Start-up CDMOs Ride the Wave of Strong Demand and Capacity Expansion

CytoNiche

3D Cell Technology Products and Services Provider

Whether new players are entering the market or established ones are transforming and listing on capital markets, the CXO sector has always been in the spotlight.

In recent months, VCBeat has observed that most pharmaceutical companies pursuing initial public offerings (IPOs) have direct or indirect ties to the CXO business.

On August 25 this year, Xuantai Pharmaceutical officially listed on the STAR Market. Its core businesses include high-end generic drugs and formulation CRO services. On October 11, Bide Pharmatech, a branded supplier of drug molecular building blocks, also made its debut on the STAR Market. As molecular building blocks are closely linked to upstream CDMO operations, CDMO has become a key direction for its future transformation. On November 1, Hongbo Medicine officially listed on the ChiNext Board. As a typical small- and medium-sized domestic CXO enterprise that started with active pharmaceutical ingredients (APIs), Hongbo Medicine is now undergoing transformation, which presents both opportunities and challenges.

Meanwhile, a cohort of noteworthy new players has emerged in the CXO sector. Some of these start-up CXO companies were founded on a high baseline, such as Sherpa Biologics, established by the CMC team of Innovent Biologics; others focus on more cutting-edge, niche service segments, such as OliBio, a start-up CDMO specializing in oligonucleotide therapeutics.

However, regardless of their starting point, all players are seeking space for survival and growth, hoping to secure a share in the vast CXO sector.

Over the past two months, Arterial New Medicine has curated a special series on CXO companies, interviewing several distinctive firms in the sector. We have found that despite the seemingly crowded CDMO landscape, new industrial opportunities continue to emerge.

