Structural Heart Intervention Leader Scientech Medical Files for Hong Kong IPO Amid the Fourth Revolution in Cardiology

ScienTech Medical

Structural Heart Disease Interventional Medical Device R&D and Manufacturer

In 2018, during China Structural Heart Disease Week, Academician Ge Junbo, an expert in interventional cardiology, pointed out that new technologies for structural heart disease have initiated and represent the fourth cardiac revolution in interventional cardiology.

Industry leaders’ remarks often hold profound foresight; since 2018, structural heart disease has become the central theme of innovation and upgrading in China’s cardiovascular medical device sector. The domestic market for structural heart disease has also witnessed rapid growth.

Since 2020, there has been a continuous emergence of new devices and technologies for structural heart disease in China, leading to a significant increase in the cumulative number of procedures. The number of transcatheter aortic valve replacement (TAVR) cases in China has surged at an annual growth rate of nearly 50%, surpassing the development pace of all previous interventional techniques. Meanwhile, procedures such as patent foramen ovale (PFO) closure and left atrial appendage closure (LAAC) have also demonstrated rapid growth in case volumes. According to Frost & Sullivan data, the market size for structural heart disease in China expanded from RMB 400 million in 2017 to RMB 2 billion in 2021.

New interventional technologies for structural heart disease have ignited the domestic cardiac intervention industry, with multiple companies entering this sector. Among the numerous enterprises in China, ScienTech Medical, a subsidiary of Lepu Medical, is a pioneer in the field of interventional medical devices for structural heart disease and a leading domestic supplier of occlusion devices for congenital heart disease. For over two decades, it has remained dedicated to the research, development, and manufacturing of interventional medical devices for structural heart disease.

ScienTech Medical is currently applying for a listing on the Main Board of the Hong Kong Stock Exchange. As a new wave in interventional cardiology, what are the future growth drivers for the structural heart disease market? As a leader emerging from the first three revolutions in interventional cardiology, how will Lepu’s spun-off subsidiary position itself in the structural heart disease sector? VCBeat (WeChat ID: vcbeat) has compiled an analysis.

From 2009 to 2019, the U.S. stock market saw the emergence of 14 pharmaceutical stocks that achieved tenfold growth and reached market capitalizations exceeding $10 billion. Among these, five were innovative medical device companies: Intuitive Surgical in the field of surgical robotics; Align Technology in clear aligner orthodontics; Dexcom in continuous glucose monitoring; and Edwards Lifesciences and Abiomed in the field of structural heart disease.

Notably, the field of interventional therapy for structural heart disease has given rise to two companies that achieved tenfold growth over a decade. In 2021, the global market size for structural heart disease reached $9.3 billion. Why has interventional therapy for structural heart disease spawned such remarkable wealth-creation stories?

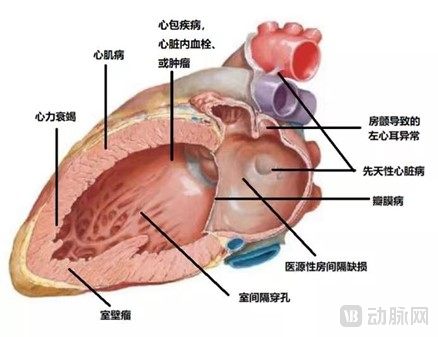

If a person lives to the age of 80, their heart will need to beat more than 2.5 billion times. Under such heavy workload, various components of the heart may develop problems. Heart-related issues can be broadly categorized into three major types: coronary artery disease, arrhythmias, and structural heart diseases. Structural heart diseases mainly include congenital heart defects, valvular heart disease, cardiomyopathy, and other conditions (such as atrial fibrillation) that lead to complications, increasing the risk of cardioembolic stroke and myocardial infarction.

Types of Structural Heart Disease

In the 1950s, invasive cardiac catheterization already enabled physicians to diagnose congenital heart disease and valvular heart disease, although treatment at that time still required open-heart surgery. With the application of new minimally invasive interventional techniques in the field of structural heart disease, the global market for structural heart disease treatments has experienced rapid growth.

In China, the maturity levels of various subfields within interventional therapy for structural heart disease vary. Interventional treatment for congenital heart disease is the most mature; interventional valve therapy is experiencing rapid development; atrial fibrillation prevention is in its early stages of development; and adjunctive therapy for heart failure is in the early exploratory phase.

First, let us examine the relatively mature market for interventional occluders, which includes congenital heart disease (CHD) occluders and left atrial appendage (LAA) occluders.

