Dongxing Medical Successfully Lists on ChiNext Amid Fierce Competition in China's Stapler Industry with Over 100 Players

Canopus

Surgical Medical Device R&D Company

On November 30, Jiangsu Canopus Wisdom Medical Technology Co., Ltd. (hereinafter referred to as “Canopus Medical”) successfully completed its initial public offering (IPO) on the ChiNext board. As of today’s market close, Canopus Medical was trading at RMB 53.12 per share, up 20.48%, with a total market capitalization of RMB 5.321 billion.

According to available information, Dongxing Medical was established in 2001. Starting as a medical device distributor, it has since evolved into a platform-based group company covering a wide range of surgical equipment and medical consumables. Its core business focuses on the research and development, manufacturing, and sales of surgical medical devices, with staplers as its representative product. Notably, Dongxing Medical has achieved full industry chain integration, encompassing stapler product R&D, mold development, component production, product assembly, and downstream sales.

In addition, Canopus Medical’s business also encompasses the manufacturing of surgical medical equipment and the distribution of medical devices. In terms of surgical equipment manufacturing, it independently produces medical devices such as surgical lights, operating tables, and ceiling-mounted pendants and bridges. Regarding its medical device distribution business, it serves as an agent for over 60 brands, including BenQ Medical, Mindray, and Becton Dickinson (BD), offering products such as surgical lights, operating tables, patient monitors, ventilators, intubation supplies, anesthesia kits, and gloves.

During the reporting period, Canopus Medical achieved dual growth in both revenue and net profit. From 2019 to 2021, its revenues were RMB 296 million, RMB 355 million, and RMB 443 million, representing year-on-year increases of 26.67% in 2020 and 19.25% in 2021, respectively. Net profits attributable to shareholders of the parent company were RMB 47.38 million, RMB 79.70 million, and RMB 110 million, respectively. In the first half of 2022, Canopus Medical recorded revenue of RMB 211 million, an 8.45% increase from the same period of the previous year, while net profit after deducting non-recurring gains and losses rose by 18.18% year on year.

From 2019 to 2021 and in the first half of 2022, the stapler and accessory manufacturing business accounted for 55.81%, 68.77%, 71.98%, and 76.42% of Dongxing Medical’s total revenue, respectively, gradually becoming its core business.

Surgical staplers are medical devices that replace traditional manual suturing, performing tissue transection, closure, and functional reconstruction of organs by firing and implanting metal staples into the tissue.

Based on the surgical approach, staplers can be classified into open staplers and laparoscopic staplers. Open staplers are primarily used in open surgeries to replace manual suturing of wounds, thereby enhancing the overall efficiency of surgical suturing and cutting. As a minimally invasive surgical medical device, laparoscopic staplers address the challenges associated with manual manipulation in minimally invasive procedures where the surgical field is narrow or the target site is deeply located.

According to DXY’s “Overview of the Stapler Industry Development,” the global market size for surgical staplers grew from USD 7.364 billion in 2015 to USD 9.018 billion in 2019, representing a compound annual growth rate (CAGR) of approximately 5%. The global market size for surgical staplers is projected to reach USD 11.509 billion by 2024.

Despite the stapler industry’s market size exceeding RMB 10 billion and maintaining steady growth, its competitive landscape is at a critical juncture of abrupt change. First, centralized volume-based procurement (VBP) of staplers launched by multiple provinces and inter-provincial alliances in China will directly impact pricing and market structure. Second, competition within the stapler industry is intensifying: overseas brands such as Johnson & Johnson and Medtronic hold significant market share, while more than 100 domestic manufacturers are engaged in fierce internal competition, narrowing the gap with imported products and competing directly with foreign brands. Finally, a new generation of stapler products has been successively approved for market entry and is experiencing rapid development, which will bring transformative changes to the existing market.

In the past two years, surgical staplers have become one of the most frequently and extensively included products in centralized volume-based procurement (VBP) programs. Provinces, municipalities, and autonomous regions across China have successively launched VBP initiatives for surgical staplers, either independently or through regional alliances.

As of July 31, 2022, centralized procurement programs for surgical staplers had been launched or participated in by 29 provinces and municipalities across China, including Chongqing, Hunan, Yunnan, Henan, Jiangsu, Shanxi, Fujian, Beijing, Tianjin, Hebei, Guangdong, Shandong, Xinjiang, Hainan, and Qinghai.

