Cutting Through the Noise: The Life Science Upstream Sector Remains Resilient

By Chengshu Investment, published with authorization from VCBeat.

The Trend of Domestic Substitution Remains Unchanged Amid the Pandemic

In the first half of 2022, the COVID-19 pandemic in China adversely affected the operational performance of some upstream life sciences companies in the second quarter, impacting either the supply side or the demand side. However, as the epidemic situation subsequently improved, the upstream life sciences industry is expected to recover, and the trend toward domestic substitution will persist in the long term.

Currently, the localization rate for most niche segments in the upstream life sciences industry remains below 30%. While the pandemic has, to some extent, accelerated the process of domestic substitution, the long adoption cycle for upstream products means that early gains in market share for domestic products may be slow. However, driven by favorable policies, accumulated technological expertise among local manufacturers, and downstream demand for cost reduction and efficiency improvement, locally produced upstream products are expected to accelerate domestic substitution once they have been validated by the market.

Domestic Production Rate of Selected Upstream Life Sciences Products:

Source: China Merchants Bank Research Institute

Policy Dividends Boost Domestic Substitution

Policy dividends at the national strategic level have successfully driven business growth for a number of upstream IVD and biopharmaceutical companies, with some emerging as industry leaders whose sales profits and performance rival those of downstream enterprises. Notable examples include Vazyme, Sansure Biotech, and Sino Biological.

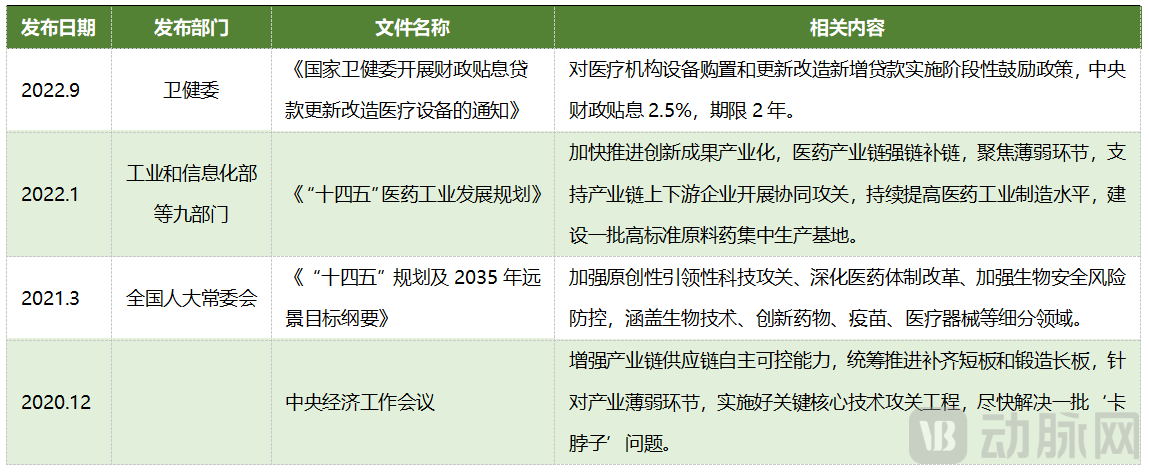

In the post-pandemic era, to reduce the domestic biomedical industry chain’s reliance on foreign sources, governments at all levels have introduced multiple incentive policies aimed at increasing the localization rate of upstream equipment and consumables in sectors such as biopharmaceuticals and in vitro diagnostics. The interest-subsidized loan policy for medical equipment renewal and upgrading, issued in September 2022, has been particularly beneficial to the medical equipment sector. Statistics show that from the policy’s announcement until October 11, approximately RMB 19.155 billion in interest subsidies had been implemented across various provinces and municipalities, with overall expectations indicating the release of hundreds of billions of yuan in demand for the medical device market. Local enterprises specializing in their respective fields and possessing extensive sales experience, such as Truking Technology, Eastpharma, and Morimatsu International, are poised to further capture market share from imported brands and rapidly achieve domestic substitution under this favorable policy environment.

