Public Outcry and IPO Hurdles: Are Nucleic Acid Testing-Related Companies Truly Profitable or Innovators?

Yeasen

Tool Enzyme Raw Materials and Diagnostic Product R&D, Manufacturer

ACROBiosystems

Provider of Biopharmaceuticals and Biological Reagents

The revenue performance and listing plans of companies involved in nucleic acid testing have attracted unprecedented attention.

On the evening of November 23, the official website of the Shanghai Stock Exchange announced that, given the need for further verification of certain matters regarding Yeasen, it had decided to cancel the review originally scheduled for the 25th.

Yeasen is an upstream raw material supplier in the in vitro diagnostics (IVD) industry, primarily engaged in molecular, protein, and cell-based biological reagents. The company’s business includes the supply of raw materials for COVID-19 test kit production and a small volume of R&D reagents. In 2020, 2021, and the first half of 2022, revenue related to COVID-19 accounted for 25.42%, 24.77%, and 38.28% of its total operating income, respectively.

On June 23 this year, the Shanghai Stock Exchange (SSE) accepted Yeasen’s IPO application for listing on the STAR Market. On November 18, the SSE notified the company that its listing review was imminent. Merely five days later, Yeasen’s IPO process was abruptly suspended.

What happened over these five days to cause a shift in the Shanghai Stock Exchange’s stance? What exactly does “relevant matters still require further verification” refer to? We remain unaware.

A clear signal is,Late on November 21, the Shanghai and Shenzhen Stock Exchanges stated that they were closely monitoring the IPO applications of companies involved in nucleic acid testing, adhering to strict review standards, with a particular focus on their sustainable operational capabilities. Yeasen became the first company to have its IPO application review canceled following the issuance of the new regulations.

The Industry Faces Its Most Severe Public Opinion Crisis

This may be the most severe public opinion crisis faced by “companies involved in nucleic acid testing” since the COVID-19 pandemic.

Let us first outline the timeline of the public opinion escalation.

Over the past three years of the pandemic, the general public has endured the hardships of nucleic acid testing. Although continuous price reductions under medical insurance and centralized procurement by the National Medical Products Administration have driven down the cost of COVID-19 testing to its limit, nucleic acid testing continues to contribute to these companies’ revenue.

Following the overnight statements from the Shanghai and Shenzhen stock exchanges, public attention has turned to companies involved in nucleic acid testing. Coinciding with the earnings season, data on the revenue for the first three quarters of 2022 for several leading nucleic acid testing-related enterprises have been compiled. Notably, companies such as Andon Health, Dian Diagnostics, and KingMed Diagnostics reported revenues exceeding RMB 10 billion, while Ruizhi Medicine, Anxu Biotechnology, and YHLO Biosciences posted net profit growth rates surpassing 400%, figures that stand out prominently in the current market environment. In addition, the approval materials of some nucleic acid testing-related companies awaiting IPO listing have also come under “scrutiny.”

The “pandemic dividends” reaped by these companies appear particularly glaring at present, with public opinion reacting as if fanning the flames.

Subsequently, the media reported that in a residential community in Guangzhou, 15 individuals initially tested positive for COVID-19, but 11 of them later tested negative upon retesting. In Lanzhou, Gansu Province, an incident occurred where individuals designated as “positive cases for transfer” were found to have negative nucleic acid test results. These various irregularities and violations have sparked public outrage, suspicion, and unease.

Notably, on November 25, the Health Commission of Lanzhou City, Gansu Province, reported that staff at Lanzhou Hezi Huaxi Laboratory (hereinafter referred to as “Lanzhou Huaxi”) had mistakenly uploaded the list of individuals with abnormal nucleic acid test results into the data package for negative cases in the work system. Lanzhou Huaxi is a wholly-owned subsidiary of Hezi Gene. This incident brought Hezi Gene and its actual controller, Zhang Shanshan, into the spotlight, with allegations of fraud becoming the focal point and triggering the largest wave of public opinion outcry.

The business models of nucleic acid testing companies that were established or rapidly expanded during the pandemic have been successively exposed. On November 29, the National Health Commission stated that it would continue to strengthen regulatory oversight.

