Medical VCs Chase Hot Trends While Exploring New Frontiers

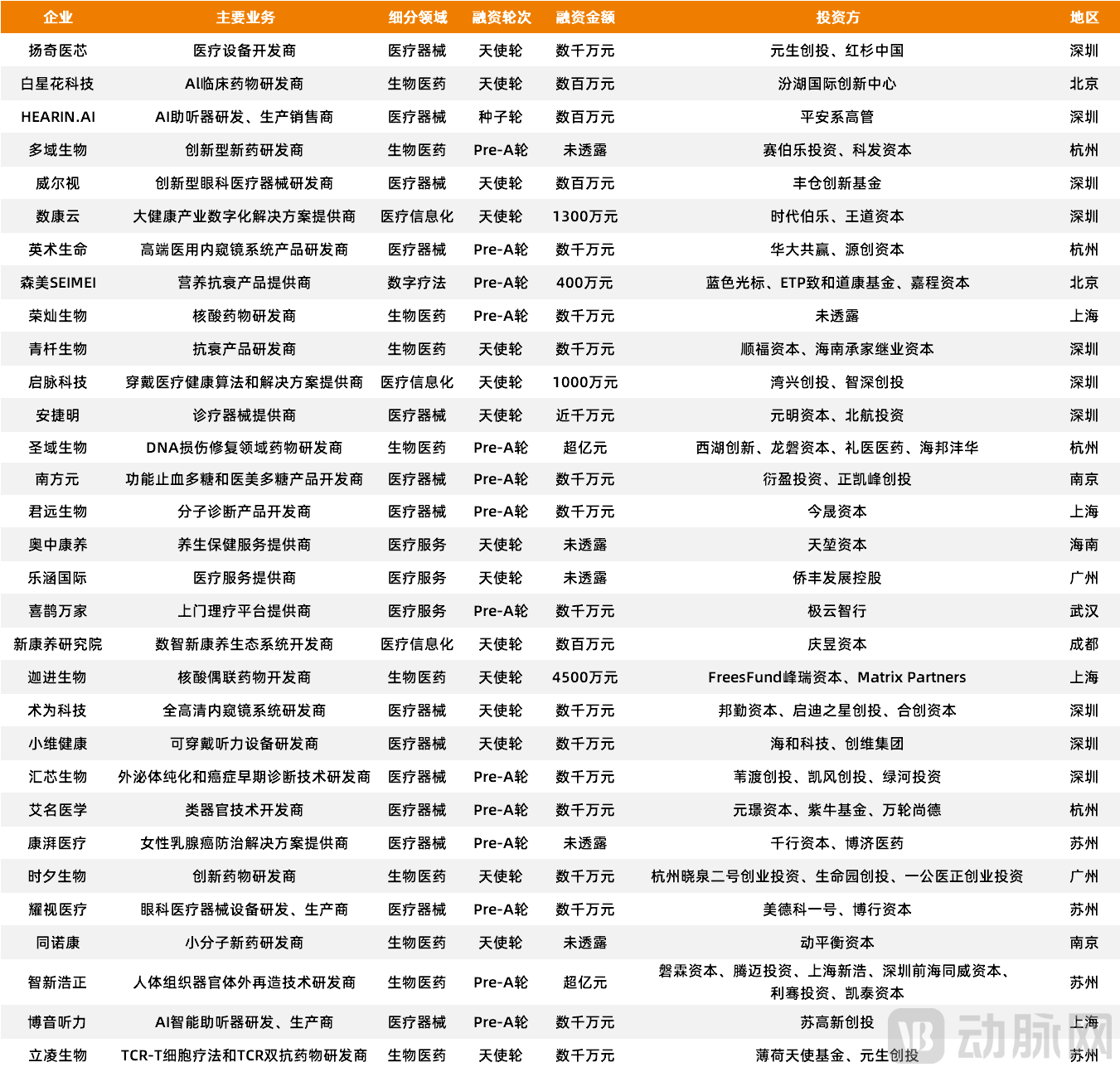

Yangqi Medical

Medical Device Developer

According to incomplete statistics, in November alone, there were 31 early-stage (seed, angel, and Pre-A round) financing events in China’s healthcare sector, with total funding exceeding RMB 1 billion. A total of 59 top-tier investment firms participated, including Sequoia Capital, Bohe Angel, Yansheng Capital, and FreeS Fund.

