2022 Digital Mental Health Industry Report: Digital Therapeutics and Internet Healthcare Unlocking 230 Million Potential Users — An Irresistible Trend

The rapidly growing demand for mental health services in China has increasingly exacerbated the pain point of “supply-demand imbalance” in the market. Against this backdrop, digitalization has emerged in the mental health services sector to meet this need. In recent years, numerous companies have chosen different entry points to advance the industry’s digital transformation, exploring solutions to key challenges such as the imbalance between supply and demand in traditional mental health services, low willingness to pay, low standardization of services, and the difficulty in quantifying treatment outcomes.

What is the current state of digitalization in the industry? What additional support is needed? By surveying more than ten innovative companies and investment institutions, and interviewing dozens of experts, company founders, and investors, this report seeks to answer these questions and provide food for thought for enterprises striving together in this sector.

Core Viewpoints:

“Internet platform enterprises” are innovating their service models, showing a trend of integrated development, with digital products emerging as new growth drivers.

For “digital therapeutics product companies,” innovative service tools must be grounded in safety and efficacy.

The Psychological Counseling Industry Urgently Needs New Professional Mechanisms to Lay a Solid Foundation for Its Development.

In the early stages of digital development, collaboration among enterprises is more important than competition, as they work together to stimulate potential market demand.

To obtain the full report, please scan the QR code at the end of the article to add our assistant. If you have already added us, please feel free to reach out directly.

Digitalization Is Born to Enhance Accessibility and Effectiveness

Traditional mental health service resources are insufficient and unevenly distributed.According to data from the 2018 White Paper on Mental Health of Urban Residents in China, 16.1% of China’s population (nearly 230 million people) experience mental health issues of varying degrees. In recent years, this figure has shown a significant upward trend. Taking depression as an example, the Report on the Development of National Mental Health in China (2019–2020), released by the Chinese Academy of Sciences in 2021, indicates that the national prevalence rate of depression is approximately 17%.

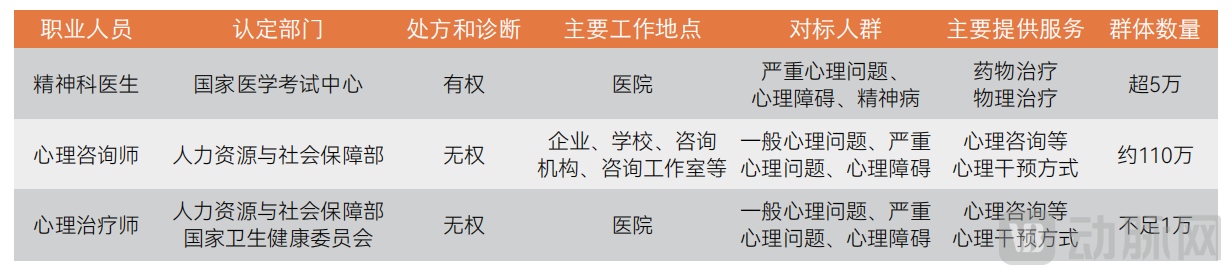

As the population with psychological issues in China continues to grow, the shortage of mental health service resources is becoming increasingly severe. Currently, professional personnel providing mental health services in China include psychiatrists, psychological counselors, and psychotherapists.

Inventory of Professionals in the Mental Health Services Sector

China has fewer than four psychiatrists per 100,000 people on average, which still lags behind international standards. Meanwhile, although there are over one million psychological counselors, fewer than 100,000 are actually engaged in full-time or part-time roles within the psychological counseling industry, indicating a substantial shortage. In addition to scarcity, mental health service resources in China are unevenly distributed, being concentrated primarily at the provincial and municipal levels, while grassroots-level resources remain severely inadequate.

Digitalization Was Born to Enhance the Accessibility and Effectiveness of Mental Health Services.In this context, digitalization has emerged as a necessity in the field of mental health services, initiating an irreversible trajectory of accelerated development. Digital mental health services refer to new service models and tools leveraging technologies such as the internet, big data, artificial intelligence, and virtual reality (VR) across various stages—including prevention and education, screening, assessment, intervention, and treatment. These innovations enable limited psychological and medical resources to reach a broader population while delivering more effective service outcomes.

Dual Drivers of Policy and Capital: Numerous Enterprises Flood into the Digital Mental Health Sector

