Intracardiac Echocardiography (ICE) Industry Overview and Product Landscape: A Prospectus Submission

Editor's Note: This article was originally written by Kaicheng Capital and published with authorization from VCBeat.

In recent years, with the expanding application of interventional and minimally invasive therapies for cardiovascular diseases, new therapeutic techniques have been continuously innovated. Various echocardiographic technologies have been employed, including conventional transthoracic echocardiography (TTE), transesophageal echocardiography (TEE), intracardiac echocardiography (ICE), myocardial contrast echocardiography (MCE), and three-dimensional echocardiography. This article will focus on intracardiac echocardiography (ICE); therefore, the following discussion will primarily center on this topic.

Intracardiac Echocardiography (ICE)Intracardiac echocardiography (ICE) involves mounting a miniature transducer on the tip of a cardiac catheter, which is then advanced via peripheral veins into the cardiac chambers. The transducer emits ultrasound waves, and the received echoes are processed by a computer to generate ultrasound images. This technique provides high-resolution, real-time visualization of intracardiac anatomical structures as well as other intracardiac catheters and devices, enabling real-time monitoring of hemodynamic status. It is not obstructed by surrounding structures such as the ribs and does not require general anesthesia.

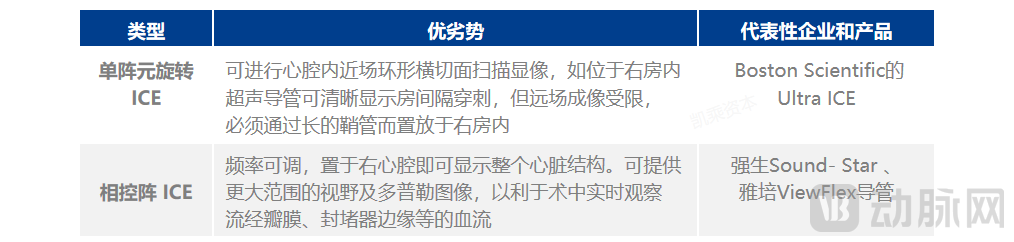

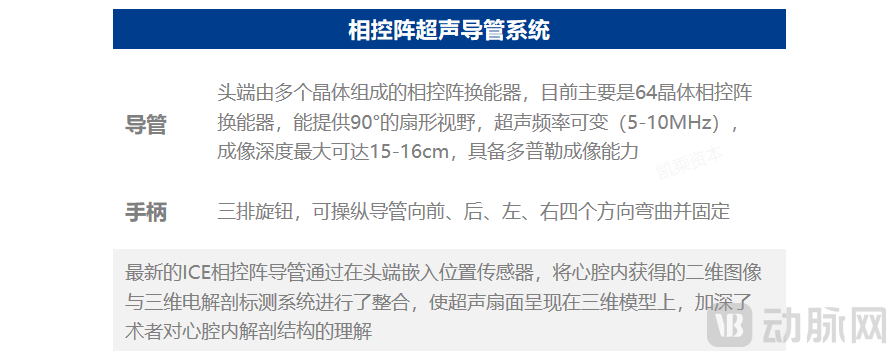

ICE utilizes ultrasound frequencies of 5–12 MHz, achieving a theoretical maximum resolution of 0.1 mm and a maximum intracardiac imaging penetration depth of 16 cm. Common 2D ICE catheters are categorized into two types: single-element rotating ultrasound catheters and electronic phased-array ultrasound catheters, with the latter being more widely used in clinical practice. Currently, ICE catheters have diameters ranging from 8 to 10 Fr.

Source: Compiled by Kaicheng Capital

Source: Compiled by Kaicheng Capital

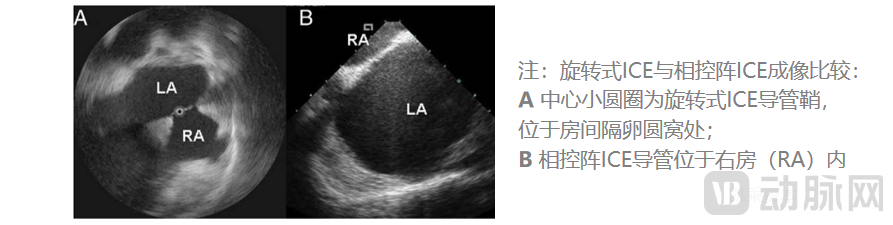

In terms of 2D ICE, phased-array ICE offers the following advantages over single-element rotating ICE: deeper imaging depth and the ability to acquire Doppler color flow imaging. Consequently, phased-array ICE is more favored among 2D ICE technologies.