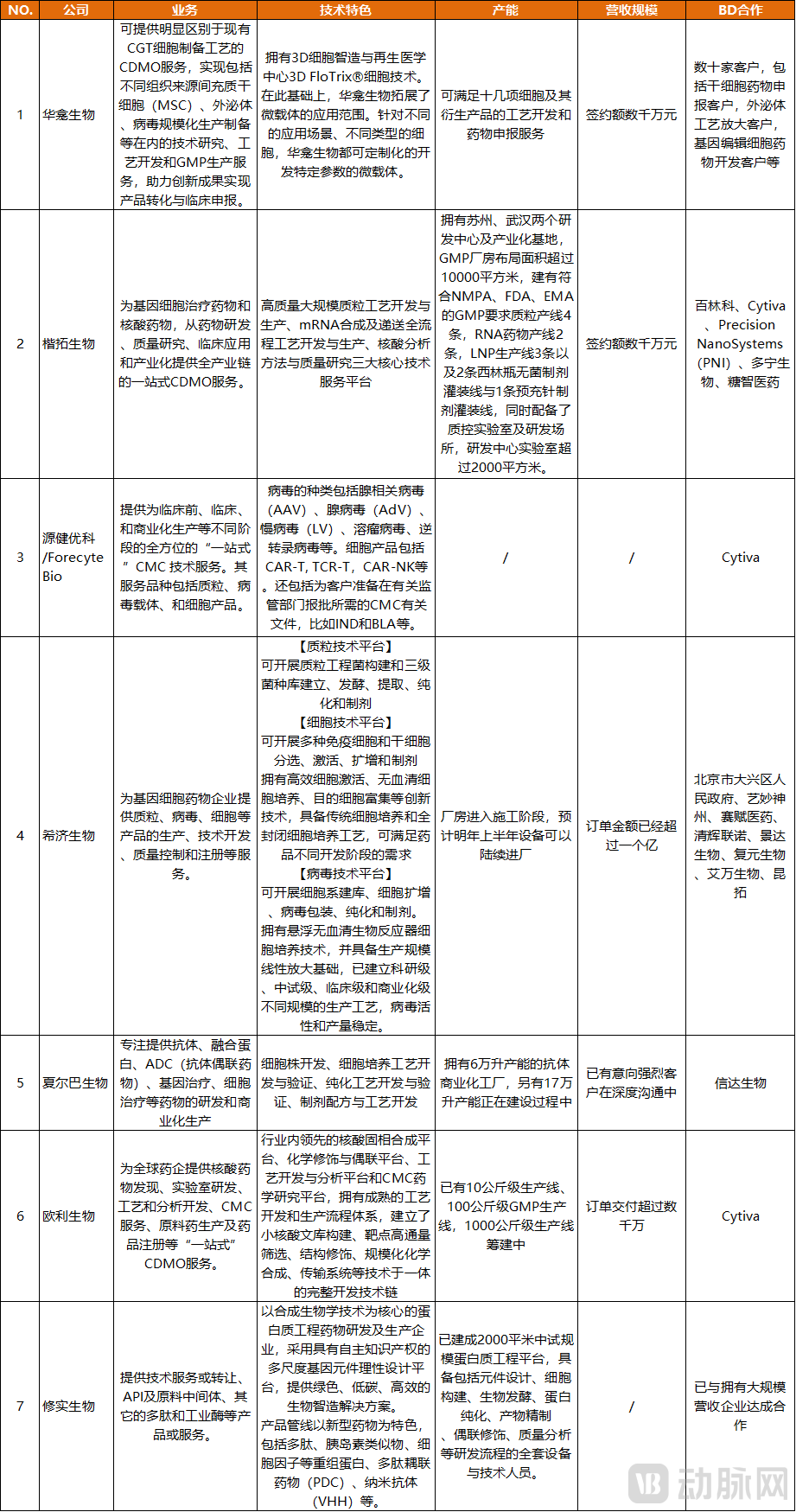

Based on recent interviews and desk research, VBInsight reviews seven representative startup CDMOs founded around 2020, primarily covering the subsectors of cell and gene therapy (CGT), oligonucleotides, and peptides. Examining the current status and technological characteristics of startup CDMOs established in the past two years offers insights into the features of these sectors, their current development stages, and emerging industry trends.

Where Do Start-up CDMOs Come From?

Among the seven companies, while Sherpa Biologics spans multiple fields including antibodies, fusion proteins, cell and gene therapy (CGT), and antibody-drug conjugates (ADCs), the other six startups each focus on specific niche areas. Three of them specialize in CGT. Of the remaining three, Oli Biotech focuses on nucleic acid therapeutics—a sector still pre-commercial production in China; Xiushi Biopharma is dedicated to peptide therapeutics; and Kaituo Biotech has adopted a dual strategy covering both CGT and nucleic acid therapeutics.

From the perspective of their founding teams, these startup CDMOs each have distinct characteristics. Apart from CytoNiche, a typical enterprise spun off from academic research at Tsinghua University, the founding teams of the other six companies primarily hail from universities, CMC departments of large biopharmaceutical firms, or leading CDMO enterprises both in China and abroad.

Among these,Sherpa Biologics and Xiji Biologics are relatively unique in that they both spun out from biotech companies and were established in 2022, reflecting the trend of domestic biotech firms expanding into the CDMO sector.

Sherpa Biosciences spun off the CMC team from Innovent Biologics to form a process development team of over 1,000 members, leveraging the extensive experience in process development and industrialization accumulated during their tenure at Innovent. Lu Xin’an, founder of Xiji Biopharma, is also a co-founder of ImmuneOnco, which began developing novel cell therapy drugs in 2015 and has since grown into a leading enterprise in the CGT sector. This background has equipped Xiji Biopharma with one of the earliest teams in China dedicated to CAR-T novel drug development.

We observed that five CDMO companies have entered different financing stages.. The CGT sector, with its relatively mature technology, has seen the fastest financing progress., CytoNiche, the earliest established company, has entered the Series B stage, while Kaituo Biotechnology and Yuanjian Youke have both completed their Series A financing.

Early-stage CDMO startups in the peptide and nucleic acid drug sector are still in their infancy. Xiushi Biotech’s latest disclosed financing round was the seed round, with its Series A round currently underway and expected to close by the end of 2022; Ouli Biotech has completed its Pre-Series A financing.

CDMO is a capital-intensive industry that relies on government resources for land acquisition, GMP facility construction, and policy support such as investment incentives in industrial parks; therefore, it maintains closer ties with local governments.

Among these financing rounds, local government funds have been prominent players. In CytoNiche’s Series B financing, the China International Capital Corporation Qiyuan National Emerging Industry Venture Capital Guidance Fund drew significant attention. This is China’s first national-level fund dedicated to investing in venture capital funds and enterprises within emerging industries, established with joint investments from the National Development and Reform Commission, the Ministry of Finance, and other social investors. Similarly, among the investors in Kaituo Bioscience’s Series A financing round, we also saw Yuanhe Holdings, a Suzhou-based local fund.

