How Chinese Healthcare Companies Select GPs as LPs: Strategies and Case Studies

Andon Health

Developer and Manufacturer of Health-related Electronic Products and Smart Hardware

Hengrui Pharma

Innovative and High-Quality Pharmaceutical Developer

Fosun Pharmaceutical

Healthcare Industry Group

Since the beginning of this year, influenced by the macroeconomic environment and the pandemic, participants in the primary market have encountered varying degrees of difficulties in both fundraising and investment. With the introduction of multiple supportive policies across various regions, despite ongoing market volatility, stakeholders have demonstrated strong confidence in the future. An increasing number of listed companies are proactively partnering with investment institutions, bringing a ray of hope to the fundraising winter amidst the turbulent economic landscape.

According to incomplete statistics, more than 150 listed companies have participated in establishing industrial funds this year, investing in areas related to their own industrial chains. Among them, over 30 companies are from the medical and healthcare sector. The list of listed healthcare companies acting as Limited Partners (LPs) continues to grow, including Yuexin Health, Anxu Biotechnology, Hybribio, Intco Medical, Bloomage Biotech, Jichuan Pharmaceutical, China Pet Foods, Hansen Pharmaceutical, and Chengda Biology.

Mencius defined the three essential elements of success as favorable timing, advantageous location, and human harmony. Today, with policy support from above and dozens of medical enterprises investing as limited partners (LPs) to build momentum from below, the remaining factor hinges on people. How do medical companies make their selections?

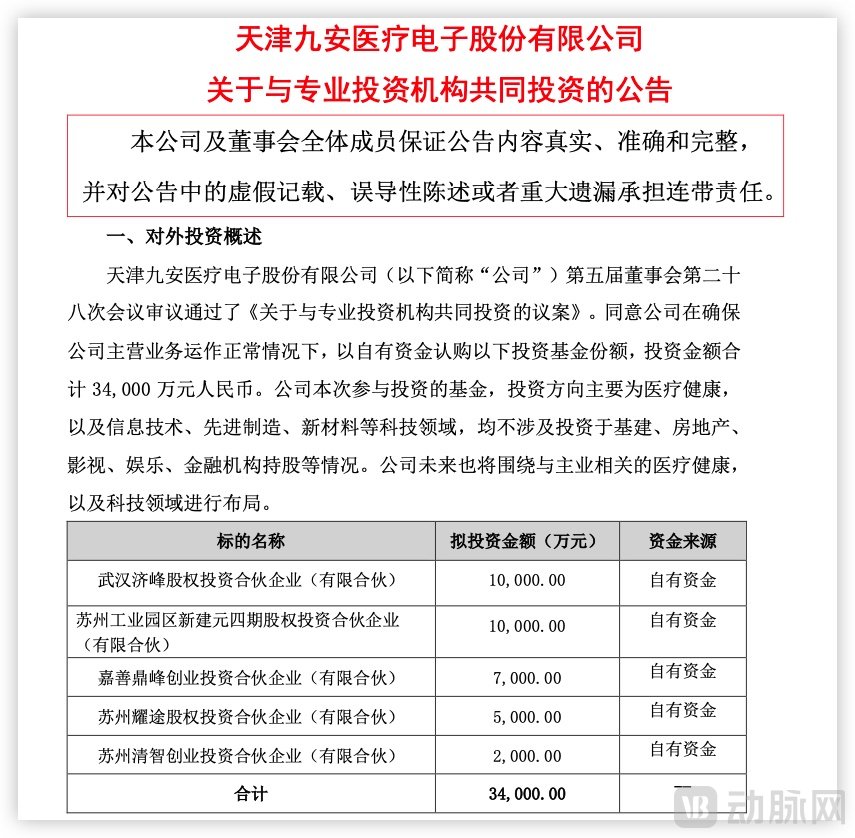

Recently, Andon Health announced that it plans to invest a total of 340 million yuan from its own funds in five funds. The investments will primarily target the healthcare sector, as well as technology fields such as information technology, advanced manufacturing, and new materials. Andon Health aims to identify new growth drivers for the company’s development by acting as a limited partner (LP).

There is no need to rehash the story of Andon Health’s stock price surging 20-fold within four months. The net profit of RMB 15.244 billion reported in the semi-annual report also reflects the company’s performance quality this year. However, a closer analysis reveals that the majority of the profit was generated in the first quarter. Financial data also show that Andon Health’s net profit in the second quarter was RMB 932 million, representing a quarter-on-quarter decline of over 90%. With the “pandemic dividend period” coming to an end, how to spend money wisely has become a pressing issue.

