Chenguang Medical Goes Public on BSE as a Key Philips Supplier Tackling China's 'Bottleneck' in Domestic Medical Imaging Equipment

ChenGuang Medical

Developer, Manufacturer, and Supplier of Core Components in the MRI Industry Chain

Amid the wave of domestic substitution for high-end imaging equipment, another leading enterprise listed on the Beijing Stock Exchange today.

ChenGuang Medical, a core upstream component supplier for magnetic resonance imaging (MRI) systems, was founded in 2004. The company has independently developed four key components of MRI systems: high-performance, high-field-strength superconducting magnets, radiofrequency (RF) systems, gradient systems, and computer systems. It possesses the capability to manufacture complete MRI units and has overcome multiple technical challenges in the production of specialized superconducting magnets. Taking its RF systems as an example, founder Wang Jie introduced phased-array coil technology and pursued technological innovation on this basis, filling the gap in China’s R&D and manufacturing capabilities for high-field, high-end RF coils. The company has launched its “Cloud Coil” product, benchmarked against GE Healthcare’s cutting-edge “Air Coils,” thereby breaking the monopoly held by multinational giants over the domestic RF coil market.

In 2006, ChenGuang Medical signed a framework agreement with Philips. Over the 16 years of collaboration, ChenGuang Medical has developed more than 50 products for Philips, serving as a “strategic supplier” for Philips’ RF detector business. To date, the vast majority of these products have been sold to developed countries and regions such as Europe and the United States, generating over RMB 500 million in revenue for ChenGuang Medical.

In China, ChenGuang Medical is a major supplier of core MRI components, such as magnets and gradient coils, to Wandong Medical and Langrun Medical. It has also established partnerships with Basda, Kangda Medical, and Kaipu Medical, with the potential to deepen these collaborations in the future and facilitate the upgrading and iteration of their MRI systems.

(ChenGuang Medical’s Major Customer Distribution Data Source: ChenGuang Medical Prospectus)

During the reporting period, ChenGuang Medical’s operating revenue demonstrated a sustained upward trend, reaching RMB 134 million, RMB 142 million, RMB 196 million, and RMB 56 million in 2019, 2020, 2021, and January–June 2022, respectively. The corresponding net profits were RMB 3 million, RMB 5 million, RMB 24 million, and -RMB 4 million. Due to the pronounced seasonal fluctuations in medical device sales, ChenGuang Medical is expected to receive more payments in the second half of the year, with net profit poised to reach new highs.

In 1987, China’s first 1,500-gauss permanent magnet MRI system was launched, with all core components—including the magnet, gradient coils, and RF coils—as well as the complete imaging software suite independently developed by Anke. However, due to the excessively long scan times and low image clarity resulting from the limited field strength of permanent magnet MRI, these devices could be used for diagnostic purposes but not for precise diagnosis, thereby precluding their application in imaging research on complex organs such as the brain and heart.

In contrast, multinational corporations’ mature superconducting MRI systems have long surpassed field strength limitations, enabling imaging to delve deeper into unraveling the unknowns underlying diseases. However, due to constraints such as international trade barriers and regulatory approval policies, leading hospitals in China tasked with advancing imaging capabilities often struggle to acquire the latest MRI scanners at the time of their global release. As a result, they typically lag behind their European and American counterparts by two to three years. By the time these institutions gain access, Western centers have already leveraged their technological advantage to conduct ample prospective studies, leaving Chinese hospitals to primarily focus on retrospective research.

The technological divide directly leads to disparities in medicine.

Specifically regarding superconducting magnets. As important tools for scientific research, the demand for superconducting magnets in China continues to grow across various fields, including high-energy physics, controlled thermonuclear reaction, plasma physics, biophysics, low-temperature physics, magnetism, material structure analysis, medicine, transportation, and industry. However, due to the prevalence of low-end products and the low localization rate of superconducting magnets in China, industries such as high-field magnets, scientific research instruments, and high-end medical equipment do not have a favorable development environment.

In this context, international manufacturers holding monopolistic positions have frequently clashed with users in China. For instance, Bruker Corporation of the United States delivered an NMR spectrometer to Peking University. When maintenance was required during operation, Bruker failed to identify the root cause and instead demanded a prepayment of RMB 200,000 before dispatching technicians for on-site service, without guaranteeing that the issue would be resolved.

Technological gaps directly result in a lack of discourse.

Confronted with the pain of being “strangled” by technological bottlenecks, ChenGuang Medical started with MRI radiofrequency detectors and took up the banner of independent R&D. After securing a long-term contract with Philips by leveraging its technological and cost advantages, the companyIt has progressively refined its production lines for core MRI components, including those for 1.5T, 3.0T, and 7.0T systems, thereby achieving the remarkable leap from manufacturing individual components to producing complete superconducting magnetic resonance imaging (MRI) systems.Especially in the manufacturing of complete MRI systems, only GE HealthCare, Siemens Healthineers, and United Imaging Healthcare possess comparable capabilities globally.

