Global Healthcare VCs Turn to Mental Health Startups for 'Psychological Comfort' Amid Surge in Digital Therapy Investments

Recently, the “digital wooden fish” has become a new favorite among young people. Many young individuals take out their “digital wooden fish” to tap on it when they experience anxiety or irritability, seeking emotional stability. It must be said that this stress-relief method is quite “cyberpunk.”

Amid the pandemic, public mental health has become a pressing social concern, spurring the emergence of companies dedicated to mental well-being. Most of these enterprises leverage the internet or cutting-edge technologies to provide psychological counseling and management, or employ approaches such as music, yoga, and meditation to help users relax both physically and mentally, thereby alleviating psychological disorders. At their core, they represent a more scientific version of the “digital wooden fish.”

In fact, the mental health industry is still in its ascendancy and is highly likely to become a new growth driver in the healthcare market. Venture capital firms with keen “instincts” appear to have already taken action. According to incomplete statistics from VBInsight’s Orange Fruit Bureau, as of November 28,In 2022, a total of 16 early-stage investments were completed in the global mental health sector, with total financing exceeding $1 billion., representing a 150% increase year-on-year! This clearly demonstrates that venture capitalists have gone all out in the mental health sector this year.

So, why are VCs around the world doubling down on the mental health sector right now? Just how much market potential lies beneath this blue ocean? Will it become a future trend? Turning our attention to China, what is the current state of development in the country’s mental health sector, and what new opportunities are emerging?

“A Booming Business” Spawned by the Pandemic

As early as 2007, the World Health Organization predicted that depression would become the second leading cause of global disease burden by 2020. Consequently, many industry insiders boldly speculated at the time, “Within a decade, the mental health sector is sure to experience a major boom.” In reality, however, the mental health field remained lukewarm in 2017.

It was not until 2020, with the outbreak of the global COVID-19 pandemic, that the mental health industry saw accelerated development. The loneliness and helplessness stemming from pandemic-related home confinement, coupled with the fear of the unknown, eroded people’s psychological resilience. Negative emotions such as distress and depression gradually spread, making mental health a growing focus of global attention.The renowned medical journal The Lancet released a report in 2022 stating that, under the impact of the pandemic, a total of 246 million people worldwide suffered from depression, representing an increase of approximately 27.6% compared with previous years.

More seriously,Mental Health Issues Are Spreading Among Adolescents and ChildrenProfessor Madigan, Chair of the Canadian Institute for Child Psychological Development, reviewed 29 clinical studies and public health projects worldwide through a meta-analysis, involving more than 80,000 children and adolescents with an average age of 13. The analysis results indicate that the number of teenagers suffering from depression and anxiety during the pandemic has doubled compared to before the pandemic!

Furthermore, psychological issues in adolescents and children are characterized by their persistence. As the saying goes, “Some people spend their entire lives healing from their childhood.” If psychological problems that emerge during childhood do not receive timely and effective intervention, they may lead to more severe issues in adulthood, and in extreme cases, may even threaten social stability.

Therefore, whether in terms of patient volume or industry necessity, the mental health sector is currently commanding significant market attention.

