Accelerated 'A-to-A' Spin-offs: A New Growth Catalyst for Chinese Healthcare Enterprises?

Endovastec

Developer and Manufacturer of Aortic and Peripheral Vascular Interventional Medical Devices

In recent years, the spin-off of large pharmaceutical companies has become increasingly common. Since the beginning of this year, in response to market changes, several multinational pharmaceutical companies have announced their decisions to spin off subsidiaries.

U.S.-based 3M Company has announced plans to spin off its healthcare business into an independent publicly listed company. British pharmaceutical giant GSK has officially demerged its consumer health division, establishing a new company—Haleon—which is listed on the London Stock Exchange. Well-known brands such as Caltrate, Centrum, Sensodyne, Fenbid, Voltaren, New Contac, and Bactroban have all been placed under Haleon’s portfolio.

Furthermore, multinational giants such as GE, Novartis, and Johnson & Johnson have announced spin-off plans, making accelerated consolidation the prevailing trend in recent times. A growing number of multinational corporations believe that their stock performance improves when their business operations are more focused; additionally, spin-offs can enhance shareholder returns when facing pressure from activist investors.

In the domestic market, spin-offs are becoming increasingly popular. According to Choice data and company announcements, more than 100 A-share listed companies have released plans related to spin-off listings, with biopharmaceuticals being a particularly hot sector. MicroPort, Lepu Medical, Hualan Biological, Salubris, Chengda Pharmaceutical, Livzon, Kelun Pharmaceutical, and Sihuan Pharmaceutical, among others, have successively announced their spin-off plans.

The Spin-Off Saga Intensifies: What Is It That Continues to Draw Companies In?

In December 2019, the China Securities Regulatory Commission (CSRC) issued the “Several Provisions on the Pilot Program for Spin-offs of Subsidiaries of Listed Companies for Domestic Listing,” ushering in a wave of A-share listed companies spinning off their subsidiaries for separate listings on the A-share market.

Prior to this, the absence of policy support meant there was no precedent for “A-share-to-A-share” spin-offs in the capital market. For a listed company to pursue a spin-off, it typically involved either an A-share listed company spinning off a subsidiary to list in Hong Kong or the United States, or a Hong Kong- or U.S.-listed company spinning off a subsidiary to list on the A-share market.

Fosun Pharma, listed in 1998, is a representative case of “A-share to H-share” spin-offs. Fosun Pharma has successively facilitated the Hong Kong listings of its subsidiaries, Sisram Medical and Henlius Biotech.

As for the “H-share to A-share spin-off,” MicroPort Scientific Corporation serves as a prime example. Listed in 2010, MicroPort successfully spun off its subsidiary, Endovastec, for listing on the STAR Market in 2019. Subsequently, MicroPort spun off and listed its other subsidiaries—MicroPort CardioFlow, MicroPort MedBot, and MicroPort NeuroTech—on the Hong Kong Stock Exchange.

“The A-share Spin-off” Policy Implementation Sparks Interest Among Multiple Pharmaceutical Companies. According to incomplete statistics, since the release of the “New Regulations on Spin-off Listings,” in addition to the 17 companies that have already completed spin-off listings, approximately 90 A-share listed companies are planning to spin off their subsidiaries for listing on domestic exchanges, with as many as eight of them belonging to the pharmaceutical and biotechnology sector.

