Comprehensive Landscape Analysis of Over 25 Organoid Companies: Technology, Commercialization, and Market Outlook

Daxiang

Developer and Producer of Human Organ Chips and Organoid Chips

Over the past two months, the organoid industry has witnessed several landmark, even milestone, events, most notably two major developments: In August, the FDA approved the first new drug to enter clinical trials with preclinical data derived from “organ-on-a-chip” studies; and on September 29, the U.S. Senate passed the FDA Modernization Act, which aims to reduce reliance on animal testing in preclinical studies by adopting more modern scientific approaches, such as organ-on-a-chip technology.

The organ-on-a-chip sector has rapidly ignited, heating up the industry.TheActivity in the field has also increased significantly.

Over the past two months, VCBeat has curated a special report on organoids, interviewed multiple domestic organoid startups, analyzed several organoid companies in Europe and the United States, and hosted an online salon to discuss “industry standardization.”

Overall, organoids remain a nascent sector in China, with technology and commercial operations still lagging behind overseas counterparts, and industrial clusters yet to fully take shape. However, the past two years have indeed seen the emergence of a cohort of innovative companies actively driving the industrialization of organoid technology.

During our interviews with these companies, we found that not only are the technical potential of organoids and cutting-edge research findings worthy of attention, but the latest industry trends and analyses also hold significant value, as activity in the domestic and international industrial sectors continues to increase.

VBInsight will continue to monitor the latest developments in the organoid industry. Meanwhile, based on frontline interviews and desk research, we have analyzed 12 overseas organoid companies and 14 domestic ones, comparing their talent and technology sources, development stages, and business models. Through this comprehensive industry overview, we aim to present readers with an authentic picture of the market landscape in this sector.

What is the industry landscape like?

Throughout, the capital markets have paid attention to the organoid sector, but enthusiasm has been lukewarm. Some investors candidly admit that due to the difficulty in clearly identifying scalable application scenarios, they remain in a “wait-and-see” phase regarding organoid projects.

