How Domestic Players in China's Multi-Billion-Yuan Dental Implant Market Leverage Centralized Procurement to Achieve 'Local Penetration'

Following the release of the official guidelines on dental implants, the entire industry breathed a sigh of relief and even saw a boost in morale.

On that day, whether it was investment firms focusing on dental implants, oral healthcare service providers, or upstream manufacturers of dental implants, their social media feeds were mostly filled with a festive atmosphere.

Some interpretations suggest that the centralized procurement in the field of dental implants did not trigger widespread outcry primarily because it targets public hospitals, focusing on standardizing surgical service fees and the costs of dental implant consumables within these institutions. This implies that upstream dental implant manufacturers, much like public hospitals, are also affected. However, this “impact” has not deterred investment firms and related companies; instead, it has been viewed as an opportunity.

Among them are the protagonists of this article—Jiangsu Trausim MEDICAL Instrument Co., Ltd. (hereinafter referred to as “Trausim”) and its Series A investors, Sunho Capital and Mingfeng Capital.

Recently, two months after the official release of the "Notice of the National Healthcare Security Administration on Launching Special Governance of Service Charges and Consumable Prices for Dental Implant Services," Sunho Capital joined forces with Mingfeng Capital to jointly invest in Trausim.

Founded in 2010, Trausim Medical is a company focused on the research, development, and production of dental implant systems. It holds five Class III medical device registration certificates for oral implants and two Class II medical device registration certificates. In 2020, it obtained the registration certificate for "machinable abutments," becoming one of the first batch of domestic Class III customized medical devices for oral care approved by the CFDA.

To date, Trausim has established partnerships with chain dental healthcare institutions including Topcare Medical, Meow Dental, Taikang Bybo Dental, Meiao Dental, and Little White Rabbit Dental, while also strategically collaborating with key public hospitals across provinces and cities throughout China.

Additionally, it is worth noting that by the end of 2020, Trausim had completed the business integration of “implantation + restoration,” taking a significant step closer to becoming an enterprise that provides doctors and patients with one-stop “digital technology support and services for implant-supported restoration.”

Although Trausim was officially established in 2010, it had already been an internal incubation project of Creations Medical, the then-leading orthopedic company, as early as 2007.

Chuangsheng Medical, formerly known as Wujin No. 3 Medical Instrument Factory, has specialized in the production of orthopedic implant medical devices since 1986. In 2010, Chuangsheng Medical successfully listed on the Main Board of the Hong Kong Stock Exchange, becoming the first Chinese orthopedic medical device manufacturer to be listed in Hong Kong.

In 2012, under the leadership of Qian Xiaojin, then Board Secretary of Chuangsheng Medical, the company secured overseas orders worth RMB 300 million, achieving a major breakthrough in international sales and laying a solid foundation for its expansion into global markets.

Moreover, the former Board Secretary has made multiple trips to Singapore, Israel, Europe, and other regions to conduct thorough inspections and research on advanced medical technology fields such as in vitro diagnostic reagents and biomaterials. He has reached a cooperation agreement with Singapore’s Mingce Medical Technology Co., Ltd. in the field of circulating tumor cell screening and established a partnership with Israel’s Collfran Company in the area of recombinant humanized collagen.

It is evident that Qian Xiaojin has cast a wide net in the healthcare sector, with involvement spanning orthopedics, in vitro diagnostics (IVD), and biosynthesis. More importantly, he has long been bullish on the prospects of dental implantology, deciding in 2007 to formally launch a project and personally lead his team into the dental implant industry.

To this day, the former board secretary of the listed company has become the general manager of Trausim. Whether it was the formal incubation of the dental implant project within Chuangsheng in 2007, the official establishment of Trausim in 2010, or today, the rapid development of the dental implant industry has all validated Qian Xiaojin’s judgment.

According to Zhongtai Securities’ “In-Depth Report on the Dental Implant Industry,” the compound annual growth rate (CAGR) of domestic dental implant procedures in China reached 46% from 2011 to 2020. In 2020, approximately 4 million implants were placed (equivalent to 28 implants per 10,000 people); however, the penetration rate remains relatively low compared with that of developed countries. Based on the existing domestic market, the potential demand for dental implants exceeds 20 million units, and the terminal market size could surpass RMB 100 billion.

