Hongbo Pharmaceuticals Lists on ChiNext: A Survival Blueprint for Small and Mid-sized CXO Firms?

After enduring a rare four rounds of inquiries and one round of implementing the opinions of the Listing Review Center, Pharmaresources (Shanghai) Co., Ltd., a CXO company under significant pressure, has finally made it to the Shenzhen Stock Exchange, ushering in the critical moment of its IPO.

Today, Pharmaresources (SZ:301230) officially listed on the ChiNext board of the Shenzhen Stock Exchange, with an opening price of RMB 48.00 and a high of RMB 55.96. As of press time, its maximum gain reached 39.90%.

Not only Pharmaresources, but on October 26, CXO concept stocks surged significantly during trading, with multiple related stocks hitting the daily limit up or closing with gains exceeding 10%. Baicheng Medicine, Joinn Laboratories, and Baihua Medicine all hit the limit up, while Asymchem also touched the limit up intraday. Pharmaron, Medicilon, Tigermed, and ChemPartner rose by more than 10%. WuXi AppTec closed up 6.83%, having approached the limit up at one point during the session.

CXO Sector’s Q3 Reports Also Show Widespread Growth. In the first three quarters, WuXi AppTec and Joinn Laboratories are expected to see year-on-year net profit growth exceeding 100%; Asymchem’s net profit is projected to rise by approximately 290%; and Porton Pharma’s net profit has surged by more than 300%.

Over the past three years, as its scale has continued to expand, Pharmaresources (Shanghai) Co., Ltd. has seen steady growth in operating revenue, which amounted to RMB 245 million, RMB 283 million, and RMB 448 million in 2019, 2020, and 2021, respectively. Net profits for these years were RMB 47.254 million, RMB 48.6914 million, and RMB 73.5766 million, respectively.

However, in terms of revenue scale, Pharmaresources is still considered a small to medium-sized domestic CRO enterprise.

How such companies leverage IPO proceeds to successfully address the existential challenges commonly faced by CXO firms—including volume-based procurement, patent expirations, the international trade landscape, the COVID-19 pandemic, and global expansion with local adaptation—thereby sustaining growth or even achieving leapfrog development, remains the industry’s primary concern.

How Significant Is the Impact of COVID-19 and Trade Dynamics on CXO?

In the IPO prospectus of Pharmaresources (Shanghai) Co., Ltd., two sets of data are particularly noteworthy.

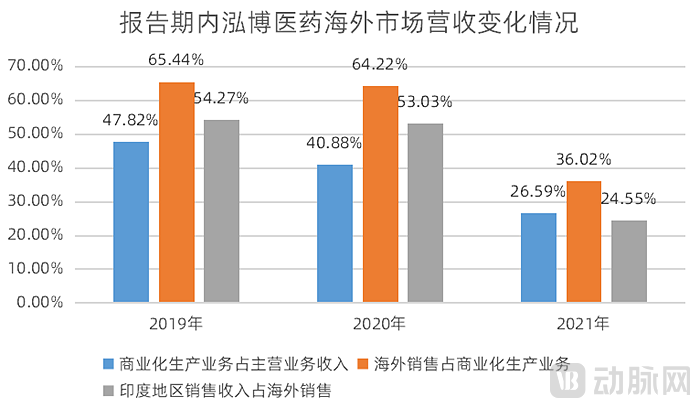

The first set of data is:Since the fourth quarter of 2020, Pharmaresources’ sales revenue in India has decreased by 74.36% compared to the same period in 2019; in 2021, its sales revenue in India also experienced a significant decline of 51.74% compared to 2020.

Another set of data is:From 2019 to 2021, the proportion of sales revenue from the United States in Pharmaresources' main business revenue was 38.42%, 39.95%, and 50.74%, respectively.

The divergent revenue trends—declining in the Indian market and growing in the U.S. market—are closely intertwined with Pharmaresources’ development strategy, corporate positioning, and the prevailing macroeconomic environment.

As a local small and medium-sized CRO enterprise, Pharmaresources initially built its business on orders from foreign pharmaceutical companies. To date, Pharmaresources has amassed a diverse clientele of domestic and international pharmaceutical enterprises, including Agios, Alexion, KSQ, Jnana, Nuvalent, BeiGene, Patheon, Sun, KRKA, Hengrui Medicine, CSPC Pharmaceutical Group, HEC Pharm, Simcere Pharmaceutical, Yangtze River Pharmaceutical Group, and Salubris, among other renowned pharmaceutical companies at home and abroad.

According to the prospectus, the overseas customers of Pharmaresources’ commercial manufacturing business (primarily ticagrelor series intermediates) are mainly located in India and Europe.

