U.S. Healthcare VCs Are Rallying Around Women's Health: FemTech Emerges as a Top Investment Priority

JINXIN FERTILITY

Assisted Reproductive Technology Service Provider

In 2022, U.S. venture capitalists collectively turned their attention to women’s health.

According to incomplete statistics from VCBeat’s Orange Fruit Bureau, as of November 15, 2022, a total of 210 early-stage financing deals were completed in the U.S. healthcare sector. Among these, 20 deals occurred in the women’s health segment, accounting for 9.5% of the total and making it the subsector with the highest number of early-stage healthcare financings in the United States this year.

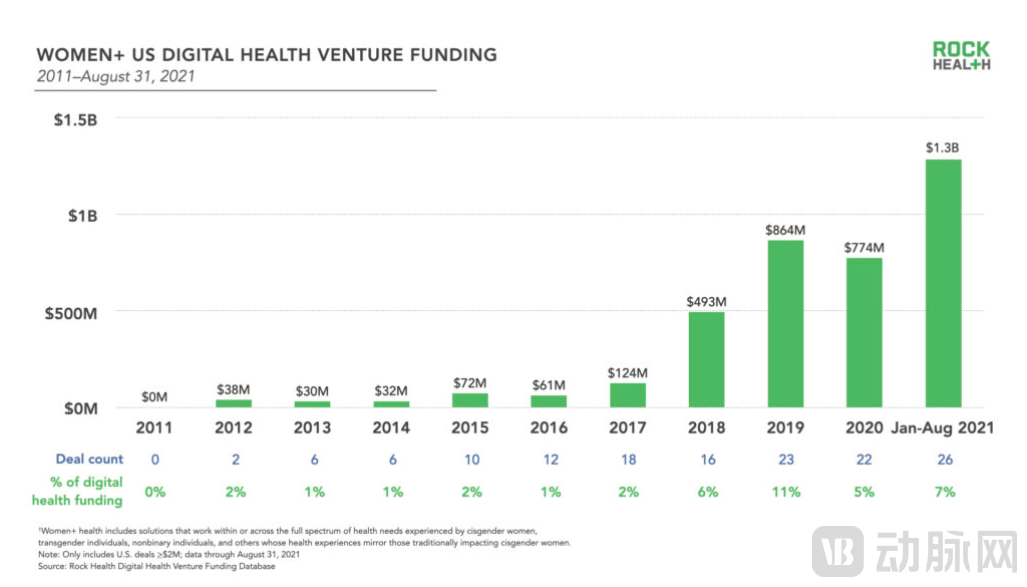

This is indeed somewhat surprising. Over the past decade, only 74 companies in the U.S. women’s health sector have secured financing, raising a total of $3.8 billion. Such a modest funding volume has hardly made any waves in the U.S. healthcare market.

However, starting in 2021, this unassuming niche sector began to attract collective enthusiasm from U.S. venture capitalists. Reportedly, 2021 marked the peak year for financing activity in U.S. women’s health enterprises over the past decade, with a total of 24 funding rounds completed throughout the year, including eight early-stage deals, accounting for 33.3%.

Entering 2022, this momentum has intensified further, with 20 early-stage deals already completed. So, what exactly is the underlying industrial logic? And what new opportunities can we identify in the women’s health sector?

From Being Overlooked by U.S. VCs to Becoming a Bet on the Future

In fact, there is a specialized term for women’s health in the international arena: “FemTech.” Coined in 2016 by Danish entrepreneur Ida Tin, the term aims to legitimize the women’s health technology market, thereby fostering innovation, attracting investment, and breaking down the barriers and taboos surrounding women’s health.

Since then, the global women’s health industry has gained momentum, with the United States taking the lead. According to statistical data, in 2017, the average age of companies in the U.S. women’s health sector was four years, and none had secured Series C financing. By 2021, the average age of startups in this field had risen to six years, with 31% of financing rounds occurring at Series C or later, while seed-stage funding accounted for 50% of the total. This indicates that both early-stage startups and mature enterprises in the U.S. women’s health sector have attracted significant attention from the capital markets.

