China's Smart Pathology Industry White Paper Released: Commercialization Emerges, Addressing Breakthroughs and Challenges in Pathology AI

As the “gold standard” for diagnosing the vast majority of diseases, particularly cancer, pathological diagnosis has earned pathologists the title of “doctors’ doctors.” Academician Zhong Nanshan once inscribed for the Chinese Journal of Pathology: “The level of clinical pathology is an important indicator of a nation’s healthcare quality.” In current oncology treatment, pathological diagnosis carries increasing weight in molecular subtyping and the assessment of existing therapeutic efficacy. Pathological results directly influence the selection of subsequent treatment plans and determine patients’ health and survival. At first glance, pathological diagnosis might seem like a highly promising field, but the reality is quite the opposite.

Because they operate “behind the scenes,” pathology professionals often self-deprecatingly refer to their department as the hospital’s “corner specialty.” In stark contrast to the high technical sophistication of their medical services, pathologists are among the lowest-paid staff within the hospital’s diagnostic and technical departments. We have witnessed the “race against time” in emergency departments and the “heart-stopping drama” of surgical suites through numerous films and television series. Yet the quiet dignity of pathologists, who summarize their careers as “a lifetime spent with a microscope, reviewing tons of histopathology slides,” seems to go unrecorded at the moment of their retirement.

The pathology diagnostics industry is trapped in a vicious cycle of “slow professional development, difficulties in departmental growth, and recruitment challenges.” While the demand for pathology diagnostics in China is substantial and rising rapidly year by year, the industry faces a shortage of pathologists and a severe imbalance in the distribution of pathological resources.Imbalance Between Supply and Demand in the Pathology Diagnosis Industry Urgently Calls for Effective Tools to Break Through Development Bottlenecks. The emergence of digital and intelligent pathology, by enhancing the work efficiency of pathologists and facilitating the decentralization of high-quality expert resources, serves as a potent remedy for the industry’s pain points. It drives transformation and reform within the traditional pathology diagnosis sector, guiding pathology departments from the “backstage” to the “frontline.”

The present moment represents a critical juncture in the development of the smart pathology industry. The continuous advancement of the “four modernizations” within the pathology sector, the localization of digital pathology equipment, the ongoing accumulation of pathological data, enterprises’ exploration of diverse and flexible business models, and the relentless decline in storage costs driven by Moore’s Law have all laid fertile ground for the further maturation of smart pathology.

What development opportunities are emerging in the industry? What commercialization explorations have leading startups undertaken, how are they currently implementing their solutions, and what are their future growth strategies? Who will secure the first Class III medical device registration certificate for “pathology + AI,” and when? What challenges does the industry face amidst its rapid development? What are the future trends of the industry, and where lies the tipping point for explosive growth? ……

VCBeat Institute conducted over 40 hours of in-depth discussions with nearly 20 frontline entrepreneurs, senior pathology experts, and prominent venture capitalists seeking investment opportunities. It produced the “White Paper on China’s Smart Pathology Industry” to address the aforementioned questions, aiming to showcase the dynamic transformation underway in the pathology diagnostics sector and analyze its future development trends for industry professionals.

1The Latest Stage in the Development of Pathological Diagnosis: The Era of Digital and Intelligent Pathology

In ancient times, 2,000 years ago, humanity embarked on the earliest pathological explorations through methods such as cadaveric dissection. It was not until the 1930s, with the advent of the electron microscope, that the era of ultrastructural pathology began. Pathological research transitioned from the cellular and subcellular levels to the molecular level, initiating investigations into the etiologies and pathogenic mechanisms of diseases. Entering the 21st century, the field of life sciences has witnessed rapid advancements. A series of new methods, technologies, and equipment have been increasingly integrated into pathological research and diagnosis. In the era of precision pathology, bolstered by technologies such as the internet and artificial intelligence, the dawn of digital and intelligent pathology has arrived.

In 2012, remote pathology diagnosis began to be promoted in China. Around 2015, driven by strong national support for “Internet + Smart Healthcare,” the adoption rate of remote pathology consultation in China rose rapidly. The development of remote pathology consultation has enabled traditional pathology diagnosis and consultation models to break through temporal and spatial constraints, significantly improving the quality and efficiency of pathological diagnosis in medical institutions.

Constrained by practical national conditions, China’s pathology diagnostics industry has developed more slowly and insufficiently in digitalization compared with developed countries in Europe and the United States. For a long time, the majority of pathology diagnostic practices have adhered to the traditional manual model of “one microscope plus histopathological slides.” Nevertheless, the development and accumulation in digital pathology have laid a solid foundation for the intelligent transformation of pathology diagnostics in China, enablingInFrom 2016 to 2017, China largely kept pace with the global community in launching the development of smart pathology.

China’s Entry into Different Stages of Development in the Digital and Smart Pathology Era

Source: Survey interviews; chart by VCBeat

The emergence of smart pathology has not only enhanced the diagnostic efficiency of pathologists and addressed the uneven distribution of pathological resources, but also powerfully driven the digital transformation of the pathology industry.

Current smart pathology typically refers to mainstream AI-assisted pathological diagnosis, but this represents only a portion of the application scenarios for smart pathology. At present, the advancements in conventional pathological sample preparation are limited to automated processes such as dehydration, embedding, and staining, and there is still a lack of integration based on lesion visualization information (including clinical and molecular imaging, etc.).Automated and Intelligent Sample Collection, based on the individualized characteristics of organ tissuesSmart Sample Preparation and Quality Control(including immunohistochemical staining and molecular pathology), etc.