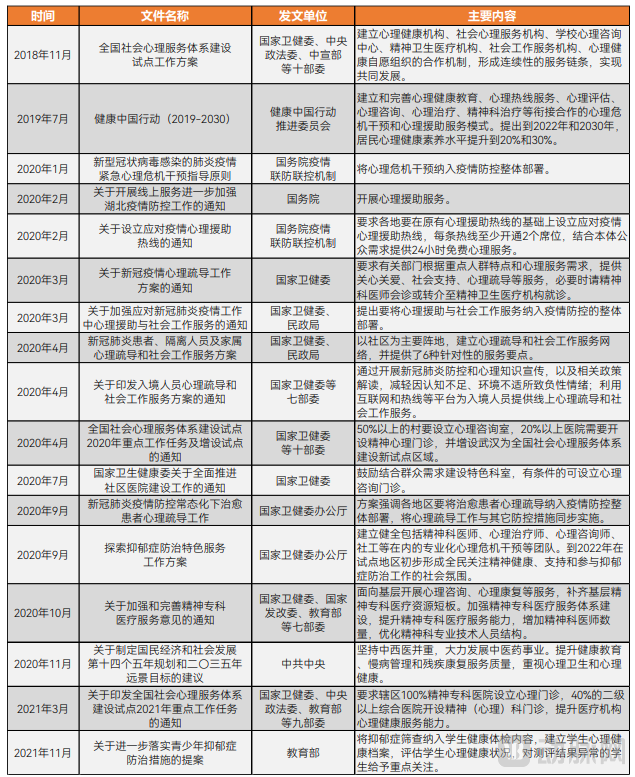

Policies are placing increasing emphasis on mental health.In recent years, policy authorities have frequently issued documents covering guidance, implementation, and sustained promotion of mental health services. These policies emphasize the establishment and improvement of a coordinated model for psychological crisis intervention and psychological assistance, integrating mental health education, psychological hotline services, psychological assessment, psychological counseling, psychotherapy, and psychiatric treatment.

A Review of National-Level Policies on Mental Health in Recent Years

Source: VCBeat Orange Database

Furthermore, under policy guidance, certain regions have initiated pilot programs to incorporate psychotherapy costs into the medical insurance system.These policies collectively demonstrate the state’s high regard for the public’s mental health. Against this backdrop, the mental health services sector has seen an influx of enterprises focused on digitalization, aiming to leverage the integration of technology and professional expertise to extend limited mental health resources to a broader population. By continuously exploring and innovating service models and tools, these efforts seek to enhance overall accessibility and effectiveness.

Capital Drives the Digitalization of Mental Health Services.In addition to policy guidance and support, astute capital has long begun to back and invest in the development of digital mental health services, with an increasing number of companies specializing in this sector securing financing.

“Internet platform enterprises” that deliver services via internet-based healthcare are generally at later financing stages, whereas “digital therapeutics product enterprises” focused on R&D in digital therapeutics are more numerous and predominantly at earlier financing stages. This indicates that the former sector is more mature, with an emerging competitive landscape, while the latter represents a newer track that has become a hot spot for corporate innovation and capital investment.

Internet Healthcare and Digital Therapeutics Drive the Digitalization of Mental Health Services

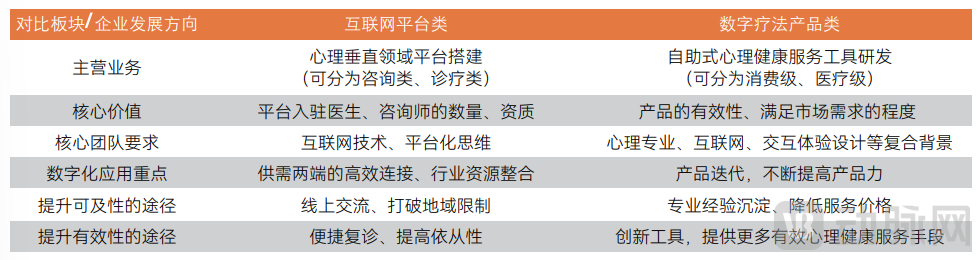

Digital Innovation Service Models and New Service Tools.To better investigate the current state of digitalization in the industry and future trends, we have categorized digital enterprises focused on mental health services into “Internet Platform Companies” and “Digital Therapeutics Product Companies.”

Comparison between “Internet Platform” Enterprises and “Digital Therapeutics Product” Enterprises

Source: Compiled from public information

“Internet platform-based enterprises” make psychological services more convenient and improve their accessibility.Internet-based diagnostic and treatment platforms, such as Zhaoyang Doctor, Haoxinqing, and Xiaodong Health, primarily provide online follow-up consultations and medication delivery for patients with severe psychological issues and mental disorders through internet hospital platforms. In contrast, counseling-oriented internet platforms, such as YiXinLi, Jiandan Xinli, and Yidianling, mainly offer psychological counseling services to individuals with severe psychological issues, general psychological concerns, and the healthy population via their self-built online platforms. Both models address the limitations of traditional offline diagnosis and treatment through online service modes, making access to psychological services more convenient and enhancing accessibility and effectiveness.

Digital therapeutics provide more service tools for psychological services, enhancing effectiveness.Enterprises that offer specific service products with digital therapeutics as their exploratory direction are categorized into two major types—consumer-grade and medical-grade—based on product application scenarios and market positioning. Companies focusing on consumer-grade products, such as Gese Technology, KnowYourself (Zhiwo Tansuo), and Mind Island Diary, primarily target individuals with general psychological concerns as well as the health-conscious population. They provide self-service or semi-self-service digital solutions designed to help users improve their emotional well-being, thereby enabling them to lead more positive and healthy lives.

