A $38 Billion Market Cap Giant Emerges: Can the Collagen-Based Aesthetics Sector Get Even Hotter?

Giant Biogene

Skin Care Product R&D Developer

Bloomage Biotech

Developer of bioactive substance products, producer of hyaluronic acid raw materials

Giant Biogene, China’s largest professional skincare company specializing in collagen products, successfully completed its IPO yesterday.

In terms of stock price performance, Giant Biogene is highly favored by secondary market investors.Giant Biogene priced its IPO at HK$24.3 per share, surging on debut and pushing its market capitalization above HK$30 billion at one point.As of yesterday's close, Giant Biogene finally closed at HK$26.7, up 9.877%, with a market capitalization of HK$26.476 billion.

(Giant Biogene Listing Ceremony)

(Giant Biogene Listing Ceremony)

As China’s first listed company in the collagen sector, Giant Biogene has attracted widespread market attention since it filed its prospectus.

· First, the impressive financial data. The prospectus shows that the company's total net profit over the past three years exceeded RMB 2 billion, with a gross profit margin of around 85%, approaching that of Moutai.

·Second, the company boasts a star-studded lineup of investors behind it. The prospectus reveals that numerous investment institutions, including Hillhouse Capital, CPE Yuanfeng, Jinyi Capital, Legend Capital, Xingnahe Capital, Maixing Investment, Greenwoods Asset Management, CDH Investments, CICC Capital, Heiyi Capital, Gaorong Capital, Haisong Capital, and China Development Bank Innovation Capital, are all shareholders of Giant Biogene. In addition, Qianxun (founded by Viya’s husband) and Sanrenxing Media also appear on the list of shareholders.

· Third, Giant Biogene represents a classic entrepreneurial story of a professorial couple. Both founders, Fan Daidi and her husband Yan Jianya, graduated from Northwest University and subsequently pursued advanced studies. In 2000, Dr. Fan Daidi and her team successfully developed recombinant collagen technology, and that same year, she co-founded Giant Biogene with her husband, Yan Jianya.

Besides the successful listing of Giant Biogene, which triggered a buying frenzy among investors, other companies in the collagen sector have also been highly active in the capital markets this year.

Regarding IPOs, Jinbo Biotech’s listing application was accepted in June; Chuanger Bio submitted its filing to the Beijing Stock Exchange in January. In the primary market, Suhua completed a strategic financing round worth tens of millions of yuan in October; Trautec Medical closed its Series A financing round of nearly RMB 200 million in August, led by Shiseido Ziyue Fund; in April, Bloomage Biotech announced the acquisition of a 51% equity stake in Yierkang Bio for RMB 233 million, formally entering the collagen industry...

It is evident that a growing number of collagen companies are emerging, while industry giants are also accelerating their entry into the market. Against this backdrop, how is the competitive landscape evolving? What future growth opportunities remain? To address these questions, VCBeat has conducted reviews and interviews with industry veterans to gain preliminary insights.

Since 2021, the collagen sector has frequently seen news of IPOs and financing rounds, driving surging industry enthusiasm.

In fact, collagen is not a novel concept in the field of medical aesthetics. Indeed, collagen products gained regulatory approval more than two decades before hyaluronic acid: as early as 1981, Zyderm, the world’s first bovine collagen implant, was approved, ushering in the era of collagen applications in medical aesthetics.

However,Although collagen products received approval earlier, their commercialization progressed more slowly than that of hyaluronic acid. This was primarily due to the relatively low cost-effectiveness and higher biosafety risks associated with collagen at the time.

A research report from Huachuang Securities indicates that approximately 3% of the population is sensitive to bovine collagen. Furthermore, collagen products require two rounds of skin testing prior to injection; even if the skin test results are negative, allergic reactions and other more severe adverse effects cannot be completely ruled out.

Relevant reports have disclosed that prior to 1990, approximately 0.04% of patients who received bovine collagen products (Zyderm or Zyplast) developed complications such as cysts at the injection site.

The turning point emerged from breakthroughs in recombinant collagen-related technologies.Specifically, recombinant collagen is a general term for collagens obtained through genetic recombination, cell factory construction, fermentation, and separation and purification technologies. Unlike traditional animal-derived collagen, recombinant collagen involves higher technical barriers in its production process.

For example, the denaturation temperature of recombinant collagen is above 72°C, significantly higher than the 37°C–40°C range for animal-derived collagen, making recombinant collagen easier to transport and store.

As a general partner (GP) that was among the first to bet on the collagen sector and has since deepened its strategic layout, Dr. Wang Zhen, Partner at Mingfeng Capital, told VCBeat that recombinant collagen offers greater standardization and lower costs for large-scale production. Meanwhile, through sequence design, recombinant collagen can minimize immunogenicity and control the risk of pathogenic virus transmission, thereby demonstrating favorable biocompatibility and safety.

