Fluorescence Endoscopy Emerges as a High-Growth Investment Hotspot with Backing from Alibaba and Gree

Stryker

Orthopedic Product Developer

OptoMedic

High-end Optical Medical Device R&D Manufacturer

In the small German town of Tuttlingen, tens of thousands of people are employed in industries directly related to endoscopes. The town has given rise to hundreds of endoscope brands, including Karl Storz, one of the top three global endoscope manufacturers, which originated in Tuttlingen.

In China, Tonglu County is also renowned for its endoscopy industry, hosting multiple endoscope manufacturers. While most domestic medical endoscope producers have established capabilities in the research, development, and manufacturing of low-end medical endoscopes, no globally recognized brands have emerged. Even within the domestic rigid endoscope market, Chinese-made endoscopes maintain a relatively weak market presence, with foreign brands such as Germany’s Karl Storz, Japan’s Olympus, the United States’ Stryker, and Germany’s Wolf commanding an 80–90% market share.

Domestic substitution of endoscopes has long resembled an insurmountable mountain, yet in one niche segment—fluorescence endoscopy—a remarkable turnaround by Chinese manufacturers is unfolding.

Fluorescence endoscopes were introduced in 2015, with the global market entering a phase of rapid growth in 2016. In China, large-scale adoption of fluorescence endoscopes began in 2018. According to Frost & Sullivan’s estimates, the compound annual growth rate (CAGR) for fluorescence endoscopes in China is projected to approach 99.8% over the next three years.

The global fluorescence endoscopy market is dominated by Novadaq, a subsidiary of Stryker. Data from 2019 shows that Novadaq held a 78% share of the global market. However, in the Chinese domestic market, Novadaq’s market share is nearly on par with that of the Chinese manufacturer OptoMedic.

Fluorescence endoscopy has also become a hot spot in the capital market. In the primary market, OptoMedic secured hundreds of millions of yuan in financing in 2021 and received investment from Alibaba in 2022; another company, DPM, completed two rounds of financing this year, with Gree Financial Investment participating in its latest Series B+ round.

In the secondary market, OptoMedic, which manufactures core components of fluorescence endoscopes for Stryker, has a market capitalization exceeding RMB 10 billion on the STAR Market. OptoMedic went public on the STAR Market in 2021 with an IPO price of RMB 35.76 per share, and its current stock price has climbed to over RMB 120 per share.

What factors have driven the past growth of fluorescence endoscopy? How are Chinese manufacturers leveraging fluorescence endoscopes to execute a disruptive market entry? VCBeat (WeChat ID: vcbeat) interviewed multiple industry insiders.

Medical endoscopes are medical devices used to provide physicians with images of internal human anatomical structures during clinical examinations, diagnoses, and treatments. Endoscopes are classified intoRigid Endoscopes (Laparoscopes, Arthroscopes, etc.)and hose-typeEndoscopes (gastroscopes, colonoscopes, etc.)Two Major Types.

Fluorescence endoscopy is a type of rigid endoscopy. Rigid endoscopes are categorized into white-light endoscopes and fluorescence endoscopes based on their operational spectral range. White-light endoscopy generates images based on the visible light spectrum (400–700 nm), depicting the superficial layers of human tissue.

Fluorescence endoscopy operates within a spectral range of 400–900 nm. In addition to providing images of the superficial layers of human tissue, it enables simultaneous fluorescence visualization of subsurface structures, such as the cystic duct, lymphatic vessels, and blood vessels. This capability plays a critical role in achieving precise intraoperative localization and reducing surgical risks.

