Xiamen Huaxia Eye Hospital IPO Raises Nearly RMB 40 Billion in Market Cap: Where Is the Next Growth Driver for China's 'Golden Ophthalmology'?

Huaxia Eye

Large Ophthalmology Medical Service Provider

On November 7, Huaxia Eye successfully completed its initial public offering (IPO) on the ChiNext board. The stock surged on its debut trading day, closing at RMB 70.10 per share, a 37.78% increase over the issue price, with a market capitalization of RMB 39.2 billion.

Huaxia Eye reported total revenue of RMB 3.064 billion and net profit of RMB 454 million in 2021. In terms of revenue scale, Huaxia Eye is the second-largest ophthalmic chain group, trailing only Aier Eye Hospital. Meanwhile, Huaxia Eye became the third ophthalmic chain institution to list on China’s A-share market in 2022. After nearly two decades of accumulation, ophthalmic chain groups are entering a harvest period.

An examination of the revenue structures and development histories of various companies reveals that refractive surgery and cataract programs dominate. Driven by market demand and policy guidance, institutions—including Huaxia Eye—are accelerating their efforts to identify new growth drivers.

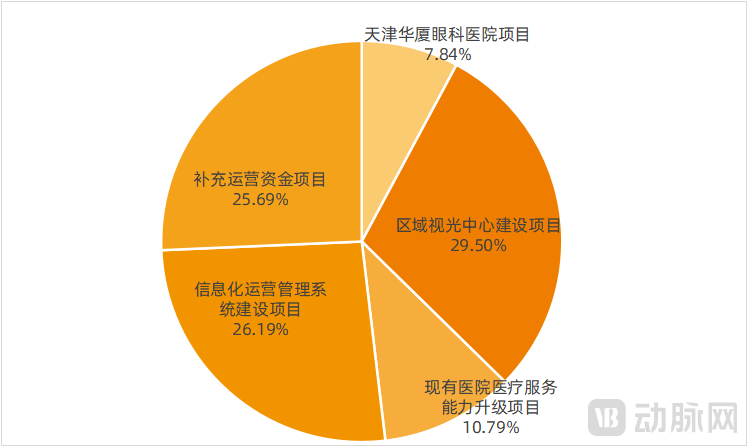

Huaxia Eye plans to invest RMB 779 million from the funds raised in this public offering into five major projects, including ophthalmic hospitals, optometry centers, and information system upgrades. Among these, RMB 230 million is earmarked for the regional optometry center construction project, accounting for 29.50% of the total planned investment—the highest proportion among the five projects—highlighting Huaxia Eye’s strong emphasis on optometry services.

Proportion of Raised Funds Allocated to Major Projects by Huaxia Eye, Source: Huaxia Eye Prospectus

Currently, the optometry centers under Huaxia Eye complement its eye hospitals, meeting patients’ diverse needs and driving patient referrals to the hospitals. Through the regional optometry center construction project, the company is further expanding its business coverage across China, creating new growth drivers.

In fact, it is not just Huaxia Eye; the ophthalmic services sector has widely made optometric services a key area for expansion. Amid the rising prominence of myopia prevention and control and the increasing diversity of intervention methods, how can optometric services support a new round of growth in ophthalmic services? VCBeat has conducted an analysis on this topic.

In recent years, the optometry services market has experienced rapid growth, as evidenced by the financial data of various publicly listed eye care chains.

According to the prospectus of Huaxia Eye, the company has established a total of 23 optometry centers in cities such as Xiamen, Shanghai, and Jinan, providing medical optometry and glasses-fitting services for patients with refractive errors.

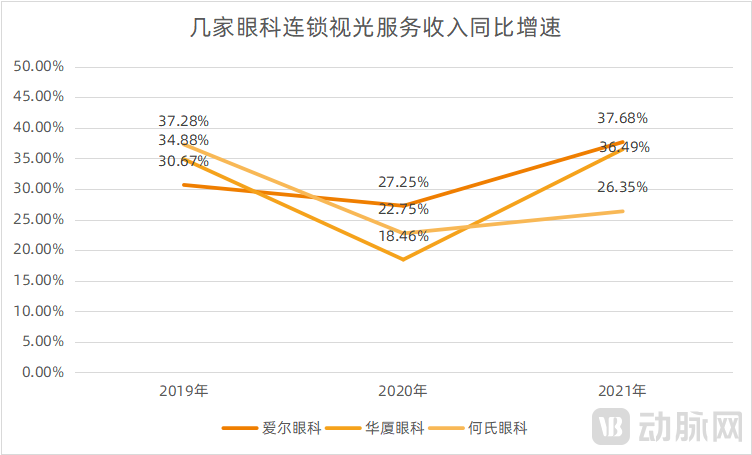

From 2019 to 2021, Huaxia Eye’s revenue from optical dispensing services showed a rapid upward trend, reaching RMB 223 million, RMB 265 million, and RMB 361 million, respectively, with year-on-year growth rates of 34.88%, 18.46%, and 36.49%. During the same period, the year-on-year growth rates for Huaxia Eye’s refractive surgery services were 31.13%, 20.48%, and 31.64%, respectively, indicating that the growth rate of its optometry services was gradually catching up with that of its refractive surgery services.