In the field of recombinant collagen, domestic enterprises such as Giant Biogene, Jinbo Biopharmaceutical, Trautec Medical, and Jiyuan Bio have already established their presence.Among them, Giant Biogene, which is going public this time, is the first company in China to utilize synthetic biology methods to develop proprietary recombinant collagen.

“Giant Biogene is a pioneer in the synthetic biology industry. It has not only established leading technology platforms in genetic engineering, tissue engineering, and materials engineering, but also applied its scientific research achievements to the broader health sector, setting a benchmark for best practices in integrating industry, academia, and research,” said Wang Wenlong, Managing Director at Legend Capital, at the time of Giant Biogene’s IPO.

(Overview of Companies Entering the Recombinant Collagen Sector)

(Overview of Companies Entering the Recombinant Collagen Sector)

It is worth specifically noting that, according to the Guiding Principles for the Nomenclature of Recombinant Collagen Biomaterials issued in 2021, recombinant collagen can be classified into three categories: recombinant human collagen, recombinant humanized collagen, and recombinant collagen-like protein.

In the field of skincare, the mass production of recombinant human collagen currently faces significant technical challenges and high production costs, making commercialization difficult. Furthermore, as the amino acid sequences of recombinant collagen-like proteins are not entirely identical to those of human collagen, their safety and efficacy require further in-depth investigation.Therefore, the strategic focus of major enterprises is on recombinant humanized collagen.

However, to achieve industrialization and large-scale production akin to hyaluronic acid, technological breakthroughs alone are far from sufficient for companies in the collagen sector; what is also required is growth in market demand and breakthroughs in supply-side production capacity.

On the demand side of the marketIn recent years, with the rise of the "beauty economy" and the continuous increase in per capita disposable income, non-surgical medical aesthetics have become increasingly popular. This has propelled the collagen sector to ride the wave of growth.

“Current public demand for medical aesthetics has evolved beyond mere aesthetic enhancement to include biological functionality, with consumers seeking products that can seamlessly integrate with their own tissues after use. This is where collagen comes into focus,” Dr. Xiao E, Chief Technology Officer and Chairman of Meibo Biopharma, previously told VCBeat.

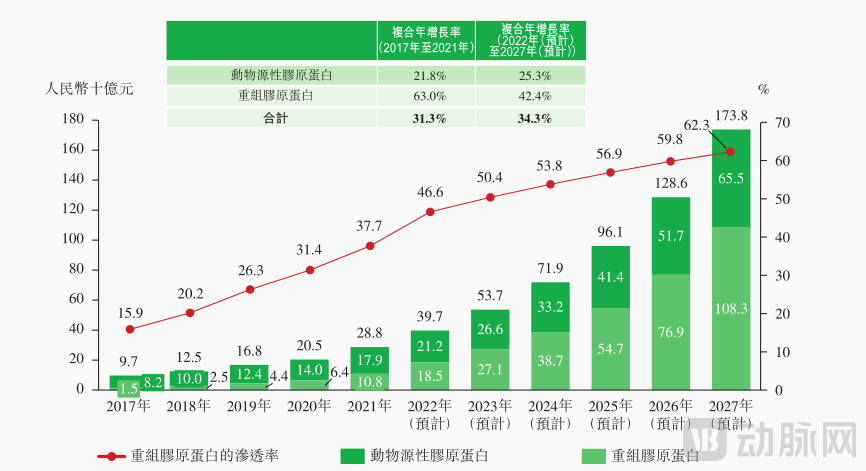

According to Frost & Sullivan, the market size of recombinant collagen products in China is projected to increase from RMB 18.5 billion in 2022 to RMB 108.3 billion in 2027, representing a compound annual growth rate (CAGR) of 42.4%.

(Market Size of Recombinant Collagen Products in China. Image Source: Giant Biogene Prospectus)

(Market Size of Recombinant Collagen Products in China. Image Source: Giant Biogene Prospectus)

Turning to Supply-Side Capacity, the collagen industry is currently in a ramp-up phase in terms of production capacity. According to a report by Huachuang Securities, Shuangmei’s annual collagen production capacity is 1.8 tons, which still lags significantly behind that of hyaluronic acid. For context, Bloomage Biotech alone currently has an annual hyaluronic acid production capacity of 420 tons.

Consequently, collagen companies are continuously improving their technologies and production processes, with many establishing new manufacturing facilities. According to the prospectus, Giant Biogene currently operates one recombinant collagen production line, with an annual capacity of 1.1 metric tons. Under its IPO financing plan, the company is expected to complete a recombinant collagen fermentation workshop in the first half of 2023, which will increase its annual capacity by approximately 20-fold to 21.25 metric tons.