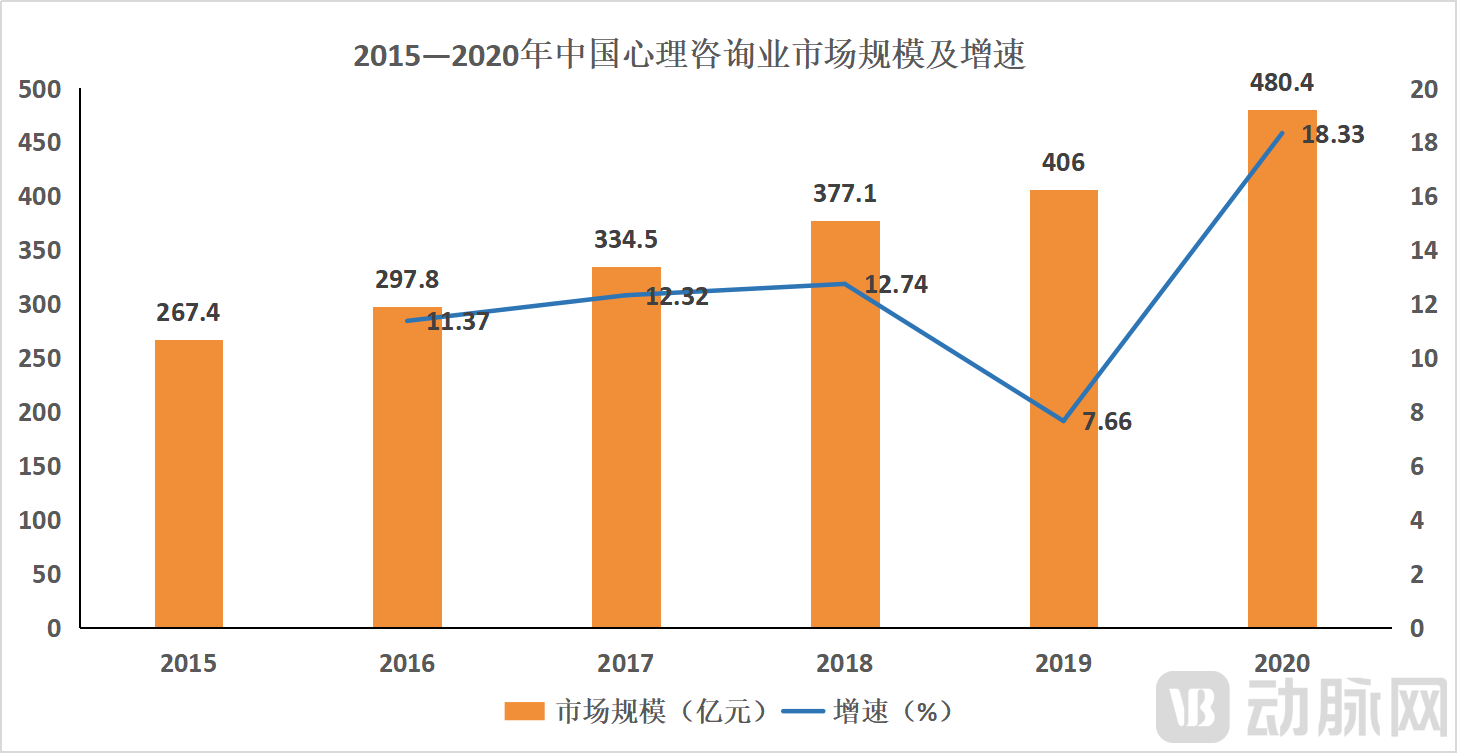

Figure 1. Market Size and Growth Rate of China’s Psychological Counseling Industry, 2015–2020 (Data Source: Huaon Intelligence Network)

However, market demand is only one factor; the influx of new technologies has brought greater possibilities to this sector.

In recent years, wearable devices and digital therapeutics have developed rapidly and gradually penetrated the mental health industry, further fueling its growth. An increasing number of mental health companies are integrating wearables into psychological diagnostics, using them to measure galvanic skin response (GSR) and thereby obtain more precise indices of patients’ emotional fluctuations, adding a layer of “objectivity” to mental health assessments.

Meanwhile, guided by the concept of the metaverse and within the framework of evidence-based medicine, digital therapeutics are flourishing globally. According to the "2022 Digital Therapeutics Market Insights" report released by Analysys in October 2022, investment in the digital therapeutics sector increased by 134% year-on-year in 2021 compared with 2020, and continued to rise in 2022. Notably, among the various sub-sectors of digital therapeutics, mental health startups accounted for the largest proportion.

According to the report "Defining the Mental Health Economy," the global mental health market has reached $121 billion, while China's mental health sector is valued at approximately RMB 300 billion, with a multi-billion-dollar market awaiting definition taking shape.

Digital Therapeutics Emerge as a "New Drug" for Mental Health

Prior to the rise of the internet, psychotherapy relied primarily on face-to-face consultations between patients and clinicians, often supplemented by pharmacological interventions. With the advent of digital therapeutics, the mental health sector is becoming more evidence-based yet increasingly human-centric, demonstrating unprecedented vitality in the venture capital market.

