Global Healthcare Investment Report Q3 2022: Capital Retreats, Investors Turn Pragmatic

Verily

Hardware and Software Developer in the Health Field

I. Financing activity in Q3 2022 failed to match previous levels, with both total financing amount and number of financing deals declining. Affected by macroeconomic forces such as inflation and supply chain challenges, coupled with a shift in investor sentiment from the peak seen in 2021, the market experienced significant volatility in the first half of 2022, which directly impacted financing expectations for the third quarter.

II. In the medical device industry, the competitive advantage of IVD has weakened; in contrast, the therapeutic equipment sector has risen rapidly due to frequent large-scale financing rounds. Benefiting from policy support, domestic targeted small-molecule oncology drugs have garnered significant attention. Investment in the digital health industry has declined, with financing in the digital mental health segment slowing down amid receding capital inflows and poor performance in the secondary market.

3. Global investment institutions are becoming increasingly cautious, with a tendency to concentrate on early-stage biopharmaceutical companies; the influence of domestic local government-guided "early-stage and small-scale investment" continues to provide support.

IV. China leads the world in the number of domestic financing events; Guangzhou surpasses Beijing in financing activity, driven by its favorable market environment and policy support.

V. Top 10 Most-Funded Companies in Q3 2022: Verily Leads Globally with $1 Billion in Funding, While the CXO Sector Sustains High Prosperity.

1.1 In Q3 2022, global and domestic healthcare financing was significantly impacted by the economic environment, while overseas markets showed signs of recovery

In Q3 2022, the global primary healthcare market recorded 671 financing deals with a total funding amount exceeding $16 billion. Both figures showed significant year-on-year declines, falling short of the capital surge seen in the healthcare industry in 2021 and also below the levels of the same period in 2020. Meanwhile, compared to the optimistic start of 2022, when the total funding amount decreased but the number of financing deals hit a record high, the primary healthcare market in Q3 2022 appeared somewhat sluggish.

China’s trends are largely in sync with global patterns, with a more pronounced decline in total financing, reaching a five-year low. It is worth noting that in the third quarter, China was hit by the combined impact of multiple external factors, including frequent localized outbreaks of COVID-19, the escalation of the Russia-Ukraine conflict, and the Federal Reserve’s tightening of monetary policy, which affected capital market expectations. However, the impact of such shocks on the primary healthcare market may not be long-lasting. As overseas markets gradually recover in September, new opportunities are expected to emerge for domestic healthcare investment in Q4 2022.

1.2 Biopharma’s Large-Scale Financing Widens the Gap with Other Sectors, While Digital Health Capital Cools Down

In Q3 2022, there were 35 financing deals exceeding $100 million globally in the healthcare sector, accounting for approximately 46% of the total financing amount in Q1. This ratio was about 4-5 times that of the same period in 2021 and Q1 2022; the reason for this phenomenon is the overall shrinkage of the capital market in the third quarter, with a more pronounced "head effect."

Financing deals in the tens of millions of dollars were the most numerous. Unlike previous periods, the biopharmaceutical sector maintained a distinct advantage in this funding range, widening the gap with companies in the digital health and medical device sectors.

In million-dollar financing rounds, the early-stage advantage of digital health projects is gradually narrowing compared to the same period last year. This quarter, investor interest in startups within the medical device and pharmaceutical sectors has increased.