From testing agencies to medical device companies, and further to upstream firms represented by Yeasen, it can be said that this wave of public opinion has impacted an exceptionally broad segment of the industry. For a time, voices from within the industry appeared particularly muted amidst the surging tide of public discourse.

An executive at an upstream IVD company lamented to VCBeat, “Public opinion has become somewhat intense lately, so we are hesitant to speak out.” However, he added, “The vast majority of nucleic acid testing companies are professional and conscientious entities that have contributed to epidemic prevention and control. The illegal monopolistic practices of a small minority should not be used to slander the entire industry.”

Some companies involved in nucleic acid testing have also come forward to clarify their positions. For instance, Wu Hongxiang, Board Secretary of Dakewei, stated in an interview with Nandu Bay Finance that Dakewei is not a “nucleic acid concept” company, with nucleic acid-related business accounting for only about 8% of its revenue. He emphasized that since its establishment in 1999, the company’s core business has been scientific research agency services and the R&D, production, and sales of medical devices. Currently, Dakewei has submitted its registration application and is on the verge of going public. However, it has faced criticism for allegedly earning RMB 840 million annually from nucleic acid sampling tubes, placing it under intense public scrutiny.

On November 26, Song Haibo, an expert in the IVD industry, published an article expressing strong support for companies involved in nucleic acid testing, which was widely shared by many industry professionals.

Song Haibo is Vice President of the Shanghai Institute of Experimental Medicine, President of the National Branch of the Medical Laboratory Industry, and Secretary-General of the Branch of Experimental Medicine. The article states, “It is understandable that under the heavy pressure of the pandemic over the past three years, the trigger for a public opinion incident may merely have been an outlet for online emotions; however, we should respond calmly, fairly, and objectively to emotional outbursts online that are clearly inconsistent with the facts.”

He also addressed the claim that “companies involved in nucleic acid testing enjoy high gross margins,” pointing out that high gross margins are closely tied to high levels of market monopoly. However, for every product offered by China’s in vitro diagnostic (IVD) companies, there are dozens or even hundreds of firms engaged in robust market competition, with highly transparent pricing and rare instances of monopolistic profiteering. In reality, after deducting costs, the gross margin for nucleic acid testing is not high. The primary reason most manufacturers of epidemic-prevention-related products have been profitable is the substantial scale effect driven by huge market demand, characterized by thin margins but high sales volumes.

“How Much Money Did ‘Nucleic Acid Testing-Related Companies’ Actually Make from COVID-19?”