This is certainly not without reason; the most critical factor is the gradually “visible” market demand. For a long time, women’s health was an overlooked industry, perpetually burdened by bias. It is reported that prior to 2011, only 3% of U.S. venture capital funds were dedicated to women’s health, and even those focused exclusively on reproductive health.

In fact, the health needs of American women are becoming increasingly diverse. In a recent report on women’s health in the United States, “mental health” was identified as the most pressing health issue facing American women, accounting for 27% of the total responses.

According to statistics, 22.3% of adult women in the United States suffered from some form of mental illness in the past year. Among women aged 18 to 21, major depressive episodes with serious suicidal ideation were most prevalent, directly contributing to the U.S. female suicide rate reaching a historic high of 2% in 2021.

Unlike young women, middle-aged women in the United States primarily face mental health challenges stemming from postpartum depression, menopause, and appearance-related anxiety. In recent years, an increasing number of American women have begun seeking treatment for mental health issues; however, there are very few therapeutic options available to them.

The second biggest health concern for American women is “cancer,” but the leading cause of cancer-related deaths is not breast cancer, but lung cancer. According to data from the U.S. Cancer Center, although breast cancer had the highest incidence rate among American women in 2021, lung cancer accounted for the highest mortality rate at 25%.

According to a research paper from Stanford University and the University of California, San Francisco, the incidence of lung cancer in the United States has declined from 67 to 43.2 cases per 100,000 people over the past two decades. However, the rate of decline has been slower among women than men, with an increasingly pronounced trend toward younger onset. The study also analyzed the underlying causes, identifying “cooking oil fumes” as the primary culprit behind the persistently high lung cancer incidence among American women in recent years.

The third most pressing women’s health issue in the United States is maternal health. A 2022 report by the March of Dimes indicated that up to 6.9 million women across the country had little or no access to maternal healthcare services, directly affecting nearly 500,000 newborns in the United States.

Additionally, according to National Public Radio (NPR), the findings from the March of Dimes indicate disproportionate harm to rural communities and people of color: one in four Native American infants and one in six Black infants are born in areas with no or limited access to maternal health care services.

Mothers and infants in maternal healthcare “deserts” in the United States are facing heightened health risks, including death. The report states that approximately 900 women in the U.S. died from pregnancy-related causes in 2021, yet nearly two-thirds of these deaths were preventable. This further underscores the critical importance of maternal health services for American women.

Beyond the gradually expanding and diversified market demand, the second core reason why the U.S. women’s health sector has become a hotly contested target for venture capital (VC) firms in recent years is the rise of female power. Here, “female” carries two connotations: female partners at VC funds and female founders of women’s health companies.

Prior to 2011, the industry attributed the underinvestment in the U.S. women’s health sector largely to the scarcity of women in venture capital investment roles. According to statistical data, approximately 64% of U.S. venture capital firms did not have a single female partner during that period.

This “gender gap” has begun to narrow in recent years. On one hand, women are increasingly becoming co-decision-makers, managing venture capital funds alongside men. This gender-balanced approach has yielded significant results in the U.S. VC sector in recent years. According to data from Amplifyher Ventures, mixed-gender teams in venture capital outperform all-male teams by 63%.

On another front, women have begun to independently manage venture capital funds. Sogal was the first female-led venture capital firm of the millennial era and has now invested in over one hundred startups. Tola Capital, Seattle’s largest VC fund, was founded by two women, with more than half of its core management team also being female. The investment team at The Jump Fund is entirely female; since its inception, it has raised two funds and invested in more than 30 female-led startups.

In addition to serving as venture capital partners, women in the United States have increasingly embarked on entrepreneurial paths in recent years. According to data analysis, over 70% of female health startups founded in the U.S. in the past five years have at least one female founder. In the Los Angeles area, the funding success rate for female-founded startups even exceeds the national average.

Female founders’ leadership capabilities have also gained market recognition. A study by Boston Consulting Group found that for every dollar invested, startups founded by women generate 78 cents in profit, whereas those founded by men yield only 31 cents. Female founders are increasingly becoming the next “bet” for U.S. venture capital firms.

What Types of Female-Founded Startups Are U.S. VCs Seeking This Year?