Source: Compiled by Kaicheng Capital

Source: Compiled by Kaicheng Capital

ICE imaging is performed by the operator rotating the catheter (clockwise/counterclockwise rotation of the handle) and manipulating the two knobs on the catheter handle. Since the catheter probe needs to be manipulated within the right atrium, the most common complication during ICE use is transient atrial tachycardia, with an incidence rate of approximately 4%.

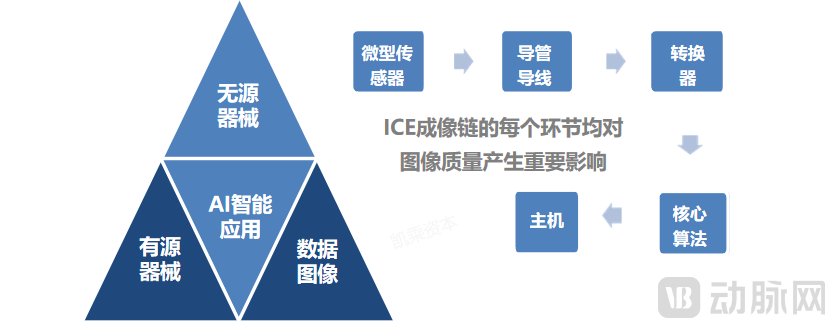

ICE has a high entry barrier and integrates the most advanced technologies in ultrasound and image processing, making it the most challenging area in intracardiac echocardiography (ICE). It requires capabilities to integrate catheter packaging, ultrasound mainframes, probes, sensors, and imaging algorithms. Probes, sensors, and AI algorithms are the core key technologies of ICE, currently mastered by only a few foreign manufacturers that have established strong patent barriers and closed-loop commercial barriers.

Source: Compiled by Kaicheng Capital

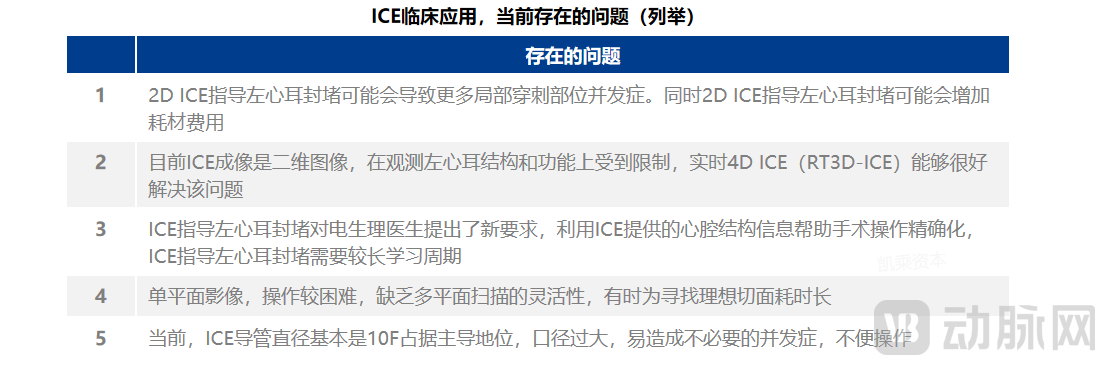

However, the vast majority of current intracardiac echocardiography (ICE) systems still rely on two-dimensional scanning or assist with three-dimensional image reconstruction via 3D electroanatomic mapping (3D-EAM), failing to achieve real-time three-dimensional reconstruction during left atrial appendage closure (LAAC) procedures comparable to that of transesophageal echocardiography (TEE). Consequently, a significant unmet clinical need remains. In this context, four-dimensional (i.e., real-time three-dimensional) ICE catheters have been developed. Featuring a wider imaging field of view, these catheters can acquire × real-time volumetric ultrasound images, thereby overcoming the limitations of traditional 2D-ICE. This enables real-time multiplanar reconstruction of interventional devices and surrounding anatomical structures, facilitating higher-quality three-dimensional modeling.