Not only that,The upstream segment of the dental implant industry also holds significant growth potential: Zhongtai Securities estimates that the market size for zirconia all-ceramic crowns used in dental implants in China could reach RMB 15.2 billion; the combined market space (at ex-factory prices) for oral repair membranes and bone grafting powders could amount to RMB 3.6–6 billion; and the domestic market size for dental implants (at ex-factory prices) is expected to reach RMB 13.6 billion. This implies that the total market size for dental implants, crowns, and restorative materials is poised to exceed RMB 30 billion.

Furthermore,With the implementation of centralized volume-based procurement, the dental implant industry will gradually break free from one of the key constraints on its development—affordability.

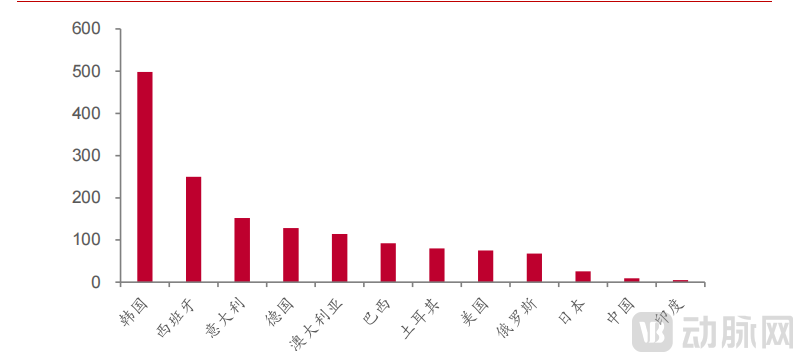

As previously mentioned, from 2011 to 2020, the penetration rate of dental implants in China remained relatively low compared with that in developed countries. According to Straumann’s annual report, South Korea ranks first globally in dental implant penetration, with approximately 500 procedures per 10,000 people; developed countries such as Spain, Italy, and Germany follow, with more than 100 procedures per 10,000 people. In contrast, China’s dental implant penetration rate is significantly lower than that of the aforementioned developed countries, exceeding only that of India.

2018 Dental Implant Penetration Rate in Major Countries Worldwide (Number of Implants per 10,000 People)

Image source: Zhongtai Securities’ “In-Depth Report on the Dental Implant Industry”

“In fact, many patients previously faced a ‘double pain’ fear when undergoing dental implant procedures: fear of surgical pain and fear of financial burden,” said Qian Xiaojin. However, the implementation of centralized volume-based procurement (VBP) has not only made upstream consumable prices more transparent but also further improved payment accessibility for dental implants. Therefore, from both long-term and short-term perspectives, and across both upstream industry segments and end-user markets, VBP is beneficial to the overall development of the dental implant sector. In the future, as payment accessibility continues to improve, the total market size will undoubtedly expand. Domestic enterprises must seize this opportunity.”

For upstream enterprises, high-quality products are undoubtedly the foundation of their survival and development. This is also the first step in seizing opportunities for growth.

For an upstream enterprise in the dental implant sector, particularly one specializing in dental implant consumables, the fundamental value of its products lies in meeting the needs of clinicians and patients.

“Reliable quality, ease of operation, and safety and efficacy” summarize the basic clinical requirements for dental implant products. How Trausim’s products meet these three core demands can be analyzed from multiple perspectives, including the number of regulatory approvals, product design, and manufacturing processes.