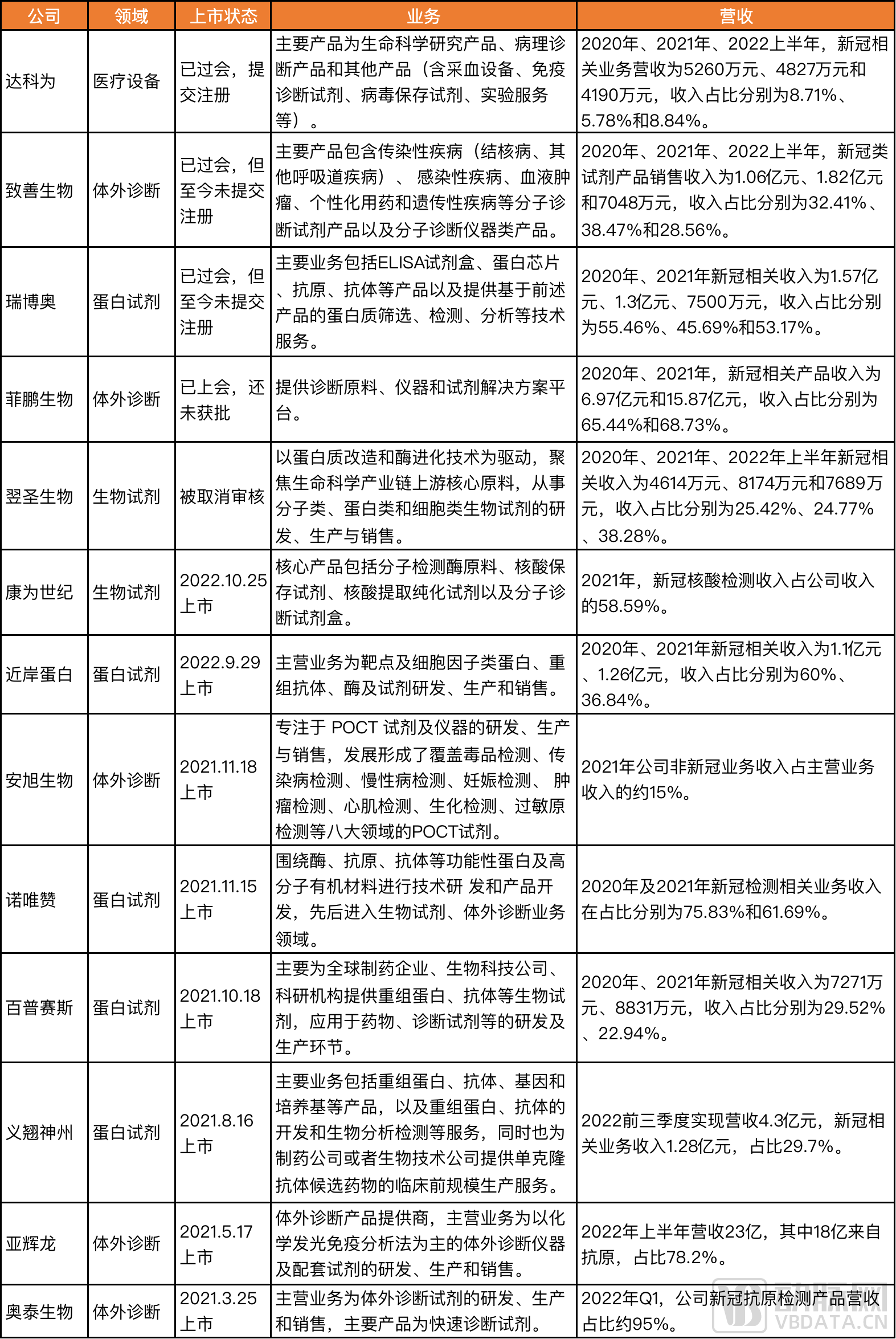

So, have all “nucleic acid testing-related companies” made a fortune from COVID-19? VCBeat New Medicine has compiled the core businesses of certain “nucleic acid testing-related companies” listed or awaiting listing on the ChiNext and STAR Market since the outbreak, along with the proportion of their COVID-19-related revenue in total revenue:

Data compiled from company financial reports, prospectuses, earnings briefings, etc.

An analysis of the compiled data reveals that the majority of “nucleic acid testing-related companies” listed on the STAR Market and ChiNext in the past two years are upstream IVD reagent manufacturers, rather than the ad hoc “testing laboratories” commonly perceived by the public.

This sector has indeed become a key battleground for domestic substitution in recent years. The Chinese IVD market has long been dominated by overseas giants, which hold more than 50% of the market share. In particular, the localization rate for chemiluminescence immunoassays stands at only 20%. Most instruments feature closed-system designs, requiring downstream customers to continuously purchase high-priced reagents. Few domestic companies possess the capability to manufacture both instruments and reagents; however, China’s IVD industry has been steadily closing the technological gap in recent years.

The COVID-19 pandemic served as a catalyst, drawing the attention of capital markets to the upstream in vitro diagnostics (IVD) sector and providing these companies with opportunities to raise funds on secondary markets, expand their operations, and break the monopoly held by foreign giants.

A founder of a relevant company stated, “Previously, the focus was largely on the clinical market, with little willingness to invest in the upstream raw materials sector. However, the pandemic has thrust the raw materials industry into the spotlight, leading to a sharp surge in capital investment interest.”

Based on the disclosed revenue figures,While COVID-19-related businesses have indeed significantly boosted the performance of these companies, such operations account for a relatively modest proportion of revenue for many firms, with some even experiencing a year-on-year decline in their COVID-19-related business.