In fact, since the beginning of this year, the healthcare industry has been consistently disparaged due to the pandemic and other multifaceted factors. Recently, remarks such as “We are no longer reviewing healthcare projects,” “My friend who invested in healthcare has shifted focus to breeding,” and “It would be commendable if healthcare companies can survive this year” have frequently emerged.

However, this “chill” does not appear to have affected the early-stage healthcare market. According to the VCBeat Orange Database, with one month remaining in the year, China’s healthcare sector has already completed 323 early-stage investment and financing deals, with total funding approaching RMB 10 billion. In addition to the substantial volume, the proportion is also significant: of the 84 investment and financing transactions recorded in China’s healthcare sector in November, 31 were early-stage rounds, accounting for 37% of the total.

This means that despite dispelling industry bubbles, grappling with fundraising challenges, and overcoming headwinds such as remote work, healthcare venture capitalists remain particularly keen on early-stage healthcare projects. So, what types of projects are they targeting? And what future trends in the healthcare industry can we anticipate? The answers may lie within the early-stage financing data from November.

Target both hot sectors and new blue oceans

As previously mentioned, it is already a significant achievement for healthcare companies to survive this year; those that have successfully secured financing are even more exceptional. VCBeat analyzed 31 startups that completed early-stage financing in November and summarized the following three trends:

First, “innovation” remains the core of the early-stage healthcare investment market. Statistics show that among 31 startups, 24 are hard-tech enterprises, accounting for 77.4%. Most of these startups are concentrated in subsectors with significant unmet clinical needs, such as oncology and cardiovascular diseases.

This is not difficult to understand. From the perspective of the healthcare industry itself, we are undergoing a critical phase of achieving domestic substitution through technological innovation. Therefore, only innovative projects that possess genuine original technologies and address substantial market opportunities are more likely to stand out in the early-stage market.

But how should “innovation” be defined? When establishing the AstraZeneca CICC Healthcare Industry Fund, Wang Lei, Global Executive Vice President of AstraZeneca and President of International Operations and China, introduced the concept of “genuine innovation, genuine science,” meaning that portfolio companies truly possess innovative technologies and have verifiable scientific data. In addition, in a recent widely circulated industry article, pharmaceutical investors have loudly called on their peers to “compete fiercely on innovation.” On this point, scientists and investors appear to be gradually reaching a consensus.

Second, popular sectors remain “crowded.” According to statistics, 11 out of 31 startups are focused on the current “high-traffic” segments in the healthcare field, such as organoids, radiopharmaceuticals, gene editing, in vitro diagnostics, and regenerative medicine. Startups in these sectors tend to attract additional attention regardless of their technological merits.

Taking organoids as an example, this is an innovative technological field with substantial potential. By definition, organoids refer to tissue-like structures with specific spatial organization and function, formed in vitro from adult stem cells or pluripotent stem cells through three-dimensional culture. By cultivating organoids, researchers can better investigate a range of topics, including the mechanisms of disease progression and drug metabolism pathways.

Between 2019 and 2020, the wave of organoid research enthusiasm that had already gained significant traction in Europe and the United States began to spread to China. In less than two years, the number of basic research studies on organoids in China surged to rank second globally. Consequently, emerging startup projects in this field have started to attract substantial attention from the capital market this year, with prominent investment firms such as CDH VGC, SDIC Innovation, Kaifeng Venture Capital, and Delian Capital taking the lead in entering the sector.

It is reported that in November, China’s organoid sector completed three financing rounds, all at early stages. Aimed Medicine secured tens of millions of yuan in Pre-A financing in November, marking its second funding round within a year, with the total amount raised approaching 100 million yuan. Currently, Aimed Medicine’s core products include the Organoid Automatic Processing and Analysis Instrument (OSCAR), the Organoid-on-a-Chip Signoid, and the Digital Organoid Platform Digituor.

Third, the early-stage healthcare market is beginning to exhibit “diversification” and “human-centricity.” According to statistics, among 31 startups, 14 are in medical devices, 10 in biopharmaceuticals, 3 in healthcare services, 3 in healthcare informatics, and 1 in digital therapeutics, covering multiple sub-sectors including oncology, cardiovascular care, rehabilitation, diagnostics, medical aesthetics, ophthalmology, and otology. Unlike the previous trend where focus was concentrated on two or three hot sectors, healthcare venture capitalists have broadened their investment horizons since November.

But beyond “breadth,” healthcare VCs are also turning their attention to underserved populations, such as women, elderly patients, and the deaf.

