Leading Oral Healthcare Provider Partners with Digital Management Platform to Empower Small and Medium-Sized Dental Clinics

ARRAI

Oral Healthcare Service Provider

The “DSO model,” specifically highlighted in ARRAI’s prospectus, has officially been unveiled.

Recently, ARRAI disclosed a partnership announcement on the Hong Kong Stock Exchange, unveiling its joint digital DSO (DDSO) initiative, “FRIDAY,” in collaboration with Jia Wosi. Leveraging ARRAI’s more than two decades of industry expertise and Jia Wosi’s digital capabilities, the project aims to empower grassroots-level, physician-founded small and medium-sized single-location dental clinics or small dental chains by decentralizing clinical technologies, standardizing service workflows, and refining management decision-making.

According to ARRAI and Jiawosi, although a few large national chain brands have emerged in China’s dental healthcare services market in recent years, standalone dental clinics and small dental chain institutions will remain the primary participants in the domestic market over the medium term. Consequently, China’s dental healthcare services market will continue to be characterized by a low chain penetration rate among large players and a fragmented landscape dominated by small-scale operators.

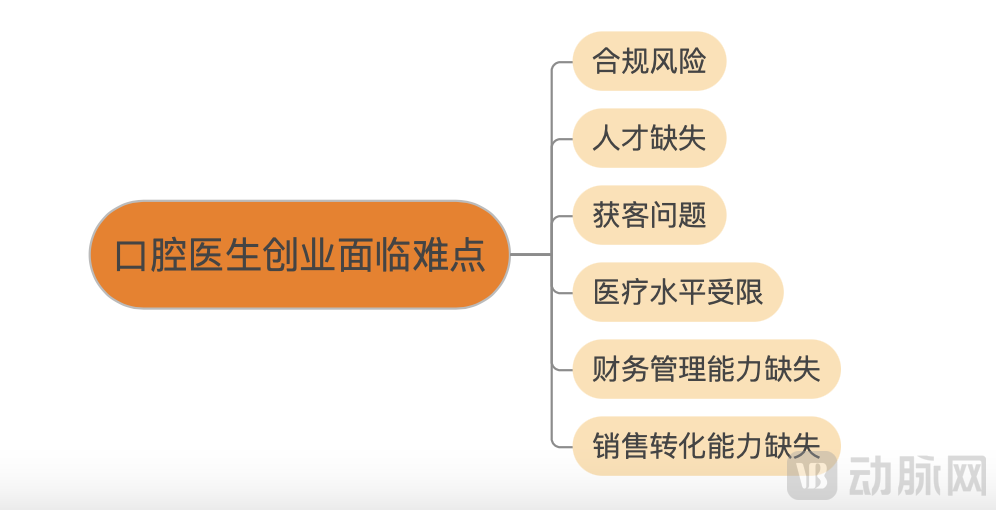

However, single-practice clinics and small chain institutions, which account for "half of the market" in China's dental medical services sector,Its development has been hindered by pain points such as compliance risks, talent shortages, difficulties in customer acquisition and traffic generation, slow improvement in medical standards, and a lack of financial management and sales conversion capabilities.

andAs the first listed company among mid-to-high-end dental chains in China, ARRAI not only ranks first in market share within the high-end private dental medical services sector but also stands among the top in total revenue across the entire domestic private dental medical services market.(Data source: Frost & Sullivan, 2020 data) Its more than two decades of accumulated experience in medical technology, operational management, and customer service within the oral healthcare services market clearly offer valuable insights for other clinics and institutions in the industry.

As for the other participant in the collaboration—Jiawosi initially entered the market through B2B supply chain solutions and SaaS for the dental industry, later expanding its service offerings to include procurement and inventory management, dentist education and training, and patient acquisition training. It has gradually evolved from a supply chain platform into a comprehensive digital management service platform for dentistry. In addition to providing the FRIDAY project with robust supply chain and digital capabilities, Jiawosi has also created greater opportunities for reaching more grassroots clinics and institutions.

When did the domestic dental medical service industry start to boom? And when did it begin to gradually return to rationality?

In a previous interview between VCBeat and Zou Qifang, founder of ARRAI Group, he revealed to VCBeat two major turning points in the history of China’s private dental services industry. First, the liberalization of regulations on medical institutions in 2000 spurred the growth of the domestic private dental services sector, leading to the emergence of numerous private dental clinics. Second, in 2019, China’s per capita GDP and per capita GNP both surpassed US$10,000, bringing public demand for oral health to a tipping point and ushering the country’s dental medical services industry into a golden age of development.