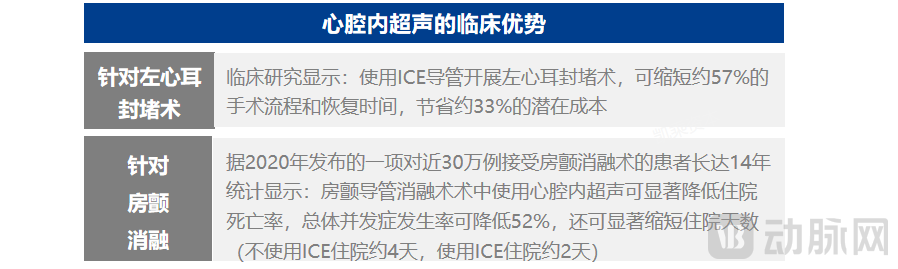

Clinical data indicate that intracardiac echocardiography (ICE) enhances the precision and safety of procedures such as radiofrequency ablation for atrial fibrillation and left atrial appendage closure, thereby reducing surgical risks and complications, lowering procedural costs, and improving patient comfort and operational efficiency. Additionally, ICE effectively reduces X-ray usage, minimizing radiation exposure for both patients and physicians. Further clinical studies have shown that using 4D ICE catheters for left atrial appendage closure can shorten procedural workflow and recovery time by approximately 57% and reduce potential costs by about 33%. ICE improves the accessibility of endovascular interventions and is expected to achieve widespread adoption comparable to digital subtraction angiography (DSA) in the future.

Source: Compiled by Kaicheng Capital

Of course, although the benefits of ICE far outweigh its drawbacks, certain issues remain. We believe that with continued commercialization and rapid technological advancements, ICE itself will continually improve, ultimately becoming an indispensable tool for interventional procedures.

Source: Compiled by Kaicheng Capital

Source: Compiled by Kaicheng Capital

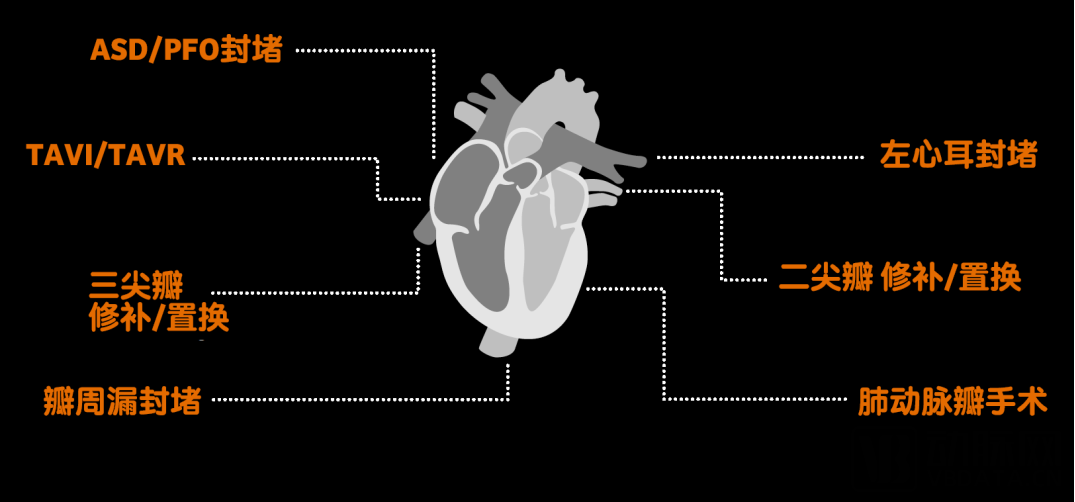

ICE is increasingly being applied in intraoperative monitoring for cardiac electrophysiology procedures, minimally invasive valvular heart disease treatments, cardiac pacing therapies, and transcatheter closure of congenital heart defects, while also playing an increasingly important role in the preoperative diagnosis of complex structural heart diseases. Currently, its most mature application lies in the management of arrhythmias.