Companies developing medical-grade products, such as Xinjing Technology, Wangli Technology, and Zheng’an Technology, primarily target severe psychological issues and associated behavioral disorders that significantly impair social functioning, such as insomnia and addiction. Products in this sector typically deliver digital therapeutics through software integrated with hardware devices like wearables. They are positioned to obtain National Medical Device Certifications based on efficacy data from clinical trials, thereby reaching patients via hospital and physician channels through prescription-based distribution. Furthermore, within the broader scope of mental health, childhood autism and developmental disorders represent key niche areas for medical-grade digital therapeutics, with companies such as Damai and Xiaomi and Peking University Medical Brain Health focusing specifically on these fields.

Platform-Based Enterprises Enhance Service Accessibility and Show a Trend of Integrated Development

Internet-based Diagnosis and Treatment Platforms: Facilitating Convenient Follow-up Visits and Improving Medication Adherence

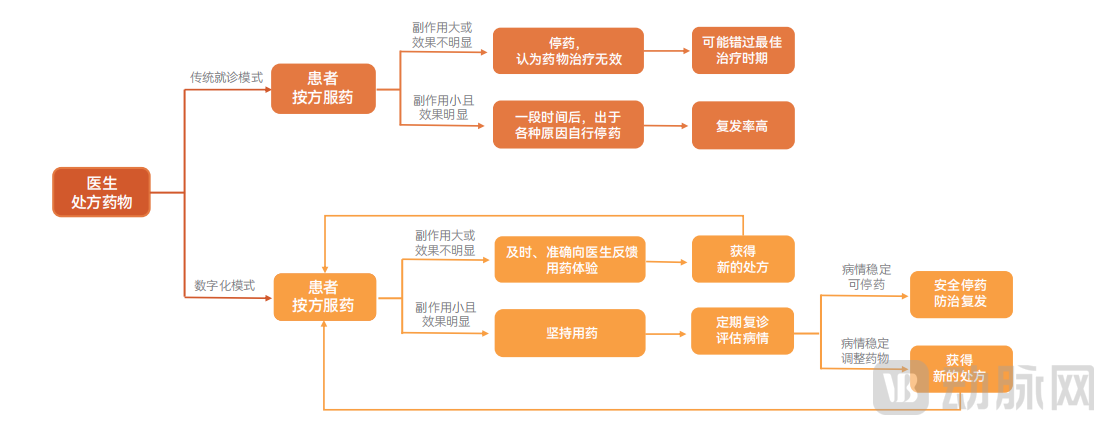

Efficient Communication to Identify Optimal Medication Regimens and Enhance Service Experience.Currently, there is a wide range of psychotropic medications available for doctors and patients to choose from. For each individual patient, determining which medication or combination of medications is effective with minimal side effects inevitably involves a “trial-and-error process.” During the first 1–3 months of initiating a new prescription, patients need to communicate their medication experiences frequently, promptly, and accurately to their physicians. Through thorough communication with their doctors, patients and physicians can jointly identify the optimal medication regimen.

In the traditional healthcare delivery model, two primary challenges directly impede patients’ pursuit of optimal medication regimens. First, because patients are required to receive long-term care from the same physician in an outpatient setting, they must accommodate the physician’s clinic schedule. For most working professionals, this often necessitates advance appointment booking and taking time off work. These “healthcare-seeking costs” frequently lead to delayed follow-up visits or even complete abandonment of follow-up care.

Second, due to the limited time available to outpatient physicians and the large number of patients, it is difficult for doctors to accurately recall the medication adjustment history of each patient. Therefore, to make efficient use of the limited consultation time, patients need strong abilities to summarize and organize information, enabling physicians to quickly understand their medication usage and provide recommendations for adjustments. In reality, these two major challenges in the traditional diagnosis and treatment model have hindered most psychiatric patients requiring pharmacological therapy.

Comparison of Current Medication Practices and Correct Protocols for Psychological Issues

In digital mental health service models, internet-based consultations facilitate long-term follow-up visits for patients on medication, eliminating the need for travel to hospitals, advance appointments, and time off work. Patients can simply upload their medication feedback and requests for assistance in text and image formats via mobile devices during their spare time (with the option to provide supplementary information multiple times). This ensures a comprehensive record of their condition, enabling more precise medication recommendations. As a result, patients can complete timely medication feedback and regular follow-up procedures without leaving home. Under the internet healthcare model, patients can identify optimal medication regimens, making adherence to long-term, regular follow-up visits significantly easier.

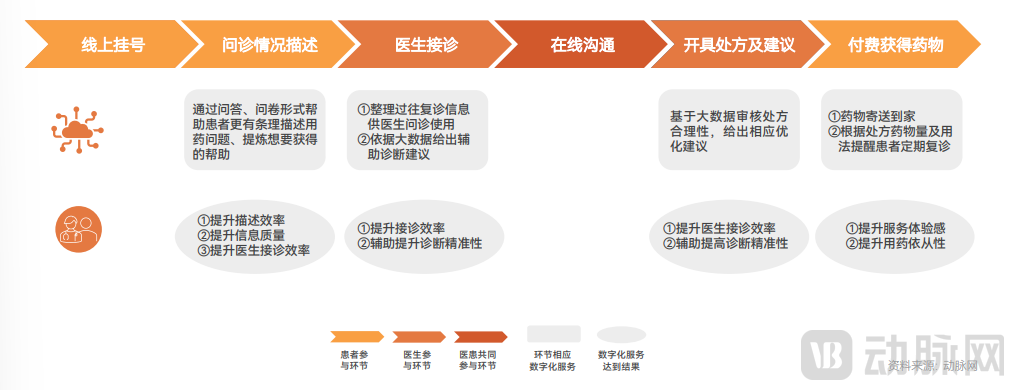

Digital services to enhance the efficiency and accuracy of diagnosis and treatment.In addition to the convenience afforded by its internet-based nature, the digital model of online psychological diagnosis and treatment leverages technologies such as big data and artificial intelligence to provide a range of digital services across key stages—including patient consultations, physician intake and prescription issuance, and medication procurement—thereby enhancing the efficiency and accuracy of online clinical care.