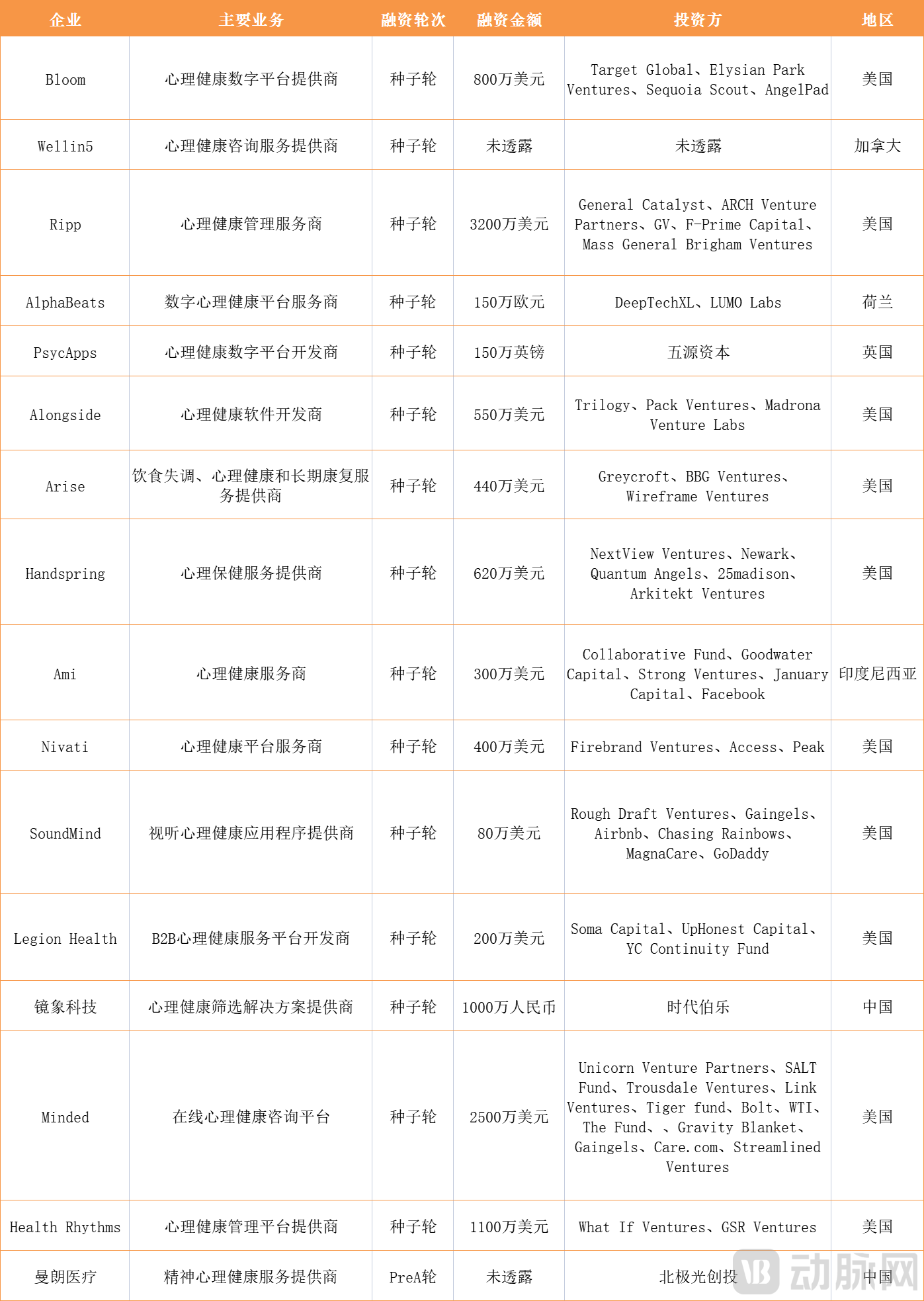

Figure 2. Sixteen Mental Health Startups That Completed Early-Stage Financing in 2022

Figure 2. Sixteen Mental Health Startups That Completed Early-Stage Financing in 2022

According to statistics, all 16 mental health startups that completed early-stage financing in 2022 focused on digital therapeutics. However, there are slight differences among them. Based on variations in target populations, treatment modalities, and service types, VCBeat categorizes them into three major types:Emotional Management Platform, Social Psychology Platform, and Mental Health Platform.