Smart pathological diagnosis is not limited to auxiliary diagnosis based on the morphological features of tissues and cells; rather, it integrates patients’ clinical symptoms and signs, laboratory test results, imaging data, pathological morphology, immunohistochemistry, and molecular pathology to achieve an integrated diagnosis via the “pathological phenome” obtained through artificial intelligence–assisted diagnostic systems.Integrated AI-Assisted Pathological Diagnosis: The Next Generation of Diagnostic Pathology(Next-generation diagnostic pathology, NGDP)the core connotation.

Multimodal Diagnostic Paradigms of Artificial Intelligence in Precision Oncology

Source: Life Sciences journal; chart by VCBeat

In the future, big data from imaging, pathology, genomics, and other sources will be further mined, and the integration of artificial intelligence technologies with medical big data will continue to deepen.Intelligent diagnosis based on integrated pathological phenomics will open new avenues for the comprehensive quantification of tumor heterogeneity and enable precise prognostic prediction of malignant tumors.Empowered by artificial intelligence, humanity is accelerating into the NGDP era, enabling patients to receive more precise and personalized diagnosis and treatment.

2The pathology industry is currently facing numerous pain points, making the development of smart pathology imperative.

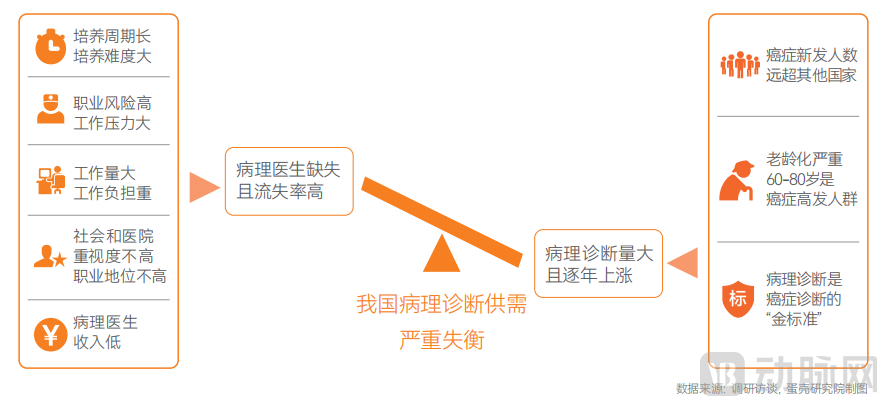

China has a large and growing cancer patient population, which is accelerating the release of market demand for pathological diagnosis. However, the country faces a shortage of pathologists and a severe imbalance in the distribution of pathological resources, leading to a supply-demand mismatch in the industry.

Figure 7: Severe Imbalance Between Supply and Demand in the Pathological Diagnosis Industry

Data source: Survey interviews; graphic by VCBeat

China is the world's most populous country, with the number of new cancer cases far exceeding that of any other country. In February 2022, the National Cancer Center released the latest national cancer statistics:In 2016, the number of new cancer cases in China was 4.064 million, which was 67.66% higher than the global average. Furthermore, as cancer incidence rates rise with age and China’s population aging accelerates, the number of cancer patients in China continues to increase.As pathological diagnosis serves as the “gold standard” for diagnosing the vast majority of diseases, particularly cancer, industry demand for pathological diagnosis has further increased.

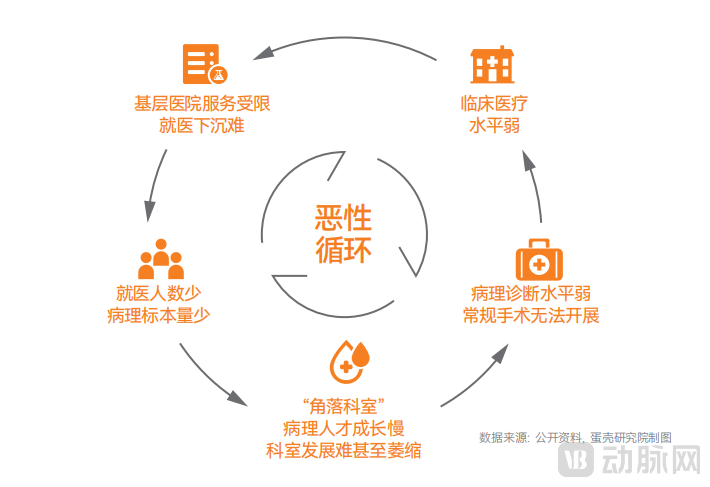

However, due to the existence of issues in China's pathology industryPathology departments face challenges such as the lengthy and difficult training process for pathologists, heavy workloads, and low income.Trapped in a vicious cycle of "slow talent development, difficult departmental growth, and inability to recruit talent,"This has led to a significant shortage of pathologists and a severe imbalance in the distribution of pathology resources.

Pathology Departments in China Are Trapped in a Vicious Cycle of “Slow Talent Development, Difficult Departmental Growth, and Recruitment Challenges”

Source: Public information; chart by VCBeat

According to the standard stipulated in the "Guidelines for the Construction and Management of Pathology Departments (Trial)" issued by the former Ministry of Health in 2009, which requires that "all secondary and tertiary hospitals shall establish pathology departments, with one to two pathologists allocated per 100 hospital beds,"As of the end of 2021, the demand for pathologists in China was approximately 141,700, while the existing number of pathologists was only 21,000, resulting in a shortage of up to 120,000 pathologists.According to the spot-check data from September 2019 released by the Bureau of Medical Administration and Hospital Management,Among the 9,620 hospitals subjected to nationwide spot checks, 5,758 did not have a pathology department or conduct pathology services, accounting for approximately 59.9% of the total number of hospitals inspected.. Pathologists and technical staff are in short supply, making it difficult to meet clinical demands.

Furthermore, an analysis of the distribution across hospitals of different tiers reveals a severe imbalance in the allocation of pathologist resources in China: according to statistics from the "2015 National Pathology Department Medical Quality Report," in 2014, China's61.8% of practicing pathologists are allocated to tertiary hospitals, while only 0.9% are assigned to primary hospitals,In 2014Level I hospitals account for 44.3% of all public hospitals.