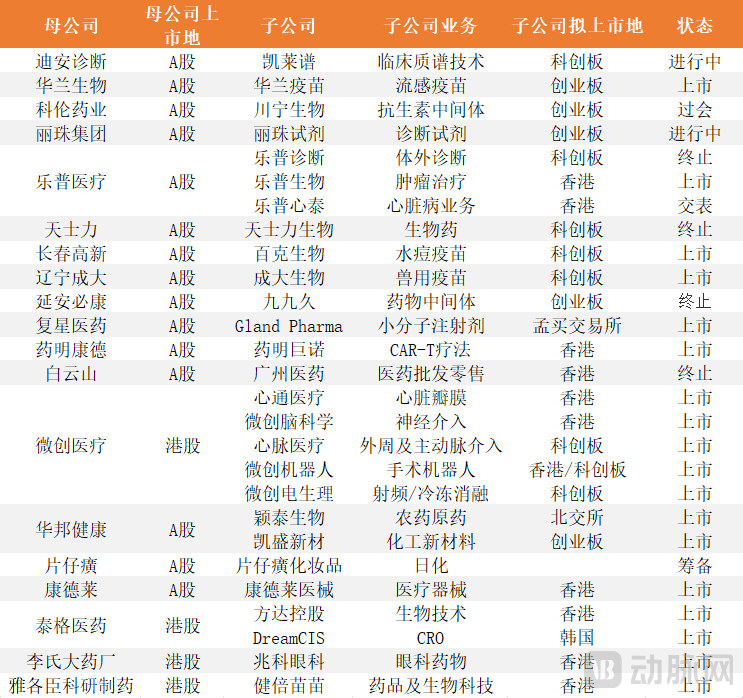

Spin-off Activities of Selected Pharmaceutical Companies in Recent Years, Compiled from Public Information

In recent years, numerous enterprises—including Livzon Group, Dian Diagnostics, Changchun High-Tech, Kelun Pharmaceutical, Tasly, Yan’an Bikang, Hualan Biological Engineering, Liaoning Chengda, Lepu Medical, and Huapont Life Sciences—have expressed intentions to pursue spin-offs.

Notably, as the pandemic evolved, the vaccine business has become a hot sector for spin-off listings.

Amid the pandemic, the state has placed greater emphasis on disease prevention, significantly enhancing public awareness of vaccines. Coupled with the continuous market launch of novel vaccine products in recent years—such as those for EV71, quadrivalent influenza, and HPV—the vaccine industry has experienced rapid growth. Capitalizing on this momentum, Changchun Biologics spun off Bakang Biologics; Hualan Biological Engineering’s subsidiary, Hualan Vaccine, successfully went public; and Liaoning Chengda also listed its subsidiary, Chengda Biotech, as an independent entity.

This phenomenon also reflects, from one perspective, that the higher the attention drawn to the business sectors of spun-off subsidiaries, the more readily they gain market recognition.

In addition to its high-quality core business, it is difficult for the market to accurately assess the value of each business line for listed companies with diversified operations.

Particularly for companies with extensive business scopes, investors may fail to properly understand and accept their diversified operations, thereby underestimating the market value of their stocks. Following a spin-off, the ongoing public disclosure by the subsidiary can have a positive impact on its operational performance.

This is also a major factor driving traditional pharmaceutical companies to spin off subsidiaries for public listing.

For the parent company, a spin-off listing that maintains unchanged control does not affect investment income or gains/losses from changes in fair value in the consolidated financial statements. Although the parent company’s profits may decline in the year of the spin-off listing due to dilution of its shareholding ratio, from the perspectives of corporate governance and long-term development, if the subsidiary’s business gains market recognition, the parent company can also achieve substantial capital premiums.

It is precisely because of these advantages that listed companies have an increasingly strong willingness to spin off their subsidiaries.

In the past, mergers and acquisitions (M&A) were the more prevalent form of corporate asset restructuring in China. Through M&A, listed companies could extend their industry chains and achieve synergies on a larger platform. Spin-offs, by contrast, were relatively less common; however, as there is market demand for them, regulatory authorities will naturally respond accordingly.

From July 2004 to January 2022, the China Securities Regulatory Commission (CSRC) successively issued a series of policies that established unified legal requirements for conditions, implementation procedures, information disclosure, and the due diligence responsibilities of intermediaries regarding corporate spin-offs and listings. These regulations have provided a legal framework supporting enterprises in spinning off their subsidiaries for independent listings both domestically and overseas.

There have been numerous successful spin-off cases in the pharmaceutical industry, such as those within the MicroPort group, Lepu Biopharma, Henlius, Chengda Biology, Bakang Biology, Hualan Vaccine, and Legend Biotech. Spin-offs can be seen across A-shares, Hong Kong stocks, and US stocks.