Congenital heart disease (CHD) occluders are used to treat congenital heart defects. Approximately half of all CHD cases consist of ventricular septal defects (VSD) and atrial septal defects (ASD). The global market size for congenital heart disease occluder products includes only three major types: atrial septal defect occluders, ventricular septal defect occluders, and patent ductus arteriosus occluders.

The technology of congenital occluders has been developing for over 30 years, and the surgical procedures are relatively mature. The total volume of interventional treatments for congenital heart disease in China has risen to rank first globally, with approximately 75,000 interventional surgeries for congenital heart disease performed in 2021.

In addition to congenital heart defect occluders, the category of occluders also includes devices for preventing cardioembolic stroke. Products in this segment primarily consist of patent foramen ovale (PFO) occluders and left atrial appendage (LAA) occluders. Implantation of these cardioembolic stroke prevention devices can help prevent cardioembolic strokes. Currently, stroke is the leading cause of death in China, with over 3 million stroke patients hospitalized in the country in 2021. The market for cardioembolic stroke prevention occluders in China is still in its emerging stage.

In the structural heart disease market, the rapidly emerging transcatheter valve intervention market over the past decade cannot be overlooked.

In 2002, Professor Alain Cribier, a French interventional cardiologist, performed the world’s first transcatheter aortic valve replacement (TAVR) procedure, employing a minimally invasive interventional approach to treat aortic valve disease. Previously, valve surgery could only be performed via open-heart surgery, which was contraindicated for many elderly patients and those at high surgical risk.

New TAVR technologies have ushered in the golden two decades of interventional valve therapy. According to data from Frost & Sullivan, global sales revenue for interventional valve devices reached $7.1 billion in 2021.

China's valve market is in the early stages of rapid development, with the volume of TAVR procedures growing at a rate of 50%. However, the penetration rate of interventional devices for valvular heart disease remains significantly low. Due to the insufficient number of qualified hospitals with experienced physicians, only 0.8% of eligible patients underwent transcatheter aortic valve replacement (TAVR) in 2021. Compared to the global rate of 4.3%, the TAVR market in China is clearly under-penetrated.

Overall, against the backdrop of an aging population, aortic stenosis, aortic regurgitation, and mitral/tricuspid regurgitation have become the predominant types of structural heart disease posing serious threats to public health. The substantial surge in patient numbers has driven significant clinical demand for diagnosis and treatment. Propelled by technological advancements and growing clinical needs, China’s structural heart disease market is experiencing rapid growth.

Interventional valve technologies in the field of structural heart disease have created a global market worth nearly $10 billion, growing from scratch. What are the future highlights for the structural heart disease market? Four trends are drawing global attention.

For congenital heart disease (CHD) occluders, bioresorbable occluders represent a key direction in research and development. Currently, occluders available on the market for interventional treatment of CHD are primarily made from non-degradable nickel-titanium alloy, which remains permanently in the human body—an outcome that is less than ideal for pediatric patients. The development of bioresorbable occluders has become a trend for next-generation CHD occlusion devices, although this endeavor faces significant challenges in materials technology.

In the field of left atrial appendage (LAA) occlusion, the clinical application of newly developed LAA occlusion devices has made the procedure safer, more effective, and more convenient, leading to the widespread adoption of simplified LAA occlusion surgery.

For transcatheter heart valves, enhancing anti-calcification properties and durability to facilitate the expansion of TAVR to younger patients represents a major trend, while improving deployment precision to increase implantation success rates constitutes another key direction for clinicians.

In addition to aortic valve innovations, advancements in mitral and tricuspid valves are also highly anticipated. Clinically, the patient population with mitral and tricuspid valve diseases is larger than that with aortic valve diseases; however, the development of interventional therapies for mitral and tricuspid valves has lagged behind. Mitral and tricuspid valve interventions are also considered key components of the future structural heart disease market.

In addition to interventional occluders and transcatheter valve interventions, attention is increasingly focusing on the heart failure sector, while the field of structural heart disease is experiencing a surge in innovation.

Structural heart disease, a sector brimming with transformative potential, has drawn the attention of multiple industry giants. Whoever dominates this track will hold the reins of the cardiac disease market for the next decade.

Which companies currently dominate the structural heart disease sector?

In the market for interventional occluders for congenital heart disease (CHD), the domestic CHD interventional market size reached RMB 426 million, according to data from Frost & Sullivan. The domestic market has basically achieved localization, with Chinese-made products accounting for over 91.5% of the market share. Among domestic companies, ScienTech Medical holds the largest market share at 38%. In 2018, ScienTech Medical completed the world’s first fully bioresorbable interventional treatment for ventricular septal defect (VSD), marking a new breakthrough in the field of bioresorbable occluders globally.