Changes in Pharmaresources' Overseas Revenue During the Reporting Period, Source: Prospectus

In addition to commercial manufacturing services such as intermediate products, Pharmaresources’ drug discovery and process research and development (PR&D) businesses also primarily serve overseas clients. From 2019 to 2021, revenue from overseas clients accounted for 95.79%, 88.44%, and 82.70% of the combined revenue from these two business segments, respectively.

Since the third quarter of 2020, overseas regions have been affected by the pandemic, with India being particularly severely impacted. This has led to a continuous decline in customer orders for Pharmaresources (Shanghai) Co., Ltd., which is the primary reason for the sustained decrease in the first group’s revenue figures.

Regarding why Pharmaresources focused on expanding into the Indian market and is now shifting its focus back to the U.S. market, an API industry analyst stated, “The logic behind market expansion is related to the degree of market regulation.”

The global pharmaceutical market can be broadly divided into two categories: regulated markets and unregulated markets.

Regulated markets generally refer to markets where drugs and related products must undergo standard regulatory submission and approval processes before being launched, and are protected by patent barriers such as market exclusivity periods. China, the United States, and Europe are all considered regulated markets. In contrast, non-regulated markets have opposing regulatory frameworks; for example, in countries like Brazil and Argentina, pharmaceutical patent terms are largely disregarded, drug purchasing power is relatively weak, and few originator pharmaceutical companies establish a presence in these regions.

India’s advantage lies in its position between regulated and unregulated markets.

In 2005, although India amended its Patent Act, patent protection was granted only to new drugs invented after 1995 or to improved drugs that could significantly enhance therapeutic efficacy, while patents for combinations of existing drugs or derivative drugs were not supported. As a result, drugs that are still under patent protection in other parts of the world are currently subject to R&D and manufacturing practices in India in accordance with the earlier legislation. Collaborating with the Indian market offers greater flexibility.

In addition to its collaborations with Indian enterprises, Pharmaresources has also made significant strategic arrangements in the United States.In recent years, uncertain factors such as trade frictions between China and the United States have appeared to undermine the competitiveness of domestic enterprises like Pharmaresources in overseas markets, but this is not the case.

The second set of data shows that the trade friction between China and the United States in recent years has indeed not had a significant impact on the revenue of Pharmaresources, and its overseas customers for pharmaceutical research and development outsourcing services are mainly located in the United States.

On the other hand, pharmaceutical R&D outsourcing services and the production and sales of intermediates are not included in the U.S. trade restriction list against China. As for how the situation will evolve in the future, it remains uncertain.

Compared with the established domestic market, small and medium-sized CROs in China appear to have broader opportunities overseas.

Industry insiders revealed, “The pandemic has had an impact on the entire pharmaceutical industry, while the impact of the trade situation remains uncertain.”The CXO market does not have a strict division between overseas and domestic operations. The key lies in securing orders, which are the essential condition for determining whether a company can continue to survive., once the order is secured, all challenges can be overcome.”

However, compared with multinational CROs and domestic CRO leaders such as WuXi AppTec and Pharmaron, Pharmaresources is relatively small in terms of both business scope and scale. This places higher demands on the company’s market development capabilities and research service standards, requiring it to break through the brand monopoly effect established by these industry giants.

Case Study: The Impact of Centralized Procurement on API Manufacturers

In addition to the shifting international landscape and the Indian market, which has been severely impacted by the pandemic, CXO companies are also facing a grim situation in China.Price reductions for pharmaceutical formulations driven by centralized procurement, coupled with impending patent expirations for drugs, constitute the two primary challenges currently facing the pharmaceutical industry and its affiliated enterprises.

Pharmaresources’ currently commercialized main products are intermediates in the ticagrelor series. The patent for these compounds expired at the end of 2019, and the finished dosage form was included in China’s National Centralized Drug Procurement program in 2020.

Will patent expirations lead to intensified competition and a heated-up market landscape?Perhaps. However, intensified competition will also drive up the demand for active pharmaceutical ingredients (APIs). According to the prospectus, generic drug manufacturers began procuring API intermediates in advance to prepare for formulation production before the expiration of the compound patent for ticagrelor. Consequently, market demand for this product, both domestically and internationally, saw a significant increase starting from 2019.

On the other hand, will the decline in finished drug product prices resulting from the volume-based procurement of ticagrelor indirectly lead to a drop in Pharmaresources’ API prices, thereby delivering a fatal blow to the company?

According to the prospectus, during the reporting period, sales revenue from ticagrelor series intermediates accounted for 81.68%, 87.16%, and 91.68% of the commercial production business, respectively. It appears that the volume-based procurement of ticagrelor formulations will deliver a fatal blow to Pharmaresources (Shanghai) Co., Ltd.