In the field of specialized superconducting magnets, ChenGuang Medical has independently developed superconducting cyclotron magnets for proton therapy systems, cryogen-free superconducting magnets for cryogen-free MRI systems, and 9.4T superconducting magnets for scientific research. Highlighting ChenGuang Medical’s breakthroughs in high-end cancer diagnosis and treatment, the 230MeV and 250MeV superconducting cyclotron magnets it developed for the China Institute of Atomic Energy under the China National Nuclear Corporation are among the core critical components of proton therapy cyclotrons. These magnets have passed testing and multiple units have been delivered, marking the first time in Asia that a compact superconducting cyclotron with independently developed proton beam energy exceeding 230MeV has been achieved.

ChenGuang Medical’s breakthroughs in the high-end medical device manufacturing sector have driven the development and application of domestic magnetic resonance (MR) technology at its source, helping midstream MR system manufacturers to some extent alleviate their dependence on overseas core components. However, a review of its revenue and profits suggests that its profitability does not appear commensurate with its breakthrough value.

The manufacturing of high-end medical devices is a pursuit of perfection; those who can achieve greater precision and refinement in manufacturing are poised to take the lead in the forefront of technological competition.

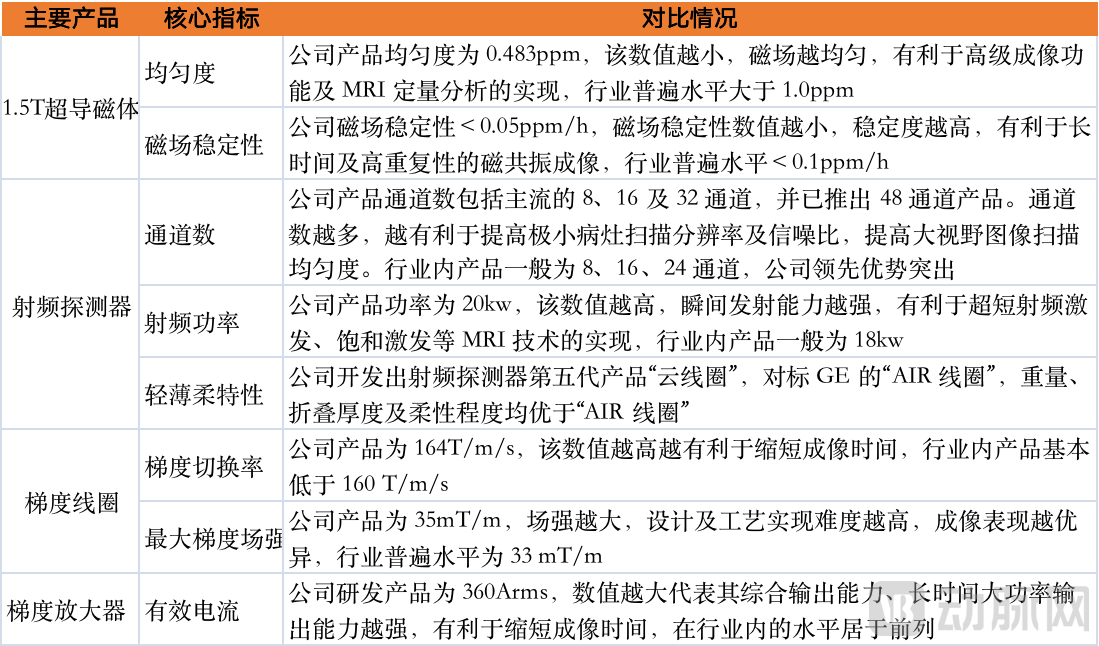

Based on the data of ChenGuang Medical's core components at the current stage, the majority of product parameters surpass the industry's leading levels, especiallyHomogeneity of 1.5T Superconducting MagnetswithThe Thin, Lightweight, and Flexible Characteristics of RF DetectorsThe former can achieve 0.483 ppm, far below the industry average of greater than 1.0 ppm (a lower value indicates a more homogeneous magnetic field, which facilitates advanced imaging capabilities and quantitative MRI analysis); the latter, the “Cloud Coil,” is the latest fifth-generation coil, comparable to GE Healthcare’s cutting-edge AIR coils, while being lighter, thinner, and more flexible.

Comparison of Core Performance Indicators for Key MRI Components Among Industry Peers (Data Source: ChenGuang Medical Prospectus)

Although core components determine the performance ceiling of MRI systems, clinical deployment and patient care are exceedingly complex endeavors. Only by identifying appropriate application scenarios and ensuring seamless integration between the overall MRI system design and its components can the full potential of high-end manufacturing be realized.

Currently, in addition to ChenGuang Medical, industry giants Neusoft Medical and United Imaging Healthcare also possess in-house R&D capabilities for all core MRI components and are competing for market share through domestic substitution strategies. United Imaging Healthcare, in particular, not only boasts a comprehensive MRI product portfolio offering magnetic resonance systems with the same field strength tailored to different application scenarios, but also optimizes the integration of systems and components based on specific requirements to maximize component performance.