The severe imbalance between supply and demand in the industry urgently calls for effective tools to break through the development bottleneck. To address the significant shortage of pathologists and the highly uneven distribution of pathology resources in China,Improving the work efficiency of pathologists and promoting the downward allocation of high-quality pathology expert resources are key to resolving industry challenges.

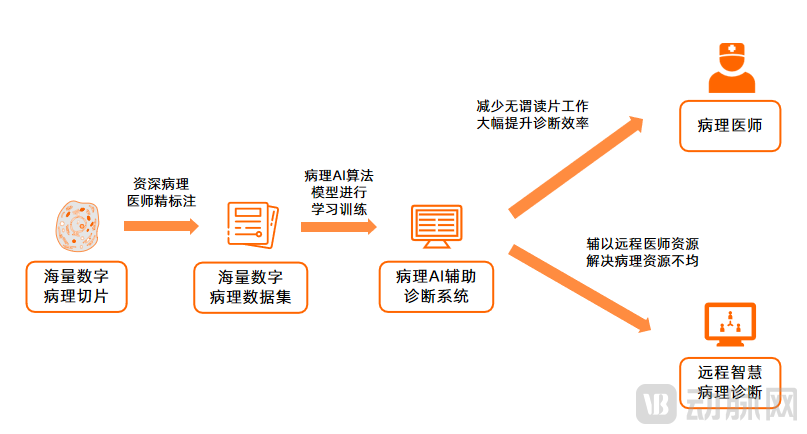

On the basis of digitizing pathological slides,Leveraging rich datasets derived from massive volumes of digitized pathology slides, and harnessing the powerful computational and deep learning capabilities of computers, AI-assisted diagnostic software can facilitate intelligent pathological slide interpretation.Process medical images in a rapid, standardized manner to identify pixels labeled as "tumor" within individual small regions, delineate and render suspicious findings, and provide auxiliary diagnostic recommendations.

Significantly Boosting Diagnostic Efficiency and Facilitating the Downward Distribution of High-Quality Pathology Expertise: AI-Assisted Pathology Diagnostic Tools Poised to Resolve Industry Challenges

Data source: Survey interviews, chart by VCBeat

Data indicate that when pathological AI systems are implemented in clinical practice, under the condition of ensuring 100% sensitivity,Can reduce 65%-75% of unnecessary slide reading workload for pathologists, thereby directing full attention to suspicious sites and enabling rapid, accurate, and highly reproducible pathological diagnoses.

Furthermore, due toAI is unaffected by environmental conditions or fatigue, ensuring consistent and highly reproducible diagnostic results. It effectively eliminates inter-observer variability in pathological interpretation among pathologists, thereby improving diagnostic accuracy.AI-assisted pathological diagnosis not only alleviates the pressure on patients seeking medical care but also helps address the severe imbalance in the distribution of pathological resources in China.

Driven by Policy, Technology, and Capital, the Development of Smart Pathology Is Imperative.

In recent years, the state has continuously issued documents to encourage and support the construction and development of the pathological diagnosis industry, demonstrating its attention to the existing problems in China's pathological diagnosis sector and its determination to promote the healthy development of the pathology industry.

![}7M{7[17J1HGG]{M26E25V7.png](http://cdn.vcbeat.top/upload/image/08/12/02/49/1669970972617784.png/dmw)

National Policies on Promoting the Development of Pathology Departments and Pathology Centers

Data source: Compiled from public information; chart by VCBeat

"In recent healthcare insurance reforms, pathological diagnosis has not only remained unaffected but has also seen a trend of increasing fee standards against the general direction, reflecting the state's recognition of the technical and labor value provided by pathologists."Taking Beijing as an example, in 2019, the city officially implemented the comprehensive reform of medical service and consumable price linkage. The fees for chemiluminescence immunoassay diagnostics were generally reduced by 5%-10%, while those for pathology-related diagnostic services saw a significant increase, with some items rising by more than 200%.

Policy tailwinds are also favoring “AI + Healthcare,” with “AI + Pathology” experiencing rapid development and emerging as a new competitive frontier for nations worldwide, as well as a key innovative application area in artificial intelligence prioritized for national cultivation.

National Policies Promoting the Development of “AI + Healthcare”

Data source: Compiled from public information; graphic by VCBeat.

In terms of product review and approval,From the original “one-size-fits-all” Class III certification to a comprehensive determination of regulatory classification based on factors such as the product’s intended use and algorithm maturity, the Chinese government has further relaxed the submission requirements for AI-based medical software.Stimulating Rapid Industry Development.

On July 8, 2021, the National Medical Products Administration (NMPA) issued the "Guiding Principles for Classification and Definition of Artificial Intelligence Medical Software Products," clarifying that AI medical software not intended for clinical decision support would be regulated as Class II medical devices. As Class II certifications can be approved by local authorities, approval processes have been accelerated and barriers lowered, thereby incentivizing the industry and further accelerating its development.

Furthermore, strong policy support for free “two-cancer” screening at the primary care level has not only generated robust demand for pathological diagnosis in grassroots settings but also spurred further development of the pathology AI industry. In January 2022, the National Health Commission issued the Work Plan for Two-Cancer (Cervical Cancer and Breast Cancer) Screening, which sets targets to be achieved by the end of 2025: a cervical cancer screening coverage rate of over 50% among eligible women, an early diagnosis rate of over 90% for cervical cancer, and an early diagnosis rate of over 70% for breast cancer. The plan also expands the target population from rural women of eligible age to all urban and rural women aged 35–64 years.