In previous rounds of centralized procurement for surgical staplers, the aggregated procurement volume accounted for 70%–100% of total demand, with average price reductions ranging from 78% to 88% and maximum reductions reaching 91%–96%. For instance, in December 2020, Jiangsu Province conducted centralized procurement for surgical staplers, achieving an average price reduction of 84% and a maximum reduction of 96%. In November 2021, a consortium of 18 provinces and municipalities, including Beijing, Tianjin, and Hebei, carried out centralized procurement for surgical staplers: the average price reduction for circular/end-to-end staplers was 87%, with a maximum reduction of 94%; for hemorrhoid staplers, the average price reduction was 88%, with a maximum reduction of 95%.

Overall, the end-user prices of surgical staplers have plummeted, but volume-based procurement has brought both advantages and disadvantages to domestic enterprises.

In regional markets, winning bids in volume-based procurement (VBP) programs helps participating companies expand their coverage of end-user hospitals, boost product sales, and increase market share. For example, after Jiangsu Canopus Wisdom Medical Technology Co., Ltd.’s stapler products won the bid in Hunan Province’s VBP program, its average monthly sales from October to December 2021 (after implementation of the VBP policy) increased by 1,159.73% year-on-year compared with the average monthly sales in 2020 (before implementation), marking significant growth.

Among them, innovative enterprises have the opportunity to rapidly enter the market and reach more end-user hospitals by leveraging centralized procurement; meanwhile, established companies that already hold a certain market share can use centralized procurement to consolidate their existing market position, thereby increasing their market share and market concentration. However, if a company fails to win the bid, its products may struggle to compete for market share in the regions covered by the centralized procurement program.

Furthermore, the winning bid rules for centralized volume-based procurement (VBP) typically adopt a price-bidding model. To increase the likelihood of securing a bid, domestic competing enterprises are more inclined to “exchange price for volume.” In this process, if sales volume increases substantially after a product wins the bid at a reduced price, it will offset the adverse effects of lower selling prices and gross profit margins, thereby increasing the company’s net profit. However, if the sales volume increases only marginally or fails to rise, it will significantly impair the company’s profitability.

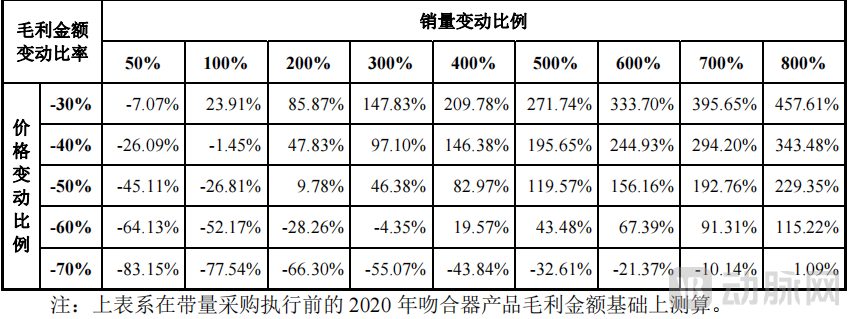

According to the prospectus of Jiangsu Canopus Wisdom Medical Technology Co., Ltd. (Dongxing Medical), based on the prices and costs of its stapler products in 2020, if the unit price of stapler products decreases by 30%-50% after the implementation of "volume-based procurement," its gross profit margin can be maintained at an overall level of above 55%; however, if the price drops by 60%, the gross profit margin will fall to 47.14%; if the price drops by 70%, the gross profit margin will drop to 29.52%.

From a profitability perspective, taking Jiangsu Canopus Wisdom Medical Technology Co., Ltd. (East Star Medical) as an example, following the volume-based procurement of stapler products, if prices drop by 40%, sales volume must increase by at least 100%; if prices drop by 50%, sales volume needs to grow by approximately 200%; and if prices drop by 70%, sales volume must surge by roughly 800%. Otherwise, its gross profit margin will shrink significantly, and its profitability will decline markedly.

For stapler manufacturers, participating in centralized volume-based procurement (VBP) is a mandatory requirement. Failure to participate will result in the direct loss of market share in VBP-covered regions, whereas participation offers an opportunity to seize market share and expand their presence.

However, how to participate in centralized procurement, how to submit bids, and how to enhance competitiveness under the centralized procurement environment have become new challenges that all enterprises must face.

In the stapler market, domestic companies are also facing the threat of intensifying competition.

Currently, there are over one hundred manufacturers of surgical staplers in China. A search for “surgical stapler” on the official website of the National Medical Products Administration (NMPA) yields 1,606 registration certificate records, underscoring the intense competition in the domestic market.