Digital Services and Corresponding Outcomes Across All Stages of Internet-Based Medical Consultations

After completing online registration, patients proceed to the chief complaint stage. Patients without a medical background often struggle to identify key information, resulting in low-quality or incomplete data that is insufficient to support diagnosis and treatment. This necessitates repeated inquiries by physicians during the consultation, potentially extending the entire diagnostic process to several hours or even days.

The diagnostic and treatment platform leverages technologies such as artificial intelligence to guide patients, through AI assistant Q&A or questionnaires, to describe diagnosis- and treatment-related information in a more comprehensive, direct, and effective manner, thereby ensuring the completeness and utility of the information and enhancing communication efficiency between patients and physicians.

Leveraging this digital service, the efficiency of subsequent physician consultations has been significantly enhanced. Furthermore, built on big data technology, the platform continuously refines its algorithms by integrating clinical practice guidelines and extensive real-world patient data from the platform. This enables the provision of auxiliary diagnostic recommendations during the clinical workflow, further improving consultation efficiency and contributing to greater diagnostic accuracy.

It is worth noting that currently, mature diagnostic and treatment platforms in the industry are equipped with complete pharmaceutical supply chains, with drug formularies comparable to those of hospitals. After a physician issues a prescription and the patient completes the payment online, the medication can be delivered directly to their home via express courier. Furthermore, based on the prescribed dosage and administration regimen, these platforms send follow-up consultation reminders when the medication is about to run out. This series of digital services enhances the efficiency and accuracy of online diagnosis and treatment across multiple dimensions and at various stages.

Consulting-oriented internet platforms that match supply and demand while ensuring consultation quality

Digitalization helps identify suitable counselors, reducing trial-and-error costs.Similar to finding the optimal medication regimen, identifying the most suitable psychotherapist is not an instantaneous process; it often requires multiple attempts and inevitably involves a trial-and-error phase.

Each counselor’s area of expertise and the underlying causes of each client’s psychological issues are unique. If clients can find a counselor whose specialized areas most closely align with the root causes of their psychological concerns when seeking counseling, it will significantly enhance the effectiveness of the therapy and shorten the trial-and-error process involved in finding the “right-fit” counselor.

So, how can one find the most suitable counselor among many more quickly and efficiently, thereby reducing the cost of trial and error? Digital services offer a viable solution—matching and recommendations through big data algorithms, with continuous algorithm training based on feedback from each consultation.

Figure 13: The Process by Which the Platform Uses Digital Technologies to Match Clients with Counselors

Digital Courses and Training to Enhance Industry Consulting Service Capabilities.Since the Ministry of Human Resources and Social Security of China abolished the certification examination for psychological counselors in September 2017, there has been a regulatory vacuum regarding the accreditation and oversight of psychological counselors at the national level. Moreover, certified counselors lack access to mechanisms and resources for continuous professional development post-certification. Consequently, the industry has remained in a state of “unregulated growth,” characterized by uneven professional competencies among practitioners, with the number of qualified and excellent counselors failing to meet the substantial market demand.

Against this backdrop, online psychological counseling platforms have begun leveraging digital technologies to gradually establish corresponding training systems for psychological counselors and related “quality control” mechanisms. In addition to providing professional platforms for psychological counselors, these platforms also assume, to a certain extent, the roles of “continuing education” and “oversight.”

In the realm of “continuing education,” digital technologies have facilitated a robust integration of offline and online professional training for psychological counseling. Regular, centralized offline training combined with long-term online training and supervision enables the limited high-quality psychological training resources in the industry to reach a broader base of professional counselors, thereby collectively enhancing the quality of psychological counseling services. Regarding “supervision,” the platform has established a client feedback mechanism that assesses counselors’ competency levels through metrics such as satisfaction rates, dropout rates, and improvement rates, assigning corresponding ratings via big data algorithms. For counselors who fail to meet the assessment standards, the platform mandates additional theoretical study, supervision, and practical training based on their rating outcomes.

Ultimately, however, addressing the issue of “oversight” for counselors, providing adequate protections for both clients and practitioners, and safeguarding the healthy development of the industry will depend on national-level policies and regulations. The original intent behind abolishing the certification system for psychological counselors was to pave the way for more standardized and favorable policies and regulations that would foster a conducive environment for the industry’s sound growth. After years of self-exploration and integration of international best practices, it is anticipated that relevant policies and regulations will be introduced in the future to provide more robust, systematic, and comprehensive “oversight” of the psychological counseling industry.