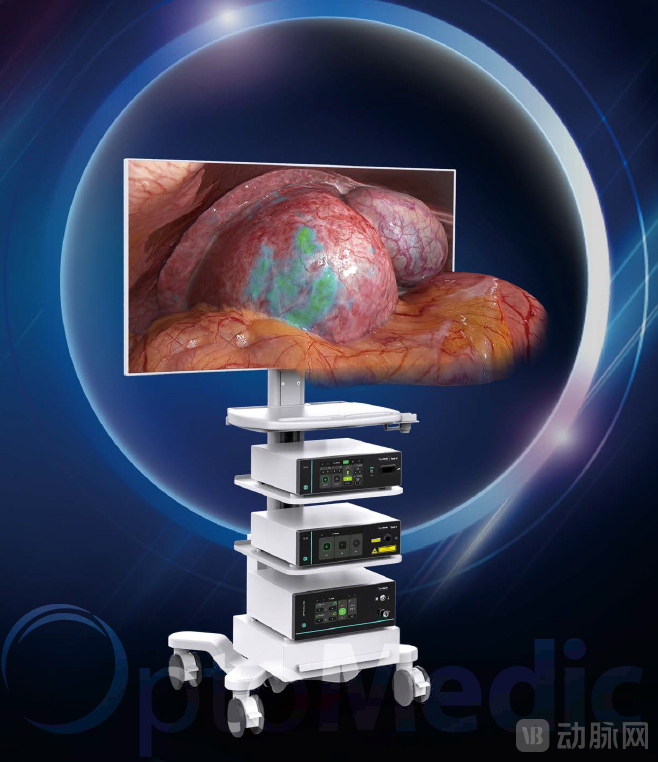

Fluorescence rigid endoscopy employs two imaging modalities: one involves the administration of exogenous photosensitizing dyes, while the other detects lesions or pre-lesional sites that are difficult to visualize by capturing autofluorescence emitted by cells. Prior to surgery, fluorescent contrast agents are administered into the body via various routes. Exogenous photosensitizing dyes can specifically label pathological sites, such as cancers, and emit fluorescence at specific wavelengths. The near-infrared light at specific wavelengths emitted by the fluorescence endoscope’s light source undergoes optical reflection upon binding with specific protein components in the blood. The light is then captured by the laparoscopic objective lens and converted into an electronic signal, thereby generating a contrast-enhanced image.

Fluorescence Endoscopic Imaging

Stryker launched its fluorescence endoscope in 2015, leveraging this technology to reclaim a leading position in the endoscopy field. At the time of the product’s initial release, Stryker’s outlook on the fluorescence endoscope market was not particularly optimistic.

Market response quickly proved Stryker’s predictions wrong. After fluorescence endoscopes were officially launched in 2016, they received widespread acclaim, and market demand surged rapidly. Surgical applications expanded from initial cholecystectomy to include lymph node dissection, tumor resection, and other procedures.

The global fluorescence endoscopy market is experiencing rapid growth. In 2019, the global market size for fluorescence rigid endoscopes reached USD 1.31 billion, accounting for 23% of the total rigid endoscope market that year. According to Frost & Sullivan, the global market size for fluorescence rigid endoscopes is projected to grow to USD 3.87 billion by 2024, expanding at a compound annual growth rate (CAGR) of 24.3%, and will share the market equally with conventional white-light rigid endoscopes.

After receiving positive market feedback for its fluorescence endoscopy systems, Stryker acquired NOVADAQ, a developer of fluorescence imaging technology, for $700 million in July. Following the acquisition, Stryker leveraged NOVADAQ’s Pinpoint platform to expand its product offerings into a broader range of surgical procedures, further solidifying its competitive advantage. With its strategic presence in the fluorescence endoscopy sector, Stryker achieved $1 billion in sales of fluorescence endoscopy systems in 2019, dominating the global market.

In China, during Tsinghua University’s centennial celebrations in 2011, four former classmates with backgrounds in optical instrumentation decided to make their mark in the high-end medical device sector. They subsequently co-founded OptoMedic, laying the groundwork for Chinese-made devices to surpass international competitors in the field of fluorescence endoscopy.

In 2018, a group of domestic companies, including OptoMedic, took the lead over imported brands in obtaining registration certificates for high-definition fluorescence endoscopes in China. They began promoting fluorescence endoscopes in clinical practice. Since the application of fluorescence endoscopy commenced in 2018, more than 20 expert consensus documents related to fluorescence have been published, and the market has experienced rapid growth. Such extensive clinical application and recognition are relatively rare worldwide.

The growth rate of China’s fluorescence endoscopy market has even surpassed that of the global market. According to Frost & Sullivan forecasts, by 2024, total sales of fluorescence rigid endoscope equipment in China will reach RMB 3.52 billion, with a penetration rate of 32%, representing a compound annual growth rate (CAGR) of 99.6% from 2019 to 2024.

What Are the Drivers Behind the Growth of China's Endoscopy Market?

First and foremost, it relies on the rapid growth of minimally invasive surgery in China.In the field of minimally invasive surgery, China’s technical capabilities are at a leading level globally. In 2019, the number of minimally invasive surgical procedures in China reached 11.9 million, and is projected to reach 26 million by 2024. The growth in the volume of minimally invasive surgeries has driven demand for endoscopes and also stimulated growth in the fluorescence endoscopy market.