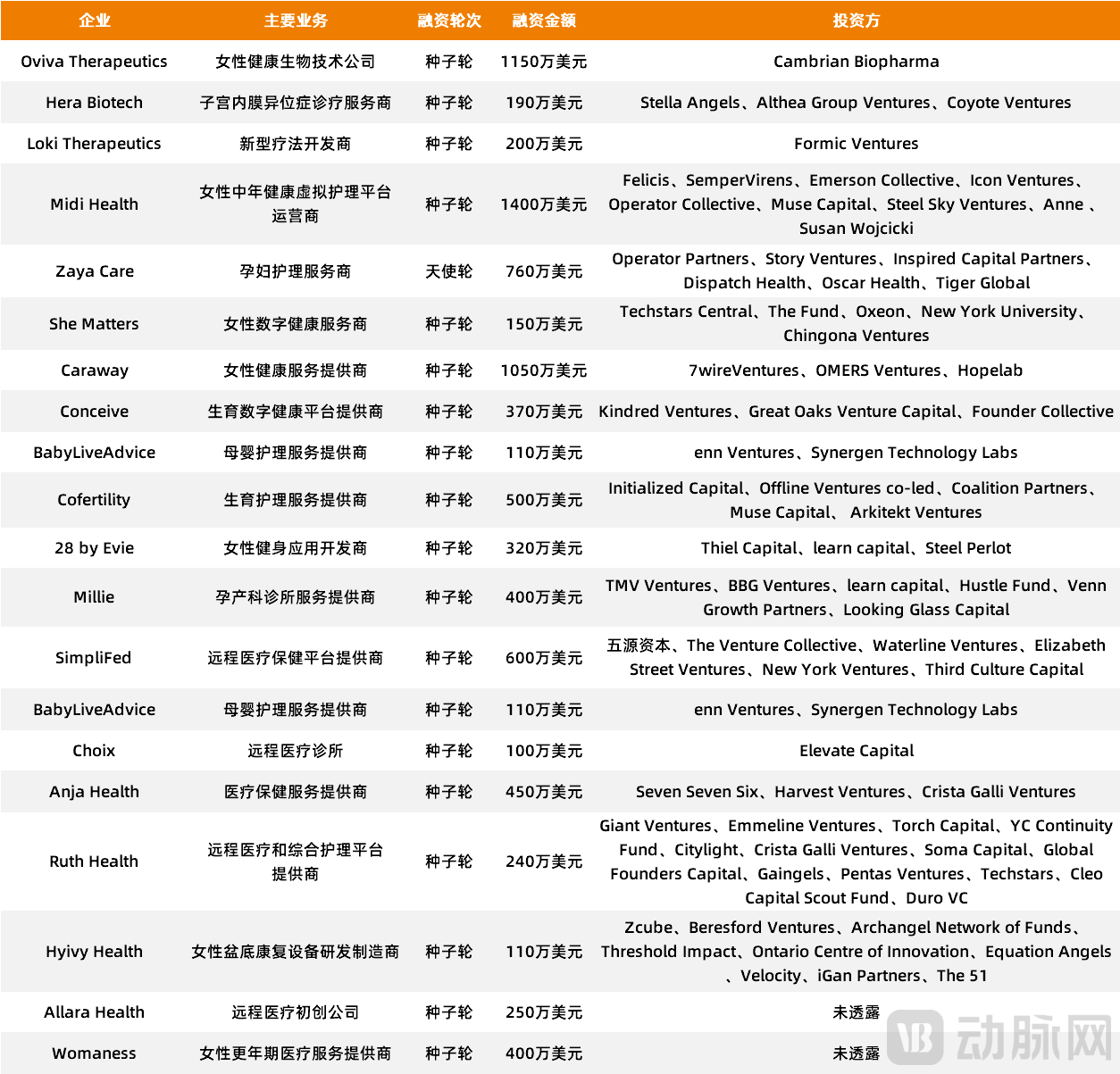

The surge in U.S. venture capital interest in women’s health has been confirmed as a genuine trend. So, which early-stage startups are capturing their attention? VCBeat conducted a systematic analysis of 20 companies that secured early-stage financing this year and identified the following three key trends:

Point 1: Digital health products are mainstream. According to statistics, among 20 startups, 10 are digital health companies, accounting for half of the total.