To enhance primary prevention and control capabilities for cervical and breast cancers, the government has encouraged the active adoption of internet and artificial intelligence technologies, accelerating the development of pathology AI.Currently, multiple provinces, including Hubei, have included computer-aided analysis of cervical liquid-based cytology in their social insurance reimbursement catalogs, with fees ranging from 150 to 220 yuan per case. Taking cervical cancer screening as an example, the potential market size for cervical cytopathological screening in China is estimated at approximately 44.2 billion yuan, calculated based on an average annual frequency of 0.5 liquid-based thin-layer cytology (TCT) tests per eligible woman in the country.

The global pathology industry boasts a market size in the hundreds of billions,The pathology AI industry is currently in its early stages of development, with significant growth potential and a broad future market landscape.According to data reported at the 2020 World Pathology Congress, the global pathology market is projected to grow from USD 30.3 billion in 2019 to USD 44.4 billion in 2024, representing a compound annual growth rate (CAGR) of 6.1%. According to Grand View Research, the global digital pathology market was valued at USD 767.6 million in 2019 and is expected to achieve a CAGR of 11.8% through 2027. The integration of AI with pathology holds significant promise.

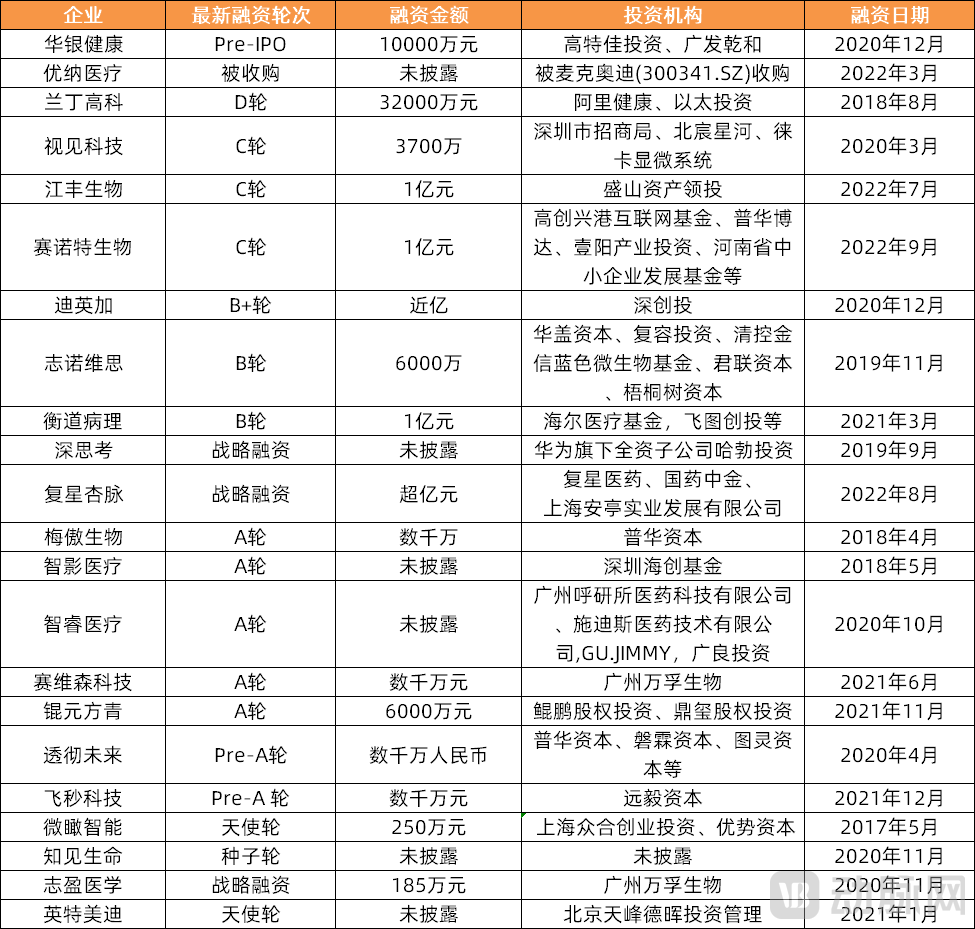

Addressing the pain points in the pathological diagnosis industry has become increasingly urgent. Supported by multiple policies and driven by continuous technological advancements, the fields of digital and smart pathology have attracted significant capital investment in recent years.

Overview of the Latest Financing Events in Digital and Computational Pathology

Data source: VCBeat

3Current State of Commercialization: Standalone Software Monetization Is Challenging; Integrated Solutions Combining Devices, Consumables, and Services Are Emerging

Currently, the upstream segment of China’s smart pathology industry chain primarily comprises manufacturers engaged in the research and development (R&D) and production of pathological diagnostic instruments, reagents, and consumables, providing conventional pathological diagnostic equipment, digital pathology systems, and various reagents and consumables. The midstream segment consists of companies specializing in the R&D of artificial intelligence (AI)-based pathology software systems. The downstream segment mainly includes hospitals at all levels, other medical institutions, third-party independent laboratories, and third-party pathology diagnostic centers, which deliver third-party pathology diagnostic services.

China's Smart Pathology Industry Landscape

Data source: Official websites of respective companies; chart by VCBeat.