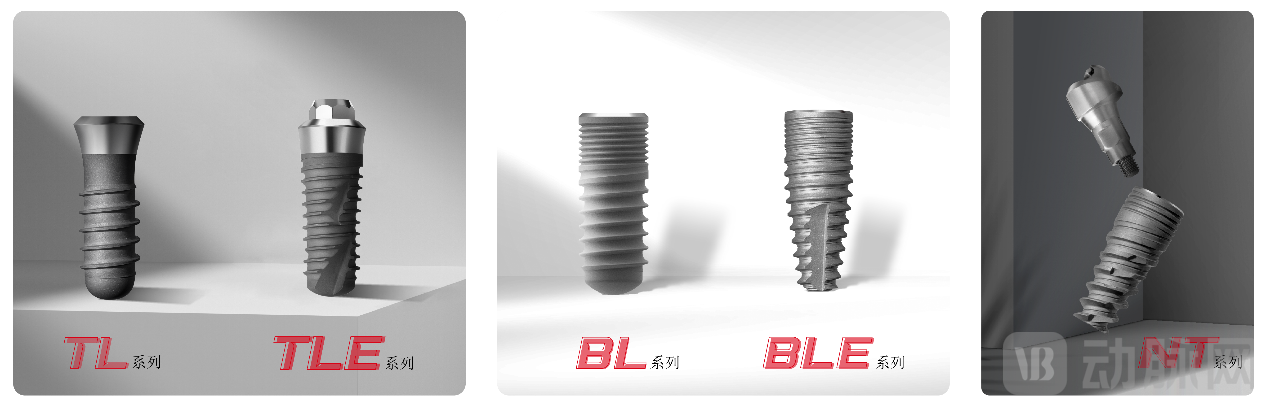

VCBeat has learned that, as of now,TrausimHolds a total of five Class III medical device registration certificates for dental implants, two Class II medical device registration certificates, and 44 Class I medical device filing certificates, andFive implant systems have been developed—the TL, BL, TLE, BLE, and NT dental implant systems—to meet diverse clinical needs and accommodate the surgical preferences of different clinicians.

Specifically, the TL dental implant system is a tissue-level cylindrical design with an internal structure featuring a Morse taper and internal octagon; the BL dental implant system is a bone-level cylindrical design with an internal structure featuring a Morse taper and cross-lock connection; the TLE dental implant system is a self-tapping tissue-level cylindrical design with an internal structure featuring a Morse taper and internal octagon; the BLE dental implant system is a bone-level tapered design with an internal structure featuring a Morse taper and cross-lock connection; the NT dental implant system is a self-tapping bone-level tapered design with an internal structure featuring a Morse taper and internal hexagon. The NT implant exhibits strong self-tapping capability and is suitable for single-tooth, fully edentulous, and partially edentulous restorations.

andIn addition to precision design, the technical barriers for dental implants are also reflected in two aspects—materials and surface treatment technologies.

According to the aforementioned research report by Zhongtai Securities, implant materials should possess good biocompatibility, corrosion resistance, wear resistance, and mechanical properties, whileTitanium and titanium alloys have become the gold standard for dental implant materials due to their excellent biocompatibility, superior mechanical properties, and favorable osseointegration. Trausim’s dental implants are made from Grade 4 cold-rolled commercially pure titanium, which offers high strength and exceptional osseointegration capability.

As for surface treatment technologies, the currently common ones mainly include sandblasted large-grit acid-etched (SLA) surface treatment, hydroxyapatite (HA) surface treatment, and titanium plasma spray coating surface treatment technology. Among them,SLA is currently the gold standard for implant surface technology.

According to Qian Xiaojin, not only were the initial production and R&D personnel at Trausim carefully selected through multiple rounds of screening from teams with extensive experience in orthopedic medical device manufacturing and R&D, but after the team was established, among themR&D personnel specializing in surface treatment were also sent to a Swiss surface treatment institution for two years of systematic study and joint development. After mastering the core SLA processes and workflows, they returned to China to construct and commission an automated surface treatment production line. This process is now stable.

In terms of production, Trausim is among the first batch of manufacturers in China to explore automated production. Currently, its production and testing equipment are on par with the world’s most advanced systems, while its stable supply chain for equipment and raw materials is distributed globally. This enables the company to enhance production efficiency and ensure consistent product quality, while simultaneously reducing production costs.

If automated production aims to achieve standardization on the basis of improving efficiency and reducing costs, then digitalization seeks to enable product personalization on the same foundation, thereby meeting the diverse needs of different clinical cases. This reflects the higher demands placed on the industry by the pronounced personalized nature of dental implantology.