For companies, spin-off listings can deliver tangible benefits. In the medical sector, many enterprises are also making concerted efforts in this regard, with MicroPort Medical undoubtedly standing out as one of the most successful examples.

Endovastec was established in 2012 as one of the many subsidiaries under MicroPort. By 2018, MicroPort’s core business of coronary intervention had reached a mature stage in China, with a relatively stable market share. In contrast, Endovastec’s focus on aortic and peripheral vascular interventions offered greater growth potential and market imagination.

At that time, Endovastec’s domestic revenue accounted for only about 3% of its total revenue. Although the peripheral vascular intervention market was dominated by foreign companies, it achieved a compound annual growth rate (CAGR) of 15.4%. From this perspective, the sector in which Endovastec operates represents a high-quality track, making it highly necessary to spin off the company for listing and fundraising in China to further expand its market presence.

From the perspective of its parent company, MicroPort, although the R&D cycle in the medical device sector is not as long as that for pharmaceuticals, the average R&D cycle still reaches five years; therefore, the demand for capital in the medical device sector remains equally high.

At that time, multiple business lines of MicroPort were still operating at a loss. Given the continuous updates and iterations in the medical industry, it was essential to maintain high levels of R&D investment. Therefore, leveraging capital operations to bolster cash flow became an imperative task for MicroPort.

Spinning off Endovastec, which operates in a high-potential sector and has already validated its commercialization logic and core capabilities, for an independent listing and external financing will not only accelerate Endovastec’s growth but also provide other subsidiaries with access to lower-cost capital.

From a personnel perspective, MicroPort currently has a management team of approximately 70 individuals, with R&D staff accounting for 26% of Endovastec’s workforce. The departure of core employees would result in substantial losses. To incentivize them, MicroPort holds an equity stake in Endovastec through its controlling interest in the private equity fund Honghao Investment; approximately 9.8% of the shares are held by senior management and technical personnel of both MicroPort and Endovastec.

Driven by its own business development needs and supported by the external environment and policies, Endovastec became one of the first companies to list on the STAR Market.

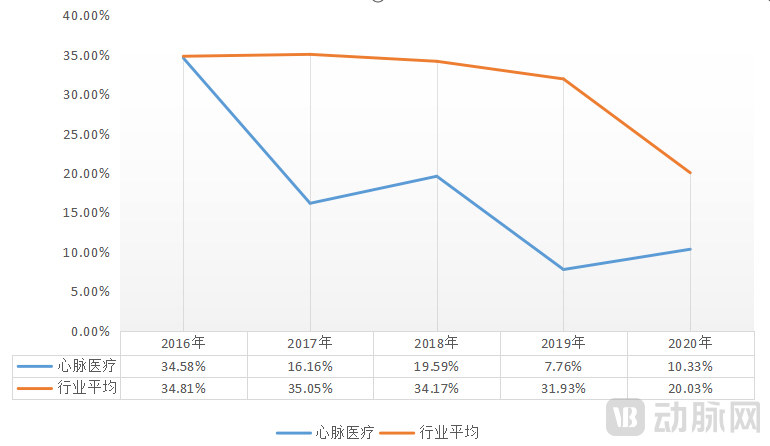

2016–2020 Asset-Liability Ratio of Endovastec; Data sourced from corporate announcements and Choice.

Following its initial public offering (IPO), Endovastec’s asset-liability ratio underwent significant changes. According to the prospectus, the company’s asset-liability ratios in the three years prior to the IPO were 34.81%, 16.16%, and 19.59%, respectively. In the year of the IPO and in 2020, the ratios stood at 7.76% and 10.33%, respectively. The spin-off listing markedly improved the company’s short- and long-term debt-servicing capabilities. In 2019, following the spin-off, Endovastec’s revenue growth rate reached 44.39%, representing a 5-percentage-point increase compared with 2018, the year before the spin-off. Evidently, the spin-off listing enabled Endovastec to achieve strong growth momentum.