·Emotion Management Platform: Provides self-service tools to help users self-regulate and manage their emotions.

Among all categories, emotion management platforms have the broadest target audience. Statistics show that 3 out of 16 startups fall under the category of emotion management platform companies.

It is defined as an “Emotional Management Platform” because it not only helps soothe the emotions of patients with mental disorders, but also alleviates psychological stress among the general public; anyone can receive emotional support through this platform.

Typically, emotion management platforms have few professional psychotherapists. Instead, they primarily help users relax and alleviate psychological stress through personalized approaches such as music, yoga, and meditation. This therapeutic model not only overcomes the common challenges of standardization and insufficient supply in the mental health sector, but also subtly encourages patients to accept treatment, thereby addressing their reluctance to seek professional medical help. Furthermore, emotion management platforms face lower barriers to commercialization, facilitating companies’ upgrade of consumer-oriented business logic.

Taking Sound Mind, which completed an $800,000 seed funding round this year, as an example, the company primarily leverages music to soothe users’ moods and achieve therapeutic effects for mental health conditions. Reportedly, its therapeutic music consists mainly of piano melodies, bird songs, flowing water, and other white noise elements that stimulate electrical signals to promote neural relaxation. Users can select and customize music according to their individual needs, thereby creating opportunities for the company’s commercialization efforts.

· Psychosocial Platform: Primarily focused on psychological counseling services, typically delivered via a SaaS model.

According to statistics, 7 out of the 16 startups are social-psychological platform companies. Social-psychological platforms primarily provide counseling and consultation for common psychosocial issues, such as depression and anxiety. Therefore, their scope of application is more targeted compared to that of emotional management platforms.

The operational model of psychosocial platforms is largely similar to that of offline psychological counseling, primarily migrating traditional in-person consultation and guidance services to online channels through video, images, voice, and other media. However, compared with the offline model, it engages a broader range of participants and offers greater autonomy.

The psychosocial platform will feature licensed mental health professionals, allowing users to select the therapist best suited to their needs based on provider profiles. This grants users full autonomy in choosing their clinician, which can, to some extent, enhance the overall effectiveness of psychotherapy.

In addition, offline services are primarily delivered by licensed mental health professionals who provide counseling to patients with psychological disorders, whereas online social-psychological platforms have broken this long-standing convention. Some of these platforms have incorporated social networking features, leveraging big data to categorize and match users, thereby enabling mutual therapeutic support among peers.

Take the Canadian company Wellin5 as an example. It primarily facilitates communication between patients and mental health professionals to help alleviate patients' psychological issues. However, Wellin5's scope of treatment is not limited to anxiety and depression. Its applications are extensive, covering nearly all psychological challenges that may arise in daily life, from premarital counseling to social phobia and domestic violence.

Wellin5 connects users with psychologists through real-time chat, helping them address negative emotions anytime and anywhere. Its business model is similar to that of offline counseling, charging based on the number and duration of sessions, while also offering flexible discounted subscription plans on a monthly or annual basis.

· Mental Health Platform: Typically operated by specialized psychiatric hospitals through online consultation models.

Mental health platforms represent the category with the highest professional requirements. Among the 16 startups, six are mental health platform companies. These platforms primarily target patients with specific psychological disorders and mostly operate on an online hospital model, facilitating consultations between patients and professional physicians.

Typically, mental health platforms encompass all diagnostic stages, including consultations, treatment planning, medication prescriptions, and follow-up visits, thereby forming a complete therapeutic loop. Take Arise, which completed a $4.4 million seed financing round this year, as an example; it primarily serves patients with eating disorders by providing them with integrated community and clinical care.

It is reported that Arise provides patients with private physician services. Physicians identify the traumatic triggers underlying patients' eating disorders through in-depth consultations, and then help resolve psychological issues by building trust and providing counseling. Meanwhile, personalized meal plans, goal-setting strategies, and treatment regimens are tailored to each patient to optimize therapeutic outcomes.