Internet Platforms Are Trending Toward Integrated Development, with Digital Products Becoming a New Growth Engine for Enterprises

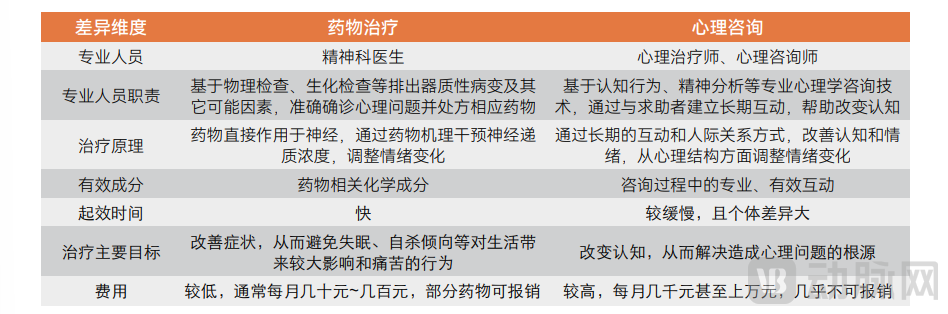

The "divide" between doctors and counselors has resulted in a lack of collaborative treatment for psychological issues.Medication and psychological counseling differ in terms of therapeutic mechanisms, onset of action, cost, and active components. The treatment and improvement of psychological issues are not a matter of choosing one over the other; rather, integrated solutions should be provided at different stages, tailored to factors such as the severity of the individual’s psychological condition, their specific service needs, and financial capacity.

Comparison of the Differences Between Pharmacotherapy and Psychological Counseling

Currently, in China's mental health services sector, medication prescriptions and psychological counseling are provided by two distinct roles—psychiatrists and counselors—and an effective collaborative mechanism between these two types of professionals has not yet been established.

Internet-based mental health platform: Creating an integrated solution for medication and psychological counseling through digitalization.Two types of platforms, focusing on consultation and diagnosis/treatment respectively, are gradually extending into each other’s business areas through self-development or partnerships, aiming to form a closed loop of integrated pharmaceutical and psychological counseling services.

Furthermore, in addition to the integration of pharmacotherapy and psychological counseling, the convergence of online and offline services has emerged as a common development trend among mental health platform enterprises. Research indicates that, particularly within the realm of psychological counseling, the online experience has not yet achieved therapeutic outcomes equivalent to those of offline sessions for all help-seekers; thus, offline mental health services remain indispensable. Consequently, mental health platform companies are increasingly establishing offline clinics and counseling centers to provide integrated online-offline mental health services to users.

Digital products have become a new growth driver for business.In addition to the aforementioned convergence trends, internet platform companies are also actively expanding into the digital product sector. On one hand, they leverage the vast amounts of data accumulated on their platforms to develop proprietary algorithms, continuously enhancing the service efficiency of doctors and counselors. Examples include AI-assisted diagnostic tools, facial emotion recognition systems, and AI-powered pre-consultation medical record organization assistants. On the other hand, through in-house R&D or strategic partnerships, these companies provide self-service or semi-self-service digital products to users seeking help, thereby strengthening the effectiveness of psychological interventions. Such offerings include various self-assessment questionnaires, psychology-related courses, and meditation-based emotional regulation products.

For internet platform enterprises, expanding into the product sector not only consolidates and strengthens existing business lines but also serves as a powerful new growth engine. As doctors and counselors constitute the platform’s most critical service resources, leveraging digitalization to enhance their efficiency is a key approach to raising the ceiling of the platform’s service capacity. Meanwhile, self-service products that visitors can purchase and experience on a paid basis will enable deeper exploration and satisfaction of the needs of the platform’s large base of help-seekers, thereby generating new business growth opportunities.

Digital Therapeutics Innovation Service Tools for Mental Health: Enhancing Accessibility and Effectiveness

Consolidate valuable intervention experience to enhance the replicability and accessibility of professional services.One of the core components of mental health service resources is the extensive specialized psychological knowledge held by psychiatric experts and psychological counseling professionals, along with the rich clinical and intervention experience they have acquired based on this expertise.

In traditional clinical practice, access to such resources relies exclusively on direct engagement with specialists. However, empowered by digital technologies, these resources can be systematically captured, recorded, categorized, and standardized as data. Leveraging this valuable data through big data analytics and algorithmic techniques, artificial intelligence enables the automatic replication of effective intervention strategies—validated in real-world settings—whenever needed. Ultimately, by enhancing the replicability of professional services and reducing dependence on specialists, the intervention process shifts toward a model dominated by human-computer interaction with specialist support as a supplement, thereby improving service accessibility.