Thus, the practical significance of a spin-off lies in breaking down information asymmetry, allowing the market to directly engage with high-potential business lines and propel them to new heights. The parent company can also benefit from this process, thereby reinvesting gains to support other incubating business lines.

In September 2022, Lepu Cardiac Therapy, a subsidiary of Lepu Medical, filed its prospectus with the Hong Kong Stock Exchange for the third time, following the expiration of its previous filings on June 25, 2021, and January 14, 2022. In recent years, companies such as Lepu Medical, BGI Genomics, WuXi AppTec, and MicroPort Medical have led the trend of spin-offs by listed companies, thereby stimulating the willingness of other industry players to pursue similar strategies.

Lepu HeartTech’s three filing submissions have become the latest footnote to the current trend of pharmaceutical companies eagerly pursuing spin-off listings.

It is worth noting that Lepu Biopharma, a subsidiary of Lepu Medical, successfully listed on the Hong Kong Stock Exchange this February after three filing attempts. MGI Tech, which recently rang the listing bell on the STAR Market, had already been spun off from BGI Genomics as early as 2016. Meanwhile, the market also anticipates potential spin-offs of BGI’s other subsidiaries, such as BGI Medical and BGI Health.

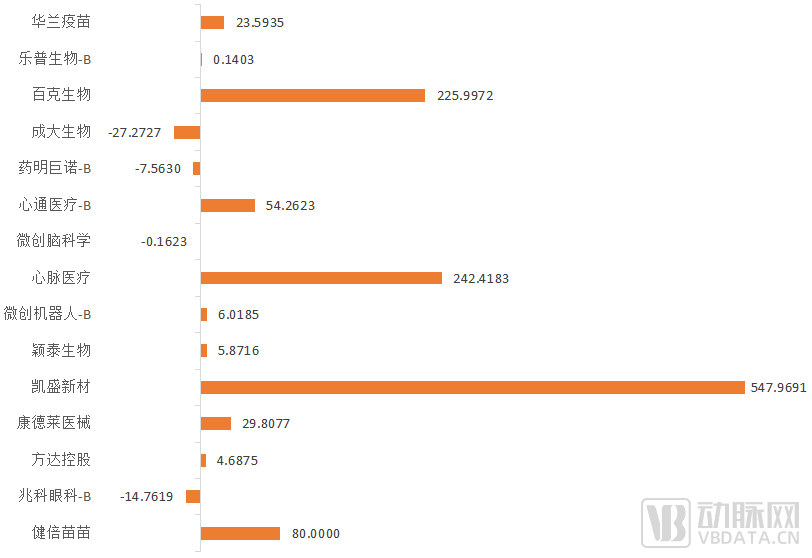

First-Day Price Change (%) of Partially Spun-Off Companies Upon Listing, Data Source: Choice

When it comes to spin-offs, MicroPort Scientific Corporation must be mentioned. With its Hong Kong-listed entity as the core, MicroPort has successively spun off and listed five subsidiaries from 2019 to present: Endovastec, MicroPort CardioFlow Medtech, MicroPort MedBot, MicroPort NeuroTech, and MicroPort EP MedTech.

It is worth noting that MicroPort CardioFlow and MicroPort MedTech, both subsidiaries of MicroPort, completed their financing rounds this year. Together with MicroPort Orthopedics, these three business lines are highly likely to be spun off for separate listings in the future. At that point, MicroPort Medical could boast a portfolio of eight listed companies, a truly impressive feat.

In the medical device sector, although the revenue ceiling for individual products is relatively low, there are numerous niche sub-sectors. During the early stages of corporate development, advancing multiple product lines simultaneously facilitates rapid diversification and leapfrog growth. With the opening of the “Chapter 18A” regulations on the Hong Kong Stock Exchange and the “Fifth Set of Listing Standards” on the STAR Market, a convenient pathway has been created for non-profit innovative pharmaceutical companies to access the capital markets.

Following their initial public offering, as external factors such as capital market conditions and the broader macroeconomic environment evolved, companies began to pursue spin-off listings to secure higher premiums and valuations than those achieved through a consolidated listing.