Taking ACROBiosystems as an example, although its COVID-19-related business has driven performance growth for more than two consecutive years, the proportion of revenue from this segment to total revenue has declined significantly even as absolute income increased. The share of COVID-19-related business dropped from 29.52% in 2020 to 18.6% in the third quarter of this year. Moreover, the company’s COVID-19-related offerings are primarily applied in vaccines and therapeutics rather than diagnostics, implying greater sustainability. In other words, COVID-19 has had a relatively limited impact on the company’s revenue and valuation.

ACROBiosystems’ core products are recombinant proteins. Recombinant proteins, obtained through genetic engineering and cell engineering technologies, possess specific functions and biological activities, serving as indispensable key biological reagents in the research, development, and production of biopharmaceuticals, cellular immunotherapies, and diagnostic reagents. As one of the leading domestic suppliers of recombinant proteins, ACROBiosystems primarily serves large industrial pharmaceutical companies, including global Top 20 pharmaceutical enterprises such as Johnson & Johnson and Pfizer, as well as renowned Chinese biopharmaceutical companies like Hengrui Medicine and Innovent Biologics.

In September this year, Novoprotein Scientific Inc., another protein reagent company that went public ahead of the new regulations issued by the Shanghai Stock Exchange, also has a presence in nucleic acid testing business but primarily focuses on the field of mRNA raw material enzymes.

An analysis of the development history of Novoprotein Scientific Inc. reveals that it was only after the 2020 pandemic that the company formally commenced large-scale production of mRNA raw material enzymes. The pandemic accelerated the development of mRNA vaccines, thereby driving Novoprotein’s revenue growth. In 2021, Novoprotein seized market opportunities to become one of the primary suppliers to major domestic mRNA vaccine developers, including Walvax Biotechnology and Abogen Biosciences, generating approximately RMB 130 million in revenue from its mRNA raw material enzymes and reagents.

However, mRNA raw material enzymes belong to the upstream segment of the mRNA industry chain, feature a high degree of innovative value, and represent a key link in the value chain. It is reported that the product specifications of Novoprotein’s mRNA raw material enzymes have already reached an internationally advanced level.

Even Yeasen, whose IPO application was “rejected” by the Shanghai Stock Exchange, is essentially a company focused on molecular enzymes rather than a pure upstream supplier for nucleic acid testing. Before 2020, over 80% of molecular enzymes were imported, reflecting high barriers to entry and significant production challenges. Since the onset of the COVID-19 pandemic, increased capital attention toward life science tools has enabled companies like Yeasen to rapidly expand by upgrading their instrumentation and manufacturing facilities.

Molecular enzymes not only play a role in COVID-19 testing but, more importantly, serve as key raw materials for high-end precision oncology diagnostics. In the field of precision oncology diagnostics, which primarily focuses on early cancer screening and companion diagnostics, Yeasen provides high-quality products and enzyme reagents compatible with both PCR and NGS technology platforms. Previously, Yeasen also stated in an interview that the company is expanding its portfolio of innovative technologies, including upstream raw materials for cell therapy, gene therapy, organoids, and synthetic biology.

Therefore, it is overly arbitrary to broadly categorize these companies together as nucleic acid testing enterprises.

We have also compiled a brief list of “nucleic acid testing-related companies” listed on the main board. In terms of establishment date, these are all well-established diagnostic reagent companies. Regarding their listing dates, the vast majority went public before the COVID-19 pandemic, rather than packaging themselves for an IPO to cash in on the pandemic-driven boom.

Data compiled from public information

A closer look at revenue figures reveals that some companies derive their primary income not from domestic nucleic acid testing. For instance, Andon Health’s semi-annual report shows overseas sales reaching RMB 22.9 billion, with the United States as its largest market, while domestic sales amounted to only RMB 300 million.

As for Wantai Bio, its semi-annual report shows that its COVID-19 antigen products are mainly sold to EU countries. Meanwhile, the company’s other flagship product, the bivalent HPV vaccine, has helped drive rapid growth in its revenue and profits.

However, since the onset of the COVID-19 pandemic, most of these companies have experienced a “sell-off” following a “buying frenzy,” driven by shifts in public and market sentiment and expectations toward nucleic acid testing. Demonstrating their future value has become a critical challenge they must address.