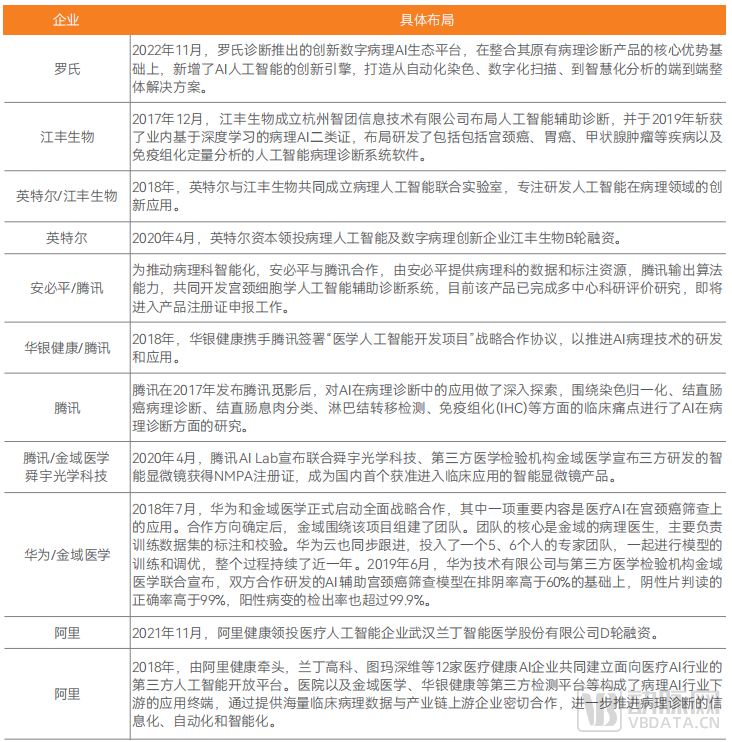

Driven by optimism about the growth prospects of the pathology AI industry, not only have pathology AI startups emerged, but upstream and downstream companies in the digital pathology sector have also actively invested in the development of pathology AI software systems, with internet technology giants joining the fray.

Upstream and downstream enterprises in the smart pathology industry, along with internet giants, are actively investing in the development of AI-powered pathology software.

Source: Compiled from public information; chart by VCBeat.

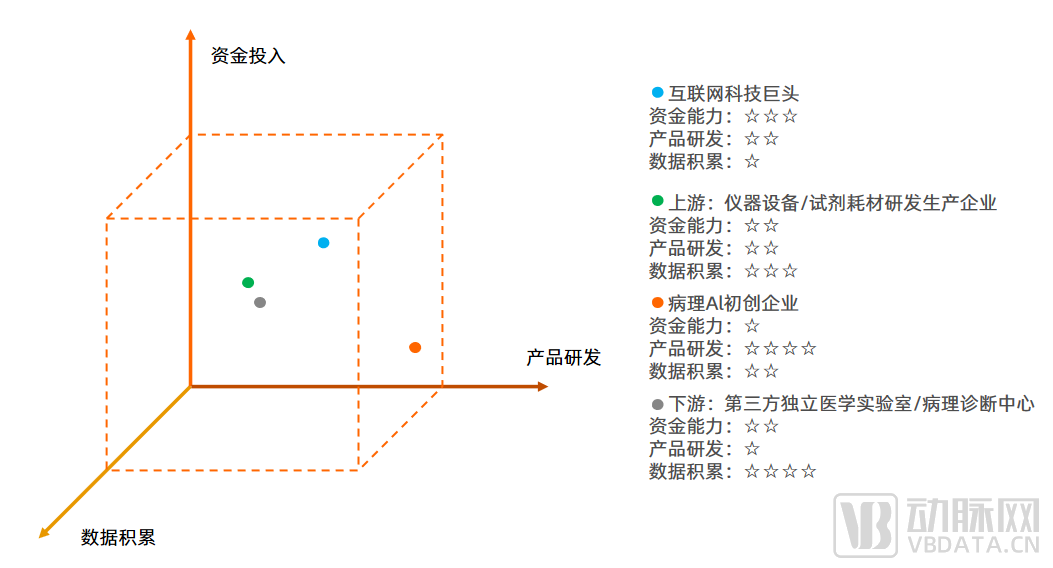

Different industry players have distinct advantages and characteristics in their development of AI-assisted pathological diagnosis systems.

VCBeat Institute believes that,Pathology AI StartupsPossesses leading product R&D capabilities, with significant competitive advantages in its products. The company operates with high agility and demonstrates exceptional responsiveness to market demands, enabling it to gain deep insights into clinical needs and pain points from the frontlines of the market.Upstream Medical Device/Reagent and Consumable Manufacturers, Third-Party Pathology Diagnostic CentersThe advantages of establishing a presence in the AI pathology sector lie in possessing foundational pathological data resources and channel advantages, abundant resources across the upstream and downstream industry chain, and close collaborations with hospitals.Cross-Industry Internet Tech GiantsStrategic positioning in the field of pathological AI offers advantages such as substantial financial resources, an abundance of algorithm and technical personnel, and no pressure to achieve short- to mid-term commercial profitability. This enables parallel project collaborations with major hospitals and enterprises, leading to the efficient generation of scientific research outcomes.

However, every strength has its corresponding weakness; players across the industry likewise face capability gaps, meaning not all enterprises are suited to “get a share of the pie” in the pathology AI sector. VCBeat provides a detailed analysis in its report of the distinct advantages and shortcomings of various industry participants in developing pathology AI software, which will not be further elaborated here due to space constraints.

Different Industry Players Bring Distinct Advantages to the Development of Pathology AI Software

Source: Survey interviews; graphic by VCBeat.

Difficulties in Charging for Pure Software: Pathology AI Companies Pass ThroughProvides bundled solutions combining software with instruments, software with reagents, and comprehensive packages integrating software, instruments, reagents, and end-to-end services.etc., with flexible implementation through various business models such as “B2B,” “B2H,” and “B2B2H.”

Charging for standalone software is challenging because hospitals, the primary payers for pathological AI software developers, typically do not allocate separate budgets for purchasing software services. Furthermore, most provinces have not established digital-related fee schedules, and most hospitals lack standardized pricing structures for digital services. Consequently, pathological AI companies are gradually extending their business layouts upstream and downstream, achieving revenue from software products through indirect channels. For hospitals, integrated solutions that bundle software with instruments or reagents not only streamline procurement but also facilitate clearer accountability when issues arise. This ensures more rapid problem resolution and avoids the blame-shifting that can occur when products are purchased from multiple vendors.