According to the announcement, the five institutions primarily focus their investments on healthcare, as well as technology sectors such as information technology, advanced manufacturing, and new materials. These institutions are LeapFrog Capital, Genesis Ventures, Wuyue Peak Capital, Yaotu Capital, and Huixin Investment. The respective investment amounts are RMB 100 million in LeapFrog Capital, RMB 100 million in Genesis Ventures, RMB 70 million in Wuyue Peak Capital, RMB 50 million in Yaotu Capital, and RMB 20 million in Huixin Investment.

Andon Health Investment Announcement, Image Source: Company Announcement

Public information shows that Jifeng Capital, established in 2015, is an investment firm focused on the healthcare sector and has previously invested in “tenbaggers” such as Intco Medical. Yuansheng Venture Capital, founded in 2013, is likewise an investment institution specializing in early-stage and growth-stage healthcare companies; more than ten of its portfolio companies have gone public on secondary markets.

If the two investment firms focused on healthcare and life sciences have a strong correlation with the company itself, then the other three institutions specializing in hard-tech semiconductor chips appear to be branching out beyond their core scope.

Wu Yuefeng Capital has recently come into the public eye because its founder, Wu Ping, served as the chief producer for the TV series *Zongheng Xinhai*, starring Huang Xiaoming.

Wu Ping earned his Ph.D. from Tsinghua University and the China Academy of Aerospace Science and Technology. Since 1990, he has studied and worked in Switzerland and the United States, participating in four startups. In 2001, he returned to China and co-founded Spreadtrum Communications in Shanghai while simultaneously maintaining operations in Silicon Valley. The company was listed on the NASDAQ in 2007, becoming the first Chinese chip design firm to go public.

Furthermore, from establishing the angel fund SpreadView in Silicon Valley, USA, in 2005 and beginning to invest in multiple early-stage startups in the region, to co-founding Wuyue Peak Capital in 2011, Wu Ping has successively participated in investments in numerous high-tech enterprises and has built an extensive industrial network globally.

As can be seen, whether in entrepreneurship or investment, Wu Ping’s career has been defined by one key theme: going global. Interestingly, the development trajectory of Andon Health has likewise been inextricably linked to this same theme of international expansion.

Andon Health’s current achievements are closely tied to founder Liu Yi’s three counter-trend overseas expansions. As early as 2006, Liu Yi recognized the limited domestic awareness of Chinese-made medical devices and chose to take its self-developed products global, successfully entering the German market in 2006 with a voice-enabled blood pressure monitor.

Subsequently, in 2010, Liu Yi led his team to launch a blood pressure monitoring tool that could sync with the iPhone. It was in this same year that Apple released the iPhone 4, a groundbreaking product. Leveraging Apple’s momentum, Andon Health secured the iHealth English trademark and listed on the Shenzhen Stock Exchange later that year. As for iHealth’s venture into the COVID-19 antigen test kit market in the United States, that story needs no further elaboration.

From the perspective of its current strategy as a limited partner (LP), Andon Health has chosen to not only continue deepening its presence in healthcare and wellness but also place significant emphasis on expanding into the information technology sector. It can be said that Andon Health’s selection of partners not only aligns with its own historical development experience but also involves choosing operators who understand its growth trajectory and resonate with its corporate vision.