Moving Beyond the COVID-19 Narrative to Find a Sustainable Growth Curve

Another focus of public opinion is whether “companies involved in nucleic acid testing” have any future.

The recent actions taken by the China Securities Regulatory Commission (CSRC) and the Shanghai and Shenzhen Stock Exchanges are primarily aimed at addressing the following issues:Are Companies Involved in Nucleic Acid Testing Eligible to Raise Funds in the Secondary Market?Because stocks are permanent bonds and financing instruments, while the nucleic acid testing business is short-term and unsustainable.

Particularly, companies such as Yeasen have filed for listing review on the STAR Market.Innovative attributes must withstand scrutiny. The suspension of Yeasen’s IPO review may be attributed to the rapid increase in the proportion of revenue from COVID-19 testing services since its entry into the nucleic acid testing market in 2020, coupled with a sharp decline in net profit, which has raised market concerns about the core profitability and sustainability of the company’s conventional business.

While the pandemic-related business did give these companies a revenue “boost,” valuations in the secondary market often price in future growth expectations in advance; only sustainable growth can keep them “soaring.”

Many companies have gradually shifted from leveraging COVID-19-related concepts during the early stages of the pandemic to distancing themselves from such associations.Companies that achieved growth during the COVID-19 pandemic are also grappling with how to balance their COVID-related and non-COVID businesses. An analysis of the prospectuses of companies that passed regulatory review this year, as well as the annual reports of listed companies, reveals that many firms are delineating between their COVID-related and non-COVID business segments.

For instance, at the onset of the COVID-19 pandemic in early 2020, Sino Biological swiftly developed a series of COVID-19-related reagent products, leveraging this opportunity to significantly enhance its brand influence. However, in its report this year, the company emphasized the growth trajectory of its non-COVID-19 businesses. For example, revenue from non-SARS-CoV-2-related businesses reached RMB 302 million in the first three quarters of 2022, representing a year-on-year increase of 12.58%; revenue from these businesses in Q3 amounted to RMB 111 million, a year-on-year increase of 18.06%.

For another example, YHLO recently stated that the profits from its COVID-19-related business have generated cash flow for the company, which has been reinvested into R&D for its non-COVID-19 core businesses, significantly accelerating the development and market launch of new non-COVID-19 products.

The head of Yeasen also stated to VCBeat New Medicine prior to the IPO that, following rapid growth, the company would focus on expanding its product portfolio and overseas markets to prepare for global and long-term competition, with the ultimate goal of becoming a cornerstone company in the life sciences tools industry.

It is undeniable that some so-called “genetic testing companies” and “nucleic acid testing laboratories” were rapidly established and expanded during the pandemic, carving out market share to reap exorbitant profits. However, it is impossible for these companies to go public solely on the basis of nucleic acid testing, as the capital market is unlikely to accept companies lacking growth potential and technological substance.

In particular, the ChiNext and STAR Market were established to support China’s technology-driven innovation industries. Oriented toward the global technological frontier, the main economic battlefield, and major national needs, they primarily serve technologically innovative enterprises that align with national strategies, have achieved breakthroughs in key core technologies, and enjoy high market recognition.

As is evident from the preceding analysis, the majority of “nucleic acid testing-related companies” that have gone public since the onset of the COVID-19 pandemic are life science tools manufacturers. Life science tools constitute a comprehensive system grounded in interdisciplinary innovation, which has long been monopolized by imported brands. Domestic enterprises must strive to master core technologies and accelerate the substitution of imported brands.

Song Haibo also pointed out in the aforementioned article that in the post-pandemic era, nucleic acid testing companies still have a promising future even without COVID-19-related business. He noted that technological advancement and corporate development follow general patterns; just as mRNA vaccine technology can be extended to various fields, the pandemic has similarly accelerated the adoption and improvement of many new testing technologies. “Leveraging the nucleic acid testing platform, we can develop numerous new testing assays. Many enterprises will undoubtedly utilize this technical pathway to create more and better in vitro diagnostic products, thereby serving the cause of public health.”

There will always be companies that make money in the current market environment,But we hope to make money from those companies that have contributed during the pandemic and are also the most innovative.