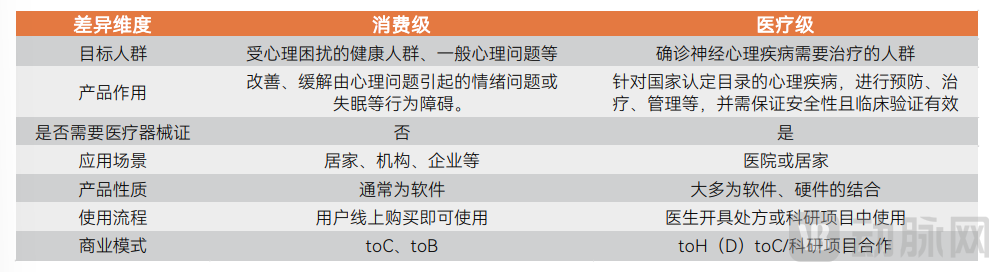

An endless stream of innovative digital therapeutics products is emerging, with simultaneous advancements in both consumer-grade and medical-grade sectors.Currently, digital therapeutics products in the field of mental health services are categorized into two types: consumer-grade digital products and medical-grade digital therapeutics, based on factors such as target population and market positioning.

Comparison of Consumer-Grade and Medical-Grade Products in Digital Therapeutics

Consumer-grade products prioritize the improvement and alleviation of emotions and behaviors stemming from psychological issues, whereas medical-grade products focus on delivering clinically validated outcomes in the prevention, treatment, and management of mental disorders listed in the national catalog, while ensuring safety.

Consumer-grade digital products fill market gaps, with differentiation being a key product strength.

A substantial unmet demand for mental health services among individuals with mild conditions has spurred the emergence of consumer-grade digital products.For Mild CasesUsers are generally healthy individuals who are temporarily burdened by mild psychological issues or who seek to maintain or pursue a better quality of life. Therefore, pharmacological interventions within traditional treatment modalities are not suitable, while stable, long-term psychotherapy plans often present poor cost-effectiveness. Driven by substantial market demand, the industry has seen an emergence of numerous digital mental health services based on digital therapeutics. Users can simply place orders online to access these tools independently, embarking on a journey of self-guided psychological intervention and self-regulation.

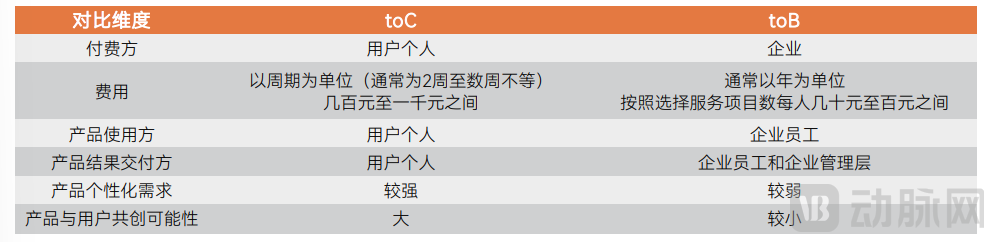

Whether it targets the consumer (C-end) or business (B-end) market remains to be validated by the market.Currently, there are two primary market promotion models for consumer-grade digital mental health intervention products: B2C, which directly reaches consumers, and B2B, where enterprises pay to provide digital psychological interventions for their employees.

Since users themselves are the payers for ToC products, “user self-motivation” holds a natural advantage during product usage. A key factor in the effectiveness of digital consumer self-service products delivered via software is adherence—specifically, consistent engagement throughout the full intervention cycle—with “user self-motivation” being one of the most significant influencing factors. Benefiting from high levels of “user self-motivation,” ToC products are better positioned to accumulate substantial real-world user data for product optimization and iteration, as well as to leverage opportunities for user co-creation.

The other side of the coin is the persistently high promotion thresholds and costs for to-C products. According to research, while the pandemic has served as a milestone in significantly raising public awareness of mental health in China, willingness to pay for mental health services has not increased accordingly; instead, it shows a trend of contraction. Industry experts believe that the key to scaling up to-C products lies in continuously lowering prices, provided that efficacy is guaranteed.

Comparison of To-C and To-B Models for Consumer-Grade Digital Products

B2B products have a distinct advantage in terms of “securing payment.” However, because the payer and the user are not the same entity—meaning employees may not yet recognize their need for mental health services—they often lack sufficient self-motivation to fully engage with the product. Furthermore, since the delivery of product outcomes involves parties beyond just the end-users, there is a potential risk that employees may complete product experience tasks in a biased or targeted manner, leading to inaccurate usage data. This poses a challenge for digital health companies that rely on authentic data to continuously optimize and iterate their product performance.

Therefore, to-C products need to leverage real user usage data and willingness to co-create, accelerating product iteration and improving “efficacy” while enhancing digital performance and reducing reliance on manual labor, thereby lowering service prices and opening up a larger consumer market; to-B products should seize the window of opportunity where “someone is willing to pay,” explore better user engagement strategies to obtain more effective data for iterative product improvements, continuously enhance “efficacy,” build a reputation for effectiveness, retain paying enterprises, and expand into more businesses.

However, as Jiang Xiaodong, Managing Partner at Changling Capital Management, emphasized during his research, companies in the mental health services sector that focus on product development should place greater emphasis on enhancing product strength and efficacy. In this growing market, what matters more than the business model is how to deliver high-quality, effective products that truly meet user needs.