4D ICE in Structural Heart Disease

4D ICE in Structural Heart Disease

Source: Siemens Healthineers Ultrasound, Kaicheng Capital Compilation

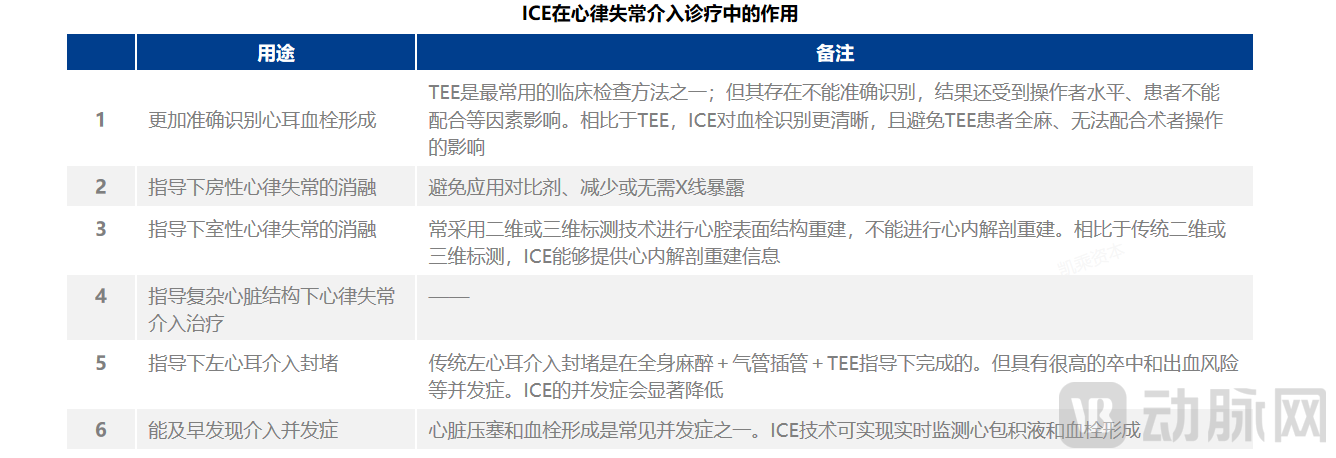

Traditional electrophysiological therapy primarily relies on X-ray fluoroscopy and electrophysiological mapping catheters for localization. Due to the inability to provide a fully clear view of the intracardiac anatomy, this approach is prone to perioperative complications such as cardiac tamponade and pulmonary vein stenosis, resulting in a high recurrence rate. Intracardiac echocardiography (ICE) allows the catheter probe to be positioned within the right atrium or right ventricle, providing real-time, high-resolution images of the left atrium, left ventricle, and pulmonary vein ostia, thereby enabling surgeons to precisely guide ablation procedures.

Source: Progress in the Application of Intracardiac Echocardiography in Cardiac Interventional Diagnosis and Treatment; compiled by Kaicheng Capital

Source: Progress in the Application of Intracardiac Echocardiography in Cardiac Interventional Diagnosis and Treatment; compiled by Kaicheng Capital

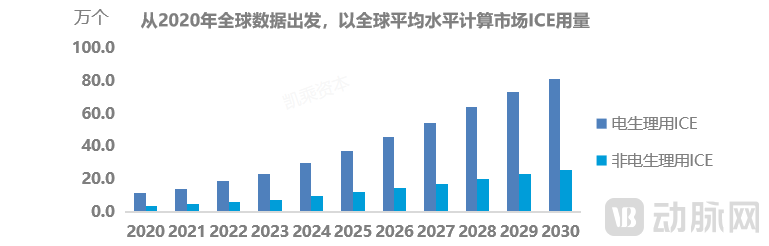

The volume of relevant surgical procedures in China has been increasing year by year. The penetration rate of interventional therapies lags significantly behind that of developed countries overseas, indicating that intracardiac echocardiography (ICE) in China holds substantial potential for explosive market growth.

Source: National Interventional Cardiology Forum, compiled by Kaicheng Capital

Source: National Interventional Cardiology Forum, compiled by Kaicheng Capital

From the perspective of electrophysiology (EP) interventional procedures, the volume of EP procedures in the United States was 1,302.3 per million people in 2019, compared with 128.5 per million people in China. In terms of valvular interventions, it is estimated that the penetration rate of transcatheter aortic valve replacement (TAVR) was approximately 23.4% in the United States and about 0.3% in China in 2019; the surgical treatment rate for mitral regurgitation was only 2% in the United States and merely 0.5% in China. Regarding congenital heart disease (CHD) interventions, the penetration rate of interventional therapy for CHD in Europe and the United States was approximately 60%, whereas in China, it was only about 22% in 2019.