In the market for cardiac stroke occluders, patent foramen ovale (PFO) closure therapy remains in an emerging stage. Four domestic companies are involved: AGA Medical and Beijing Huayi Shengjie have received approval to market their alloy-based PFO occluders; ScienTech Medical’s bioresorbable PFO occluder is in the pre-registration phase; and Shanghai Jinkui Medical’s bioresorbable-material PFO occluder is in the clinical trial phase.

The global left atrial appendage (LAA) occluder market reached $900 million in 2021. The penetration rate of LAA occluders in China remains at a very low level; according to Frost & Sullivan, the penetration rate is only 5.9%, compared to 44.9% in the United States and 14.6% in Europe. Consequently, the current market size for LAA occluders in China is relatively small, amounting to RMB 500 million in 2021. Several companies have launched LAA occluder products, including ScienTech Medical, Boston Scientific, Abbott, and Lifetech Scientific. Boston Scientific is the dominant player in the LAA occluder market, with its LAA occluder products generating sales revenue of approximately $830 million (equivalent to RMB 5.5 billion) in fiscal year 2021. The domestic market in China has not yet been fully exploited. Currently, ScienTech Medical’s bioresorbable LAA occluder has completed type testing and animal studies and is about to enter the clinical trial phase. Leveraging the dual advantages of import substitution and technological innovation, ScienTech Medical is poised to overtake competitors through its bioresorbable LAA occluder.

In the interventional valve market, according to Frost & Sullivan data, the market size of interventional devices for valvular heart disease in China reached RMB 1 billion in 2021 and is projected to increase to RMB 7.9 billion by 2025, representing a compound annual growth rate (CAGR) of 69.8%. Currently, nine TAVR products have been commercialized in the domestic market. In 2021, the number of TAVR procedures performed in China (including transfemoral and transapical approaches, but excluding clinical trials) exceeded 6,500 cases, compared with only 3,500 cases in 2020.

In the mitral valve market, only Abbott’s edge-to-edge repair product, MitraClip, has been approved for marketing in China. MitraClip has also received FDA and CE certifications. More than 14 companies are currently positioning themselves in the Chinese mitral valve market. In 2021, approximately 350 transcatheter edge-to-edge repair (TEER) procedures for the mitral valve were performed in China.

The structural heart disease market is complex and diverse. In the interventional congenital heart disease market, ScienTech Medical has emerged as a domestic “hidden champion,” while the entire valve market remains in a fragmented, highly competitive phase akin to the Warring States period. The cardioembolic stroke market is in its early stages of development, with a clear trend toward domestic substitution.

The structural heart disease market in China is characterized by complexity. Despite a large patient population, the field faces challenges including the relatively high technical difficulty and prolonged learning curve associated with interventional procedures, a lack of market education, and a shortage of experienced operators. Furthermore, while numerous enterprises are engaged in product development, there is significant homogenization among their offerings.

Breaking through in the structural heart disease market places high demands on a company’s long-term ability to understand clinical needs, commercialize products, and educate the market.

Among the emerging domestic companies engaged in R&D of interventional devices for structural heart disease, ScienTech Medical has been deeply committed to this field for over two decades.

ScienTech Medical is a hidden champion in the field of interventional therapy for congenital heart disease. It developed China’s first ventricular septal defect occluder, won the Second Prize of the National Science and Technology Progress Award, and has maintained the largest market share in the field of interventional occlusion for congenital heart disease for many consecutive years.

ScienTech Medical has not only been a pioneer in the field of interventional therapy for congenital heart disease but also continues to drive iterative innovation. Leveraging the leading bioresorbable technology of its parent company, Lepu Medical, ScienTech Medical has applied this technology to the field of structural heart disease, launching MemoSorb®, the world’s first commercially available fully bioresorbable occluder, and has already laid out a pipeline of five original bioresorbable products.

Compared with traditional metal occluders, bioresorbable occluders are designed to gradually degrade into carbon dioxide and water. As bioresorbable occluders do not remain permanently in the human body, they provide patients with additional options for future treatments.

Biodegradable technology will drive market expansion in the field of interventional occlusion for congenital heart disease (CHD). CHD occluder products have entered a phase of commercial harvest, with the market size expanding from approximately RMB 1.5 billion to nearly RMB 5 billion. Due to ongoing product upgrades and iterations, ScienTech Medical’s MemoSorb® fully biodegradable occluder will secure a first-mover advantage and dominate the market for a certain period.