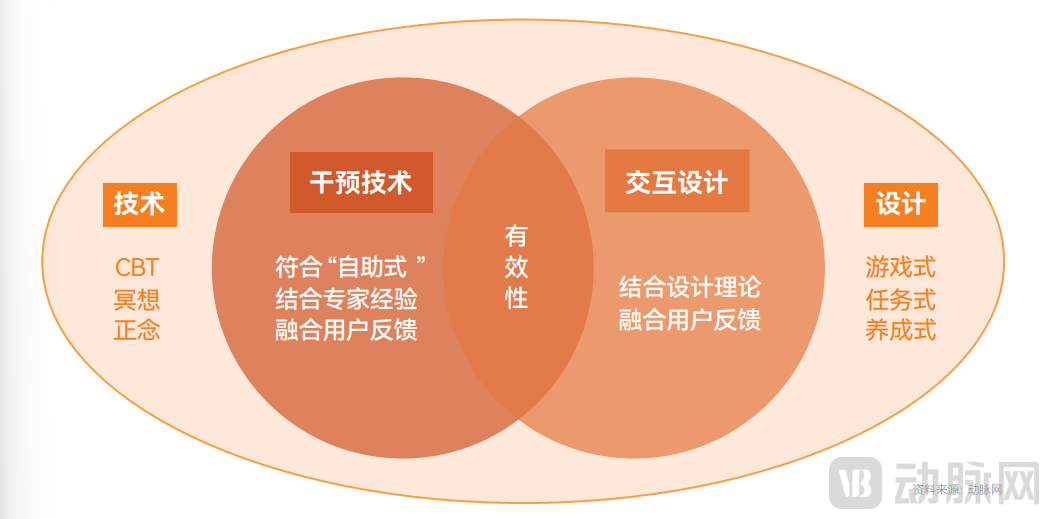

Effectiveness is the key to product differentiation, relying on the organic integration of user experience, expert insights, and technology.Research indicates that the theoretical foundations underlying current consumer-grade digital therapeutic products are similar, which inevitably leads to product homogenization in the early stages of industry development. The key to overcoming this homogenization lies in continuously enhancing product efficacy. Two critical dimensions for refining and improving efficacy are “intervention technology” and “interaction design”; these two elements complement each other and drive a spiral, co-evolutionary improvement in product effectiveness.

Foundations and Key Points for Enhancing the Effectiveness of Consumer-Grade Digital Products

There are no shortcuts in the process of product refinement. The high-cost, labor-intensive efforts required in the early stages are essential for establishing a product’s long-term market position and competitive barriers, ultimately enabling the enterprise to capture a larger market share. During this period, companies must focus on acquiring more valid, real-world data in less time to accelerate product iteration and upgrades. By continuously enhancing both product efficacy and self-service capabilities, companies can reduce product costs and lower market pricing, thereby driving volume growth in broader markets.

Medical-grade digital therapeutics offer innovative treatment approaches that complement traditional therapies.

Digital therapeutics are predominantly focused on the assessment phase, with the least emphasis on the treatment phase.Currently, among the digital therapeutics approved in China, products utilized for assessment account for the largest proportion, while those intended for disease treatment represent the smallest share. There is an urgent need for more therapeutic products targeting conditions listed in the mental disorder catalog to emerge, obtain approval from the National Medical Products Administration (NMPA), and be implemented in clinical practice.

“Product refinement” and “clinical trials” proceed in tandem to create highly effective, medical-grade digital therapeutics.Research indicates that the field of mental health, positioned around medical-grade digital therapeutics, has seen numerous attempts to integrate emerging technologies and disciplines based on psychological intervention techniques and digital infrastructure. This integration reduces users’ “difficulty of use” and improves adherence; meanwhile, it enhances the precision of assessing and monitoring user status, thereby enabling continuous refinement of product design and improving the effectiveness of product usage.

Currently, the indications for medical-grade products in the field of mental health are largely concentrated on insomnia disorder, addiction, and post-traumatic stress disorder. As mentioned above, medical-grade products inherently possess a certain degree of “differentiation” due to their integration with new technologies and interdisciplinary approaches. Nevertheless, product refinement must not be relaxed. This requires continuous algorithm optimization leveraging large volumes of real-world user data, while simultaneously developing more personalized intervention strategies to address the needs of patients at different disease stages and with varying severity levels.

Through continuous “product refinement,” once a product achieves the safety and efficacy required to meet market demands, it will face the test of “clinical trials.” For medical-grade products positioned for clinical use, obtaining a medical device registration certificate from the National Medical Products Administration (NMPA) is a prerequisite for market launch. Currently, the field of digital therapeutics for mental health in China is in its very early stages, with few reference protocols available for the design of clinical trials for related medical-grade products. Therefore, developing effective and feasible clinical trial designs represents another significant “market-entry hurdle” that companies must overcome. Enterprises need to collaborate with experts to explore and rigorously implement reasonable clinical trial designs based on product characteristics and intended validation objectives.

Digital therapeutics serve as a powerful complement to, rather than a replacement for, traditional diagnostic and therapeutic approaches.The industry is in urgent need of more effective, highly standardized, and scalable treatments and tools for mental and psychological disorders to supplement the shortcomings of traditional therapies and break through their limitations.