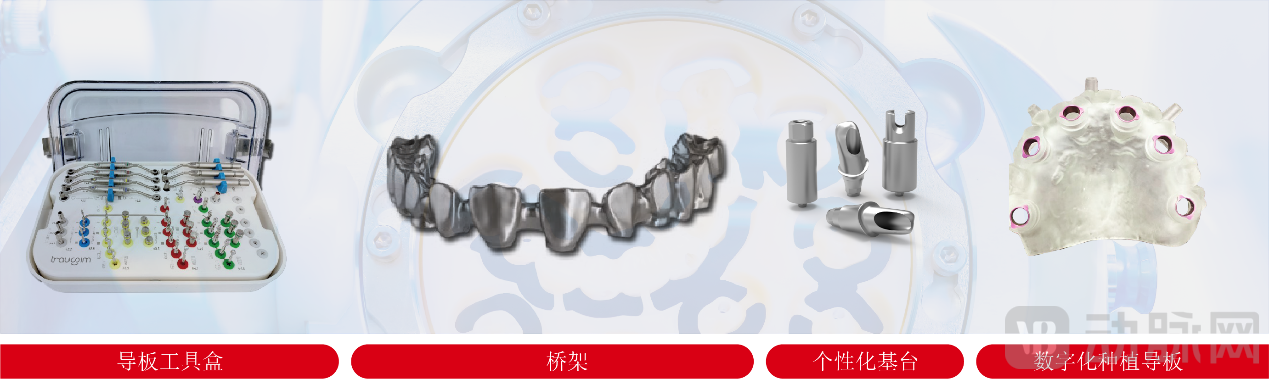

In response, to align with the personalized nature of dental implantology and the ensuing trend toward digitalization, Trausim has taken two strategic steps in its product portfolio. First, it has developed a suite of implant-centric digital products, such as dental scan bodies, warehouse scanning solutions, 3D-printed analogs, and composite abutment scan posts. These digital accessories are interoperable with mainstream digital software platforms on the market, including 3Shape, exocad, and Guide Master. “It was not merely a whim on Trausim’s part to develop these digital accessories; rather, the inherent characteristics of the dental implant industry demand that enterprise product functionalities comply with the requirements of digital implant restoration.”

Another initiative involves layering restorative products onto implant products, thereby integrating implant and restorative services to provide dentists and patients with “one-stop” digital technical support and solutions for implant-supported restorations. Additionally, Qian Xiaojin revealed that personalization in dental implants is primarily achieved through diversified restorative approaches.

“For example, some patients undergoing implant therapy may have insufficient bone conditions, making it impossible to place implants at the conventional vertical 90-degree angle. In such cases, implants must be placed at an inclined angle. However, currently available so-called standardized abutments have a limited range of angulation. Therefore, manufacturers need to provide personalized restorative solutions based on the patient’s actual clinical condition and the dentist’s restorative design plan,” said Qian Xiaojin. “Personalization is primarily reflected in the restorative phase.”

In terms of restorative solutions, Trausim has not only developed restorative accessories compatible with major international brands and initiated in-house R&D projects for products such as dental restoration membranes and bone powders, but also established a comprehensive digital workflow for the production, service, and delivery of dentures.

Notably, Trausim is not the only domestic enterprise attempting to integrate implantology and restorative services. VCBeat has observed that last year, Zhenghai Biological obtained the distribution rights for Trausim’s NT implant system. This collaboration is viewed by both parties as a mutually beneficial arrangement and represents another concerted effort by domestic dental implant companies to break the monopoly held by overseas brands.

Like many niche segments in the medical device industry, dental implants face a common challenge: dominance by foreign brands.

According to data from Zhongtai Securities, in 2013, the South Korean dental implant brand Osstem and the Swiss brand Straumann held 34% and 30% of China’s dental implant market, respectively. Although Straumann’s market share declined to 22% by 2018, the combined market share of the South Korean brands Osstem and Dentium reached 58%. Thus, in 2018, these three foreign brands collectively accounted for 80% of the domestic market.