Secondly, another major driver of the domestic fluorescence endoscopy market is the participation and promotion by Chinese endoscope manufacturers.China’s endoscopic minimally invasive medical device industry has a development history spanning more than 30 years. Although the overall technical level and industrialization progress of the sector still lag behind those of developed countries, a few enterprises have achieved breakthroughs from zero in the high-end market of certain niche segments of medical endoscopy. If the fluorescence endoscopy market were driven solely by imported products, its penetration rate would not have risen rapidly.

In the field of fluorescence endoscopy, Chinese manufacturers have repeatedly achieved leadership. The first domestic registration certificate for a fluorescence endoscope was issued to Suzhou Guoke Meirunda, a Chinese manufacturer, while the first 4K fluorescence endoscope in China was introduced by OptoMedic, another domestic company. The early entry of Chinese manufacturers has also driven the growth of the domestic fluorescence endoscopy market.

Finally, in terms of clinical value advantages, fluorescence endoscopy is widely used in surgical procedures and can directly help surgeons reduce surgical risks.Fluorescence endoscopy can image blood supply, lymphatics, and nerves in specific scenarios, as well as certain tumors. It enables real-time tracking of the lymphatic system, observation of tissue perfusion, and precise localization of tumor boundaries.

The fluorescent endoscopy market is expected to maintain sustained growth in the future.

In recent years, the development of fluorescence endoscopy in the U.S. market has been remarkably rapid. Currently, fluorescence-guided surgeries are predominantly concentrated in abdominal procedures; however, as the medical community gains greater familiarity and proficiency with this technology, its application is gradually expanding from abdominal surgery to other specialties, including urology and gynecology. Fluorescence endoscopy systems integrate both white-light and fluorescence imaging capabilities. This all-in-one design helps reduce the number of devices required in operating rooms, and fluorescence endoscopes are increasingly replacing traditional white-light endoscopes across a broader range of surgical scenarios.

In China, the penetration of fluorescence endoscopes in the primary care market is another major growth highlight. The application of fluorescence endoscopy at the primary care level is expected to significantly reduce the risk of complications associated with surgical techniques. By the end of 2019, approximately 4,400 (18.5%) of the 24,000 hospitals in China were capable of performing minimally invasive surgeries (including 1,400 Grade A tertiary hospitals and 3,000 other hospitals). In the same year, 71% of the 6,146 hospitals in the United States were able to perform minimally invasive surgeries. There is still substantial room for improvement in the penetration rate of minimally invasive surgeries in China.

Domestic companies are also capturing a share of the growth in the fluorescent endoscopy market. OptoMedic has emerged as the leader in this niche segment, surpassing Stryker to claim the top market share in 2021. Haitai New Light reported operating revenue of RMB 340 million for the first three quarters of 2022, a 55% increase from RMB 218 million in the same period of the previous year; its net profit reached RMB 139 million, representing a 52.5% increase from RMB 92 million in the corresponding period last year.

In the high-end endoscopy sector, few domestic companies have managed to capture a significant market share. For new products, physicians tend to trust imported brands more. In the field of high-end medical equipment, minimally invasive laparoscopic surgeries carry extremely high risks; poor product quality can easily lead to surgical complications. Therefore, physicians have exceptionally high standards for the quality of instruments used in laparoscopic procedures. As a result, even low-price strategies adopted by domestic manufacturers fail to break into the high-end market.

Endoscopes integrate multiple technologies, including optics, mechanics, electronics, and computing, requiring a balanced optimization of these diverse technical domains. Fluorescence endoscopes combine two imaging modalities: white-light and fluorescence endoscopy. They demand high-quality white-light imaging as well as accurate and sensitive fluorescence imaging, with the further requirement of fusing these two image types.

How Have Domestic Companies Broken Through This Entrenched Market Perception in the Fluorescence Endoscopy Market?

Ding Yan, Deputy General Manager of OptoMedic, stated: “First, we believe it is only natural that doctors prefer high-performance surgical equipment and place greater trust in imported brands. For domestic companies, appealing to sentiment is meaningless; only by developing products that outperform imported alternatives can they win over the market, rather than leaving users with no choice but to passively accept domestically produced products.”