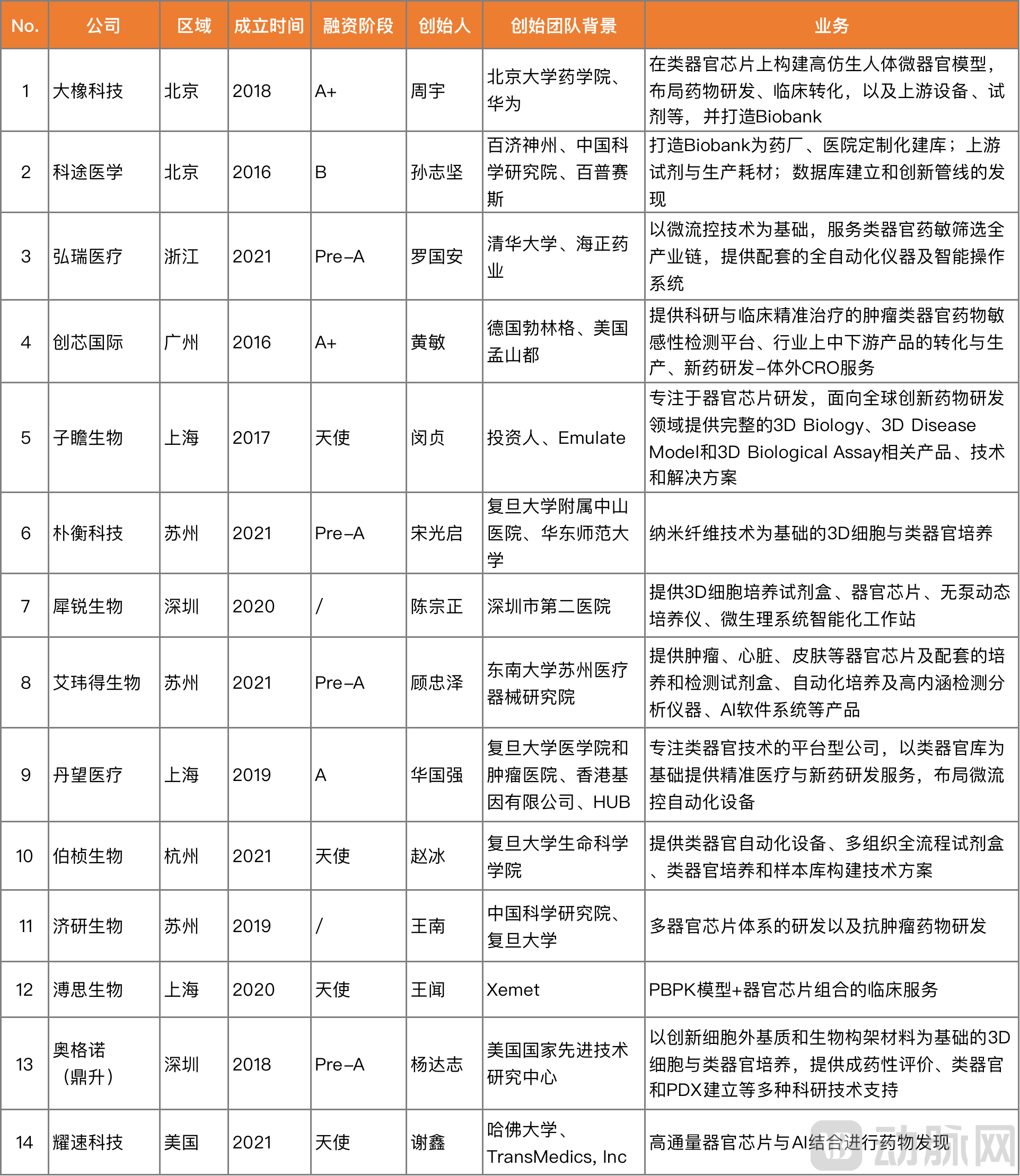

Domestic organoid companies were primarily established between 2018 and 2021, indicating that the industry is still in its nascent stage.

Currently, the majority of organoid companies are in the angel to Pre-A financing rounds (based on publicly disclosed funding only). The only company to have reached Series B is Ketu Medicine, which announced the completion of its latest round of tens of millions of yuan in financing this July. Additionally, Daxiang Biotech and Chuangxin International, two companies with more advanced commercialization efforts, have both secured financing up to the A+ round.

Information sourced from interviews and public materials; listed in no particular order.

However,In the past two months,Spurred by the two aforementioned landmark industry events, investment activity in this sector has significantly increased.. According to reports, a domestic organ-on-a-chip company had already completed its fundraising round, yet during the National Day holiday in October, many investment institutions eagerly approached it again.

Since the Hans Clevers laboratory first cultured intestinal organoids in 2009, the development of organoids has been most prominent in countries such as the United States, the Netherlands, the United Kingdom, and Germany.The majority of companies are spin-offs from university research institutes, with clearly defined technology sources.

Prominent organoid companies abroad include TissUse from the Technical University of Berlin, Hesperos from Cornell University, and Mimetas from Leiden University. Emulate, originating from Harvard University’s renowned Wyss Institute for Biologically Inspired Engineering, is another notable player.

Furthermore, HUB, the organoid technology incubator co-founded by Hans Clevers, as the world’s earliest R&D center for organoids, has also facilitated the emergence of a number of organoid companies through technology licensing.

Although the research foundation for organoids in China is not as deep as that in Europe and the United States, it is accumulating rapidly.The number of organoid-related publications from China ranked second globally in 2020.

From a regional perspective, domestic organoid companies are primarily concentrated in the Guangzhou-Shenzhen area, the Yangtze River Delta, and Beijing.Part of the reason is that, as an emerging technology, organoids require close collaboration with universities, hospitals, and research institutions in the translation of scientific achievements.In recent years, Fudan University and Southeast University in the Yangtze River Delta region, as well as Sun Yat-sen University and the Shenzhen Tsinghua University Research Institute in Guangdong Province, have all been intensifying their efforts in the field of organoids.

For example, the Southeast University Suzhou Medical Device Research Institute, jointly established by Southeast University, the Suzhou National New & Hi-Tech Industrial Development Zone, and the Jiangsu Industrial Technology Research Institute, has achieved breakthroughs in tumor organoids, cardiac organoids, organ-on-a-chip technology, and upstream materials and equipment automation since its inception. It has also incubated the organ-on-a-chip company Aiweide Biotech. This July, Aiweide Biotech announced the completion of its Pre-A financing round, with a total transaction value approaching RMB 100 million.

Fudan University has also made prominent strides in the field of organoids. Its “Organoid Center,” housed within the State Key Laboratory of Genetic Engineering, is a national key laboratory-level technical platform dedicated to the development of cutting-edge organoid technologies and their applications in regenerative medicine. The center established the world’s first human-derived organoid model for SARS-CoV-2 infection. Publicly available information shows thatAmong the organoid startups that have emerged, many teams have a background at Fudan University.