Despite the industry’s development to date, with domestic brands achieving certain breakthroughs in R&D and manufacturing, Qian Xiaojin revealed that,Currently, foreign brands still hold an absolute dominant position in the domestic market.As a result, domestic substitution has seemingly become the main theme in the field of dental implant devices.

But unexpectedly, Qian Xiaojin corrected this statement—“It’s not about domestic substitution, but rather domestic penetration.”

Regarding the reasons, Qian Xiaojin explained: “In fact, both European and American brands and Korean brands have their own characteristics and advantages. For example, European and American brands have made indelible contributions in academic research, technological leadership, and case accumulation, earning their place in the Chinese market through their own efforts."Therefore, domestic brands should seize market opportunities by enhancing their overall capabilities and deepening their understanding of the Chinese market and policies, with the aim of benefiting more edentulous patients and ensuring that every patient has access to reasonably priced, safe, and effective dental implants. This approach will clarify the appropriate market positioning for national brands and enable private enterprises to fulfill their social responsibilities."

Therefore, Qian Xiaojin believes that, against this backdrop,What domestic brands should prioritize is to learn from the successful experiences of imported brands, continuously grow and strengthen themselves, and establish differentiated competition with imported brands. As for “substitution,” it should refer to replacing those small and medium-sized brands that previously lacked clear product quality, market positioning, and brand strategies, as well as core competitiveness, and relied on the “heritage” of imported brands as their sales advantage.

What lessons can domestic brands learn from imported brands? Taking European and American brands as examples, their moats for market expansion lie in R&D and manufacturing, academic achievements, and case accumulation.

According to Qian Xiaojin, domestic brands have now reached the same level as imported brands in terms of product quality and efficacy. “Given that China’s manufacturing capabilities are already highly robust and its supply chain is globalized—for instance, Trausim sources raw materials from the United States and Germany, while its slitting lathes come from Japan and Switzerland—we can confidently state that we are now able to provide high-quality dental implant products.”

Nevertheless,Compared with European and American brands, domestic brands still lag significantly behind in academic achievements, case accumulation, and market education. These gaps cannot be bridged by short-term market investment; instead, they require brands to define clear strategic positioning, commit to long-term academic research, actively organize and participate in activities and conferences that promote the development of the dental implant industry, establish collaborations with teaching hospitals across various provinces and cities in China, and provide theoretical and practical training opportunities in dental implant technology for a wide range of healthcare professionals.

Furthermore, in the interview, Qian Xiaojin emphasized,Since the outcomes of dental implant procedures require long-term observation and follow-up, there are no shortcuts to accumulating case data; one must diligently carry out case collection work.Since performing its first dental implant surgery, Trausim has placed great emphasis on the continuous collection and monitoring of case data, without interruption, to verify product efficacy, inform product development, and observe market penetration.

The development experience of South Korean brands also holds significant reference value for the growth of domestic enterprises in China.

The development trajectories of the two major South Korean dental implant brands mentioned earlier, Osstem and Dentium, align with the period of explosive growth in domestic dental implant demand in South Korea. From these South Korean brands, we can identify three key secrets to their success: first, the external environmental factors of rising dental implant demand coupled with rapid economic growth; second, policy support in the form of national health insurance coverage for dental implants in South Korea; and third, the provision of specialized professional training for dentists by manufacturers. As dentists are one of the primary drivers of development in the dental implant industry, providing them with clinical training not only indirectly expands the market but also strengthens the stickiness between dentists and brands, thereby enhancing market penetration.

Qian Xiaojin also frankly stated:“The greatest contribution of South Korean brands to the Chinese market lies in physician training.”Therefore, in the future, physician training programs will be a key strategic focus for domestic companies, including Trausim.