In response to the widespread scarcity of pathology resources in regional hospitals, where even the acquisition of integrated hardware-software solutions fails to enable effective pathological diagnosis, some pathology AI software developers have begun offering a comprehensive package—comprising full sets of instruments and equipment, reagents and consumables, software, and end-to-end services—to regional hospital entities on a per-case fee basis to cover all associated costs.

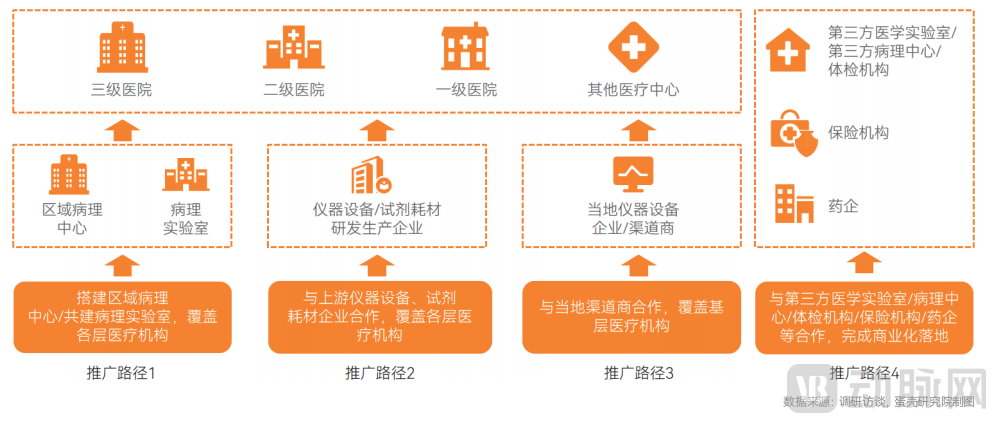

By leveraging “promotional and collaborative bridges” such as medical device/reagent manufacturers, local distributors, third-party independent laboratories, third-party pathology diagnostic centers, health checkup institutions, and insurance companies, pathology AI enterprises can indirectly charge hospitals or patients, thereby advancing commercial implementation. The report provides a detailed introduction and analysis of each business model; due to space limitations, further elaboration is not provided here.

Primary Promotion Pathways for Pathology AI Products

Data Source: Survey Interviews, Chart by VCBeat.

Compared with fields such as AI-powered medical imaging, the field of pathological diagnosis is characterized by lower levels of automation, standardization, digitization, and informatization, as well as slower development. As a result, the development of AI in pathology has been less mature and rapid than that of AI in medical imaging. However, VCBeat believes that precisely due to these developmental “disadvantages,” the commercial deployment models for companies developing AI-based pathology software are more flexible and diversified.

In the upstream segment of the smart pathology industry, importers dominate the high-end market for instruments, equipment, reagents, and consumables in China, leaving substantial room for growth for domestic manufacturers.By partnering with upstream manufacturers of instruments, equipment, reagents, and consumables that boast significant growth potential and rapid momentum, pathology AI companies can achieve business synergy and mutual promotion with upstream and downstream enterprises, leverage complementary strengths, and ultimately realize win-win outcomes.Currently, the commercialization of the pathology AI industry is still in its early stages, with vast market potential in the future.

However, given the differing team capabilities, competitive factors, and product development mindsets required across various domains, stakeholders in the future smart pathology industry must further strengthen collaboration to maximize the efficiency of social resources, with the ultimate product form being comprehensive solutions. For most enterprises,Blind expansion into new domains not only leads to the waste and depletion of resources, with post-investment progress failing to meet expectations, but also squeezes the survival space of the core team.

Once pathological AI software obtains Class III medical device certification in the future, it will further expand its market potential. According to the “Guiding Principles for the Classification and Definition of Artificial Intelligence Medical Software Products,” AI-based medical software not intended for auxiliary decision-making may be regulated as Class II medical devices. While this has stimulated further vitality and development within the industry, it has also allowed many companies to exploit regulatory gray areas. Several domestic companies have successfully obtained Class II certifications for pathological AI; however, their auxiliary diagnostic performance varies significantly, resulting in inconsistent product quality. Consequently, most hospitals remain hesitant to adopt these products. As the national authorities refine relevant review and approval standards, pathological AI solutions that obtain Class III certification—truly reflecting their clinical value—will follow the precedent set by AI-enabled imaging products, which have secured Class III certification and been successfully included in the reimbursement catalogs of most hospitals, thereby further unlocking market potential.

4Challenges and Countermeasures: Outlook on Future Trends in the Smart Pathology Industry

Although numerous companies have entered the digital pathology sector in recent years, AI-based pathological diagnosis remains in a very early stage of development and faces many challenges. Due to high professional barriers and long R&D cycles, AI pathology products have gradually discouraged many industry teams from pursuing this field.