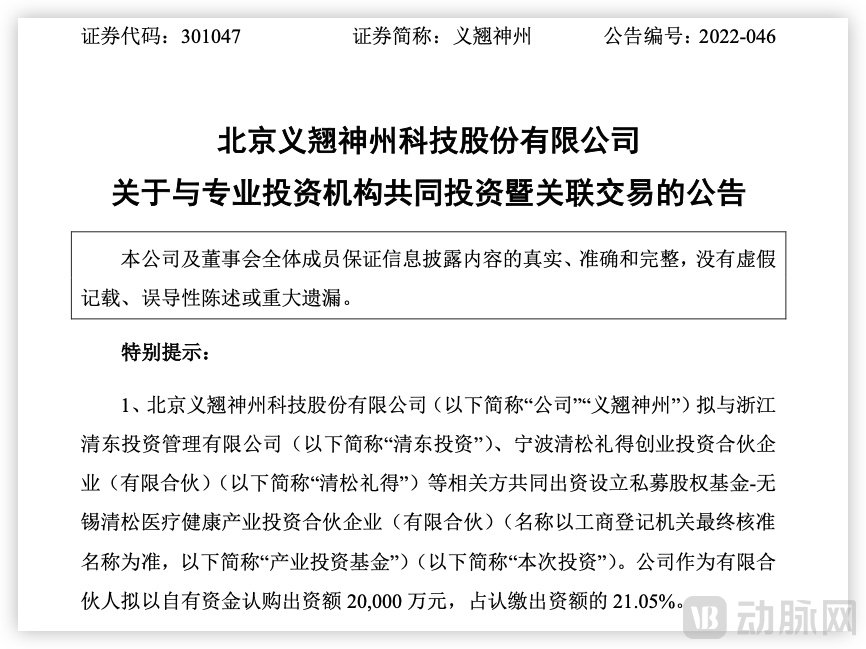

Sino Biological Inc. announced in July this year that it plans to jointly establish a private equity fund, Wuxi Qingsong Medical Health Industry Investment Partnership, with Zhejiang Qingdong Investment Management Co., Ltd., Ningbo Qingsong Lide Venture Capital Partnership (Limited Partnership), and other related parties. The company intends to subscribe RMB 200 million from its own funds, accounting for 21.05% of the total subscribed capital.

The announcement stated that Wuxi Qingsong Medical and Health Industry Investment Partnership will primarily engage in direct or indirect equity or quasi-equity investments, or investment-related activities, targeting non-listed companies in the life and health sector that are established or operating in China, or have other significant connections to China.

Interestingly, Qingsong Capital appeared as an investor in the shareholder list of Sino Biological Inc.’s 2021 IPO prospectus. Serving as a limited partner (LP) to investors who have previously invested in one’s own company is becoming an increasingly popular choice among publicly listed healthcare companies and entrepreneurs.

Sino Biological Inc. Investment Announcement, Source: Company Announcement

In 2019, when Qingsong Capital first engaged with Sino Biological Inc., the latter was still relatively small in scale, with annual revenue just surpassing RMB 100 million. Leveraging its in-depth understanding of the upstream segment of the innovative drug industry, Qingsong Capital identified high-end biological reagents as a sector worthy of intensive exploration. After conducting rigorous and comprehensive due diligence, the firm swiftly decided to invest. From investment to IPO, Qingsong Capital achieved nearly a tenfold return on paper within less than three years.

The reason for such swift and decisive action is that behind Qingsong Capital stands Dr. Zhang Song, a bioinformatics Ph.D. graduate of Tsinghua University with a profound understanding of healthcare investment. With over 15 years of investment experience, Dr. Zhang has led Qingsong Capital, founded in late 2017, to manage assets exceeding RMB 5 billion and invest in more than 30 companies in the life sciences and biopharmaceutical sectors.

United Imaging Healthcare, the leading domestic manufacturer of medical imaging equipment that listed on the STAR Market in August, is a representative investment by Zhang Song. As an investor, Qingsong Capital recorded a paper gain of more than threefold on this investment on its listing day. Similar to its investment in Sino Biological Inc., this RMB 200 million investment went from project initiation to final decision in less than two weeks.

Decision-making speed depends on the depth of industry understanding.

“Although its revenue scale is not large, overseas orders have continued to grow, and a significant number of its clients are top-tier research institutions, which indirectly attests to the product quality of Sino Biological Inc.” Regarding the assessment of these two companies, Zhang Song stated, “At the time of investment, United Imaging Healthcare was already a potential leader in the medical imaging industry. We believed then that this sector would continue to experience sustained growth, and that, compared with its competitors, the company clearly enjoyed faster growth and greater resource aggregation.”

Qingsong Capital has invested in five publicly listed companies: Sinocelltech, Recbio, Ascentage Pharma, Sino Biological, and United Imaging Healthcare. This also indirectly reflects market recognition of its investment strategy.

It is precisely because of these achievements that Sino Biological Inc. has maintained a strong relationship with the firm even after its IPO, becoming a limited partner (LP) in Qingsong Capital. While giving back to enterprises that have supported its growth is one aspect, more importantly, entrusting capital to managers with such a distinguished investment track record provides reassurance to the company’s shareholders.