Moreover, similar to how South Korean domestic brands have begun to emphasize cost-effectiveness and how the Korean National Health Insurance has increased its support for dental implants, the implementation of China’s centralized procurement policy has further lowered the financial barrier to accessing dental implant services. ButIn Qian Xiaojin’s view, beyond improving payment accessibility, volume-based procurement (VBP) has also inadvertently launched a market education campaign. “It is akin to VBP sending a signal to patients about what constitutes a reasonable price and which brands are reliable.” Riding the wave of VBP, domestic brands with assured product quality can seize this momentum to increase their market penetration.

However, in addition to leveraging the momentum of centralized volume-based procurement, Trausim is also committed to breaking through its business model to empower channel partners and end-user clinics. Specifically, Trausim and Taikang Online have jointly launched a commercial dental implant insurance product called "Zhongya Bao." By purchasing this insurance, patients can access the full range of dental implant restoration services provided by Trausim’s partner dental clinics. The insurer provides two years of post-operative coverage; if accidental implant failure occurs within the coverage period, the insurer will provide a full refund, and the partner clinic will perform a free re-implantation for the patient.

Trausim’s commitment to exploring the integration of dental implant services with insurance stems from its founding mission: “To enable patients to access high-quality, guaranteed dental implant products and services at affordable prices through continuous technological breakthroughs.”

Trausim’s original aspiration and drive have also attracted the attention and favor of a number of investment institutions.

Guo Lei, founding partner of Sunho Capital, believes that during China’s 13th Five-Year Plan period, the compound annual growth rate (CAGR) of dental implant consumption reached as high as 23%, and domestic annual consumption of dental implants is expected to maintain rapid growth throughout the 14th Five-Year Plan period. In the current landscape of domestic dental implant supply, Korean brands account for half of the market share, followed by European and American brands, while domestically produced implants hold less than 5% of the market. As domestic implant technology has matured in recent years and brand recognition continues to rise, coinciding with the national implementation of centralized procurement policies for dental implants, the rapid expansion of market share for domestically produced implants has become an inevitable trend, propelling leading implant manufacturers onto a fast track of development. As a leading enterprise in domestically produced dental consumables, Jiangsu Trausim Medical Instrument Co., Ltd. began making significant investments and comprehensively laying out various product lines in the field of dental implant consumables twelve years ago, becoming the company with the most complete product portfolio in the niche segment of domestic implant systems. Following the completion of this round of financing, the company will rapidly expand production capacity and refine its product pipeline to embrace the era of substantial growth in domestically produced dental consumables, aiming to become an industry leader in its specialized sector.

Fei Simin, Partner at Ming Feng Capital, stated: “In terms of overall industry scale, data from the ‘2020 China Dental Medical Industry Report’ shows that the compound annual growth rate (CAGR) of China’s dental implant market reached 48% from 2011 to 2020. According to estimates by Huaan Chemical, the total number of missing teeth in China may reach 3.7 billion by 2027, with 180 million new dentures added annually, representing an average annual growth rate of approximately 6.6%. Among denture restoration solutions, the proportion of dental implants has increased significantly, with the number of implants potentially reaching 2.83 million units and an average annual growth rate of 30.6%. The overall market size for dental implants is enormous. Secondly, regarding the current competitive landscape, the market share of domestically produced dental implants in China remains low. Thirdly, continuous technological innovation on the dental service side will make rapid development in the dental implant market possible. For example, a dental implant robot project we invested in this year provides auxiliary functions such as positioning and navigation for implant surgeons, significantly reducing surgical difficulty and greatly shortening physician training time, thereby enabling services to meet the growing market demand. We believe that continuous technological innovation will also expand the overall market space for dental implants, reduce industry-wide costs, and improve efficiency. Finally, both the service and consumable segments of dental implants are facing centralized procurement, which will further enhance public awareness of dental implants in China. Moreover, the reduction in unit prices driven by policy measures will inevitably lead to a further expansion of the dental implant market size. Rapidly growing market demand, room for penetration of domestic products, new technological iterations, and policy support lead us to believe that this industry is poised for an explosive breakthrough. As one of the leading companies in China’s dental implant industry, Jiangsu Trausim MEDICAL Instrument Co., Ltd. features robust products, strong cost control capabilities, and a focus on brand and service development, making it an inevitable choice for our layout in the dental implant niche.”