Let’s start with women. Women’s health has long been an overlooked sector in the Chinese market. According to incomplete statistics, from 2019 to the present, there have been only 33 financing events in China’s women’s health sector, of which only nine involved amounts exceeding RMB 100 million.

So far this year, only two financing deals have been closed in the women’s health sector, one of which was Kangpai Medical’s tens-of-millions-of-yuan Pre-A round completed in November. Founded in 2019, Kangpai Medical focuses on the breast care specialty. Its core team comprises renowned overseas-returning scholars and experts, senior technical specialists from internationally recognized equipment manufacturers, and seasoned industry professionals, backed by a network of top clinical expert advisors both in China and abroad. To date, Kangpai Medical’s breast specimen imaging system has filed for or secured nearly 50 intellectual property rights and obtained regulatory approvals in major global markets. The product is widely sold and has received extensive acclaim in the United States, Western Europe, the United Kingdom, and China.

Turning to the elderly population. Population aging has become a significant issue facing Chinese society today. The diverse needs in this demographic have created substantial opportunities in the healthcare sector; however, venture capitalists (VCs) seemed to have overlooked this trend in the past, or perhaps they had not yet identified more effective entry points.

But now, venture capitalists have begun to take action. Among the 31 startups that completed early-stage financing in November, two focused on health issues related to aging. One is Qimai Technology, which primarily addresses the demand for out-of-hospital medical and healthcare services among the global elderly population. Leveraging a multidisciplinary team and years of R&D accumulation, it is committed to providing professional medical and healthcare algorithm and data services to wearable device manufacturers, industry clients, and hospitals. The other is Aozhong Kangyang, which mainly provides wellness and healthcare services for the elderly.

Finally, there are individuals with hearing loss. According to data from the World Health Organization’s 2021 World Report on Hearing, more than 1.5 billion people worldwide currently suffer from some degree of hearing loss, and this number is projected to rise to 2.5 billion by 2050. Among them, at least 430 million require rehabilitative services, while an additional 1.1 billion young people are at risk of permanent hearing loss due to poor listening habits. Based on data on unilateral deafness in the United States from recent years, it is conservatively estimated that China has at least 40 million individuals with unilateral deafness-related hearing impairment.

Even so, otology remains a niche sector in China’s medical venture capital market. This is partly because most hearing assistance devices currently available in China are imported, with few breakthrough domestic technologies and slow progress in import substitution; it is also due to the relatively high unit price of hearing assistance devices and low levels of market awareness. Consequently, compared with dentistry and ophthalmology, otology has remained lukewarm.

However, this situation began to improve this year. Statistics show that in November alone, three otology-focused startups secured early-stage financing: HEARIN.AI, Boyin Hearing, and Xiaowei Health. All three companies are dedicated to the research and development of hearing aids.

Overall, China’s early-stage healthcare market is becoming increasingly diversified. In addition to startups in popular sectors, high-quality companies in niche areas are gradually attracting capital attention. Furthermore, after a period of consolidation and the accumulation of lessons from failed cases, the early-stage healthcare market is becoming more rational. For startups to secure financing, it is no longer sufficient to rely solely on cutting-edge technology or endorsements from top global research institutions; instead, they must possess diverse, composite capabilities and maintain a longer-term strategic vision.

“Veterans” Hold Firm, “Newcomers” Enter the Field

A seasoned angel investor remarked, “There is increasingly more capital focusing on early-stage medical projects. In the past, only a few firms like ours were evaluating them; now, everyone is.”

This is indeed a major trend. Taking the 59 investors that participated in early-stage investments in November as an example, the group includes top-tier firms such as Sequoia Capital, as well as Mint Angel Fund and Yuansheng Ventures, which have long focused on early-stage investing. It also comprises large pharmaceutical companies like Boji Medicine, Beihang University Investment backed by research universities, and Xihu Innovation and Life Science Park Venture Capital led by local governments or industrial parks.

Certainly, some individual investors are also getting involved in this wave of medical innovation. For example, the seed funding round of several million RMB obtained by HEARIN.AI, a developer and manufacturer of AI-powered hearing aids, in November was personally invested by executives from Ping An Group.

So, why are they choosing to bet on the early-stage healthcare sector at this moment?

The answer is multifaceted. First, it reflects the current developmental characteristics of the healthcare industry. At present, follow-on innovation in the healthcare sector is nearing its end, with original innovation taking its place as the focal point in the new era of Chinese healthcare venture capital and private equity. Second, the boom in the secondary market is exerting pressure on the primary market. Since 2020, the listing cycle for healthcare companies has been significantly shortened, accelerating the overall pace of financing and investment. Investment boundaries have become increasingly blurred, making it difficult for institutions that previously focused solely on mid-to-late-stage investments to find suitable entry points.