However, the prospectus also shows that in 2020 and 2021, the revenue from Pharmaresources’ ticagrelor API awarded bids accounted for 23.66% and 31.59%, respectively, of its commercial production business revenue, but only 9.67% and 8.40%, respectively, of its total main business revenue, indicating that it did not constitute a majority of the company’s overall revenue.

Thus, it is evident that the series of ticagrelor intermediates does not determine the survival of Pharmaresources (Shanghai) Co., Ltd. Moreover, not only for Pharmaresources but for most companies, the inclusion of finished formulations in the centralized volume-based procurement program does not necessarily lead to a significant decline in API prices.

VBInsight has verified through multiple sources that the cost of most APIs accounts for less than 10% of the total formulation cost.

"Under the pressure of centralized procurement, most formulation companies do not choose to significantly reduce hard costs such as API, but instead opt to cut soft costs like marketing. 'The cost of most APIs has already hit rock bottom, so the impact on them (API companies) after centralized procurement will not be significant,' an industry insider revealed."

The Impact of Volume-Based Procurement on API Manufacturers Is Not as Devastating as Commonly Perceived. From various perspectives, policies such as volume-based procurement also reflect the gradual standardization of China’s pharmaceutical sector, whereby companies with cost advantages and technological innovation capabilities are poised to emerge as leaders.

Is Transformation an Inevitable Choice for CMO Companies?

Although CXO companies such as Pharmaresources (Shanghai) Co., Ltd. face a series of common uncertainties, including volume-based procurement, trade dynamics, the COVID-19 pandemic, and localized monopolies, the R&D of innovative drugs has become a new driving force for the pharmaceutical industry. This shift is influenced by multiple factors, including rising clinical demand, iterative advancements in therapeutic methods, patent cliffs, and the pursuit of profits, presenting unprecedented opportunities for contract research organizations (CROs).

Some CMO companies that primarily focus on API production are also beginning to consider transformation.

Regarding the transformation of traditional CMO companies, industry experts have pointed out that transformation is not a mandatory choice for such traditional enterprises. Each company has its own “soul,” and the risks associated with transformation are no less than those posed by these comprehensive factors. “If you already occupy a stable market position in your niche segment and possess technological barriers, you may choose to continue deepening your expertise in this area.”

Some industry insiders have also expressed differing views,“Most traditional CMO companies are actually considering transformation, as everyone aims to achieve integration of active pharmaceutical ingredient (API) and drug product manufacturing.”

For instance, large enterprises such as Qilu Pharmaceutical, Kelun Pharmaceutical, and Yangtze River Pharmaceutical Group initially focused primarily on finished dosage forms, gradually expanding their API production capacity to transform into integrated companies. Jiuzhou Pharmaceutical serves as an even more typical example. As one of the largest CMOs in China, Jiuzhou Pharmaceutical has increasingly emphasized its CDMO capabilities in recent years, shifting its development focus toward the “D” (development) aspect. “The CMO market is largely saturated; to increase market share beyond this point, companies must explore new products and services.”

Pharmaresources clearly falls into the latter category. Since its establishment, its core business and operational model have undergone three distinct phases of evolution:

From 2007 to 2010, Pharmaresources’ business scope was primarily focused on the drug discovery stage, providing overseas new drug R&D enterprises with services ranging from hit-to-lead development to clinical candidate screening, thereby meeting their R&D needs in compound design, optimization, and synthesis during the new drug discovery phase.

Building on the R&D and experimental expertise accumulated during the first phase, Pharmaresources laid a solid foundation for process development. From 2010 to 2014, the company expanded its business scope to encompass drug discovery and process research and development (R&D) services, gradually establishing a comprehensive system for synthetic process development and research. Its drug development services cover the entire spectrum from preclinical stages to New Drug Application (NDA) submission, including overcoming existing synthetic routes, pioneering innovative synthetic pathways, and providing customized optimization from preclinical development through to NDA approval.

Pharmaresources has laid the foundation for commercial production of intermediates and active pharmaceutical ingredients (APIs) from kilogram to ton scale by researching and developing low-cost, safe, environmentally friendly, and robust synthetic processes. Its development has entered the third phase, which has remained stable to date (2014–present): drug discovery, process research and development, and commercial manufacturing. During this phase, Pharmaresources expanded downstream into commercial manufacturing through the merger with Kaiyuan Hongbo.

With this, Pharmaresources has successfully completed its transformation, establishing a technical platform and service system that covers all stages of drug research and production, including drug discovery, process research and development, and commercial manufacturing.

It is not difficult to foresee that, with this IPO, Pharmaresources (Shanghai) Co., Ltd. hopes to leverage the capital market to make a leap forward in its transformation journey.