From the perspective of technological and process breakthroughs, Jinbo Bio has achieved breakthroughs in two core technologies: “Application Technology Based on Virus Entry Inhibition Mechanism” and “Biological Fermentation Technology for Preparing Recombinant Humanized Collagen.” These advancements have provided support for the industrialization of its recombinant collagen products and anti-HPV biological protein products.

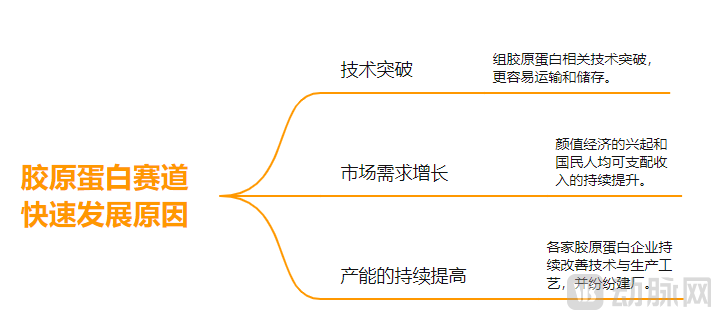

As can be seen from the above, under the broader trends of rising demand, technological breakthroughs, and accelerated capacity expansion, collagen is gradually approaching the eve of a market explosion.

(Reasons for the Rapid Development of Collagen; Graphic by VCBeat)

(Reasons for the Rapid Development of Collagen; Graphic by VCBeat)

Currently, an increasing number of companies are entering the collagen sector.

These include Giant Biogene, Jinbo Bio, Trauer Bio, Suhua, Trauer Medical, Yierkang Bio, Meibo Pharmaceutical Biology, Jiyuan Bio, Marubi, Shuangmei Life Sciences, Changchun Botai, Bloomage Biotech, Aoyuan Beauty Valley, and other enterprises.

From the choices made by various companies, collagen is predominantly used in functional skincare products, medical dressings, and injectable fillers. Among these, functional skincare products and medical dressings are the mainstream choices, accounting for the vast majority of market share.

According to Frost & Sullivan’s data, functional skincare products and medical dressings ranked as the top two categories in sales revenue within the collagen product segment, achieving growth rates of 52.8% and 92.2%, respectively, from 2017 to 2021.

In terms of market size, taking functional skincare products containing recombinant collagen as an example, the market size has grown from RMB 840 million in 2017 to RMB 4.6 billion in 2021, with a compound annual growth rate (CAGR) of 52.8%. It is projected to further increase from RMB 7.2 billion in 2022 to RMB 64.5 billion in 2027, achieving a CAGR of 55%, indicating a market potential worth tens of billions of yuan.

There are two primary reasons for this. First, from a technical perspective, the R&D threshold for collagen-based functional skincare products and medical dressings is lower than that for Class III injectable products. Second, driven by the surge in market demand for energy-based devices, medical dressings—used as post-procedure care products—have experienced growth in tandem with the expansion of the non-surgical medical aesthetics sector.

Giant Biogene’s rapid growth has been driven by its strategic positioning at the forefront of the rising functional skincare and medical dressing markets.

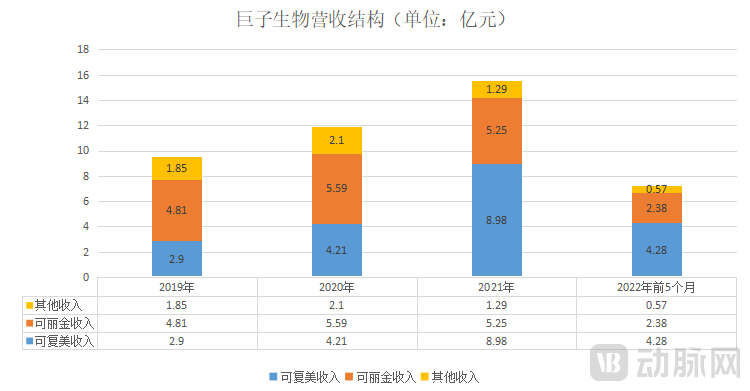

A review of Giant Biogene’s prospectus reveals that its revenue is primarily driven by two flagship products: Collgene, a functional skincare product (registered as a cosmetic), and Comfy, a medical dressing (registered as a medical device).

Financial data shows that from 2019 to the first five months of 2022, Comfy’s revenues were RMB 290 million, RMB 421 million, RMB 898 million, and RMB 428 million, respectively; while Collagen’s revenues were RMB 481 million, RMB 559 million, RMB 525 million, and RMB 238 million, respectively. The combined revenue of these two brands accounted for more than 90% of the total revenue.