Finally, early-stage healthcare projects offer high returns. Before the current wave of medical innovation gained momentum, the limited availability of early-stage capital was primarily due to the complexity, high risk, and narrow profit margins of early-stage healthcare projects, with most financing rounds amounting to only around RMB 1 million. However, in the past one to two years, early-stage healthcare financing has nearly all reached the tens of millions of yuan, with numerous deals exceeding RMB 100 million, thereby creating substantial profit potential for early-stage investment firms.

However, new challenges follow in the wake of these opportunities. For investment firms entrenched in the early-stage healthcare market, industry shifts are imposing new demands on how they pursue “early-stage” investments.

First, it is essential to establish an early-stage investment thesis tailored to one’s own capabilities. Early-stage healthcare projects are highly diverse, with each venture presenting unique circumstances and distinct pain points. Therefore, investment institutions cannot simply replicate so-called “success formulas” when investing at the early stage. Instead, they should leverage their existing strengths to develop proprietary strategies, create differentiation, and build a competitive moat in the early-stage market as soon as possible.

Second, it is essential to carefully select investment tracks and targets. Early-stage healthcare projects are not suited for a “spray-and-pray” approach; instead, investors should adopt a focused strategy by conducting in-depth scans of specific niche sectors. Therefore, investment firms must not only keep pace with currently popular tracks but also explore new blue-ocean markets. Regarding investment targets, as previously mentioned, the core objective is to identify startups that both address current clinical needs and demonstrate genuine innovative capabilities.

Third, it is essential to master the “language of scientists.” Early-stage healthcare investment is complex because it involves extensive communication and interaction from initial project sourcing to final deal closure; therefore, reducing communication costs is critical for early-stage investing. In addition, early-stage investment firms must also master the “language of scientists,” meaning they should be able to think from scientists’ perspectives and communicate effectively with them.

Fourth, it is essential to refine post-investment capabilities. For the vast majority of early-stage healthcare projects, capital may not be the only critical factor; more importantly, these ventures rely on the post-investment support provided by investment firms. This is because early-stage projects encounter a wide array of challenges as they progress, such as team building, product development, and commercialization. Therefore, they require investors who demonstrate long-term commitment and loyalty, as well as multidisciplinary capabilities to address practical problems effectively.

Fifth, adopt a long-term perspective. Investing early is investing in the future; therefore, when selecting early-stage targets, investment institutions should pursue long-term interests, maintain a global outlook, and embrace a big-picture mindset. Additionally, institutions themselves should take a longer-term view in their strategic planning, such as building early-stage investment teams and enhancing post-investment service capabilities.

Yan Yi, Managing Director of Shuimu Ventures, stated in an exclusive interview with Chengguo Bureau that if project evaluation in the early years was akin to discovering exposed ore deposits, then in the wake of the current wave, it has become a process of sifting gold from sand. Regardless of future developments, the essence of this change is that the landscape for hard-tech innovation is evolving favorably. To address the corresponding challenges, investment institutions should respond to all changes with constancy by persisting in investing in technological innovation—particularly technologies that create social value—and by committing to deep investment and the establishment of robust service systems.

Who Will Be the Next Silicon Valley?

Innovation requires talent, funding, and, of course, a vehicle.

The success of American healthcare innovation to date is inextricably linked to Silicon Valley, which has not only cultivated and attracted a cohort of visionary scientist-entrepreneurs but also gathered a cluster of venture capital firms that invest in such aspirations. In effect, Silicon Valley has established a comprehensive, end-to-end ecosystem for innovation, encompassing discovery, research and development, incubation, commercialization, and accelerated growth.

So, when turning our attention to China, who has the potential to become the next Silicon Valley? Beijing, Shanghai, and Suzhou are certainly strong contenders, but there is another place that may also have this potential: Shenzhen.