2.1 Global Healthcare Financing Shrinks Overall, While China’s Digital Health Sector Cools Down

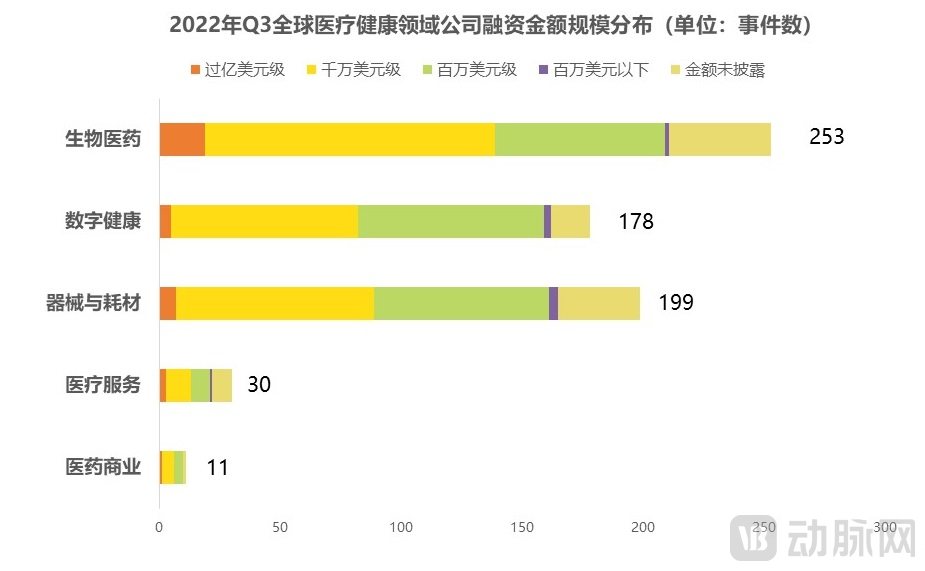

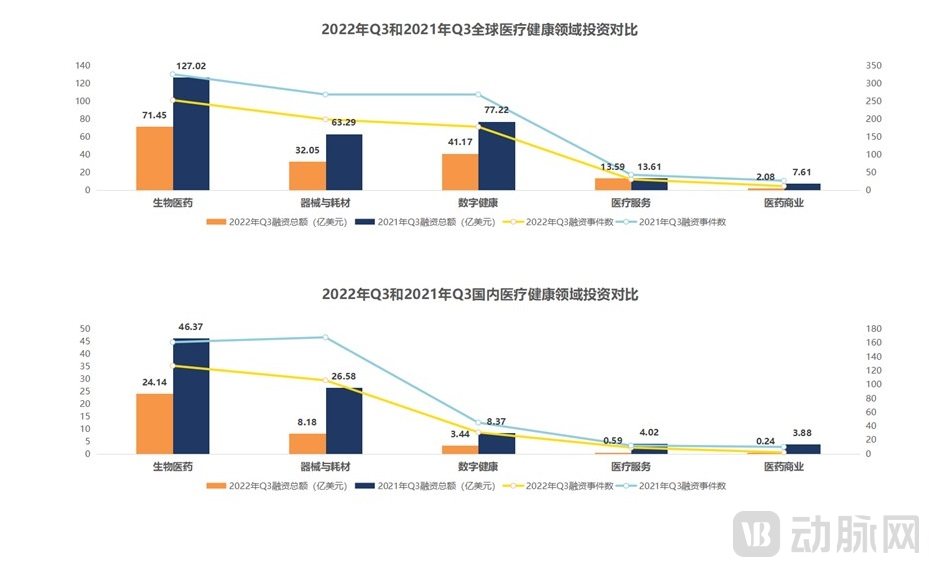

In Q3 2022, the global biopharmaceutical sector once again led all subsectors with 253 transactions totaling $7.145 billion (approximately RMB 51.145 billion). The medical device and digital health sectors followed closely behind, with 199 and 178 transactions, respectively.

Compared with Q3 2021, the total global financing amount and the number of financing deals across all sectors have declined to varying extents this year.