Furthermore, Arise leverages its big data platform to analyze patients’ symptoms and the underlying causes of eating disorders, matching individuals with similar conditions to form support communities. Within these communities, patients can offer mutual encouragement and facilitate each other’s healing.

In summary, the operation of these three models is inseparable from the development of digital therapeutics, as well as the support of AI and big data. Driven by digital therapeutics, patients with mental disorders have shown significantly greater acceptance of online diagnosis and treatment; meanwhile, digital management models have improved patient treatment adherence, leading to markedly enhanced therapeutic outcomes.

The integration of digital therapeutics and mental health medicine is still in its nascent stages, with neither the landscape for psychological disorder consultation platforms nor the emotional counseling market having fully taken shape. Looking ahead, significant uncertainties remain regarding technology, service models, and platform concepts.

The Current State of Mental Health in China: Opportunities and Challenges Coexist

According to statistics, among the 16 mental health startups that completed early-stage financing in 2022, 10 were based in the United States, while only two were Chinese enterprises. Does this indicate that there is no market for China’s mental health industry, or that it has not received adequate attention?

The answer is clearly no. According to the VCBeat Orange Database,From 2021 to the present, there have been 24 investment and financing transactions in China's mental health sector, with a cumulative amount exceeding RMB 1.5 billion.Venture capital firms such as Matrix Partners China, Qiming Venture Partners, BlueRun Ventures, and Northern Light Venture Capital have paid considerable attention to this sector. Notably, in September 2021, a digital mental health service platformGood MoodCompleted a C-round financing of RMB 200 million led by ByteDance, setting a new record for the largest single investment in China’s mental health sector at that time.

Although such financing volumes are negligible in the grand scheme, it is worth emphasizing that prior to 2021, few enterprises in China’s mental health sector secured financing, with most deals occurring before Series B and involving relatively small amounts.

So, how exactly did China’s mental health industry experience its explosive growth?

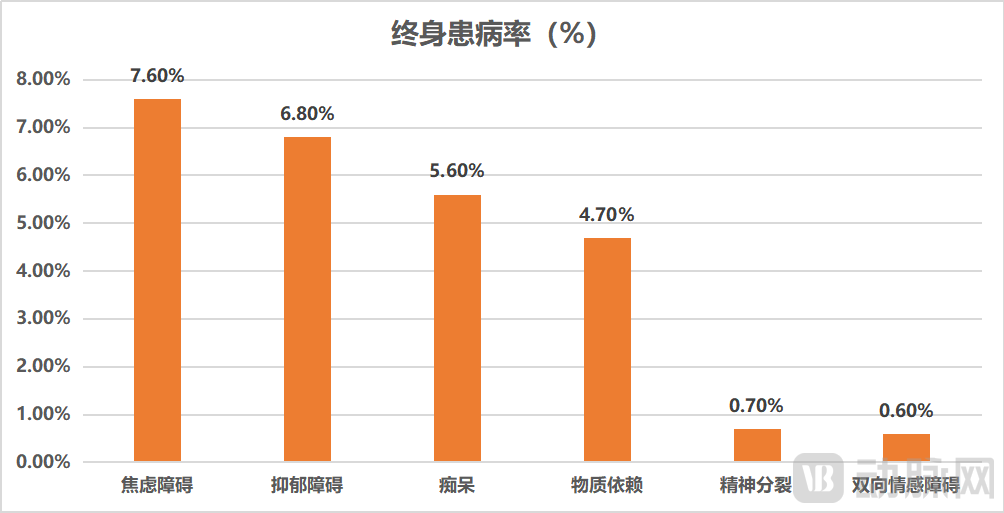

The primary factor is, of course, the ever-growing market demand.According to the “2022 Blue Book on Digital Mental Health Services Industry” released this year, the lifetime prevalence of mental disorders in China is 16.6%. Given China’s large population base, both the absolute number and the probability are strikingly high.

Among these, anxiety disorders and depressive disorders had the highest prevalence rates, reaching 7.6% and 6.8%, respectively, which also reflects that symptoms of anxiety and depression are relatively prominent among the Chinese population. In terms of age, psychological issues appear to be more severe among young people.