According to 2020 data from Frost & Sullivan, United Imaging Healthcare held a 24.0% share of China’s superconducting MRI market. Notably, in the 1.5T MR segment—ChenGuang Medical’s core focus—United Imaging Healthcare surpassed GPS (GE, Philips, and Siemens) to rank first with a 25.4% market share.

Due to its minimal involvement in complete system sales, ChenGuang Medical’s revenue is heavily dependent on buyers’ demand for nuclear magnetic resonance (NMR) components. Data show that although Wandong Medical ranked fifth in China’s superconducting MRI equipment market in 2020, its market share was only 3.9%; Langrun Medical ranked fifth in the 1.5T MRI market, with a market share of just 5.4%.

Weak demand from major customers has significantly curtailed ChenGuang Medical’s revenue growth. Amid the wave of domestic substitution, ChenGuang Medical stands at a critical crossroads, facing pivotal decisions on how to seize the forefront of this trend.

The challenges facing ChenGuang Medical are not confined to the MRI sector. Constrained by the relatively weak sales performance of most midstream equipment manufacturers, independent third-party suppliers of core components for CT, XR, and other modalities have long been in a situation where they can make ends meet but remain far from prosperous.

There are many possibilities for breaking through the status quo, but not every path will prove effective. In its prospectus, ChenGuang Medical implicitly outlined at least three potential development paths.

The first is to directly join the frontline.。ChenGuang Medical currently holds a Class III medical device registration certificate for its 1.5T MRI system, and its 1.48T superconducting MRI system has completed clinical trials, with a market launch expected in the near future. Given that midstream partners in the industry chain have struggled to break through market barriers, could ChenGuang Medical potentially enter the midstream segment directly?

Following this route, the core challenge lies in addressing brand and channel issues. As an upstream supplier for MRI systems, ChenGuang Medical has limited opportunities for direct engagement with downstream medical institutions. Its brand influence among hospitals is significantly lower than that of Wandong Medical and Longruan Medical, and pales in comparison to industry leaders such as United Imaging and the “GPS” group (GE Healthcare, Philips, and Siemens Healthineers). Building a strong brand would require ChenGuang Medical to expand its complete-system product line and invest substantial capital and time—burdens that are difficult to bear given the company’s current asset scale.

Building distribution channels is equally challenging. Data from the prospectus shows that ChenGuang Medical’s revenue is primarily derived from direct sales, with direct sales contributing 94.66%, 94.93%, 92.44%, and 95.80% of its principal business revenue during the reporting periods. The near-zero reliance on suppliers also means that ChenGuang Medical must build its distribution network from scratch, requiring substantial upfront investment before the network becomes operational.

In summary, for ChenGuang Medical to transition directly from the upstream to the midstream sector would require substantial investment and entail the risk of sales failure. Maintaining its existing business model or adopting an OEM (original equipment manufacturer) sales strategy may be a more viable option for ChenGuang Medical.

The second is deep integration with midstream manufacturers.Integration may take the form of holding companies or targeted collaborations centered around a specific product. Taking the CT X-ray tube manufacturing sector as an example, Nanovision, a static CT manufacturer, once acquired a controlling stake in Maimo Vacuum through investment, thereby commissioning the development of specialized X-ray tubes required for its static CT systems.

In this way, NanoVision Imaging can develop cutting-edge CT technology in a highly customized and relatively cost-effective manner, while Mammotome Vacuum has secured stable and continuous orders, enabling rapid growth in the field of X-ray tube manufacturing.

For ChenGuang Medical, which possesses core technologies, the second pathway is a favorable option. By deeply integrating with midstream imaging equipment manufacturers, it can develop magnetic resonance products featuring breakthrough technologies or significant cost advantages, offering a price-to-performance ratio far superior to the industry average, thereby establishing differentiated competition against other players in the sector. Compared to the first pathway, this approach enables ChenGuang Medical to effectively mitigate various risks associated with investment.

Third, continue to focus on further innovation in MRI components, winning with cost-effectiveness.This approach can be exemplified by Dunlee, an upstream supplier of imaging equipment that originally focused on the manufacturing of CT X-ray tubes. Over the course of its development, Dunlee transitioned from supplying individual imaging equipment components to providing comprehensive imaging chain services, offering personalized CT, MR, and X-ray imaging solutions tailored to customer needs and the specific characteristics of their imaging equipment. Leveraging this business model and robust product quality, Dunlee has effectively expanded its OEM market presence in China in recent years.

With innovation as its core competitive advantage, ChenGuang Medical can likewise continue along this path. Judging from ChenGuang Medical’s current product portfolio layout, the company can not only achieve further breakthroughs in the field of high-field-strength magnets but also leverage the competitiveness of its specialized superconducting magnet series to expand into markets beyond healthcare, such as high-energy physics, via a research-oriented approach. In particular, the latter strategy may help ChenGuang Medical unlock a market with immense potential.

Regardless of the path chosen, innovation remains the sole option for success when competing at the forefront of advanced technology. However, it is important to note that translating innovation into tangible results requires long-term support in terms of both time and capital. Even with the financial backing from the secondary market, ChenGuang Medical may still need to continue exploring its sustainable business model under stable conditions.