Data serves as a visual representation of market conditions. According to a report by Frost & Sullivan, the size of China's private dental medical service market grew from RMB 43.3 billion in 2015 to RMB 83.1 billion in 2020, with a compound annual growth rate (CAGR) of 13.9%. Within this sector, the high-end private dental medical service market expanded from RMB 1.3 billion to RMB 2.6 billion during the same period, registering a CAGR of 15.2%.

As the market size expands at a rapid pace, the number of private dental hospitals in China has also been on the rise. According to the Health Statistics Yearbook, the number of private dental hospitals in China increased from 103 in 2007 to 723 in 2019, representing a more than sevenfold growth.

Meanwhile, China’s private dental care services market, currently in its golden age of development, has not only achieved rapid growth in market size and a continuous rise in the number of institutions but also embraced a key trend: chain operations. National and regional dental chains, such as Topchoice Medical, ARRAI, and Delun Dental, have entered a phase of rapid expansion.

Indeed, although a number of large private dental chain organizations with strong capabilities and rapid growth momentum have emerged in China’s dental care services market, single-practice clinics and small chains will remain the primary participants in the domestic market over the medium term.

There are two primary reasons for this. First, large dental chain organizations have achieved some success in addressing challenges related to talent acquisition and standardization inherent in chain expansion, but these solutions remain in the exploratory stage. Second, due to the low barriers to entry for establishing dental clinics, it is common practice within the industry for individual dentists to operate solo practices or for small groups of two to four dentists to form partnerships and open small clinics.

However, the growth of both large dental chains and individual or small-chain clinics appears to have slowed in recent years. In the words of Zou Jin, founder of Jia Wosi, this marks a return to rationality.

Some attribute the underlying reasons to the COVID-19 pandemic. Indeed, under the impact of the pandemic, the expansion pace of large dental chain institutions has slowed down, and a large number of small and medium-sized dental clinics have either shut down or are on the verge of closure.But in Zou Jin’s view, “the pandemic was merely a catalyst. The true root cause is that the hidden dangers stemming from the industry’s past extensive growth model have all come to light.”

Zou Jin attributes the past boom in the industry to two main factors: First, there was a severe shortage of supply capacity in the face of the surge in oral health demand following rapid economic growth, and the hidden business opportunities attracted a large number of enterprises to enter the market. Second, driven by capital, some companies adopted short-sighted strategies for development, namely fierce competition for public-domain traffic, with an excessive focus on acquiring new patients and closing deals for high-ticket items.

To this day, facing the still-growing oral healthcare services market, Zou Jin continues to believe that there remains a significant gap between supply and demand in the industry—“the entire sector is far from reaching full competition.”

On one hand, the lack of full competition in the industry indicates that significant market opportunities remain; on the other hand, as the sector transitions from extensive growth to a more rational development model, enterprises in China’s dental medical services industry—whether large national chains, independent clinics, or small and medium-sized chains—are all facing varying degrees of developmental challenges.

Among these, physician-founded clinics or small chain practices often require third-party support in operational management—namely, Dental Support Organizations (DSOs)—due to the specific characteristics of their founding entities.

DSO is a general term for operational management organizations or enterprises that provide non-clinical business support services to dentists and clinics. It primarily empowers clinics with non-clinical operations such as operational management, finance, legal compliance, and training, enabling dentists to devote more energy to clinical work.

DSOs originated in the United States and have experienced rapid growth in the U.S. market. According to a report from April last year, there are now more than 10 DSO organizations in the United States with over 200 affiliated clinics each, among which Heartland Dental has scaled to operate more than 1,600 dental practices. Drawing on international experience, some domestic companies have also embarked on the path of localizing the DSO model in China, including Joyous and ARRAI.

Both parties collaborating on the FRIDAY project are highly prominent.

Let’s first look at Jiavos. This is a young company founded in 2016. Although its founder, Zou Jin, is also quite young, he graduated from the Wharton School of the University of Pennsylvania, one of the top three academic institutions globally. He previously served as the Head of All-Asia Supply Chain for Ann Taylor, a well-known publicly listed U.S. company, where he was responsible for global procurement and e-commerce distribution in North America.

Young entrepreneurs and their nascent startups are aiming to tackle a critical issue that has long constrained the industry’s development—the supply chain system.

The root cause lies in the vast variety of dental consumables contrasted with the relatively low demand from individual dental clinics. Amidst this “supply-demand mismatch,” dental clinics have seen their bargaining power within the supply chain weakened. This has not only given rise to multiple layers of distributors but also triggered a series of issues, such as opaque pricing and forced increases in purchase volumes that indirectly raise economic costs.

Zou Jin’s initial expectation for Jovision was to leverage the internet as a platform and build a transparent, convenient, and effective material management system centered on the supply chain, integrating both upstream and downstream industries.