Corporate Spin-offs and IPOs: While offering the numerous benefits outlined above, such transactions are inherently double-edged; risks associated with spin-offs include the erosion of core business assets, dilution of shareholder equity, and operational pressures on subsidiary companies.

Taking MicroPort as an example, since 2019, the company has spun off and listed one subsidiary per year on average. However, these continuous spin-offs have failed to boost MicroPort’s market capitalization as expected. Instead, its market cap has plummeted from a peak of over RMB 100 billion to just above RMB 24 billion (as of the end of September).

MicroPort’s semi-annual report also corroborates secondary market concerns regarding the company’s operations. In the first half of 2022, MicroPort Medical reported revenue of $405 million, a year-on-year increase of 5.3%, with growth slowing from 20.45% in the previous year; the net loss amounted to $253 million, representing a 120% year-on-year increase.

The primary factor behind this situation lies in the sluggish performance of MicroPort’s core businesses, with its three main segments—cardiovascular interventional devices, orthopedic medical devices, and cardiac rhythm management—experiencing weak growth and declining revenues.

Among the subsidiaries that have been spun off for separate listing, only Endovastec, whose multiple products have entered the maturity stage, achieved profitability according to its 2022 interim report. Its net profit for the first half of the year reached RMB 215 million, a year-on-year increase of 16.42%. Although VitaFlow Medical’s revenue grew by nearly 45% in the first half of the year, it still reported a loss of RMB 120 million. MicroPort MedBot, which went public in 2021, posted a loss of RMB 463 million in the first half of the year, representing a 91% year-on-year increase in losses.

Hualan Vaccine, which was spun off and listed this year, faces the same issue.

Hualan Vaccine’s share price has currently fallen below its IPO price. As of the market close on October 12, it stood at RMB 45.00, representing a decline of nearly 36% from its closing price on the first day of listing (RMB 70.30), with a current market capitalization of approximately RMB 18 billion. Meanwhile, the stock price of its parent company, Hualan Biological Engineering, is also on a downward trajectory, having dropped by 70% from its peak in August 2020. Its total market capitalization is now around RMB 33 billion, reflecting a loss of nearly RMB 100 billion from its peak value.

As the global industry landscape evolves, pharmaceutical companies continue to pursue spin-offs. Although revenue growth is accompanied by various risks, high-quality spun-off assets can still attract a substantial number of investors.

An investor told VCBeat, “For spun-off subsidiaries, investors primarily focus on their growth prospects. Therefore, parent companies must exercise considerable caution when selecting entities for spin-offs. Only if the subsidiary is a high-quality asset with growth potential can the parent company signal to the market that it has been undervalued, thereby achieving the goal of enhancing its own valuation. Conversely, as information is disclosed, assets with limited development potential will not only trigger investor sell-offs but also drag down the parent company’s valuation.”

This view is also corroborated by some pharmaceutical companies that were spun off and listed earlier.

Henlius is an innovative drug subsidiary under Fosun Pharma, listed on the Hong Kong Stock Exchange in September 2019. Three years later, five of its products had successfully reached the market, marking a relatively smooth commercialization journey. In the first half of 2022, Henlius reported total revenue of RMB 1.289 billion, a year-on-year increase of 103.5%; its net loss stood at RMB 252 million, representing a 35.8% narrowing in the loss margin. The company was just one step away from transitioning from a biotech firm to a biopharma enterprise.

Notably, Henlius chose a shrewd timing for its initial public offering (IPO). Prior to the spin-off listing, most of Henlius’s pipeline products were still in clinical stages, requiring substantial capital for further development. Had the company waited for domestic spin-off regulations to mature, it might have missed critical growth opportunities. At that juncture, Fosun Pharma decisively selected the Hong Kong Stock Exchange as the venue for the spin-off IPO, effectively accelerating Henlius’s development.

Not every pharmaceutical company can successfully spin off and list on the stock exchange. As spin-offs become increasingly prevalent, regulatory oversight is being strengthened in tandem.