In recent years, the digitalization of healthcare has become a major global trend. The development of the internet and emerging technologies has accelerated the advancement and widespread application of digital health technologies, making them an effective entry point for transforming the current state of the healthcare industry. In the realm of women’s health, digital healthcare not only provides more medical options but also further enhances diagnostic and treatment efficiency, while breaking down spatial and temporal barriers. This is particularly evident for pregnant women, for whom digital health technologies are playing a significant role.

BabyLiveAdvice, a virtual maternity telehealth provider that primarily offers women virtual, real-time maternal education classes, completed a $1.1 million seed funding round this September. SimpliFed closed a $6 million seed round in May; its core business is providing virtual breastfeeding services to improve women’s access to high-quality care while reducing costs. Additionally, SimpliFed addresses the issue of maternal sleep deprivation.

Second, women’s health services have become more comprehensive and diversified. For a long time, the women’s health industry was equated directly with assisted reproductive technology (ART), but in recent years this “bias” has eased in the United States. Reportedly, among the 20 companies that completed early-stage financing this year, only one was directly related to ART. Overall, the women’s health industry is becoming more empathetic and more innovative.

Caraway completed a $10.5 million seed funding round this July. It is a digital health company providing comprehensive psychological, reproductive, and physical healthcare services to female college students. The company’s team comprises gynecologists, psychiatrists, family physicians, adolescent specialists, therapists, nurses, and care coaches, ensuring that women can access the necessary care services when needed.

Cofertility closed a $5 million seed funding round this October. The startup primarily offers two programs for women: Keep and Split. Through Keep, women can pay to freeze their eggs and store all of them for their own future use, while the Split program allows women to freeze their eggs for free in exchange for donating half of them to families struggling with infertility.

As for menopausal women, U.S. venture capital firms are also actively expanding their presence. Midi Health completed a $14 million seed funding round in October this year. It is a comprehensive virtual care clinic targeting women undergoing midlife hormonal transitions, primarily providing specialist care, hormonal and non-hormonal medications, supplements, lifestyle guidance, and essential preventive health advice to perimenopausal and menopausal women.

The third point is to explore new methods for treating ovarian cancer. Ovarian cancer is a common malignant tumor among women in the United States. In recent years, although the incidence of ovarian cancer in the U.S. has been declining and treatment options have continued to improve, its mortality rate remains high compared to other female cancers. The five-year survival rate is only 49%, which is significantly lower than the 90% five-year survival rate for breast cancer in the United States.

Among the 20 companies that secured early-stage financing this year, three are focused on ovarian cancer treatment and have introduced novel solutions.

Loki Therapeutics completed a $2 million seed financing round in January this year. The company’s primary development project is AWAKE-LM-TT, which leverages the childhood tetanus toxoid (TT) vaccine to elicit immune responses against solid tumors and metastases that present tetanus antigens. Loki Therapeutics is currently advancing AWAKE-LM-TT as a potential treatment for metastatic pancreatic cancer and metastatic ovarian cancer.

Oviva Therapeutics completed a $11.5 million seed financing round in May this year. Co-founded by Dr. Daisy Robinton, a molecular biologist from Harvard University; Dr. Patricia Donahoe, a tenured professor of surgery at Harvard Medical School; and Dr. David Pépin, an associate professor at Harvard Medical School, the company is dedicated to researching and developing novel therapeutics addressing female physiology. Starting with a focus on ovarian aging, Oviva aims to tackle the significant unmet needs in women’s health and extend female lifespan.

According to Acumen Research & Consulting, the global women’s health market reached $25.3 billion in 2021 and is projected to expand to $97.3 billion by 2030, with a compound annual growth rate (CAGR) of over 16% from 2022 to 2030. After decades of neglect, the women’s health market is now demonstrating significant growth potential.

Meanwhile, countless imaginative founders are rapidly entering this high-growth-potential sector, and the future needs of women’s health are being viewed from a broader perspective that extends beyond reproductive health.

Is There No Market for Women's Health in China?