However, domestic companies are primarily competing in the low- to mid-end markets, such as for open surgical staplers, while the high- to mid-end markets, including laparoscopic and electric surgical staplers, remain dominated by multinational medical device corporations such as Johnson & Johnson and Medtronic.

Specifically, in the field of open surgical staplers, many domestic manufacturers have overcome technical challenges after years of development, bringing product quality and performance to a level comparable with imported products, thereby gradually achieving import substitution. Currently, domestically produced surgical staplers account for approximately 50% of the open surgical stapler market, which features numerous participants and intense competition.

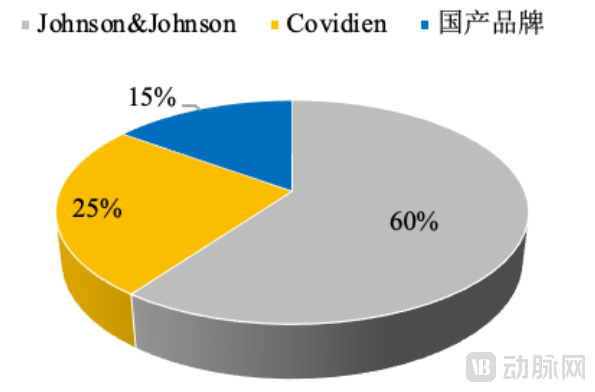

In the field of laparoscopic staplers, due to high technical barriers, only a few leading domestic enterprises have developed such devices, and the market remains largely monopolized by foreign brands such as Johnson & Johnson and Covidien (a subsidiary of Medtronic). Among them, Johnson & Johnson and Covidien hold 60% and 25% of China’s laparoscopic stapler market, respectively, while domestic companies account for only about 15% of the market share.

(Competitive Landscape of the Domestic Endoscopic Stapler Market; Data Source: Prospectus of Jiangsu Canopus Wisdom Medical Technology Co., Ltd.)

Overall, imported products primarily dominate the high-end price segment, while domestically produced products focus on the mid- to low-end market. Chinese manufacturers are breaking through market barriers by achieving import substitution in the mid- to low-end segment and simultaneously making inroads into the mid- to high-end market.

Amid steep price cuts from centralized procurement and intensifying market competition, leading Chinese stapler manufacturers are not only ramping up R&D and deploying next-generation stapler products, but also upgrading manufacturing processes, enhancing production capabilities, reducing production costs, and strengthening product competitiveness.

To date, the low- to mid-end surgical stapler market has become intensely competitive, while the mid- to high-end segment remains a blue ocean due to high technical barriers.

In China, only leading stapler manufacturers such as Tianchen Medical, David Medical (its subsidiary Weierkaidi), Canopus Medical, Partel Medical, and Jianshi Medical (its subsidiary Ruiqi Surgical) are developing or have already developed third-generation electric staplers, positioning them to capture the mid-to-high-end market currently monopolized by Johnson & Johnson and Medtronic.

According to reports, stapler products have evolved from first-generation open surgical staplers and second-generation laparoscopic staplers to third-generation electric staplers. Compared with the previous two generations, third-generation electric staplers are simpler to operate, require less effort and time for firing, and provide continuous and smooth cutting and suturing of tissue. They offer superior hemostatic effects, helping to reduce the incidence of medical accidents.

Among them, multinational corporations such as Johnson & Johnson and Medtronic possess substantial technological expertise, having developed electric staplers earlier and thus securing a dominant market position. In contrast, only first-tier domestic companies are continuously increasing their financial investment to innovate and develop intelligent electric staplers.

For example, in the first half of 2022, Canopus Medical increased its R&D investment to a total of RMB 16.4667 million, accounting for 15.51% of its operating revenue, representing a 39.77% year-on-year increase. During this period, Canopus Medical’s “Third-Generation Laparoscopic Cutting Stapler and Cartridge Component” project entered the product trial production stage, the “Second-Generation Minimally Invasive Stapling Technology for Extra-Thick Tissues” project advanced to the pilot-scale production stage, and the “Electric Intelligent Stapler” obtained the NMPA product registration certificate.

From 2019 to 2021, Dongxing Medical maintained a high level of R&D investment, amounting to RMB 11.1806 million, RMB 18.3242 million, and RMB 20.6741 million, respectively. As a result, its single-use electric endoscopic stapler received market approval in 2021. According to the company, its new-generation electric endoscopic stapler features an electric firing transmission design, with both firing and retraction fully motorized, thereby further enhancing stability and safety during surgical procedures.

