligent consumables.

For instance, current vascular interventional surgical robots have limitations in catheter and guidewire exchanges. A multi-functional catheter can integrate multiple capabilities, such as serving as a support catheter and an instrument delivery device, thereby avoiding or reducing the need for catheter and guidewire replacements. This enhances the robot’s coverage of surgical maneuvers and procedural workflows in vascular interventions.

Beyond the products themselves, the market for vascular interventional surgical robots will not experience “involution” in the short term, with companies engaged in healthy competition. First, in the field of high-end medical devices, hospital procurement is not driven solely by price or a race to the bottom. Second, when setting prices, manufacturers of vascular interventional surgical robots take into account multiple factors, including product differentiation advantages, R&D and production costs, policy guidance, and the competitive landscape. Finally, during their early development stages, these companies are focused on expanding the market and growing the overall industry rather than engaging in price wars.

From the perspective of market structure, the vascular interventional surgical robot market will undergo a transition from fragmentation to consolidation. As the market matures, certain companies will see their market shares eliminated, others will be acquired or merged, while a select few will rise with the trend, capturing the vast majority of the market and emerging as representative enterprises in the domestic high-end medical device sector.

In such circumstances, companies with unique product advantages, strong R&D innovation capabilities, experienced and well-resourced commercialization teams, comprehensive patent portfolios, and robust supply chain management, production, and quality control capabilities are more likely to emerge as the ultimate winners.

The above is an excerpt of the main content of the report. The complete framework of the report is as follows,Scan the QR code to get the full report for free。

Chapter 1: The Dark Horse in a Multi-Billion-Dollar Market, Vascular Interventional Surgical Robots Become a Market Hotspot

I. The Emergence of Vascular Interventional Surgical Robots: Paving the Way for Intelligent and Precise Interventional Procedures

II. Rapid Development of Vascular Intervention, with Coronary Intervention as the Primary Market for Vascular Interventional Surgical Robots

III. Major Players Enter the Arena, Vascular Interventional Surgical Robots Become a Hot Sector

Chapter 2: Technological Breakthroughs and Accelerated Product Iteration Make Clinical Applicability the Core Element

I. Pain Point-Driven: Vascular Interventional Surgical Robots Promote Standardization of Interventional Procedures and Extend Physicians' Career Longevity

II. Multidisciplinary Integration Creates High Barriers for Vascular Interventional Surgical Robots

III. Five Major Development Directions: The Vascular Interventional Surgical Robot Market Continues to Innovate

Chapter 3: China’s Market Growth Rate to Exceed 90%, Domestic and Foreign Companies on an Equal Footing

I. Europe and the US Dominate the Major Markets, While China’s Market Holds Significant Future Potential

II. Differences Exist Between Domestic and Overseas Markets; the Domestic Market Is Constrained by Time, Cost, and Demand

III. Starting from the Same Line, Domestic Companies Achieve Multiple First-Ever Surgeries

IV. Overseas Companies Accelerate Entry into China, While Domestic Firms Possess Hidden Advantages

Chapter 4: Future Trend Analysis—Vascular Interventional Surgical Robots Moving Toward Full Intelligence and Full Automation

I. Digitalization Lays the Foundation for Fully Intelligent and Fully Automated Systems

II. Specialized Version of Vascular Interventional Device-Derived Robots

III. Companies Prioritize Market Expansion in the Early Stages of the Industry

IV. Growing Through Competition: Those Without Weaknesses May Monopolize the Market

Chapter 5: Analysis of Innovative Cases—A Hundred Flowers in Bloom, Differentiated Layout

I. RainMed Medical—The First Listed Company in Vascular Interventional Surgical Robotics, a Domestic Enterprise with Comprehensive Strengths in Both Hardware and Software

II. Ruixin Medical – Providing a Full Suite of Software and Hardware Solutions from Diagnosis to Treatment of Cardiovascular and Cerebrovascular Diseases

3. Siemens Corindus – Acquired by a Giant, the First Vascular Interventional Surgical Robot to Launch Globally

IV. Robocath—In Collaboration with MicroPort, the R-One Surgical Robot Becomes the First to Complete Registration Clinical Trials