Overall, there are substantial gaps between China, Europe, and the United States in the penetration rates of electrophysiology (EP), transcatheter aortic valve replacement (TAVR), and interventional therapies for congenital heart disease (CHD). The disparity in intracardiac echocardiography (ICE) penetration is also particularly pronounced. Data indicate that ICE penetration exceeds 90% in EP procedures in the United States, whereas Johnson & Johnson’s target penetration rate for atrial fibrillation management in China next year is only around 50%. This highlights significant room for growth in the Chinese market.

Source: Global Market Insights, etc.; compiled by KaiCheng Capital

According to data from VCBeat, intracardiac echocardiography (ICE) catheters currently cost approximately RMB 20,000 per unit in the market. Assuming a 10% penetration rate, the market size for ICE catheters in China will exceed RMB 10 billion. The console systems for ICE are priced at around RMB 1 million per unit. If only one console is installed per tertiary hospital (excluding non-tertiary hospitals), the market size for ICE consoles will exceed RMB 1.4 billion.

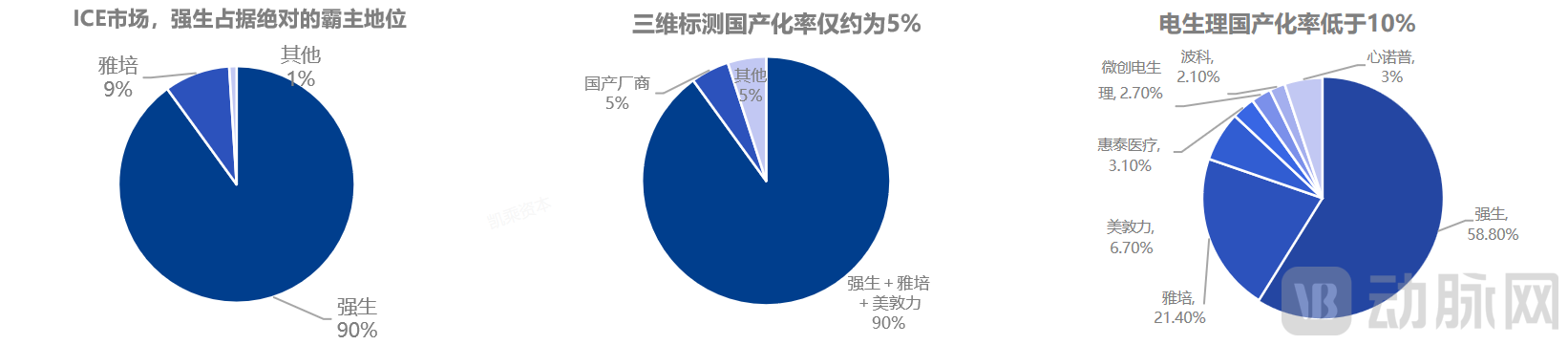

In China, the dominant model for intracardiac echocardiography (ICE) systems remains one of imitation and follow-on development. There is a pronounced reliance on foreign manufacturers for core components and key algorithms, resulting in a substantial gap between domestic and imported products. Meanwhile, due to the significant advantages of ICE systems, their indications are rapidly expanding, and expectations for centralized volume-based procurement are accelerating. In this context, while foreign brands hold an absolute leading position in this multi-billion RMB market, high-quality domestic enterprises still have substantial opportunities to capture value.

1. Intracardiac Echocardiography (ICE) has extremely high technical barriers, and core components of major domestic manufacturers still rely on imports.

The core technologies and manufacturing processes of ICE primarily include ultrasound transducers, cables, and software imaging algorithms. Interviews indicate that transducer size and sensitivity are critical to the final performance of ICE systems. These two factors are positively correlated: while clinical practice demands the smallest possible transducer size, reducing the size inevitably leads to a decrease in sensitivity.