As domestically produced electric staplers continue to enter the market, they will capture a share of the traditional stapler market by virtue of superior clinical outcomes; meanwhile, they will compete with imported products and make inroads into the mid-to-high-end market.

In addition to innovative products, leading enterprises are also procuring intelligent and automated equipment to enhance production capacity and product quality, reduce costs, and cope with increasingly fierce market competition and the substantial demand from centralized volume-based procurement.

For example, 30% of the funds raised by Canopus Medical in this offering will be allocated to the intelligent manufacturing and capacity expansion of medical device components. Canopus Medical will construct new production workshops and auxiliary facilities, and purchase and install advanced software and hardware equipment, thereby increasing the annual production capacity of staplers and related products by 1.185 million units.

Paier Medical plans to achieve 24/7 production by installing additional automated equipment for manufacturing, assembly, and packaging. Meanwhile, Paier Medical will purchase advanced production equipment to enhance its intelligent manufacturing capabilities.

Canopus Medical is also driving the transformation of its manufacturing operations toward automation and intelligence. Its first intelligent automated production line for the laparoscopic platform has entered the commissioning phase, with acceptance and operational deployment scheduled for completion in 2022. The implementation of a Manufacturing Execution System (MES) has enabled interoperability and visualized management of production data, thereby enhancing production safety and decision-making efficiency.

Notably, some of these companies are expanding upstream. For instance, Jiangsu Canopus Wisdom Medical Technology Co., Ltd. (Dongxing Medical) has established a presence in the core components of surgical staplers, with its designed and manufactured parts cumulatively supplied to over 100 domestic surgical stapler manufacturers. Piert Medical plans to reduce its reliance on external component suppliers and lower costs by producing certain high-end core components for surgical staplers.

It is evident that leading domestic stapler manufacturers are increasingly engaging in fierce competition to reduce costs. As costs decline, terminal sales prices are expected to continue falling, thereby driving out numerous small and medium-sized enterprises characterized by low innovation, product homogenization, and high production costs. This trend will shift the market landscape from one of “diverse proliferation” toward “oligopolistic dominance.”

In response to the pressures of centralized procurement and market competition, leading domestic stapler manufacturers are accelerating their global expansion.

According to the prospectus, as of now, Canopus Medical’s stapler products have obtained certifications from multiple countries and regions, including the U.S. FDA, Brazil’s ANVISA, and South Korea’s KFDA, and have been exported to overseas markets such as Brazil, Iran, South Africa, Saudi Arabia, and Italy. In 2021, Canopus Medical intensified its efforts in expanding overseas markets, leading to a significant increase in revenue from its stapler products abroad. In the first half of 2022, the proportion of overseas sales revenue to total revenue further increased.

Canopus Medical is also actively expanding its overseas business. In collaboration with B. Braun, a world-leading professional medical equipment and device company based in Germany, it promotes and sells Canopus Medical’s stapler products in 27 countries. Meanwhile, in international markets where Canopus Medical had previously established a presence, the company has not only engaged professional marketing consultants to expand product coverage but also participated in various group purchasing programs and regional tenders, securing a series of significant contracts.

In addition, Canopus Medical is advancing market access initiatives in previously unserved countries and regions, with applications currently underway in 10 nations. Its products are expected to enter more countries worldwide in the future.

David Medical has developed a network of over 40 distributors in the international market, selling its stapler products to more than 100 countries across Asia, Africa, Europe, and South America. In the first half of 2022, while consolidating its existing markets, David Medical newly entered multiple national markets in regions including Europe, Africa, and South America, driving a year-on-year increase of 150.41% in its overseas revenue.

Purui Medical is a well-established leader in the export of surgical staplers. From 2016 to 2020, it ranked first among domestic surgical stapler brands in terms of export volume. According to reports, Purui Medical exported its surgical stapler products to more than 60 countries and regions worldwide in 2020, with overseas sales revenue accounting for 40% of its total revenue. In addition, Purui Medical plans to continuously expand its sales channels and integrate third-party high-end product resources to enhance its overall solution capabilities, thereby further boosting the international competitiveness of its products.

Overall, multiple leading domestic stapler manufacturers are accelerating their globalization efforts, driving the sale of Chinese-made stapler products worldwide. It is expected that as these companies expand into overseas markets and achieve higher revenues, they will also realize greater profits.

However, with over a hundred players in the domestic market, there is clearly an “oversupply.” It is expected that fierce future competition will lead to a “winner-takes-all” outcome, thereby increasing market concentration.

VCBeat will continue to monitor how the market evolves in the future.