Other ophthalmic chains also show a similar trend.

Year-on-Year Growth Rate of Optometry Service Revenue for Several Ophthalmology Chains, Data Source: Company Financial Reports or Prospectuses

In 2021, Aier Eye Hospital’s optometry services generated RMB 3.378 billion in revenue, representing a year-on-year increase of 37.68%. Even in 2020, amid the impact of the pandemic, it achieved RMB 2.454 billion in revenue, a year-on-year growth of 27.15%. Aier Eye Hospital had long since begun establishing optometry outpatient departments (clinics) as an integral component of its tiered diagnosis and treatment network.

Aier Eye Hospital has also intensified its efforts in developing optometry services, for example, by increasing the sales proportion of high-unit-price optometry products and focusing on promoting products such as orthokeratology lenses, which drove the growth of optometry service revenue and average unit price. In 2020 and 2021, Aier Eye Hospital's optometry services grew by 12.83% and 34.35% year-on-year, respectively.

Among several listed ophthalmic chain institutions, He Eye Specialist Hospital places particular emphasis on optometry services. The company has extensively established primary eye care facilities, including optometry dispensing outlets and clinics, offering basic ophthalmic medical services such as eye health monitoring, diagnosis and treatment of common eye diseases, and optical correction of refractive errors. In 2020 and 2021, He Eye Specialist Hospital’s optometry service revenue maintained stable year-on-year growth rates of 26.35% and 22.75%, respectively.

The proportion of optometry service revenue to total revenue among listed companies has also been gradually increasing, currently reaching 10%-30% for the industry as a whole; among them, He Eye Specialist Hospital's optometry service revenue accounts for approximately 30% of its total revenue, the highest figure among several companies.

Accelerating the Expansion of Optometry Services: A Mandatory Choice for Listed Eye Care Chains

Currently, listed ophthalmic chain groups primarily adopt three models for deploying optometry services: first, in-house optometry clinics, optometry centers, or medical optometry and dispensing centers; second, off-site optometry clinics or practices, which are required to obtain a Medical Institution Practice License; and third, off-site optometry centers staffed with professionals such as optometrists. The term “optometry service institutions” used in this article mainly refers to off-site optometry clinics and optometry centers.

Building on their historical performance growth, listed ophthalmology chains continue to accelerate the establishment of new optometry service institutions.

After investing RMB 230 million in the construction of regional optometry centers, Huaxia Eye plans to establish 200 new directly operated optometry stores across China, offering medical optometry services to better compete in the optometry services market.

In 2022, He Eye Specialist Hospital prepared to launch five new optometry clinic projects, involving both new establishments and renovations/expansions, within Liaoning Province, and initiated the construction of two optometry clinics in the Chengdu-Chongqing region. He Eye Specialist Hospital has implemented a nationwide layout based on its “1+N” strategy, wherein one He Eye Specialist Hospital drives N He Optometry Clinics. This model fosters positive interaction between eye hospitals and optometry clinics, facilitating mutual referrals and patient flow, while simultaneously expanding in the fields of ophthalmic medical services and myopia prevention and control among adolescents.

Furthermore, Puri Eye Hospital is exploring the “1+N (Optometry Outpatient Clinics)” model in select cities as its business model for optometry services. Meanwhile, Aier Eye Hospital is accelerating the deployment of optometry outpatient clinics or facilities within its tiered diagnosis and treatment system for optometry services in the same cities.

Capabilities in diagnosing and treating ocular diseases, performing surgeries, and providing refractive services largely reflect the proficiency of an ophthalmic hospital and directly influence its reputation. These constitute the foundational services that hospitals consistently uphold. Meanwhile, given the broad patient demographic, the increasingly diverse range of optometric products, and the varied approaches to myopia prevention and control, expanding optometry services has become an imperative for ophthalmic hospital chains.

With Supply Chain Advantages, Upstream Companies Are Eager to Expand into Vision Care Services

Moreover, upstream companies in the optometry sector are also expanding their businesses into service-oriented areas.

In 2022, the third-quarter report released by Autek China showed that the company achieved a revenue of RMB 1.211 billion in the first three quarters, representing a year-on-year increase of 21.58%. The main reason for the performance growth was that the application of its core product, orthokeratology lenses, was on an upward trend, with continued increases in product sales and revenue from marketing service terminals.

Ophthalmic hospitals and optometry service outlets are key channels for orthokeratology lenses. In addition to selling orthokeratology lenses to these institutions, Autek China is accelerating the deployment of its proprietary optometry centers, transitioning from a manufacturer of optometric products to a comprehensive provider of eye care and optometry services.

In 2021, Autek China disclosed during an investor survey that the company already operated more than 200 optometry endpoints and planned to establish 1,300 optometry centers within three years. Meanwhile, Autek China did not position these optometry centers as exclusive outlets for orthokeratology lenses; rather, it positioned them as professional institutions providing vision correction services. Based on user needs, they offer the most suitable solutions or products, including functional spectacle lenses and vision therapy.

In other words, optometry centers serve not only as sales channels for Autek China’s proprietary products but also as a key component of the company’s ophthalmic and optometric services segment.

As another upstream player in the optometry sector, Aier Medical has also begun expanding into optometric services: Jiongjiong Ophthalmology, in which Aier Medical holds a stake, has commenced operations, with its primary services including myopia prevention and control for adolescents and medical optometry dispensing. Currently, Jiongjiong Ophthalmology has opened nine clinics in Sichuan Province.

Although Aier Medical has not yet established its own optometry centers, nor does it participate in the operations of Jiongjiong Ophthalmology, this still reflects an attempt by upstream optical manufacturers to expand into downstream services.

In addition, a wave of small and medium-sized chain or independent optometry clinics has rapidly emerged in the past two years, becoming a new force in the optometric services market.

Eye Care Chains, Upstream Manufacturers, and Innovative Companies Race to Accelerate Their Market Presence: What Makes the Optometry Services Market So Attractive?

From a macro perspective, market demand is naturally high.According to data from the National Health Commission, in 2020, the overall myopia rate among children and adolescents in China was 52.7%, ranking first globally; specifically, the rate was 14.3% among 6-year-olds, 35.6% among primary school students, 71.1% among junior high school students, and 80.5% among senior high school students, indicating a serious trend of myopia onset at younger ages.

Since children and adolescents are not suitable candidates for refractive surgery, there is a greater need for myopia control methods that are personalized, comfortable, and convenient. Meanwhile, as China’s population ages and educational attainment rises, the demand for presbyopic glasses among the elderly is also growing rapidly.

The macroeconomic environment facing ophthalmic chains is also influenced by policy. Among the services offered by various institutions, diagnosis and treatment items under sub-specialties such as cataracts, fundus diseases, and ocular surface disorders must be settled through medical insurance. Affected by cost-containment policies in medical insurance, the revenue growth for these services has generally slowed down, leading to certain short-term pressures on revenue growth.

As a non-reimbursable service, refractive surgery has long been a key pillar for private eye hospitals and continues to demonstrate growth. Similarly, as an intervention for refractive errors, optometric services do not rely on medical insurance, making them a major focus of expansion for eye care chains.

From the perspective of market structure, optometry service providers, as a business model situated between specialized eye hospitals and traditional optical stores, are better positioned to meet user needs.Optometry service providers are located closer to communities, making it more convenient for users to access services. With the endorsement of medical optometry, they are more likely to gain user trust.

From the perspective of corporate development, optometry service institutions can synergize with eye hospitals, serving as a patient source for refractive surgery projects or the diagnosis and treatment of other ocular diseases.

For example, Huaxia Eye has established multiple optometry centers in core commercial districts across the same city, achieving coverage of key high-traffic areas and maximizing the reach of its optometric services to a broader audience. Meanwhile, these optometry centers provide basic ophthalmic examinations and can refer patients requiring further medical attention to affiliated hospitals.

In He Eye Specialist Hospital’s three-tier eye health medical service model, primary eye care institutions that provide optometric services also have the function of referring patients to higher-level institutions.

It is worth noting that in optometric services, orthokeratology lenses impose stringent requirements on fitting qualifications. Regarding institutional qualifications, the fitting facility must be a medical institution at Level II or above, with ophthalmology included in its scope of diagnosis and treatment, and equipped with corresponding facilities such as examination rooms and fitting rooms. In terms of personnel, physicians must hold an intermediate or senior professional title in ophthalmology, and technicians must hold an intermediate or senior professional technician title; both must complete relevant training and pass the required assessments.

Optometry clinics and vision care centers do not meet the aforementioned qualification requirements. Therefore, in practice, the fitting of orthokeratology lenses by ophthalmic chains is typically conducted within qualified medical institutions, while optometric service providers may engage in the sale of orthokeratology lenses and provide usage consultations. This represents the synergy between the two.

Of course, more critically, optometry services boast a relatively high gross profit margin.According to publicly available data, the gross profit margins for optometry services at Aier Eye Hospital and Huaxia Eye both exceed 50%, while He’s Eye Hospital’s optometry service gross profit margin is also around 50%.

Furthermore, optometry services are not subject to significant regional restrictions, making cross-regional replication relatively easier.In the consumer healthcare sector, regional restrictions pose a significant challenge for chain institutions, as there are substantial variations in medical technology standards, physicians’ practices, and patient care-seeking behaviors across different regions. Consequently, cross-regional replication entails high costs. Optometry services, however, are not subject to such constraints and may even serve as the “vanguard” in the expansion of ophthalmology chains, paving the way for the replication of eye hospitals.

In optometry services, primary revenue streams include sales of lenses and frames, orthokeratology lenses, and care solutions, while the services themselves are provided free of charge or at a nominal fee.

In particular, since orthokeratology (OK) lenses have accelerated their market penetration, they have become a key product for chain eye care providers. The annual cost of a pair of OK lenses, including care solutions, ranges from RMB 10,000 to RMB 20,000, and the lenses need to be replaced periodically based on their service life, which directly increases the average transaction value per customer in optometry services. In 2022, soft contact lenses designed to slow myopia progression in children aged 8–12 at initial fitting were launched in mainland China, with an annual cost of RMB 20,000; these may also become the next prominently recommended product in optometry services.

However, the product-dependent revenue and profit model also has its limitations, as exemplified by the recent widely discussed centralized procurement of orthokeratology lenses.

Recently, the Hebei Provincial Healthcare Security Administration included orthokeratology lenses in its centralized procurement list and initiated the information submission process, with the Sanming Procurement Alliance subsequently following suit. To date, no further definitive details regarding this round of centralized procurement have been released; however, it has prompted reflection within the optometry service sector: If centralized procurement is implemented on a large scale, will private institutions still retain a price advantage over public ones? And if private medical institutions participate in centralized procurement, what level of profits can they expect to achieve?

If the answers to the above questions are all pessimistic, how should optometric services in the private sector respond?

First, orthokeratology lenses have a large potential user base, primarily comprising children and adolescents. Drawing on policy orientations in the education sector, including such products in centralized volume-based procurement would indeed carry specific social significance. As for other optometric products, some exhibit a high degree of homogenization. These factors necessitate that optometric service institutions enhance their medical technologies and service capabilities, as well as diversify their service offerings, including improving physicians’ diagnostic and treatment competencies and the professionalism of optometrists.

For users, glasses are needed as a myopia intervention tool, but more importantly, personalized optometric correction, visual training, and eye health maintenance solutions are required to maintain good visual status in daily life.

Only with high-quality solutions can service providers have the confidence to set service fees and break away from reliance on a single revenue stream.

Secondly, accelerate digital upgrading. Digitalization can help optometry institutions extend services to users' homes, increase touchpoints with users, and enhance the convenience of accessing services.

Meanwhile, optometric services exhibit a high degree of compatibility with digital therapeutics. According to the "2022 Digital Therapeutics Industry Research Report" by VCBeat’s Eggshell Research Institute, ophthalmic digital therapeutics represent the most mature niche segment in China: characterized by clear mechanisms of action, relatively straightforward implementation methods, and well-defined therapeutic outcomes, with 12 products having received regulatory approval. Internationally, ophthalmic digital therapeutics have also gained significant momentum over the past five years. Companies in this sector are primarily focused on innovative product development for conditions such as amblyopia, strabismus, and myopia, particularly by integrating gamification into visual training to enhance treatment adherence.

Compared with technology companies, optometry service institutions are closer to users’ usage scenarios, have a deeper understanding of user needs, and possess richer professional service experience. These institutions may also serve as delivery channels for digital therapeutics. Therefore, their involvement in the research and development, promotion, and application of digital therapeutics can drive diversification of products and services within these institutions.

Finally, unlock the value of eye health data within a compliant framework. Optometry service providers are widely distributed; in addition to providing vision correction and eyewear dispensing services, some also offer basic screening, diagnosis, and treatment for ocular diseases. For ophthalmology chain institutions, they also serve as patient acquisition channels.

Eye health data accumulated by optometric service institutions can be leveraged through AI and big data analytics to unlock value for applications such as scientific research and personalized diagnosis and treatment services.

In summary, whether viewed from the perspective of myopia prevention and control among children and adolescents or the visual needs arising from an aging population, the vast market potential for optometric services is undeniable. However, the objective existence of market pain points does not imply that there are already sufficient high-quality products or services to meet these needs. In the future, both listed companies and startups offering optometric services must build their products and services based on users’ actual needs and aligned with their corporate social value, thereby continuously strengthening their competitiveness.