Tasly Biopharmaceuticals, a subsidiary of Tasly Group, has announced the termination of its listing plans after three failed attempts at an initial public offering (IPO). As more companies pursue spin-off listings, a significant number have also terminated their plans. Key areas of regulatory scrutiny include related parties and related-party transactions, horizontal competition, and the independence of assets, finances, and personnel.

Subsidiaries of listed companies that meet the criteria for spin-offs are typically incubated within the corporate group in the form of product lines, resulting in inherent deficiencies in independence. It is common for such subsidiaries to have intertwined business channels, assets, and personnel with the listed parent company and its related parties.

This imposes higher requirements on the internal controls and standardized corporate governance of listed companies, which must balance integrated operations and management cost control while having the resolve to support and incentivize the independent development of teams driving innovative businesses.

Spin-offs of pharmaceutical companies are highly susceptible to external disruptions; underperformance by the subsidiary or a liquidity crisis within the parent company can both lead to the failure of the spin-off. For instance, Yan’an Bikang decided to terminate its plan to list its subsidiary, Jiujiujiu, on the STAR Market after its actual controller was penalized by the Shaanxi Bureau of the China Securities Regulatory Commission. Subsequently, Jiujiujiu encountered continuous setbacks, with its IPO initially suspended and its equity transfer later halted.

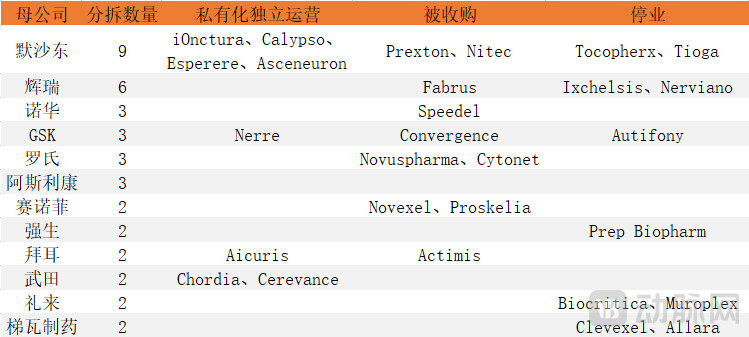

Statistics on Unlisted Companies Following Spin-offs by Multinational Pharmaceutical Firms, Compiled from Public Information

The Path of Spin-offs Is Not Easy, Even for Global Giants. According to incomplete statistics, over the past decade, 12 large pharmaceutical companies worldwide have spun off approximately 39 subsidiaries, among which 10 successfully went public, a number roughly equal to those acquired (10) or discontinued (10).

An investor told VCBeat, “For companies, spin-offs mean higher valuations and debt relief. Companies seek new financing through spin-offs to address issues such as R&D costs, but not all companies are suitable for this strategy. Generally, companies suited for spin-offs fall into several categories. First, those with diversified businesses and certain debt pressures, while possessing product lines that are highly profitable and in a growth phase. Second, incubator-style platform companies that gradually exit and realize gains by listing their subsidiaries. Third, companies where there is a significant gap between the core business and the spun-off business, leading to high management costs. The spin-off process is less likely to encounter problems in areas of regulatory concern, such as independence, core technologies, and horizontal competition.”

The introduction of spin-off policies has allowed many enterprises to recognize the associated benefits. Spin-off listings can enhance a company’s capital operation capabilities, create room for expanding its equity base, foster group-level development, and improve competitiveness. For listed companies, the objectives of pursuing a spin-off listing are twofold: on one hand, to clarify the core business focus, enabling subsidiaries to concentrate on their respective operations and achieve focused growth; on the other hand, to maximize valuation.

From a long-term development perspective, companies should not blindly follow trends, as not all businesses are suitable for spin-off listings. Listed companies should thoroughly consider multiple factors, such as whether the spin-off listing helps highlight their core business and promotes group development, and whether there is horizontal competition between the parent and subsidiary companies. They should remain vigilant against the risks of "business hollowing out" of the parent company and horizontal competition.