Similar to many sectors in the biopharmaceutical industry, numerous organoid companies in China are founded by individuals with overseas backgrounds.Research and industrialization of organoids were first initiated in Europe and the United States, with some companies deriving their technologies from overseas collaborative licensing agreements.

Hua Guoqiang, founder of Danwang Medical, has been engaged in organoid research at the Memorial Sloan Kettering Cancer Center in the United States since 2009. He has witnessed the field’s progression from academic proof-of-concept to clinical validation and industrial application, and established connections with Hans Clevers, a pioneer in organoid technology. Recognizing the immense potential of organoid technology, Hua returned to China in 2015, joining Fudan University Shanghai Cancer Center and the School of Medicine at Fudan University. There, he collaborated with Hans Clevers to conduct clinical trials on colorectal cancer organoids, before founding Danwang Medical in 2019.

Entrepreneurs with backgrounds in Chinese universities and research institutes have also recognized the potential of the organoid field in the past two years, joining the wave of startup ventures. In 2021, Professor Luo Guoan, one of the pioneers of microfluidics technology in China, chose to embark on an entrepreneurial journey in his seventies by founding Hongrui Medical, translating decades of prior basic research achievements into the organoid sector.

In addition to founders with backgrounds in universities and research institutes, those from pharmaceutical companies are also a significant force in organoid entrepreneurship., while the former aims to translate cutting-edge achievements into practical applications, the latter is driven by the identified needs in drug development. Typical examples of such industry founders include Sun Zhijian, founder of Ketu Medicine, who previously worked at BeiGene and Novartis Pharmaceuticals, and Huang Min, Chairman of Chuangxin International, who formerly worked at Boehringer Ingelheim in Germany.

VBInsight also observed that,Some domestic organoid companies take commercialization and operational management considerations into account in advance when building their teams,For instance, Zhou Yu, Founder and CEO of Daxiang, previously worked at Huawei for over ten years and has extensive experience in operations management.

Commercialization Exploration: China Is Still in Its Early Stages, While Foreign Companies Have Entered Deep Waters

From a business perspective, domestic organoid companies have gradually expanded from the upstream segment to the midstream and downstream segments.Upstream efforts emphasize material innovation, iterative advancements in culture technologies, and domestic substitution. Midstream and downstream sectors can develop interactive microphysiological systems, such as Organ-on-a-Chip. However, both organoid models and organ chips require further improvements in throughput, as well as solutions to issues of accuracy and reproducibility.

In terms of business model,Phase I,Organoid companies typically choose to develop organoid models and chips, positioning themselves in the field of drug sensitivity screening.Phase II,Leverage data accumulated from drug sensitivity screening to gradually collaborate with pharmaceutical companies, positioning for drug indication expansion or venturing into new drug development.Finally,Some companies are proactively positioning themselves in the field of regenerative medicine.

Some companies are also leveraging other cutting-edge technologies to unlock the application potential of organoids. For instance, Pusen Biotechnology employs pharmacokinetic simulation software to iteratively advance its organ-on-a-chip technology, recapitulating the complex structures and authentic microenvironments of human organs while partially simulating the physiological functions specific to the source organs or tissues. Yaosu Technology integrates high-throughput organ-on-a-chip platforms with computer vision techniques based on cell morphology, utilizing large-scale automated organ-on-a-chip systems to generate three-dimensional cellular bioimages and combining them with AI for drug screening.

Furthermore, during the interview with VCBeat New Medicine, it was learned that some companies are establishing biobanks, aiming to support drug development or clinical needs through high-quality, large-capacity sample repositories. In this regard, the interviewed founders stated that this represents a significant advantage for China in the field of organoids:Organoids represent clinical applications and clinically relevant technologies and assays, areas in which China holds advantages in policy, resources, and industry.“China possesses an advantage in sample resources, enabling the establishment of truly dominant international standards during the industrialization process. Currently, there is no such large sample size abroad to support the creation of a comprehensive organoid biobank.”

In fact, if you study the overseas market for organoids, you will find thatAlthough Western countries started early, their industrialization is also in an exploratory phase and has gradually entered a more complex stage.

According to research, the North American organoid market reached $290 million in 2019 and is projected to reach $1.4 billion by 2027, growing at a compound annual growth rate (CAGR) of 21.7%, indicating substantial market potential.However, for over a decade, there have been no publicly listed companies in the overseas organoid sector; the most advanced is Emulate, an organ-on-a-chip company that has secured Series E funding.Most other well-known organoid companies have halted their public fundraising at Series A or B rounds, while some, such as TARA Biosystems and OcellO, have been acquired.

Emulate Inc., officially established in 2014, has raised nearly $225 million in total funding following its Series E round last September, making it the most heavily funded company in this niche sector.