In the valve sector, ScienTech Medical was not the first to enter the market. How has ScienTech established its competitive advantage in this fiercely competitive landscape?

ScienTech Medical’s strategy is to establish a competitive advantage in the field of valvular heart disease through innovative and distinctive products, thereby achieving overtaking on a curve in the valve sector.

In terms of pipeline layout, ScienTech Medical has established a presence in the four major valve segments: aortic, mitral, tricuspid, and pulmonary valves. Among these, three key products—TAVR, mitral chordae tendineae repair, and clip-based repair—have entered clinical trials.

In terms of product strategy, ScienTech Medical has adopted a differentiated design approach. The original design of ScienTech Medical’s ScienCrown TAVR aligns with the trend of younger patients on the patient side, while its “short valve + fully retrievable system” effectively reduces procedural risks for physicians on the clinician side.

In addition to innovation, ScienTech Medical’s advantages in the valve field also include the patience to cultivate the market.

In recent years, China’s medical device sector has often exhibited a trend where participants flock to the market and supply surges ahead of an explosion in demand. However, demand in the healthcare industry requires a certain period of market cultivation. In the field of valve interventions, which involves high procedural complexity, the requirements for operators are even more stringent. Market cultivation demands both capital and time, and the market needs to reach a certain scale before it can develop organically. The domestic valve intervention industry is expected to experience its take-off point in 2024 and 2025. ScienTech Medical has established a rich pipeline in the field of valve interventions, strategically aiming to leverage innovative products to capitalize on the impending market surge.

In the design of transcatheter mitral valve systems, interventions are broadly categorized into two main approaches: repair and replacement. Mitral valve repair products encompass various procedural strategies, including edge-to-edge repair, annuloplasty, chordae tendineae repair, and annular remodeling. ScienTech Medical has strategically positioned its mitral valve portfolio across both repair and replacement pathways. Its repair product line covers multiple technological approaches, such as edge-to-edge repair, chordae tendineae repair, annular repair, and annular remodeling, thereby providing tailored solutions for patients with diverse mitral valve pathologies.

In terms of market education capabilities, ScienTech Medical has cultivated the structural heart disease sector for 20 years, accumulating extensive and professional commercialization experience and resources. Furthermore, ScienTech is backed by Lepu Medical, which boasts over two decades of practical experience in the cardiovascular field and has repeatedly achieved remarkable turnarounds to capture niche market segments.

In terms of commercialization, ScienTech Medical has also demonstrated strong profitability, making it one of the few profitable and high-growth companies in the structural heart disease sector of the Hong Kong capital market. In the first half of 2022, ScienTech Medical’s revenue reached RMB 125 million, compared with RMB 110 million in the same period of the previous year; its operating profit was RMB 34 million, down from RMB 46 million in the same period last year. The company’s gross profit margins for 2018–2020 were 87.9%, 88.3%, and 89.8%, respectively; its net profits were RMB 38.61 million, RMB 51.91 million, and RMB 68.77 million, respectively, with net profit margins of 39.0%, 44.6%, and 46.4%, respectively.

From a long-term development perspective, ScienTech Medical leverages its bioresorbable technology platform to consolidate its advantages in the field of interventional occluders. Drawing on its specialized market education and training expertise cultivated through deep engagement in the structural heart disease market, the company is actively participating in the development of China’s interventional valve market. We look forward to ScienTech Medical making greater contributions to the domestic structural heart disease market in the future.

Over the past decade, a wave of transformation in the field of structural heart disease has continuously swept through clinical practice in China. Driven by this powerful momentum, the domestic industrial ecosystem has been reshaped, and seeds of innovation have taken root. The gap between China’s innovative medical devices for structural heart disease and international standards has gradually narrowed. Companies such as ScienTech Medical have repeatedly led global innovation. Whether they can grow into towering trees in this underexplored frontier of structural heart disease remains to be seen.

Reference Article:

ScienTech Medical Prospectus

Domestic Innovative Left Atrial Appendage Occluders Are Rising Rapidly: Can They Overtake Competitors on This Multi-Billion-Yuan Track? — China Medical Technology Network

"2021 Structural Heart Disease Annual Report Released: Interventional Therapies for Structural Heart Disease Flourish, with Significant Room for Improvement in Multiple Technologies" — Outpatient Clinic

Academician Ge Junbo: Definition, Scope, Current Status, and Future of Structural Heart Disease – Heart Focus