The extent to which women’s health in China is overlooked by the capital market is no less than in the United States, and may even be more pronounced. According to incomplete statistics from VCBeat Orange Data, only 33 financing deals have occurred in the women’s health sector from 2019 to present, with just nine of these exceeding RMB 100 million. Over the past three years, the total financing amount in this sector has been approximately RMB 2.6 billion.

Turning our attention to the early stage, as of October 1, 2022, none of the 194 early-stage investment and financing transactions that had occurred in China’s healthcare sector involved startups directly focused on women’s health.

Does this prove that there is no market for women’s health in China? The answer, of course, is no.

First, from the perspective of cancer. In China, there are approximately 100,000 new cases of cervical cancer each year, with about 30,000 deaths. Among malignant tumors of the female reproductive system in China, cervical cancer ranks first in both incidence and mortality rates. Regarding breast cancer, China sees approximately 420,000 new patients annually. In recent years, the annual incidence rate has been increasing by 3% to 4%, with a increasingly pronounced trend toward younger age groups.

Secondly, from the perspective of female reproductive services. With the adjustment and improvement of China's fertility policies, the proportion of advanced maternal age pregnant women in China has also increased. According to data, the number of such pregnant women in China exceeded 3 million in 2020. Moreover, these women face greater pressure during pregnancy and childbirth, and their needs for prenatal care and mother-infant management are often more pronounced. However, the market penetration rate of postpartum care centers in mainland China remains very low, far behind that of regions such as Taiwan, China, and South Korea.

Finally, from the perspective of menstrual health services. Currently, the age range for menstruation among women in China is extending at both ends, with a rising proportion of individuals experiencing dysmenorrhea and irregular menstruation. Meanwhile, the incidence of dysmenorrhea in China is also on the rise. According to incomplete statistics, as early as 2019, the prevalence of dysmenorrhea among Chinese women reached 33.1%, with severe cases accounting for 13.55%. Data from the Dama Yi (Big Auntie) app in China shows that in 2021, 55% of users had recorded symptoms of dysmenorrhea; among them, 57% experienced mild dysmenorrhea, 33% moderate dysmenorrhea, and 10% severe dysmenorrhea.

In addition to the rising visible clinical needs of women, awareness of self-care among women has also strengthened in recent years, with significant improvements in their willingness to pay and purchasing power.

Maternal Health Care in China: According to data from the National Health Commission of China, the national prenatal examination rate reached 97.4% in 2020, an increase of 0.8 percentage points compared with 2018; the postpartum visit rate reached 95.5%, up by 1.7 percentage points from 2018; and the hospital delivery rate stood at 99.9%, basically unchanged from 2018. Specifically, in 2020, the hospital delivery rate in urban districts nationwide reached 100.0%, while that in county towns was 99.9%, both representing a 0.1-percentage-point increase over the 2018 figures.

Despite this, the women’s health sector in China remains a tranquil blue ocean, awaiting more “pebbles” to be cast in to create greater ripples. However, identifying these “pebbles” and deploying them into the blue ocean is not as straightforward as it may seem; at the current stage, numerous challenges persist.

First, from the source perspective, the number and scale of laboratories or research institutes in China focused on women’s health are relatively small, making it difficult to incubate scientific achievements with significant market prospects in the short term. Second, regarding industrial focus, 95% of China’s women’s health sector concentrates on reproduction or maternal and infant care. As leading enterprises have already emerged in these two fields, it is challenging for startups to enter. Moreover, startups lack sufficient innovative vision to open up new niche segments.

Finally, from the perspective of “her” power: although women have demonstrated increasingly significant value in China’s healthcare sector in recent years, their representation remains exceedingly low, whether in terms of female partners at venture capital (VC) firms or female founders. The future development of the women’s health industry will require greater engagement and influence from women.

According to statistics, in the 20 early-stage financing deals completed this year in the U.S. women’s health sector, a total of 85 venture capital (VC) funds participated as investors. This scale of investment and level of attention are unprecedented. Furthermore, many U.S. VC firms have stated this year that they will explore more opportunities in the women’s health market, making it their next major “bet.” This presents an opportunity for the U.S. women’s health industry and may also bring new possibilities to China’s women’s health sector.