Digital therapeutics represent one of the most promising and imaginative avenues in healthcare. Development must remain firmly grounded in professional expertise, industry guidelines, and expert experience, leveraging technology as an enabling tool to enhance the efficiency, accessibility, and replicability of diagnosis and treatment. Digital therapeutics are not intended to replace traditional treatments or medical experts; rather, they serve as an effective complement. Provided their safety and efficacy are validated, they can improve the efficiency and outcomes of conventional therapies, thereby contributing to digital mental health service tools and acting as an accelerator for industry development.

The Digitalization Trend Is Irreversible: The Industry Remains in Its Early Stages as Companies Build Their Own Moats

In the future, the competitive landscape of platform-based enterprises will gradually become clearer. Leading platform companies will continue to capture larger market shares, while product-focused enterprises will continuously launch safe and effective mental health service products that are evidence-based and thoroughly validated by the market. In each niche segment, dominant products with absolute competitive barriers will gradually emerge.

The Industry Urgently Needs a New Professional Mechanism for Consultants to Lay a Solid Foundation for Digital Development

Industry insiders have stated that China is actively establishing a professional framework for psychological counselors. Due to significant differences between China and Western countries in terms of the healthcare system, insurance payment mechanisms, and public demand for mental health services, although the more mature professional systems abroad offer valuable references, they cannot be directly replicated.

Nevertheless, it is clear that raising the entry standards for psychological counselors and improving the systems for continuing education and professional oversight represent the overall direction. It is believed that in the near future, the mental health services sector will see the introduction of a new professional mechanism for psychological counselors. At that time, the mental health services industry will continue to develop rapidly on a more solid foundation, thereby also accelerating the process of digitalization.

"Balancing 'Product Refinement' and 'Market Promotion',"Forging a Virtuous Development Environment

On the demand side of mental health services, user awareness is growing rapidly, but genuine willingness to pay still depends on the penetration of market education and the establishment of industry trust through the satisfaction of successive waves of early adopters. With strong attention and support from both policy makers and capital investors, it is only a matter of time before the market is fully activated. At this critical stage, rather than competing within the currently limited developed market, companies should join hands to build market trust, devote themselves to carefully refining safe and effective products, and collectively expand the true market size of the digital mental health services industry.

The above is an excerpt of the main content of the report. The complete framework of the report is as follows:

Chapter 1: Digitalization Forges New Models and Tools for Mental Health Services

1.1 Digitalization Is Born to Enhance Accessibility and Effectiveness

1.2 Dual Drivers of Policy and Capital: Numerous Enterprises Enter the Digital Mental Health Sector

1.3 Internet Healthcare and Digital Therapeutics Drive the Digitalization of Mental Health Services

Chapter 2 Platform-Based Enterprises Enhance Service Accessibility, Showing a Trend of Integrated Development

2.1 Internet-based mental health platforms: breaking geographical barriers and enhancing service accessibility

2.2 Internet-Based Diagnosis and Treatment Platforms: Facilitating Convenient Follow-Up Visits and Improving Medication Adherence

2.3 Consultation-Oriented Internet Platforms: Matching Supply and Demand While Ensuring Consultation Quality

2.4 Internet Platforms Are Trending Toward Integrated Development, with Digital Products Becoming a New Growth Engine for Enterprises

Chapter 3: Digital Therapeutics Enrich the “Toolkit” for Mental Health Services; There Are No Shortcuts to Product Refinement

3.1 Innovative Digital Therapeutics Tools for Mental Health: Enhancing Accessibility and Effectiveness

3.2 Consumer-grade digital products fill market gaps, with differentiation being the key product strength

3.3 Medical-Grade Digital Therapeutics: Innovative Treatment Modalities with Complementary Advantages to Traditional Therapies

Chapter 4 Future Trends

4.1 The Digitalization Trend Is Irreversible: The Industry Remains in Its Early Stages, and Companies Are Building Moats

4.2 The Industry Urgently Needs a New Professional Mechanism for Consultants to Lay a Solid Foundation for Digital Development

4.3 Balancing “Product Refinement” and “Market Promotion” to Foster a Healthy Development Environment

Chapter 5 Corporate Case Studies

5.1 Pause Lab—Digital Mental Fitness Gym

5.2 Xinjing Technology—Focused on XR Digital Therapeutics (DTx) Medical Solutions for Mental Health

5.3 Modern Health—Exclusive Mental Health Service Program for Corporate Employees

5.4 Talkspace—An Online Therapist Service Platform Continuously Disrupting and Innovating

Please scan the QR code to add our assistant and obtain the full report. If you have already added us, please initiate a conversation to request it.

Special Acknowledgments (in order of survey):

Mr. Xu Feng, Vice President of Haoxinqing; Ms. Qian Zhuang, Founder and CEO of KnowYourself; Mr. Li Dai, Founder and CEO of Wangli Technology; Ms. Guo Tingting, Founder and CEO of Gese Technology; Mr. Wang Ding, CEO of Yidianling; Dr. Zeng Songtian, Dean of the Damai and Xiaomi Institute for Child Development; Mr. Jiang Xiaodong, Managing Partner of Changling Capital; and Mr. Cao Qun, Founder and CEO of Xinjing Technology.