2.2 Top Global Financing Tags: Biopharmaceuticals, Healthcare IT, and R&D and Manufacturing Outsourcing

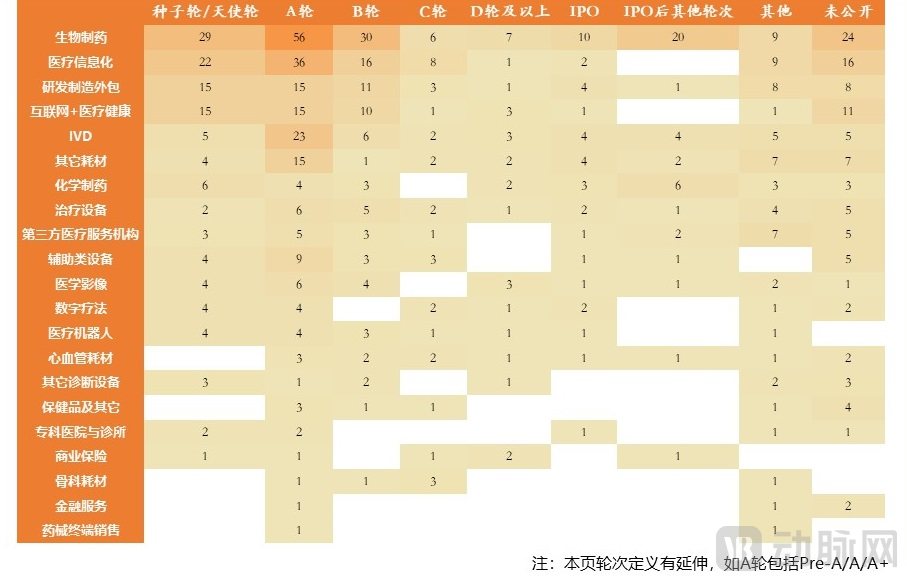

In Q3 2022, tags such as biopharmaceuticals, healthcare informatics, R&D and manufacturing outsourcing, and internet health garnered high levels of attention.

From the perspective of funding rounds, public financing in Q3 2022 was concentrated primarily in the early stages, particularly Series A.

Few companies reach Series D and beyond; those that secure large-scale financing are mostly developing innovative products, such as targeted therapy developer RayzeBio and cardiovascular disease drug developer Orchestra BioMed.

Thirty-eight companies went public this quarter, one-third the number of listings in Q3 2021.

It is evident that the “capital winter” in the global healthcare sector persisted in 2022.

2.3 Policy-Driven Development of Small-Molecule Drugs, Outstanding Performance in the Therapeutic Device Sector, and Shifts in Capital Allocation within the Digital Health Space

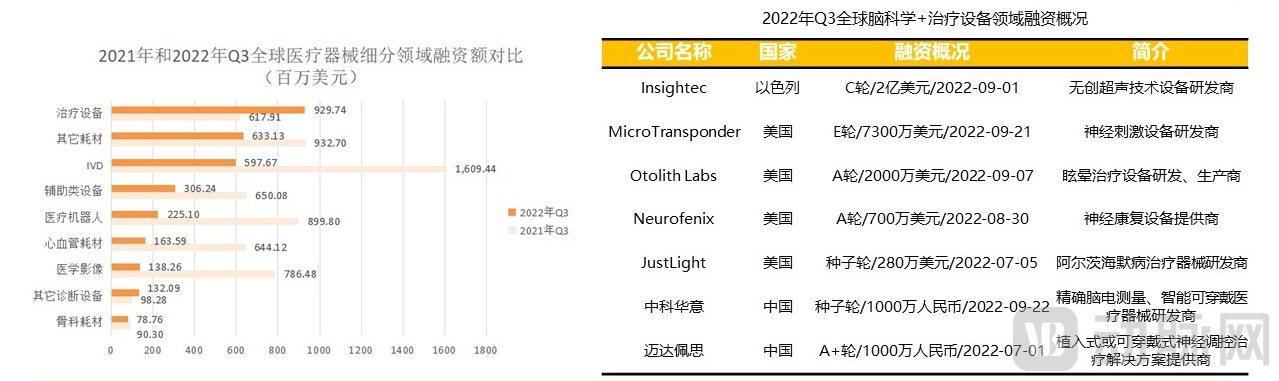

In Q3 2022, global financing activity in the medical device sector generally trended downward. Therapeutic devices, however, stood out with 25 financing deals totaling over $900 million—a 50% quarter-on-quarter increase. Large-ticket financings were frequent, with an average deal size exceeding $37 million.

Specifically, enthusiasm in the field of brain science remained high in Q3 2022. Insightec, a developer of non-invasive ultrasound technology devices, completed a $200 million financing round on September 5, ranking as the second-largest financing deal in the medical device sector for the quarter. Insightec’s Exablate Neuro received FDA approval in 2016 for the treatment of essential tremor. Subsequently, in 2018, regulatory authorities expanded its indications to include the treatment of tremor-dominant Parkinson’s disease.

In Q3 2022, a total of 54 transactions occurred in the global small-molecule drug sector, with cumulative financing amounting to $1.32 billion (approximately RMB 9.4 billion).

With the increasingly integrated development of information technology and biotechnology, the application of new technologies in small-molecule drug research—such as PROTACs and molecular glues—is gradually maturing. On the other hand, the substantial capital requirements inherent in the license-in model have further enhanced the sector’s ability to attract investment in the field of small-molecule drugs.