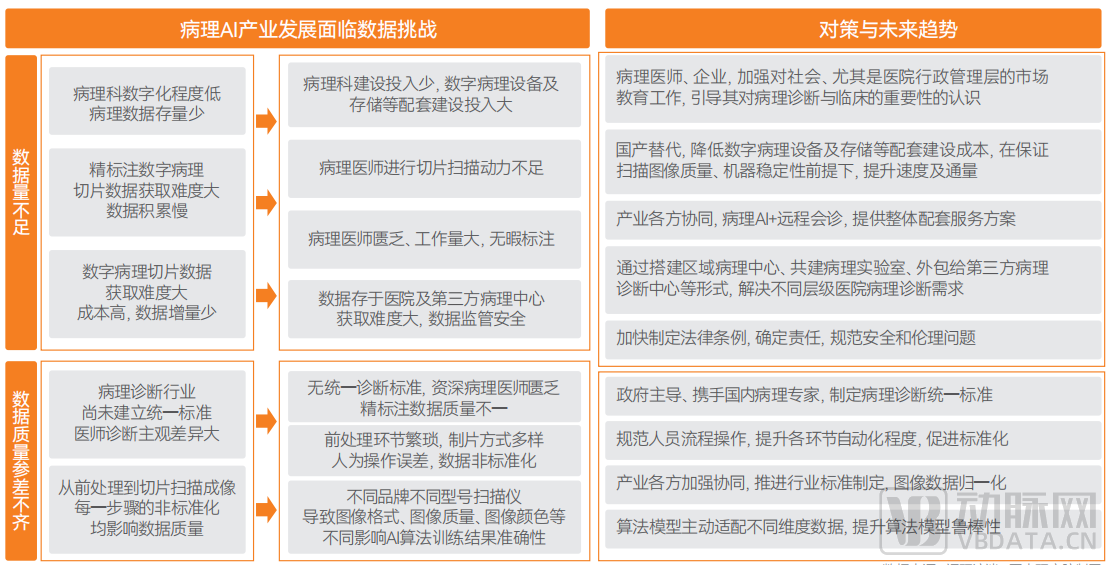

Data IssuesThis is the biggest barrier limiting the current development of the pathology AI industry. The development of algorithm models for pathology AI software requires a large amount of high-quality training data, but the data in the pathology AI industry faces dual challenges in both quality and quantity, making it difficult to obtain sufficient high-quality training datasets. Although there are numerous clinical pathology AI products available, their quality varies significantly.

Data Challenges, Countermeasures, and Future Development Trends in the Field of Pathology AI

Data Source: Survey Interviews, Chart by VCBeat

As the saying goes, “increase revenue and reduce expenditure.” To advance the “four modernizations” of pathology departments and promote more efficient and rapid development of pathology AI, it is essential not only to “reduce expenditure”—by lowering the investment costs for hospital pathology department construction through the domestic substitution of upstream equipment and consumables—but also to “increase revenue”—by enhancing awareness among society, particularly hospital administrative leadership, of the critical importance of pathological diagnosis in the healthcare industry, thereby increasing investment in the development of pathology departments.

As a critical instrument for advancing digital pathology, digital pathology slide scanners have achieved a significant level of domestic production in China; however, their adoption rate in hospitals remains low. While the upfront cost of the equipment itself is one factor, the associated storage costs also pose a major barrier to the development of digital pathology. Fortunately, as storage costs continue to decline annually in line with Moore’s Law, an increasing number of Chinese scanner manufacturers are leveraging their local advantages under market mechanisms. Through continuous technological breakthroughs, these companies are steadily improving the price-performance ratio of their products, thereby further facilitating the entry of digital pathology devices, such as scanners, into hospitals and their penetration into grassroots healthcare markets.

Upstream equipment and consumables companies are targeting expenditures in pathology department construction to further advance domestic substitution. Meanwhile, pathology AI enterprises are exploring diverse models to promote the commercial deployment of their products and address profitability challenges, continuously expanding the coverage of pathology AI solutions through initiatives such as establishing regional pathology centers and co-building pathology laboratories.

By leveraging the radiating influence of large hospitals and collaborating with multiple primary healthcare institutions through initiatives such as establishing regional pathology centers and co-building pathology laboratories, the costs associated with the digitalization and intelligent transformation of pathology departments can be distributed. This approach harnesses economies of scale, thereby facilitating the development of digital and smart pathology in primary healthcare settings, maximizing resource efficiency, and addressing the imbalance between supply and demand in pathological diagnosis caused by insufficient budgets for pathology department construction and scarcity of pathology resources.Furthermore, for primary-care hospitals, outsourcing pathological diagnosis tasks to third-party medical laboratories or pathology diagnostic centers is also an effective way to address their insufficient pathological resources.

With the support of the government,Regional Pathology CenterThey are better positioned to bear the cost of capital-intensive hardware equipment, such as digital pathology slide scanners, which can range from hundreds of thousands to millions of yuan, and to invest in foundational infrastructure for information and storage systems. Building on this basic hardware foundation, regional pathology centers digitize pathology slides and upload them to a regional cloud-based pathology diagnosis platform. This enables further development of digital and intelligent remote pathology diagnosis, addressing the insufficient coverage of pathology resources at the primary care level, promoting tiered diagnosis and treatment, and ensuring revenue generation for hospitals.

Third-Party Medical Laboratory / Pathology Diagnostic CenterWith strong capabilities in autonomy, innovation, and operational flexibility, it holds distinct cost and specialization advantages over public hospitals. Under intensive management, it can maximize the utilization of pathological diagnostic equipment and physician resources, thereby handling a large volume of specimen referrals from primary healthcare institutions.

Co-building Pathology LaboratorySome enterprises address the scarcity of pathology resources and inadequate development of pathology departments in primary healthcare institutions by providing the necessary instruments, equipment, reagents, consumables, AI-assisted diagnostic software, and pathologist resources, and by co-establishing pathology laboratories with Maternal and Child Health Hospitals. Under the supervision and guidance of hospitals, associations, and local Health Commissions, this model ensures quality control in pathological diagnosis, increases the positive detection rate of pathological diagnoses at local Maternal and Child Health Hospitals, and generates economic benefits for the hospitals.

Establishing regional pathology centers, co-building pathology laboratories, and outsourcing to third-party pathology diagnostic centers are effective solutions currently being adopted in the pathology industry to further address the shortage of pathologists and the severe uneven distribution of pathology resources in China. These approaches also represent the future development trend of the industry. The three models cater to different regional stakeholders, each with its own implementation scenarios and corresponding developmental advantages. VCBeat provides a detailed discussion and analysis of these three models in its report; interested readers may download the report for further information.