Currently, major domestic manufacturers in this field have yet to resolve core imaging algorithm issues, necessitating the basic reliance on imported ultrasound probes from abroad. Furthermore, the required cables closely follow Johnson & Johnson’s technical pathway, with evident signs of imitation. Their capacity for rapid and sustainable technological iteration remains to be seen, and they are likely to face significant patent challenges in international competition.

2. Foreign companies still maintain absolute control over the domestic ICE and 3D mapping system markets, making import substitution a promising prospect.

Drawing on the development models of international ICE and 3D mapping leaders, their business models are all built around complete “system + equipment + consumables” solutions, with 3D navigation systems based on closed-loop algorithms that are incompatible with mapping and ablation catheters from other brands. We anticipate that domestic manufacturers must intensify R&D in algorithms to establish their own closed-loop moats if they are to break through. In the field of 3D mapping systems, contact mapping is currently the most advanced mainstream technology, adopted by leading Chinese manufacturers such as MicroPort EP and Huitai Medical; non-contact mapping technologies also exist. According to estimates by CICC, Johnson & Johnson’s CARTO system holds the largest market share in China, estimated at 60–80%, and there remains a substantial gap between the mapping and algorithm capabilities of major Chinese manufacturers and those of J&J.

According to 2020 data, domestically produced products are mainly concentrated in atrial septal puncture systems and simple mapping catheters; no domestically produced ICE catheter system has been successfully commercialized.

Source: MicroPort EP Prospectus, compiled by Kaicheng Capital

In the 2D ICE market, Johnson & Johnson holds over 90% of the market share in China, with the remainder accounted for by Abbott; domestic products have a 0% market share, making import substitution urgently needed. Currently, there are no approved products in the 4D ICE market in China.

3. Intracardiac Echocardiography (ICE) is currently primarily used in electrophysiology, with interventional therapy for structural heart disease representing one of the next major growth areas.

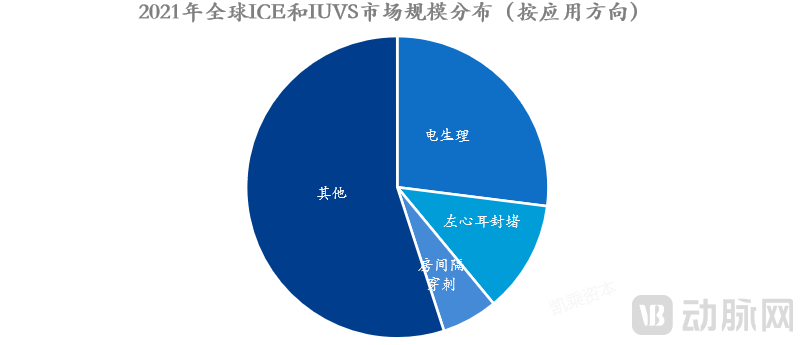

According to Global Market Insights data, in terms of application areas, global ICE usage in 2021 was primarily concentrated in electrophysiology and left atrial appendage closure, accounting for nearly 45%, with atrial fibrillation representing the vast majority. In the United States, the penetration rate of ICE in electrophysiology exceeds 90%, whereas in China, it is only one-tenth of that in developed countries. Reports indicate that Johnson & Johnson aims to achieve an ICE penetration rate of over 50% in China’s atrial fibrillation market by 2023, striving for a total ICE consumption of nearly 90,000 catheters. The application of ICE in China is poised for explosive growth.

Source: Global Market Insights, compiled by KaiCheng Capital

We believe that with the rapid adoption of interventional procedures for structural heart diseases, such as congenital heart disease, valvular heart disease, cardiomyopathy, and large vessel disorders, the penetration rate of intracardiac echocardiography (ICE) catheters in structural heart interventions will rise quickly. According to industry insiders, Johnson & Johnson has already begun establishing a team dedicated to ICE applications in structural heart disease this year, and large-scale market promotion is expected to commence next year. The market for ICE in electrophysiology and structural heart interventions is poised for substantial growth. Furthermore, we anticipate strong and steady growth prospects for ICE as its applications expand into interventional therapies for numerous other conditions.

4. High prices are the key constraint on the rapid adoption of ICE products, with expectations of centralized procurement accelerating

Currently, the clinical price of ICE is relatively high. According to incomplete statistical data, the unit price of mainstream 2D ICE products already on the market is around RMB 20,000. Due to limited short-term market volume, the per-unit cost of 4D ICE products in the medium to short term after mass production is estimated to be approximately RMB 12,000. The high price severely restricts the product's penetration into lower-tier markets and its rapid promotion and adoption.