These investments have strengthened the ties between CDMO companies and local industries. CytoNiche has chosen Beijing as the location for its headquarters and production base, while Kaituo Biology has also established a production workshop in Suzhou.

From a geographical perspective, six CDMO companies have chosen to establish their presence in the Yangtze River Delta region. The Yangtze River Delta is a major hub for China’s biopharmaceutical industry,Suzhou, Hangzhou, and Shanghai have emerged as popular site selection choices, only CytoNiche, with a background from Tsinghua University, has placed its headquarters in Beijing.

Furthermore,Single-site facility construction can no longer meet the capacity layout requirements of CDMOs., even start-up CDMOs are directly initiating multi-location expansion; Kaituo Biologics has chosen a dual presence in Suzhou and Wuhan, while Sherpa Biologics has not only established a manufacturing facility in Suzhou but also set up production workshops in Hangzhou.

No Shortage of Orders: Capacity Expansion Remains the Main Theme—Why?

During the interview, VCBeat New Medicine discovered thatMost CDMO startups founded after 2020 need not worry about securing orders, with contract values ranging from tens of millions to over 100 million yuan.Some companies no longer have the capacity to take on new orders, while others have their R&D pipelines essentially fully occupied by CDMO contracts.

Taking Xiji Biotech as an example, the company was established in January this year, began accepting orders in April, and has recently continued to secure new contracts, bringing its revenue scale to nearly RMB 100 million. Currently, its production capacity for the year has been fully utilized, with new capacity under construction.

Securing CDMO orders from large enterprises, anticipating robust cash flow, expanding production capacity, adding R&D equipment, recruiting high-level technical professionals, and gradually penetrating international markets remain the central themes for these startup CDMO companies.

Numerous new opportunities are emerging in the CDMO sector, particularly well-suited for early-stage startups.

Among them, CGT CDMOs are relatively ahead of the curve, with the sector becoming increasingly refined and more opportunities emerging in vertical niche markets.

This is evidenced by the emergence of a new generation of CDMO companies, such as CytoNiche, in 2018. CytoNiche is a typical project resulting from the commercialization of academic scientific and technological achievements. Its proprietary technologies, including microcarrier technology and 3D cell culture process technology, were all derived from technology transfer initiatives at Tsinghua University.

Currently, multinational and domestic CGT CDMO companies predominantly focus on plasmid and viral vector services, while their cell-based service capabilities remain a critical gap needing urgent resolution. CytoNiche emphasizes 3D cell culture processes, exploring how to integrate 3D culture technology across the entire CGT sector and even into the traditional CDMO industry.

Although Xiji Biologics is a CDMO company providing end-to-end services for plasmids, viruses, and cells from investigator-initiated trials (IITs) to commercialization, it also emphasizes its outstanding cell therapy service capabilities. Furthermore, Xiji Biologics has established a differentiated positioning in terms of geographic layout. Currently, most domestic cell and gene therapy (CGT) CDMOs are concentrated in the Yangtze River Delta region, with very few in northern China. Located in the Beijing Daxing Biomedical Industry Base, Xiji Biologics leverages Beijing’s educational and medical resources to expand its operations starting from the northern region.

In the CGT CDMO sector, the growth potential for startups lies in emphasizing their advantages in more specialized niches, whether technical or related to geographic and resource-based service capabilities.

In the field of small nucleic acids, the industrial ecosystem is still in its early stages. “One-stop” CDMO services—covering small nucleic acid drug discovery, process development, CMC services, active pharmaceutical ingredient (API) manufacturing, and drug registration—remain the most sought-after by the market. The domestic small nucleic acid industry will truly flourish only when it can effectively support downstream R&D enterprises in advancing nucleic acid therapeutics into clinical trials and further into commercialization.

Currently, oligonucleotide drugs in China are largely at various stages of pre-commercial production, preclinical development, and clinical research. According to VCBeat New Medicine, corporate demand is primarily concentrated in the range of 10 milligrams to 10 kilograms, which represents a relatively modest capacity requirement compared with small-molecule drugs and peptides. Nevertheless, relevant companies are closely monitoring the progress of oligonucleotide therapeutics. Should any product advance rapidly and show strong potential for entering commercial-scale manufacturing, these companies will expand their production capacity accordingly.