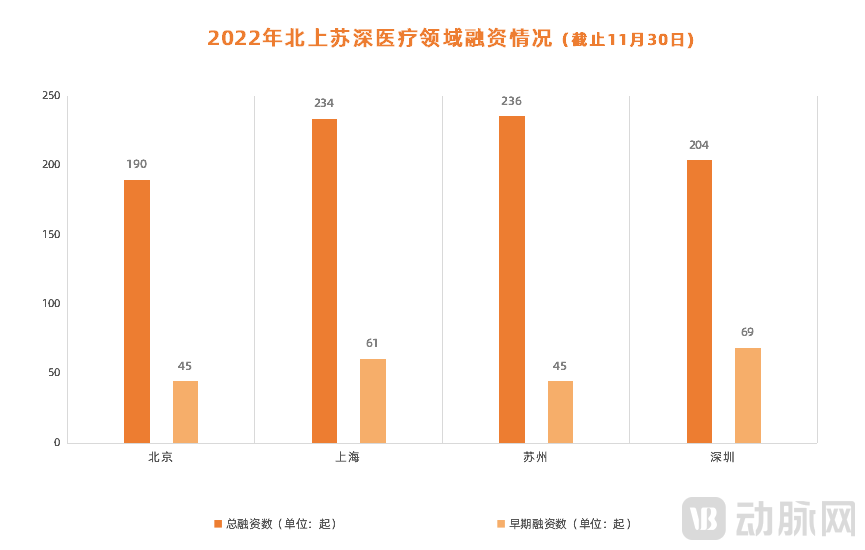

According to statistics, among the 31 healthcare companies that completed early-stage financing in November, 10 were from Shenzhen, a number equal to the combined total of Beijing, Shanghai, and Suzhou. In fact, not only in November but throughout 2022, Shenzhen has demonstrated its immense potential in medical innovation. According to the VCBeat Orange Database, as of November 30, Shenzhen had completed a total of 69 early-stage healthcare investment and financing deals in 2022, surpassing the combined totals of Beijing, Shanghai, and Suzhou.

This is by no means a coincidence. First, Shenzhen has adopted an open policy framework, which is crucial for innovation. In recent years, the core principle guiding Shenzhen’s industrial innovation policies has been to implement, as rapidly as possible, any measures that can more effectively foster innovation.

Second, Shenzhen is home to a cohort of world-leading research institutions and scientists. In terms of research institutions, Shenzhen hosts the Shenzhen Institute of Advanced Technology (SIAT) and Shenzhen University. Regarding talent, as of now, the city has 74 academicians from the Chinese Academy of Sciences and the Chinese Academy of Engineering, over 19,000 high-level professionals, and nearly 170,000 returnees who studied abroad. Furthermore, Shenzhen boasts abundant clinical resources; as of June 2022, there were 28 Grade A tertiary hospitals in the city.

Third, Shenzhen is home to a number of venture capital firms specializing in early-stage healthcare investments, such as Genesis Capital and Shenzhen Capital Group. According to statistics from the VCBeat Orange Database, as of November 30, Genesis Capital had completed 32 financing deals in the healthcare sector this year, with 22 occurring before Series A, accounting for 69%. Shenzhen Capital Group completed 16 healthcare financing deals this year, six of which were pre-Series A. In addition to venture capital firms, Shenzhen also has numerous local fund-of-funds, government special funds, and social capital, all of which are continuously converging on the early-stage healthcare market.

Fourth, Shenzhen boasts a robust foundation for its medical industry. Since prioritizing the development of a biomedical industrial cluster in 2009, Shenzhen’s biomedical sector has maintained rapid growth in recent years. In 2021, the operating revenue of Shenzhen’s biomedical industry reached RMB 46.1 billion, representing a 13% year-on-year increase. At the enterprise level, Shenzhen is home to more than 20 biomedical companies, highlighting a pronounced agglomeration effect. Two major industrial clusters—the Nanshan High-Tech Park and the Pingshan National Biotech Industrial Base—have initially taken shape.

But Shenzhen is not just about this. In the just-concluded November, two major events took place in Shenzhen’s medical innovation circle.

First, renowned scientist Yan Ning announced at the Shenzhen Global Innovation Talent Forum that she had submitted her resignation to Princeton University and would soon return to China full-time to participate in the establishment of the Shenzhen Medical Academy.

Second, at the 2022 Xili Lake Forum, the New Cornerstone Science Foundation officially announced its establishment in Shenzhen. Reportedly, this foundation is a new type of non-profit organization initiated and established by Tencent to fund basic research. Tencent has committed to investing RMB 10 billion over ten years to support a group of outstanding scientists in dedicating themselves to basic research and achieving original innovations from “0 to 1.” Shi Yigong, an academician of the Chinese Academy of Sciences and President of Westlake University, serves as the Chairman of the Scientific Committee for the “New Cornerstone Investigator Program.”

These developments, both realized and ongoing, have heightened our expectations for the future of Shenzhen’s medical innovation market.