Against this backdrop, on August 26, 2022, the Fujian Provincial Healthcare Security Administration released the “Provincial Alliance Centralized Volume-Based Procurement Plan for Cardiac Electrophysiology Interventional Medical Consumables (Draft for Comment),” formally considering the inclusion of 10F 2D ICE catheters in volume-based procurement, with an estimated participation from more than 15 provinces. This policy has placed most mainstream domestic manufacturers in an awkward predicament, as their products are still in the R&D or clinical trial stages yet face imminent inclusion in centralized procurement. From a capital perspective, the profit margins and revenue potential of this product pipeline have shrunk significantly, resulting in a severely imbalanced return on investment. Chinese manufacturers urgently need to initiate the development and iteration of new ICE products to establish differentiation from 10F ICE catheters.

We believe that, at present, companies can draw on the practices of certain international centers regarding the reuse of devices after strict sterilization to accelerate the market penetration of ICE products. By implementing rigorous cost control at the source of production and R&D, establishing foundational core technology platforms, and mastering multiple key technologies, companies can reduce reliance on imports and accelerate product iteration, innovation, and optimization. This approach not only helps enterprises stand out in intense homogeneous competition but also supports their expansion into international markets and broadens the patient population eligible for these products. Furthermore, differentiated products can mitigate the risks associated with centralized volume-based procurement, provide more options for patients and operators, address the current market issue of limited product diversity, and enhance corporate resilience against risks.

Additionally, according to incomplete statistics, as of now, global medical device giants such as Siemens, Philips, GE HealthCare, Johnson & Johnson, Abbott, and Boston Scientific have all entered the intracardiac echocardiography (ICE) market. However, due to the extremely high technical barriers, Johnson & Johnson basically holds a monopolistic position in the global market.

Source: Compiled by Kaicheng Capital

Source: Compiled by Kaicheng Capital

In China, there are currently four approved 2D ICE products, supplied by Boston Scientific, Johnson & Johnson, and Abbott. All of these are 2D ICE devices, and the market is completely monopolized by imports, with Johnson & Johnson and Abbott holding absolute dominance. Domestic manufacturers’ 2D ICE products remain in the R&D and clinical stages, and the vast majority of these companies still focus on 2D ICE as their core product pipeline. Due to the exceptionally high technical barriers associated with 4D ICE, few domestic companies have made genuine strategic investments in this area.

Source: Compiled by Kaicheng Capital

From the perspective of the 4D ICE system, Philips and Johnson & Johnson successively obtained regulatory approval for market launch abroad in 2021 and rapidly initiated commercialization. Industry forecasts suggest that imported 4D ICE products are expected to enter the Chinese market as early as 2024. Overall, the 4D ICE market remains in its nascent stage. Given the limited number of domestic companies currently developing 4D ICE technologies, it is anticipated that both domestically produced and imported products will be launched simultaneously, jointly addressing the substantial unmet clinical demand.

Author Biography

WinX Capital is a leading investment bank in China’s healthcare sector. Headquartered in Beijing and Shanghai, it serves over 3,000 active institutional investors and industrial groups. From 2020 to 2022, WinX Capital was consecutively recognized by Qimingpian & Xinsheng Chuangfu as “Top 2 Best Financial Advisors in Healthcare (2021–2022),” “Top 4 Best Financial Advisory Firms in Healthcare (2020),” “Top 10 Most Active Financial Advisors (2021),” “Top 6 Comprehensive Financial Advisors (Mid-2022),” and “Top 7 Most Active Financial Advisors (Mid-2022).” It was also listed among 36Kr’s “WISE 2020/2021 Top 5 Most Promising Emerging Investment Banks in China” and received VCBeat’s “Pengcheng Award: Top 5 Healthcare Financial Advisors of the Year (2022).”

*References

1. Advances in the Application of Intracardiac Echocardiography in the Interventional Diagnosis and Treatment of Atrial Fibrillation

2. Advances in the Clinical Application of Intracardiac Echocardiography

3. MicroPort EP Prospectus

4. China Interventional Cardiology Forum