“In the fluorescence endoscopy market, OptoMedic obtained the registration certificate for its 4K fluorescence endoscope in 2020. This product was launched globally at the same time as imported 4K fluorescence endoscopes; however, the latter have not yet entered the Chinese market, where only high-definition (HD) fluorescence endoscopes that have been available for many years remain. In white-light endoscopy, 4K resolution is significantly superior to HD. This generational difference in products gives domestic brands a distinct advantage.”

OptoMedic 3D Multi-Fluorescence Endoscopic Imaging Platform

Ding Yan also calmly pointed out that this advantage in market access and registration is similarly enjoyed by imported brands in the U.S. and European markets, as Chinese manufacturers also face prolonged timelines when seeking FDA and CE certifications.

“Fluorescence endoscopy offers a favorable window of opportunity for China’s domestic endoscope industry, much like new energy vehicles have done for the automotive sector.”

For Chinese manufacturers to maintain a sustained competitive advantage, they must remain at the technological forefront. At this year’s China International Import Expo (CIIE), Stryker unveiled its next-generation endoscopic solution: the 1688 4K Dual-Fluorescence Intelligent Imaging Platform. With the debut of imported 4K fluorescence endoscopes, in what directions can domestically produced fluorescence endoscopes once again take the lead?

Fluorescence endoscopy is, in essence, still an endoscope.

The primary trend in the development of endoscopy is the advent of ultra-high-definition imaging.Endoscopic imaging has progressed through the standard-definition and high-definition (1080P) eras and is now advancing toward ultra-high-definition (4K) resolution.

The second development trend is the transition from two-dimensional to three-dimensional stereoscopic imaging.In laparoscopic surgery, surgeons typically view two-dimensional images but must think in three dimensions. 3D endoscopes can restore the true three-dimensional stereoscopic surgical field, facilitating the identification of lesions and enabling precise resection and reconstruction. This enhances hand-eye coordination during procedures and significantly improves surgical efficiency. Therefore, the transition from planar to stereoscopic endoscopic imaging represents a major trend.

The third major trend is the integration of endoscopic imaging technologies.Building upon traditional endoscopic technology, novel hybrid endoscopy products have been developed by integrating other imaging modalities, such as ultrasound, optical coherence tomography, fluorescence, and confocal microscopy. In recent years, fluorescence laparoscopy, which combines intraoperative fluorescence imaging with minimally invasive laparoscopic techniques, has been gradually adopted in clinical practice. The value of real-time fluorescence image navigation in the diagnosis and treatment of surgical diseases is increasingly evident, making it a major trend in the industry.

The development of fluorescence endoscopy also requires the development of more contrast agents. At present, indocyanine green (ICG) is the most widely used and representative fluorescent contrast agent. ICG is a near-infrared fluorescent dye with good biocompatibility. ICG can be excited by external light in the wavelength range of 750–810 nm, emits near-infrared light at around 850 nm, and can penetrate human tissue with a thickness of 5–10 mm to be received by the fluorescence imaging system and displayed on the screen.

Currently, multiple companies worldwide are developing additional targeted imaging agents. This October, Intuitive Surgical, the company behind the da Vinci surgical robot, invested in a firm developing tumor-targeted fluorescent imaging agents.

Fluorescence technology holds significant potential for further development. In the early diagnosis of cervical cancer, Ushio Medical leverages tissue autofluorescence by exciting intrinsic fluorescence within cervical tissue, capturing and resolving the signals to analyze characteristic features of various epithelial lesions in grayscale autofluorescence images, thereby completing the detection process. This autofluorescence technique eliminates the need for contrast agents and shortens the time required for early cervical cancer diagnosis through excitation at specific wavelengths. Currently, Ushio Medical is also expanding the application of this technology to other disease areas.

Currently, endoscope manufacturers worldwide are striving to integrate the aforementioned three major trends, ultimately providing physicians with more options.

Currently, domestic manufacturers have launched 4K 3D fluorescence fusion endoscopes in the Chinese market, positioning themselves to lead the development of endoscopy in China.

Over the past three decades of development, China’s domestic endoscopy industry has achieved a critical breakthrough in fluorescence endoscopy technology, gaining significant influence over both upstream key components and downstream domestic brands. This pivotal leap forward is underpinned by years of accumulated expertise within the domestic endoscopy sector, coupled with the timely opportunities presented by the emergence of fluorescence endoscopy technology. Time waits for no one; we must seize the day. It is hoped that more enterprises will capitalize on this opportunity to establish globally renowned brands.

References:

Haitai XinGuang Investor Research Record for October 2022

Haitai Optics Prospectus