Emulate’s fundraising pace reflects market recognition of its commercialization capabilities. By offering more integrated solutions, abundant collaborative resources, and strong commercialization prowess, Emulate has established close partnerships with a diverse range of customers. In addition to academic research institutions, 10 of the top 25 global biopharmaceutical companies—including Johnson & Johnson, Roche, and Takeda—have adopted Emulate’s products. The company has also secured various government contracts.

During interviews conducted by VCBeat in the healthcare industry,Experts have pointed out that Emulate’s business model is difficult to replicate,Emulate’s clientele includes not only pharmaceutical companies and research institutions but also substantial government contracts, with its core business revolving around instruments and reagents, as well as services and solutions.

However,As an industry bellwether, Emulate signifies that leading companies in the sector are entering the deep waters of commercialization.

Emulate appointed Jim Corbett as its new CEO in 2020. With over 25 years of commercialization experience in the healthcare and life sciences sectors, Mr. Corbett previously served as an executive at PerkinElmer, where he managed a workforce of more than 4,000 employees, accumulating extensive operational expertise. Some analysts believe that Emulate is inclined to evolve into a precision instrumentation company rather than following the traditional biotech pathway.

Mimetas is also venturing into the deeper waters of commercialization. To enhance its market competitiveness, this company, which has specialized in organ-on-a-chip technology for over a decade, appointed a CFO with consulting and business development expertise to oversee BD in 2019. Additionally, it named a scientific advisor with extensive pharmaceutical industry experience last year to accelerate collaborations with pharmaceutical companies.

In the field of organoids, the pioneering role of policy is particularly evident.

The development of the organoid industry in Europe and the United States is not only driven by substantial scientific research accumulation but also closely linked to policy incentives.

In 2012, the NIH, FDA, and the Defense Advanced Research Projects Agency (DARPA) jointly launched the “Organs-on-chips” Challenge with a $75 million investment, aiming to develop a chip-based system that simulates human organs.This project spurred the emergence of a generation of U.S. organ-on-a-chip companies., including Emulate, which has secured the largest funding to date, and Hesperos, which collaborates with Sanofi on clinical trials for rare diseases.

The European Union has also recognized the importance of organoid technology. In 2010, the Technical University of Berlin received support from the GoBio Fund. The EU’s Seventh Framework Programme included projects on “human-on-a-chip,” and initiatives such as the EU-ToxRisk project, launched in 2016, have also provided support for organ-on-a-chip research. This financial backing has significantly advanced global research in the field of organ-on-a-chip technology, while also attracting more projects and institutions to this emerging area.

The early signs of domestic policy emerged in 2016, when China approved the market launch of its first new cosmetic product that had not undergone animal testing, thereby ushering in the era of using “artificial skin” for research on novel cosmetics.

In the past two years, the Ministry of Science and Technology, the National Health Commission, and the Center for Drug Evaluation (CDE) have continuously introduced policies to deregulate the widespread application of organoids. Meanwhile, regulations on human genetic resources have been progressively tightened, creating a broader development environment for China’s organoid industry.

In January 2021, the Ministry of Science and Technology listed “organoid-based malignant tumor disease models” as one of the first batch of key special tasks launched under the National Key R&D Program during the 14th Five-Year Plan period. In November of the same year, the Center for Drug Evaluation (CDE) of the National Medical Products Administration (NMPA) included organoids for the first time in its guidelines for gene therapy and gene-modified cell therapy products.

In the clinical market, the state is promoting the implementation of Laboratory Developed Tests (LDTs) and Independent Clinical Laboratories (ICLs) to facilitate the translation of scientific research achievements into clinical applications. Hospitals may independently develop innovative in vitro diagnostic (IVD) reagents based on clinical needs and use them within their institutions.

Beyond major policies,China is also developing various standards for organoid models and organ-on-a-chip technologies.The Stem Cell Innovation Platform Conference held this September released a series of standards related to the field of stem cells, including the group standards “Human Colorectal Cancer Organoids” and “Human Intestinal Organoids.” The project initiation of the “General Technical Requirements for Skin-on-a-Chip,” led by Professor Gu Zhongze’s team at Southeast University, has also been publicly announced.

Some investors believe that,The FDA’s gradual acceptance of organ-on-a-chip technology will create more room for the commercialization of organoids.Domestic policy support has also been a major driver of the surge in interest in China’s organoid sector over the past two years.“For organoid companies, disease model development sees annual growth and iteration, but favorable policies can bring about true breakthroughs for the industry.”

References: