Odin Health: Pioneering the $10B+ Healthcare Integration Market with Forward-Looking Architecture

Actual Construction Requirements: Medical Institutions Are Gradually Entering a New Phase of Application System Integration and Data Interconnectivity

The development of healthcare informatization has evolved from an early focus on financial management, to a core emphasis on physician orders and medical records, and further to the emergence of clinical applications centered on data integration and utilization. It is now progressively entering a phase characterized by data-driven, integrated, intelligent, and ecosystem-based applications that enable cross-system and cross-institutional interoperability—a long-term and sustained process.

Under new business models such as medical consortia/alliances, hospital groups, and internet-based healthcare, the cross-institutional application of multiple systems, along with the demand for data integration driven by big data computing, operational management, business intelligence (BI), and artificial intelligence (AI), has placed higher and more stringent requirements on the real-time interaction, stability, and load capacity of integration middleware. Integration middleware has also garnered increasing attention from healthcare institutions, evolving from its original role as an auxiliary tool for system integration"Lubricant", becoming responsible for the flow of business data between the hospital's core systems“Aorta”。

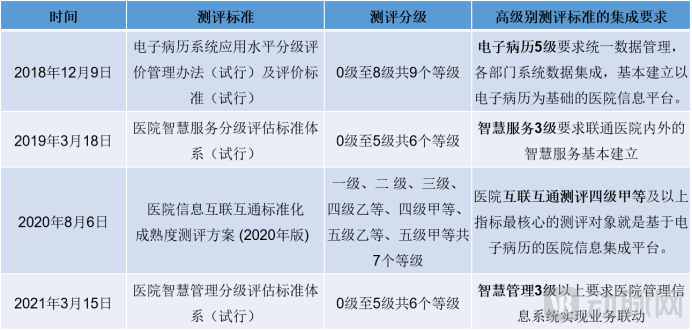

Policy Support Clarified: Frequent Release of Assessment Standards for Interconnectivity and Electronic Medical Records Further Promotes Integrated Healthcare Informatics Construction

Integration and data interoperability technologies will serve as the core technologies in the current stage of healthcare informatization development. This is clearly reflected in national policies, including those governing interconnectivity, electronic medical records (EMR), smart services, and smart management assessments. In particular, the high-level requirements of these assessments explicitly specify standards and requirements for integration technologies, underscoring their critical importance. The increasing frequency of policy releases further indicates that the Chinese government will place greater emphasis, attention, and support on the integrated construction of healthcare informatization in the future.

Compilation of Evaluation Standards for Medical Integration

Source: National Health Commission | Compiled by Odin Health

According to a report by VCBeat Research, the construction cost of an integration platform alone for a hospital ranges from RMB 2 million to 3 million. The integration platform is typically centered on data exchange components (such as an integration engine), which account for approximately 15%–20% of the total construction cost, and is supplemented by a Clinical Data Repository (CDR), master data management, Enterprise Master Patient Index (EMPI), unified authentication, patient portals, and platform management systems. For healthcare institutions aiming to build a relatively comprehensive hospital information system framework that includes both an integration platform and a Clinical Data Center, even secondary hospitals would need to invest around RMB 5 million, while the construction costs for tertiary hospitals exceed RMB 10 million.

Software Prices of Subsystems at Each Stage of Information System Development

Image source: VCBeat Eggshell Research Institute

Meanwhile, according to the number of medical institutions published by the National Health Commission at the end of 2021, there were more than 3,200 tertiary hospitals and over 10,000 secondary hospitals in 2021. However, CHIMA’s survey indicates that fewer than 50% of secondary hospitals and above in China possess data integration capabilities. Even after excluding the nearly 600 tertiary hospitals that had already passed the Interconnectivity Maturity Assessment before 2021, there remain more than 2,600 tertiary hospitals and over half of secondary hospitals with demands for data integration construction. This reveals that the market for integration engines still holds significant potential.

Number of Medical and Health Institutions Nationwide at the End of 2021

Source: National Health Commission; Compiled by Odin Health

In addition to the construction of hospital integration platforms, multi-system cross-institutional applications under new business paradigms—such as medical consortia/alliances, regional healthcare, hospital groups, and internet-based healthcare—as well as the development of business and data middle platforms, and the demand for data integration driven by big data computing, operational management, BI, and AI, all require the support of integration technologies. As these business models mature, the market size for data integration and interoperability middleware will continue to expand.

The following is an estimate of the market size for medical integration based on preliminary research:

1. Regional Health Informatics Construction

Generally, the cost of integrating middleware for provincial-level platform construction is RMB 1.2 million, nearly RMB 1 million for prefecture-level cities, and RMB 300,000–600,000 for county-level platforms. China needs to build 30 provincial-level platforms (excluding Hong Kong, Macao, and Taiwan), approximately 280 prefecture-level platforms, and around 2,000 county-level platforms, resulting in a total market size of approximately RMB 1.5 billion upon full completion.

2. Hospital Information Technology Infrastructure

The construction of integration middleware for tertiary hospitals costs between 600,000 and 800,000 yuan, while for secondary hospitals it ranges from 300,000 to 600,000 yuan. Given the current demand for data exchange integration among the remaining 2,600 tertiary hospitals in China and 50% of secondary hospitals (i.e., 5,000 facilities), the total addressable market for full implementation is approximately 4.5 billion yuan.

3. New Businesses and Technologies Emerging from the Integration of Healthcare with “Cloud Computing, Big Data, IoT, Mobile Internet, and AI”

● Market Size of China's Smart Healthcare Industry: According to data from the China Business Industry Research Institute, the market size reached RMB 221.6 billion in 2020, with a projected growth rate of 33%.

● Internet Hospital Development: The number of internet hospitals in China increased by nearly 1,000 over the five-year period from 2015 to 2020, entering a phase of steady growth in 2021. According to data from iiMedia Research, the market size of China’s mobile medical health sector was projected to reach RMB 63.55 billion in 2021 and is expected to hit RMB 83.96 billion by 2024.

● Medical AI: Statistical data indicate that the market size of China's medical artificial intelligence industry reached RMB 26.5 billion in 2020, representing a year-on-year increase of 46.41% compared to 2019. The market size is projected to reach RMB 140 billion by 2027.

An integrated statistical analysis of the aforementioned information reveals that the market for data integration and interoperability middleware still holds “tens of billions” in potential.

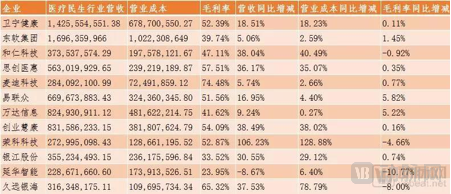

As a supplier of core middleware components for integration platforms, no fewer than half of the top 12 listed healthcare IT vendors in China by revenue have adopted Odin Health’s engine products. Its products are also the designated integration engines used by Winning Health and B-Soft, two HIT enterprises listed on the ChiNext board.

Ranking of Listed Companies Related to Healthcare Informatics in April 2019

Image source: VCBeat

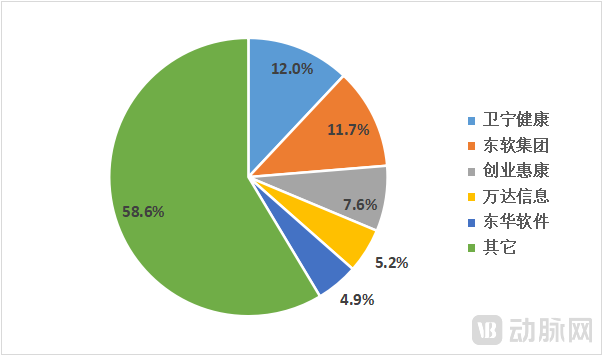

According to Frost & Sullivan data, the top five players in China’s healthcare IT market by market share in 2019 were Winning Health (12.0%), Neusoft Group (11.7%), B-Soft (7.6%), Wonders Information (5.2%), and DHC Software (4.9%). Among these, three HIT vendors maintain close partnerships with Odin Health. Currently, half of the new customers building integrated platforms prefer to use the Odin Engine as the core data integration component for their new healthcare integration platforms.

2019 Market Share of China's Healthcare IT Industry

Data Source: Frost & Sullivan, compiled by Odin Health

Meanwhile, Odin has also established partnerships with several major domestic enterprises, including China Resources Healthcare (a wholly-owned subsidiary of China Resources Group) and China Telecom Wanwei (a wholly-owned subsidiary of China Telecom), to further expand its market presence.

Abroad, Odin has also garnered favor from numerous Fortune 500 companies.

Furthermore, Odin maintains close collaborative relationships with numerous internationally renowned enterprises and has earned the favor of Fortune 500 companies. For instance, Odin signed an agreement with a Fortune 500 medical device company to become its global supplier. Additionally, Odin has accumulated many years of cooperative testing experience with Intel, and Intel’s official website has published the “White Paper on the Optimized Solution for the ODIN Engine All-Scenario Integrated Cluster Edition Based on the 3rd Generation Intel® Xeon® HCI Platform.”

Odin NeXT: A High-Concurrency, Highly Available “Quasi-Endgame” Cloud-Native Architecture

With the application of digital technologies such as cloud computing, the Internet, and 5G in the healthcare sector, healthcare informatization is evolving from a closed internal system into a socialized ecosystem. The integration of numerous new services and technologies will lead to a significant increase in the volume of systems connected to future hospital and regional information platforms, as well as in the amount of services provided and data generated, resulting in high service concurrency. These developments demand high real-time performance and continuous availability, while business requirements become increasingly complex and dynamic. Consequently, traditional approaches to healthcare informatization integration are facing mounting challenges.

Odin has long been dedicated to innovation in integration technology and keenly recognized the changes that the aforementioned trends might bring to this field. In response, it undertook long-term research and development specifically targeting such ultra-large-scale integration demands, investing substantial capital to overcome technical challenges. As a result, in mid-2019, Odin NeXT (New generation eXchange Technology), a distributed cloud-native platform specially designed for ultra-large-scale data centers and large-scale cloud-based application scenarios, was officially launched.

As the “quasi-final” form of the integration platform, Odin NeXT will provide “ultimate” assurance for large-scale data interaction and integration services on the cloud, including significantly improved resource utilization through fine-grained resource allocation, millisecond-level response times after containerized distributed deployment, and enhanced horizontal scalability to meet high-concurrency data processing demands at the scale of tens of thousands per second.

Odin NeXT Addresses the Needs of "National-Level" Large-Scale Project Scenarios

Odin NeXT’s capabilities have been comprehensively validated in large-scale “national-level” projects overseas. In May 2021, ALEX (Application Layer EXchange), billed as the “world’s first primary care data interoperability platform,” was officially launched nationwide in New Zealand, covering 90% of the country’s primary care data. As its core data exchange middleware deployed within Microsoft’s Azure cloud environment, Odin NeXT provides the ALEX platform with high-concurrency, low-latency, highly stable, and end-to-end integrated scalability for large-scale real-time computing.

The rapid development of the healthcare informatics industry, coupled with the frequent release of relevant policies and the continuous emergence of business needs, is injecting new vitality into the healthcare integration market, which holds potential valued at tens of billions. As forward-thinking concepts and various innovative technologies achieve successful implementation and gain customer recognition in numerous cases both domestically and internationally, Odin, as a pioneer, has already “broken new ground” in addressing the challenges of integration requirements characterized by ultra-large scale and ultra-high concurrency.

Moreover, the Odin engine meets integration needs not only in the healthcare IT sector but also in other industries, including supporting a super-large Grade A tertiary hospital in building its financial middle platform. Therefore, Odin is actively seeking strategic partners to further expand into both healthcare and non-healthcare markets, thereby providing diversified support for data integration services.