To date, through the efforts of Zou Jin and the members of JIAWOsi,Jiawosi has indeed achieved remarkable results—serving over 50,000 registered medical institutions with a material information database comprising 3,500 suppliers, more than 50,000 specifications, and nearly 1,000 brands.

It was precisely through communication and collaboration with more than 50,000 dental clinics and small-to-medium-sized dental chain institutions that Jawors realized that, for entrepreneurship in the dentist-led oral healthcare services industry, supply chain management is indeed a core issue, but only one among many other critical challenges.

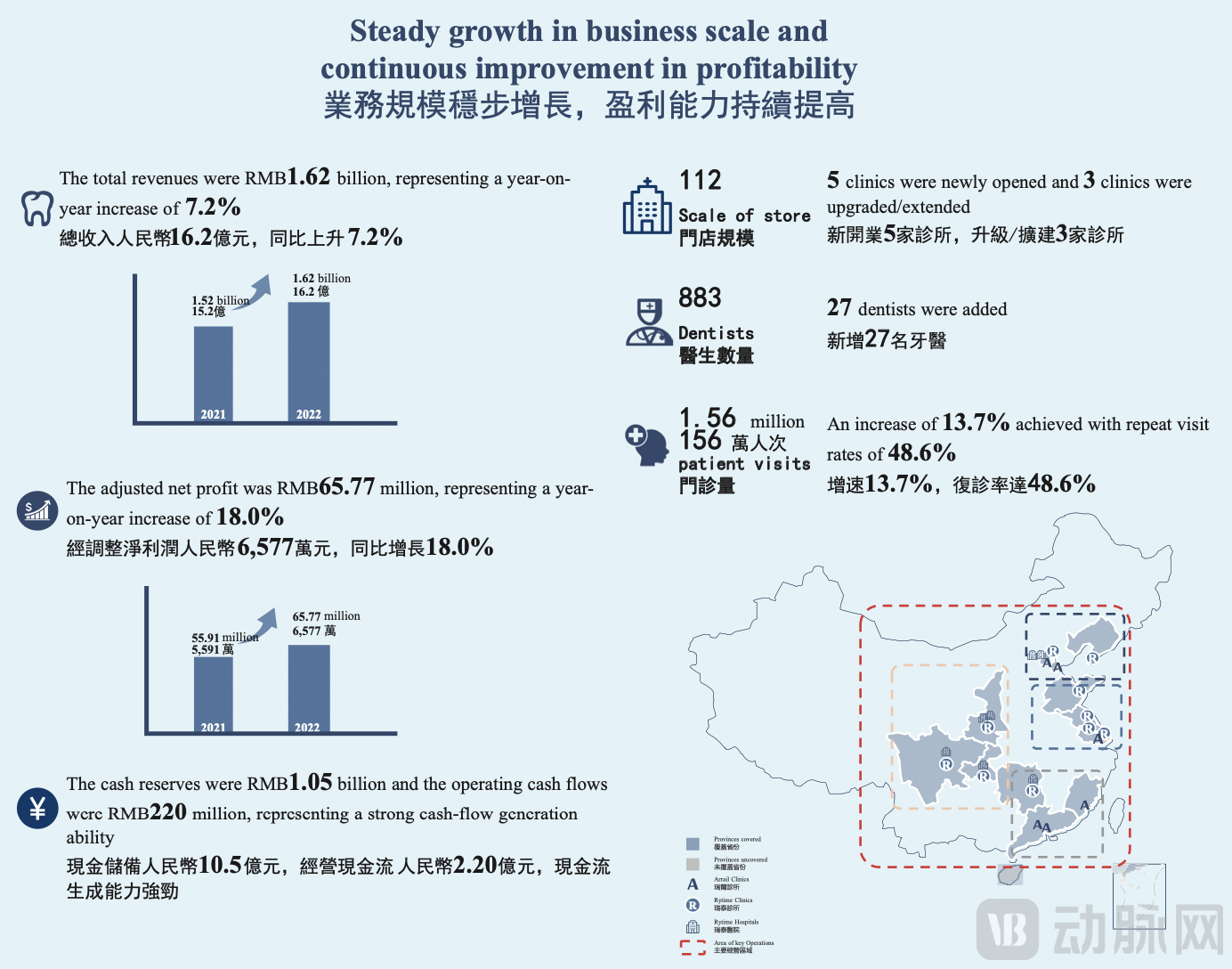

And the other party to the collaboration—ARRAI, as the first listed company in China’s mid-to-high-end dental chain sector, owned 105 dental clinics and 7 hospitals across 15 cities in China, along with 883 experienced dentists, achieving a 7.2% revenue growth by March 31, 2022, underscoring its significant industry influence. (Source: ARRAI Annual Report 2021/2022)

(Image source: ARRAI 2021/2022 Annual Report)

More importantly, as one of the earliest dental service chains in China to explore the oral healthcare market and achieve remarkable success, ARRAI not only possesses a deep understanding of the development trajectory, challenges, and trends of China’s domestic oral healthcare services market, but has also accumulated increasingly profound expertise in medical technology and business management through overcoming numerous obstacles and navigating complex challenges.