In January 2022, the Ministry of Industry and Information Technology (MIIT) and eight other departments jointly issued the “14th Five-Year Plan for the Development of the Pharmaceutical Industry,” which listed frontier core technologies and drugs—including targeted protein degradation technology such as PROTAC—as key areas for development. The precise policy support explicitly naming PROTAC underscores the significant strategic importance of pharmaceutical technologies represented by PROTAC.

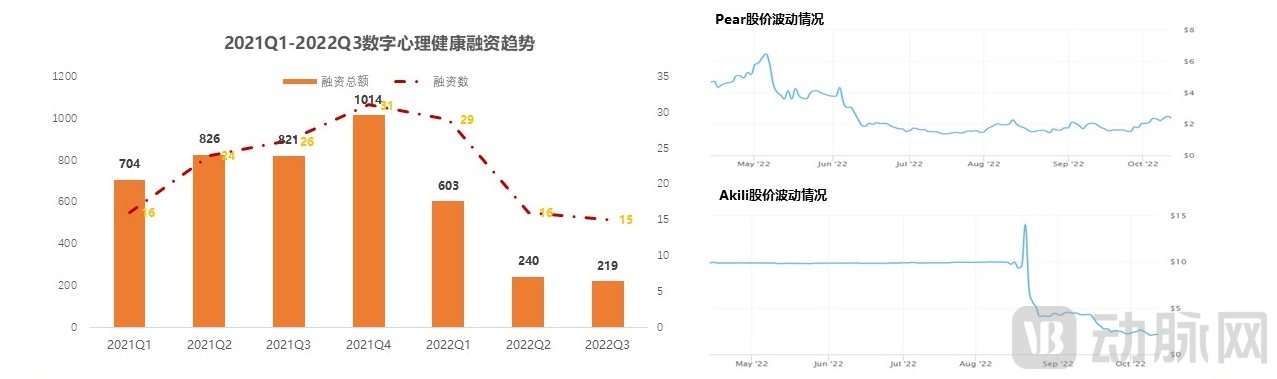

From the perspective of indications, funding amount and deal count in the digital mental health sector still held an advantage in Q3 2022. However, it should be noted that overseas capital experienced a surge in 2021, driven by the dual stimuli of the pandemic and the development of digital healthcare infrastructure. This capital boom itself accelerated the fundraising pace of some startups, enabling them to complete financing rounds ahead of their original schedules. In contrast, startup fundraising slowed down in the third quarter of 2022.

Furthermore, Pear and Akili, a digital therapeutics company specializing in gaming-based interventions, went public in late 2021 and Q3 2022, respectively. However, both have encountered bottlenecks in the development of commercial insurance reimbursement models and faced resistance from some healthcare practitioners, hindering their commercialization efforts. Coupled with financial reports that fail to demonstrate potential for performance growth, their stock prices have declined repeatedly. The setbacks experienced by these two publicly listed companies have, to some extent, dampened primary market expectations for related vertical sectors. Although high hopes are pinned on digital therapeutics, particularly the more advanced mental health segment, this emerging modality, which holds promise for reshaping existing treatment systems, still has a long road ahead.

3.1 Global Investment Turns Cautious, Qiming Venture Partners Becomes the Most Active Investor in Q3

In Q3 2022, Qiming Venture Partners surpassed Sequoia Capital China, which had long dominated the rankings for investment activity, to become the most active institution in global healthcare. It made a total of 11 investments, primarily targeting biopharmaceutical and medical device companies. Notably, unlike other firms that slowed their investment pace, Qiming Venture Partners maintained a quarterly deal volume of more than 10 since the beginning of 2022, investing in both early-stage projects and mature-stage enterprises.

Currently, global investment institutions are increasingly concentrating on early-stage biopharmaceutical companies. However, unlike the cautious investment trend in China’s digital health sector, overseas investors continue to maintain a strong focus on digital health enterprises. Furthermore, after a downturn in the first half of 2022, overseas secondary markets have shown signs of recovery, with investment firms such as Cowen Healthcare Investments and Invus resuming investments in publicly listed companies dedicated to clinical drug development in the third quarter.