To address the issue of inconsistent quality in current digital pathology slide data, first, government leadership is required to collaborate with domestic pathology experts in promoting the establishment of unified standards for pathological diagnosis; second, personnel operational procedures need to be standardized, the level of process automation enhanced, and standardization promoted in the pre-analytical phase of pathological diagnosis. In addition, strengthening collaboration among industry stakeholders, opening up data interfaces, advancing the formulation of industry standards, normalizing image data, and enabling pathology AI companies to adapt their algorithmic models to multi-dimensional data to improve model robustness are all important solutions currently being adopted by pathology AI enterprises to tackle data quality challenges.

Furthermore, emerging technologies such as label-free femtosecond laser imaging, which can generate standardized digital images without the need for sectioning and staining, directly circumvent data variations introduced by the processes of pathological sectioning, staining, and slide scanning. As such, they represent ideal input data for pathology AI models and warrant attention from the industry.

Profitability Challenges, Countermeasures, and Future Development Trends in the Smart Pathology Industry

Data source: Survey interviews; chart by VCBeat

Profitability remains a significant challenge currently facing the entire AI+healthcare sector. In addition to intensifying market education and enhancing societal recognition of software value, pathology AI-assisted diagnostic tools must be further diversified across various clinical application scenarios to meet the needs of pathology departments.

Currently, the development of AI-assisted diagnostic tools in pathology is uneven across various application scenarios. Companies are clustering in the field of cytopathology—primarily Thinprep Cytologic Test (TCT)—characterized by substantial data accumulation, a large market size, and relatively simple morphological features. Beyond assisting in pathological diagnosis, there are numerous pain points to be addressed across all stages of the pathological workflow; however, AI intervention in these areas remains limited.

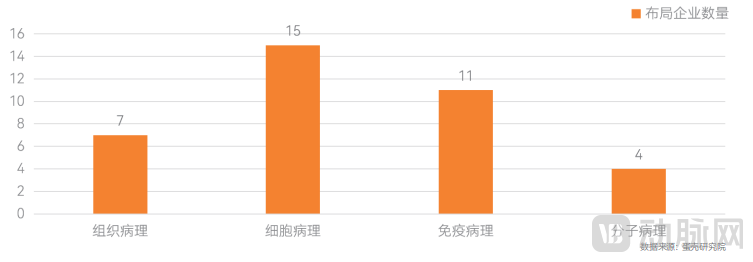

Overview of the Layout of Domestic Pathology AI Enterprises in Various Fields of Pathological Diagnosis

Source: VCBeat

In the future, products in the field of cytopathology should undergo more extensive clinical validation to improve the accuracy of AI algorithm models for cytopathology, in preparation for obtaining Class III medical device certification. For histopathology AI products, given the complex morphological features and high background noise inherent in histological pathology, it is essential not only to ensure precisely annotated data and adopt correct product development strategies but also to enable artificial intelligence to “comprehend” the diagnostic criteria for discriminating complex morphological features in histopathology.The team needs to innovate in algorithms;While enhancing the accuracy of algorithmic models for related products, it is equally important to expand product functionalities and broaden the range of covered diseases to meet the department’s needs for auxiliary diagnosis across multiple disease types.The tipping point for the field of pathological AI may be reached when such software covers approximately 80% of the daily sample volume.

In addition to assisting in pathological diagnosis, the pre-processing steps of pathological slides, such asSpecimen Collection, Slide Preparation, and Quality ControlThese are all application scenarios where AI can intervene, awaiting further development by enterprises. In addition to horizontal coverage, smart pathology products have more application scenarios and development space in the deep interpretation of multimodal information.

In the era of precision medicine, the rapid development of targeted therapy and immunotherapy has demonstrated an increasing demand for immunopathology and molecular pathology. For instance, many biomarkers in immunohistochemistry (IHC) require precise quantitative analysis, as their results directly influence medication decisions for malignant tumors and patient prognosis. However, the interpretation of IHC results faces several challenges in both testing and pathological diagnosis, including poor stability and consistency due to subjective interpretation, image analysis tools that are disconnected from standard workflows, inability to perform precise quantitative analysis, and lack of unified criteria for interpreting antibodies used to guide pharmacotherapy.AI-assisted precise interpretation of immunohistochemistry results has demonstrated promising application prospects in tumor diagnosis, guidance of therapeutic strategy selection, evaluation of treatment efficacy, and prognosis prediction.With further advancements in immunopathology and molecular pathology, pathological AI will unlock greater market potential in the field of clinical drug research.

The above is an excerpt of the main content of the report. The complete framework of the report is as follows:

Scan the QR code to add the assistant and access the full report. Please initiate your inquiry after adding.

Special Acknowledgments (in order of interviews):

Shang Bin, CEO of Kunyuan Fangqing; Pan Weijun, Chief Medical Officer of Kunyuan Fangqing; Wang Zihan, COO of Shengqiang Technology; Cui Hongliang, CEO of Zhijian Life; Kong Xiangbing, COO of Zhijian Life; Liu Zheng, Marketing Director of Jiangfeng Bio; Fan Yujun, Founder of Dangier; Qi Hua, Founder of Synoite Biology; Du Rui, Deputy Director of the People's Hospital of Tibet Autonomous Region and Associate Chief Physician of Guangdong Provincial Maternal and Child Health Hospital; Wang Shuhao, CTO of Touche Future; Chen Rui, CEO of Sewise Technology; Ding Yanqing, Chairman and Founder of Kunyuan Fangqing; Xu Bingwei, Founder of Femto Tech; and other unnamed industry professionals.