Remarkably, since its founding in 1999, ARRAI has never sought to monopolize the industry; instead, it has maintained an open attitude, sharing its successful experiences with the sector.

So, when two leaders in their respective fields come together, what kind of empowerment will they bring to physician entrepreneurs in the industry?

According to Zou Jin,The FRIDAY project empowers dentist-founded dental clinics and small-to-medium-sized dental chains primarily in three aspects: decentralization of medical technology, standardization of service processes, and refinement of management decision-making.

First, the FRIDAY digital healthcare platform not only features over 400 cross-functional online courses for primary-care dentists but also leverages ARRAI’s dental medical team to provide remote consultation and support. Specifically, when primary-care dentists encounter clinical or technical challenges, they can seek guidance from ARRAI’s experts through the digital platform.

According to ARRAI’s 2021/2022 annual report, as of March 31, 2022, the group employed a total of 883 dentists, with over 50.1% of its full-time dentists holding master’s degrees or higher. Many of these dentists also hold titles and qualifications such as Attending Physician or Medical Discipline Leader. The dental team has an average of 10.6 years of industry experience after obtaining their professional qualifications.

Not only that,Members of FRIDAY clinics can also audit the weekly case study seminars on complex and refractory conditions regularly convened by ARRAI Group, thereby enhancing their ability to manage such cases. These seminars are primarily moderated by Professor Zhang Jincai, with participation from key medical professionals across the Group’s various locations, providing robust support for clinical diagnosis and treatment.

Secondly, leveraging ARRAI’s 20-plus years of industry expertise and drawing on user service experience across the five touchpoints—“Pre,” “Initial,” “Diagnosis,” “Conclusion,” and “Follow-up”—of its “ArrailCare 5A” service system, FRIDAY will automatically classify customers and treatment complexity at these five touchpoints and push corresponding tasks to the relevant medical and service personnel.

Furthermore,FRIDAY has also established risk stratification for 142 treatment items, ensuring timely intervention by medical experts to manage risks. Furthermore, FRIDAY has standardized care pathways for 448 treatment stages and over 2,000 procedures, along with defining more than 1,300 service task nodes and corresponding scripts. This helps clinics improve service conversion rates while lowering the barrier to entry for practitioners.

Finally,This is also the most critical empowerment—FRIDAY’s “Group Early Insights” BI system comes with over 400 operational metrics at various levels, helping clinics achieve refined operational management.

“Actually,“You can think of FRIDAY as a data repository. Most physicians lack formal business training; they do not know how to interpret data or what metrics to prioritize. Our system serves as the platform that leverages this accumulated data, with the aim of teaching physicians how to interpret and apply it,” explained Zou Jin.

Notably, according to Zou Jin,Once a member clinic meets the prescribed service protocols and over 400 operational metrics, and receives positive user experience feedback, it will obtain official certification from ARRAI. As an additional benefit, the certified clinic will be granted access to ARRAI’s high-quality individual and corporate client base.“This actually creates a positive cycle: the better the service processes and operational metrics are performed, the more high-value customers will be attracted, and the conversion rate will be improved, forming a relatively healthy and sustainable development.”

andWhen VCBeat asked about the most distinctive features of the FRIDAY project, Zou Jin highlighted two key points: market-validated success and an open mindset.

All the empowerment provided by the FRIDAY project stems from the extensive industry experience accumulated over many years by Joywise and ARRAI. With ARRAI’s public listing, this accumulated expertise has been further recognized and validated by the market. Whether it involves training in medical technologies, the 5A service system, or more than 400 operational management indicators, all have been rigorously tested through ARRAI’s internal practices. Now, ARRAI and Joywise will share these market-proven insights with industry peers without reservation, leveraging digital formats. As previously stated, since its inception, ARRAI has never sought to monopolize the industry; rather, its mission has been to deliver higher-quality oral healthcare services to the public and society.

Now in a phase of stable development, ARRAI has moved beyond the stages of self-improvement and internal consolidation. Looking ahead, it will collaborate with multiple stakeholders to enhance the quality and service standards of dental healthcare through greater professional expertise and experience, a more open mindset, and increased sharing of resources, thereby “helping all parties expand the market together.”