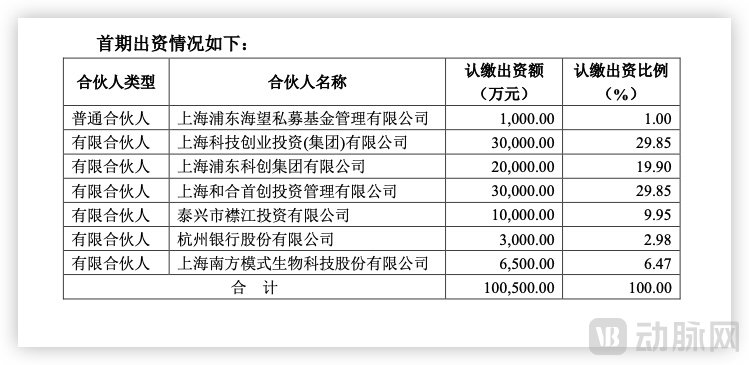

In August 2022, Shanghai Model Organisms Center, Inc. issued an announcement stating its intention to collaborate with Shanghai Pudong Haiwang Private Equity Fund Management Co., Ltd. (hereinafter referred to as "Haiwang Private Equity") and other limited partners to invest in the Shanghai Haiwang Medical Health Industry Private Equity Fund Partnership (Limited Partnership) (hereinafter referred to as the "Haiwang Medical Fund"). The fund's initial size is approximately RMB 1.005 billion. Shanghai Model Organisms Center, Inc. plans to contribute no more than RMB 65 million, while Haiwang Private Equity intends to contribute RMB 10 million and serve as the fund manager.

Haiwang Private Equity is the core platform for fund operation and management under Shanghai Science and Technology Venture Capital (Group) Co., Ltd. It manages various direct investment funds initiated by Shanghai Sci-Tech Innovation Group and serves as a key vehicle for the group’s market-oriented mechanism innovation. Currently, Haiwang Private Equity manages multiple funds, including the Shanghai Haiwang Intellectual Property Investment Linkage Fund, the Shanghai Haiwang Integrated Circuit Industry Investment Fund, and the Shanghai Haiwang Public Health and Medical Healthcare Industry Investment Fund, with assets under management exceeding RMB 10 billion.

Capital Contribution Details of Shanghai Model Organisms Center, Inc. (Source: Company Announcement)

It is worth noting that another wholly-owned subsidiary under Shanghai Science and Technology Innovation Investment Group is a shareholder of Shanghai Model Organisms Center, Inc. (Southwest Model Biology) and has played a significant role in its development. As early as 2005, in accordance with the approval from the Shanghai Municipal Development and Reform Commission, Shanghai Science and Technology Investment Co., Ltd. served as the project legal entity to construct the Shanghai Laboratory Animal Resource Public Service Platform, which was provided free of charge to Southwest Model Biology and several other entities.

Based on past investment experience, unlike other market-oriented venture capital firms, Shanghai Science and Technology Innovation Investment Group positions itself as an integrator of innovation resources and a shaper of industrial development. In equity investments, it focuses more on industry chain-oriented investing, listing all sub-sectors within each industry to pursue a “fill-in-the-blank” investment strategy, with the ultimate goal of building complete industrial chains.

Faced with the limited market space for model organisms, it is necessary to actively explore new development paths. Shanghai Model Organisms Center, Inc. has extended its business into the upstream and downstream markets of new drug R&D, entering the preclinical drug evaluation industry chain by offering CRO services such as phenotypic analysis and pharmacological efficacy evaluation, thereby establishing a one-stop service system ranging from the construction of genetically modified animal models to phenotypic analysis and pharmacological efficacy evaluation.

Although the GP he selected is not as renowned as those chosen by other publicly listed healthcare companies, at this stage of development, it is a reasonable and prudent choice for Shanghai Model Organisms Center, Inc., acting as an LP in its outward investments, to partner with such a GP. This partner has previously assisted the company in its own growth, pursues investments aimed at deepening vertical integration within the industry chain, and boasts a reliable background.

Hengrui Pharma announced in June that it plans to jointly establish the “Shanghai Shengdi Biopharmaceutical Fund” with its controlling subsidiary, Shengdi Investment, and its controlling shareholder group, with a total scale of RMB 2 billion. The most distinctive feature of Hengrui’s role as a limited partner (LP) is its use of a holding subsidiary as the general partner (GP), thereby granting Hengrui Pharma greater control over investment directions.