3.2 Continued Policy Guidance to “Invest Early and in Small Ventures,” with Domestic Focus on Targeted Radionuclide Therapy

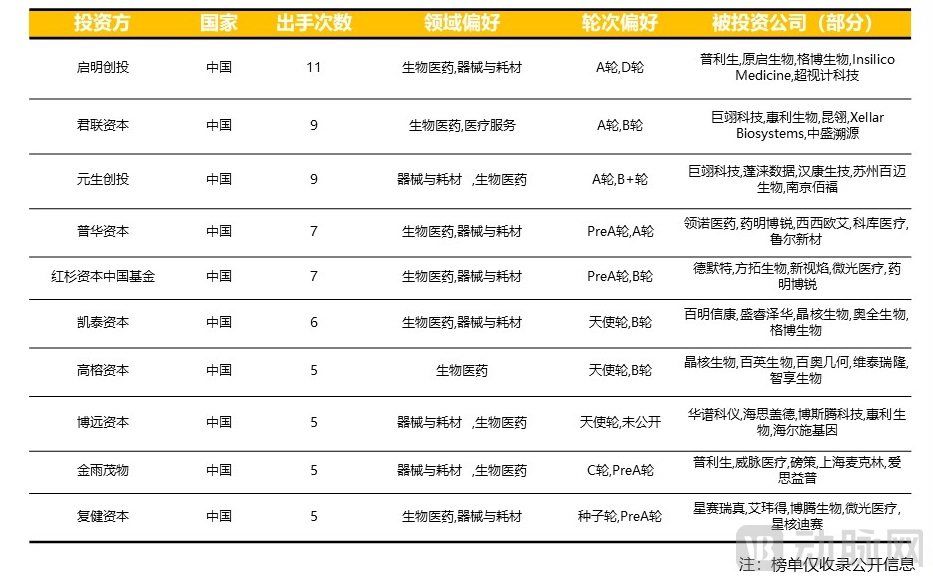

Qiming Venture Partners led the pack with 11 investments this quarter; Legend Capital and YS Ventures followed closely, each recording nine investments and maintaining their focus on early-stage healthcare startups. The remaining active firms on the list showed relatively small differences in investment activity. It is evident that the influence of local government guidance funds in encouraging investments in early-stage and small-scale ventures continues to persist.

Unlike the situation in the first half of 2022, the top 10 domestic investment firms in the third quarter all favored biopharmaceuticals and medical devices, with a decreased emphasis on digital health.

In addition to innovative medical devices, the top 10 investment firms in the third quarter continued to focus on oncology therapies, with targeted radionuclide therapy emerging as a particularly noteworthy subsector. This trend aligns with the current situation in China, where over 90% of medical isotopes used in nuclear medicine rely entirely on imports, as well as with the specialized policies introduced by the state to support the development of radiopharmaceuticals.

4.1 Global: China Leads the World, with Over 200 Financing Deals in a Single Quarter in Both China and the US

In Q3 2022, the five countries with the highest number of global healthcare financing events were China, the United States, the United Kingdom, Canada, and India.

In Q3 2022, China led the world with 276 financing deals and $3.659 billion (approximately RMB 26.1 billion) in funding. The United States and China together accounted for 84% of the total global financing amount and 81% of the total number of financing deals.

Although the number of financing deals in the United States this quarter was lower than that in China, its total funding amount reached $9.809 billion (approximately RMB 69.8 billion), surpassing China. This phenomenon is closely related to the distribution of large-scale financing rounds.

From the perspective of investment hotspots, biopharmaceuticals and medical devices are the sectors garnering global attention this quarter.

4.2 China: Shanghai Remains Dominant, Guangdong’s Financing Heat Surpasses Beijing

The five regions with the most concentrated healthcare and medical investment and financing activities in China in Q3 2022 were, in order, Shanghai, Jiangsu, Guangdong, Beijing, and Zhejiang.

Shanghai ranked first with 54 financing events, raising a total of $716 million (approximately RMB 5.1 billion); Jiangsu followed closely with 51 financing events and became the TOP1 in total financing amount with $736 million (approximately RMB 5.2 billion).

Notably, benefiting from Guangdong’s mature market environment and economic development, as well as policy support, financial backing, and a solid industrial foundation, the province surpassed Beijing by a narrow margin this quarter to rank among the top three hottest domestic regions for financing.

5.1 Top 10 Global Financing Amounts: Verily, a subsidiary of Alphabet (Google’s parent company), secured $1 billion in funding, ranking first in Q3 2022

5.2 Top 10 Financing Amounts in China: 10 Biopharmaceutical Companies Make the List, Sustained High Prosperity in the CXO Sector