Figure 3. Major Symptoms and Development Trends of Mental Health in China (Data Source: "2022 White Paper on the Digital Mental Health Services Industry")

Figure 3. Major Symptoms and Development Trends of Mental Health in China (Data Source: "2022 White Paper on the Digital Mental Health Services Industry")

Secondly, China’s policy framework is also strongly supporting the development of the mental health industry.In the past one to two years, China has issued as many as 10 policies related to the field of mental health. These policies primarily target core areas such as enhancing the professional competence of mental health practitioners, increasing the number of mental health outpatient clinics, and improving community-based mental health services. They emphasize the importance of attention to mental health from disciplinary, clinical, and social development perspectives.

Finally, shifts in social awareness are also driving the expansion of China’s mental health market.China’s mental health industry started relatively late, and public awareness remains insufficient; consequently, psychological counseling and management have long been neglected. Moreover, societal prejudice and discrimination against patients with mental disorders and their families persist, leading many patients to avoid seeking medical care.

However, with societal progress, the dissemination of accurate medical science and the improvement of civic literacy are jointly reshaping social consciousness. Growing tolerance toward individuals with mental illnesses has empowered more patients to confront their conditions and seek appropriate professional help. This rising market acceptance is driving market expansion and further deepening the demand for mental health services in China.

However, the path forward has not been smooth.

First,There is a shortage of qualified professionals, clinical outcomes vary widely, and the market lacks more flexible and efficient solutions.China’s mental health workforce is characterized by a complex composition and uneven professional competence. After excluding teachers, neighborhood committee members, and other amateurs from diverse backgrounds, there are only 40,000 licensed psychiatrists.

Many non-professional mental health practitioners on online counseling platforms mislead the public by advertising “short treatment courses” and “high efficacy,” thereby disrupting market order. However, the integration of digital therapeutics and mental health care in China is still in its early stages, and the industry lacks standardized regulation.

Moreover, the service models and counseling content offered by psychological counseling firms in the current market are largely homogeneous, with no clear industry leader capable of setting standards. Therefore, establishing industry standards and regulatory frameworks has become an urgent issue to address in China’s mental health market.

Second,The mental health industry features high per-unit market prices, posing challenges for commercial promotion.Currently, except for Beijing, Shenzhen, and Guangdong Province, most provinces and municipalities in China have not included psychotherapy in their medical insurance coverage, requiring patients to pay out-of-pocket. It is understood that the current average market rate is 150 yuan per hour. Given the prolonged treatment cycles for mental health conditions, this imposes a significant financial burden on patients, thereby hindering the promotion of the mental health industry and its market acceptance.

Third,China's foundational research in mental health is relatively weak, and there is still room for improvement in discipline development.In 1951, China established its first research institute dedicated to academic studies in mental health—the Institute of Psychology, Chinese Academy of Sciences—marking the first systematic investigation into the psychological well-being of the Chinese population. However, due to various reasons, the Institute of Psychology suspended all research activities in 1968 and was subsequently disbanded, only to be reinstated in 1977. This interruption resulted in a significant gap between China’s mental health research and that of the rest of the world.

As early as 1946, the United States established the National Institute of Mental Health (NIMH), which has since grown into the largest mental health research institute in the world. Currently, most representative psychological theories in clinical practice, and even the standards in the field of mental health research, are formulated by this institute. There is still a significant gap between China’s mental health research and that of the United States.

Nevertheless, China’s mental health market remains vast. Technologies such as online consultations, virtual counseling, comprehensive emotional management models, and AI-powered digital therapeutics are increasingly permeating daily life. With the industry’s rapid growth, mental health issues have garnered significant societal attention, prompting individuals to acknowledge and prioritize their own mental well-being. In the coming years, we can expect to experience more innovative technologies while gaining a more comprehensive understanding of the importance of “mental health” for every individual.

Thus, the current fervor is merely the beginning. Over the next few years, this sector will enter a golden period of development, and those startups that can truly address existing challenges may seize the first-mover advantage and rise to the forefront of the industry.