Professional investment teams serving as General Partners (GPs) prioritize returns and exit strategies. In contrast, private equity funds backed by Hengrui Pharma place greater emphasis on products and their integration with the company’s existing resources. As an industry leader, Hengrui’s industry-focused funds generate industrial empowerment effects when investing in the pharmaceutical sector. Furthermore, mergers and acquisitions (M&A) serve as a key exit route for such industry funds; this implies that the Limited Partners (LPs) may well be among the potential acquirers of the target companies at the time of investment.

When pharmaceutical companies like Hengrui Pharma act as limited partners (LPs), their specialized industry expertise enables them to better identify high-value projects. Furthermore, Hengrui’s move into the LP role carries implications for strategic industrial layout. In the future, this could even give rise to a Chinese version of the “Eli Lilly Asia Ventures.”

When pharmaceutical companies act as limited partners (LPs), in addition to leveraging their industry expertise, they also adhere to the principle of “not investing in what is unfamiliar.”

Fosun Pharmaceutical issued an announcement in April, signing the "Target Fund Partnership Agreement" with Shanghai Weiyi and Shanghai Anpu. Fosun Pharmaceutical intends to act as a limited partner (LP) and contribute RMB 60 million to subscribe for an equivalent equity stake in the target fund’s initial fundraising round. The fund manager is Shanghai Weiyi (Jingxu Venture Capital), which primarily invests in enterprises engaged in innovative medical devices, diagnostic reagents, new drug and vaccine research and development, and other biomedical-related fields.

It is worth noting that Qian Tingzhi, Founding Partner of Jingxu Venture Capital, previously held long-term positions at Fosun Group, serving as Head of Group Strategy and Head of International Business Development, among other roles. As early as 2009, while working at Fosun Group, Qian Tingzhi engaged with numerous overseas venture capital firms; at that time, healthcare venture capital in China was an emerging sector.

With the rapid development of domestic medical venture capital (VC) funds since 2013, Qian Tingzhi established Jingxu Venture Capital in 2015, investing successively in projects such as Biocytogen, Xnuo Pharmaceutical, and Kunyuan Genomics. Among these, HaiChuang Pharmaceuticals and Chaoju Eye Care have successfully completed their initial public offerings (IPOs), while 18 other portfolio companies have smoothly advanced to their next rounds of financing.

It is precisely on the basis of such achievements that Qian Tingzhi received a collaboration proposal from her former employer.

For listed pharmaceutical companies, becoming a limited partner (LP) is merely the first step. A fund typically undergoes a full lifecycle of 5 to 7 years, encompassing fundraising and structuring, investment management, exit strategies, and liquidation. The biotech sector, which Hengrui Pharma targets, has recently faced a turbulent environment. Research and development efforts are concentrated on crowded therapeutic targets, costs are soaring, and commercialization requires navigating multiple hurdles. Even after market approval, companies still confront a series of uncertainties, including national reimbursement drug list (NRDL) negotiations, volume-based procurement (VBP), and payment system reforms. These combined factors have contributed to the sluggish investment climate in both the primary and secondary markets for biotech.

Regardless, while many listed pharmaceutical companies are flocking to become limited partners (LPs), most remain focused on their familiar domains. This strategy not only enhances industrial synergy and strengthens their own supply chains but also facilitates the identification of high-quality M&A targets, thereby creating new profit growth drivers and seeking capital appreciation. At the same time, this trend injects vitality into the entire pharmaceutical industry.

An investor told VCBeat that when publicly listed healthcare companies act as limited partners (LPs), they primarily consider two aspects: “First, to manage the company’s market capitalization; second, after establishing a fund, the listed enterprise can make external investments centered on its own industrial chain, thereby better capturing innovative technologies within the industry and laying the groundwork for future mergers and acquisitions. For investors, the funds allocated to equity investment funds can be viewed as R&D expenditures, with the R&D being conducted by external companies.”

Amidst industry transformation and intensifying competition, numerous publicly listed healthcare companies are not only increasing their R&D investments but also seeking to break through the current predicament of insufficient product innovation and weak competitiveness by investing as limited partners (LPs). These major enterprises are adopting diverse strategies to select different general partners (GPs). How they will navigate the industry’s painful adjustment period and achieve strong performance in the future remains worthy of close attention.