(Giant Biogene's Revenue Structure | Chart by VCBeat)

(Giant Biogene's Revenue Structure | Chart by VCBeat)

Moreover, the gross profit margins of these two major brands are also substantial: Comfy’s gross profit margin has consistently remained above 85%, while Collgene’s has been maintained at over 80%. This has supported Giant Biogene’s exceptionally high gross profits, which amounted to RMB 797 million, RMB 1.007 billion, RMB 1.354 billion, and RMB 667 million in 2019, 2020, 2021, and the five months ended May 31, 2022, respectively, with corresponding gross profit margins of 83.3%, 84.6%, 87.2%, and 85%.

However, the functional skincare and medical dressing sectors are becoming increasingly “crowded.”Bloomage Biotech, one of the “three musketeers” of the medical aesthetics industry, has already established its presence. Its portfolio of functional skincare brands includes Biohyalux, QuadHA, Medrepair, and BM Actives, with products priced around RMB 100 to RMB 300.

Botanee’s portfolio includes Winona, a skincare brand for sensitive skin, which contributes the vast majority of Botanee’s revenue. According to financial reports, Botanee’s revenues from 2019 to 2021 were RMB 1.944 billion, RMB 2.636 billion, and RMB 4.022 billion, respectively, with sales from the Winona brand accounting for 99.68%, 99.85%, and 99.37% of the company’s total revenue over these three years.

Additionally, in March 2021, Marubi Co., Ltd. collaborated with the National Engineering Research Center for Genetic Engineering Pharmaceuticals to launch “Beauty Rule,” a high-efficacy anti-aging skincare brand featuring fully human-derived collagen as its key ingredient. Trauer Biotech has also established the “Trauerme” brand, whose primary component is natural collagen.

How Intense Is the Competitive Pressure? According to a report by Guohai Securities, as of June 2020, there were a total of 467 approved medical skin repair dressings in China. Class I certifications, primarily for medical cold compress patches, accounted for 90%, while Class II and Class III certifications, mainly for wound dressings, accounted for 9% and 1%, respectively. The variety of approved medical dressing products has become quite extensive.

In the realm of functional skincare products, data from Biaodian Pharma indicates that between July 2019 and June 2020, among the top 100 best-selling reparative sheet masks on the Taobao Tmall platform, 28 brands each achieved sales exceeding RMB 10 million. Meanwhile, even for cosmetics companies with significant brand influence, such as Kans, Mask Family, and Shiseido, their individual market shares did not exceed 10%.

Therefore,Considering key factors that significantly influence the sales of consumer-oriented products, such as sales channels and brand influence, competition in the functional skincare and medical dressing sectors is expected to intensify in the future.

With Giant Biogene’s listing, the acceptance of Jinbo’s IPO application, and Chuanger Bio’s shift to the Beijing Stock Exchange, the market landscape is gradually stabilizing, with early signs of a leading-player effect emerging.

In such a scenario, do other collagen companies still have a chance to emerge as leaders?

In this regard, Wang Chenchen, an investor at Shaanxi Venture Capital Group, previously told VCBeat that in the medical dressing market, unless startups can develop more innovative products, it will be difficult for them to compete with several leading companies. The opportunities remaining for them may be limited to peripheral products and contract manufacturing.

After all, the medical dressing market is primarily oriented toward mass consumers, necessitating substantial marketing investments. Financial report data reflect this: Trauer Bio’s marketing expenses exceeded RMB 300 million from 2019 to 2021, while Giant Biogene’s total selling expenses during the same period reached as high as RMB 600 million.

In addition, collagen enterprises in China face a series of regulatory policies. These include policies specifically targeting the collagen industry, as well as relevant regulations governing application sectors such as medical devices and cosmetics.

In this case,Venturing into the more technically challenging field of Type III collagen filler products may be a superior direction.In this market, there are currently only four domestic companies: Shuangmei Biotech, Changchun Botai, Hanfu Biotech, and Jinbo Biotech.

Currently, product types vary among manufacturers. Shuangmei Biotech, Changchun Botai, and Hanfu Biotech offer animal-derived collagen products, while Jinbo Biotech’s Wei Yi Mei is currently the only collagen product derived from genetically engineered recombinant technology.

From the perspective of the competitive landscape, the current collagen filler market has few participants, which presents significant development opportunities for innovative companies with strong R&D capabilities.

“Animal collagen technology is already highly mature, and future technological iterations are likely to focus on differentiating animal sources.“Dr. Wang Zhen, Partner at Mingfeng Capital, stated, “andIn the field of recombinant collagen, companies whose collagen exhibits higher bioactivity and longer expressed functional domains are highly likely to emerge as the next generation of industry giants.”

In summary, for companies in the collagen sector, technological prowess remains the most critical core competency. Only by leveraging technology as a driving force can they capitalize on the window of opportunity presented by industry growth and thereby achieve substantial returns.

After all, in the medical field, technology determines qualifications and also establishes time-based barriers.