Taking Ouli Biologics as an example, the company entered the nucleic acid drug CDMO sector in 2021, recognizing that while professional nucleic acid CDMOs were relatively scarce in the Chinese market, demand from nucleic acid pharmaceutical companies for CDMO services was continuously expanding. Currently, Ouli Biologics operates five production lines with capacities ranging from 10 milligrams to 100 grams, and by the end of the year, it will have two additional production lines with capacities ranging from 10 grams to 100 kilograms.

Currently, Oli Bio is not only undertaking early-stage orders for nucleic acid drugs but also has two other core business segments: providing primers and probes for IVD companies, and supplying CpG adjuvants for vaccine manufacturers. Since its establishment over a year ago, Oli Bio has fulfilled orders totaling more than RMB 22 million.

The peptide sector is a typical example of a field experiencing a resurgence, with this vitality gradually extending to upstream CDMO businesses.

To reduce costs and mitigate R&D risks, peptide pharmaceutical companies often partner with specialized CRO/CDMO firms in the early stages of development. As a result, while the peptide CDMO sector has a long history, there are relatively few market participants. Among domestic peptide CDMOs, PeptiChem (Zhongtai Shenghua) and Chengdu Sinotech were both established in 2001, Hybio Pharmaceutical in 2003, Ambio Pharmaceuticals in 2005, and Nuotai Bio in 2009, each boasting over a decade, and in some cases more than two decades, of development experience.

With the emergence of multiple “blockbuster” drugs such as semaglutide, the peptide sector is returning to the public spotlight, and peptide drug CDMOs are attracting increased attention. As a wave of innovative peptide companies emerges in China, innovation-driven demand is further stimulating growth in upstream industries.

For example, traditional peptide CDMOs often employ chemical synthesis or classical genetic engineering methods, which generally entail higher costs and lower synthesis efficiency.

Xiushi Biotech is a rare peptide CDMO established in recent years. Founded in late 2020, the company claims to be among the very few startups that effectively leverage synthetic biology technologies to address the challenges of industrial-scale development of peptide drugs. It is reported that Xiushi Biotech has achieved production efficiency 5–10 times higher than that of traditional genetic engineering techniques in its GLP-1 receptor agonist analog drug projects, with gross margins on active pharmaceutical ingredients (APIs) exceeding 85%. Currently, many leading companies in this field are engaged in collaboration discussions with the firm.

Driven by Innovative Products and Technologies, Moving Upstream

After years of development, there is no shortage of CDMO companies in China that offer end-to-end services for drug development and commercialization. Most Chinese CDMOs provide related products and services covering the entire drug development lifecycle. These enterprises excel in establishing drug development systems and handling regulatory submissions, with a significant proportion having prior experience in drug registration before entering the CDMO space.

“In the early stages of industry development, the primary concern was how to develop a drug—specifically, how to successfully advance it from early-stage development through IND approval for clinical trials, and ultimately to commercial-scale manufacturing. In other words, the focus was on establishing an end-to-end drug development pipeline,” Dr. Liu Wei, Co-founder and CEO of CytoNiche, told VCBeat New Pharma. “HoweverAs the industry matures, attention is increasingly focused on every detail of drug development. For example: What are the specific excipients, reagents, equipment, and manufacturing processes required for a drug?”

Driven by innovative products and technologies, moving further upstream represents the most significant growth opportunity for startup CDMOs.

Driven by a product- and technology-oriented business model, emerging CDMOs are also innovating their business models at the business development (BD) level. CytoNiche has stated that, in addition to emerging cell and gene therapy (CGT) pharmaceutical companies adopting its 3D cell culture process to reduce costs and improve efficiency while meeting future commercial production demands, traditional CDMOs can develop and upgrade their entire process workflows based on their existing two-dimensional cell culture platforms, thereby integrating new technologies into the client projects they support.

Avoid competing with traditional CDMOs; instead, export new technologies, with traditional CDMOs also serving as their clients.

In summary, domestic substitution across the upstream ecosystem presents systematic entrepreneurial and investment opportunities, not only in the life sciences tools sector but also in the CDMO track. Lu Xin’an, founder of CytoNiche, pointed out, “When developing gene and cell therapies, we must always consider the development of the entire ecosystem. Even if a company grows successfully or excels in a specific R&D stage, it will still face significant constraints if there are vulnerabilities or chokepoints in the upstream or downstream segments of the ecosystem.”

For most new drugs currently marketed in China, the manufacturing processes, production tools, and raw materials and reagents remain heavily dependent on imports. What are the original Chinese innovations in biomedical tools, products, technologies, and processes? This is a question that the entire industry must answer.