Data Source: Public Information Collection

Accumulation and Innovation in Foundational Technologies Are the Core Drivers of Domestic Substitution

Domestic upstream companies are gradually narrowing the technological gap with overseas manufacturers by continuously enriching their product and service portfolios, while demonstrating significant advantages in cost control, customized services, and response speed. Taking the culture media sector as an example, the price of domestically produced basal media is only about one-third that of imported products when using catalog media, while the price of domestically produced feed media is nearly two-thirds that of imports. For both catalog and customized products, the lead time for leading domestic culture media manufacturer OPM (Shanghai Opm Biotech Co., Ltd.) is generally around 2–4 weeks, whereas imported culture media typically have a lead time of three months or more due to international logistics and geopolitical factors. As domestic culture media manufacturers continue to upgrade their technologies, expand production scales, mature their manufacturing processes, and enhance product quality stability, the pace of import substitution is expected to accelerate further.

Cost Reduction, Efficiency Gains, and Safety Needs Drive Downstream Companies to Turn to Domestic Suppliers

Although China’s policies provide strong support for innovative drugs, the national medical insurance system holds a dominant position in pharmaceutical payment. The short-term clustering of approvals for similar innovative drugs has also intensified market competition. From 2016 to 2021, medical insurance negotiations drove a substantial 44%–62% reduction in hospital procurement prices for drugs, with a trend toward even deeper cuts. This has compelled domestic innovative pharmaceutical companies to place greater emphasis on upstream production costs and efficiency.

China’s upstream life sciences supply chain has long relied on overseas sources, with high-end products such as biological filtration membranes and single-use bioreactors being almost entirely imported. In the wake of the pandemic and the enactment of the Biden Administration’s relevant legislation, an increasing number of biopharmaceutical companies have incorporated geopolitical risks into their bidding criteria. Domestic pharmaceutical companies are placing greater emphasis on supply chain stability, thereby creating more windows of opportunity for import substitution with domestically produced alternatives.

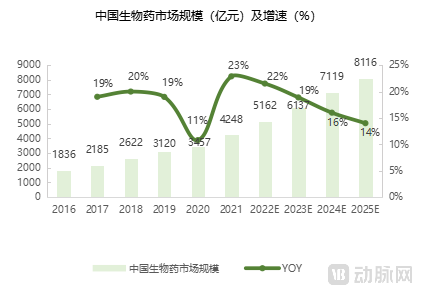

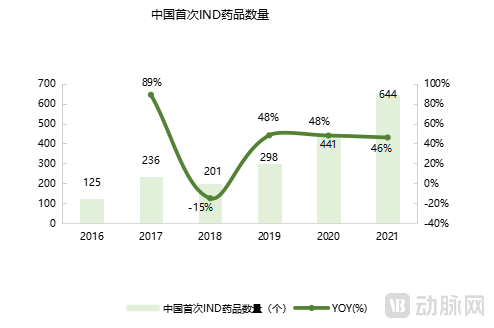

From 2016 to 2021, the market size of biological drugs in China grew from RMB 181.6 billion to RMB 424.8 billion, with a compound annual growth rate (CAGR) of 18%, which was twice the global growth rate during the same period. It is projected that by 2025, the domestic biological drug market will exceed RMB 800 billion, maintaining a CAGR of 18% from 2021 to 2025E. In terms of R&D, the number of first-in-class Investigational New Drug (IND) applications in China increased from 125 in 2016 to 644 in 2021, representing a CAGR of 39%. The vigorous advancement in drug R&D will further drive the expansion of the biological drug market.

Data sources: OPM’s prospectus, PharmCube

CXO Capacity Is Not Truly in Surplus

According to statistics, CDMOs with a high proportion of overseas revenue (over 50%) and a focus on late-stage R&D do not currently face issues of overcapacity. They enjoy substantial market potential and are less affected by the waning boom cycle of domestic innovative drugs. Leading CXOs primarily engaged in overseas business have not slowed their capacity expansion efforts, as exemplified by WuXi Biologics, the industry leader that consecutively completed the acquisitions of Ke Wang and Harbour BioMed this year. Global production capacity is not truly in surplus; rather, CXOs predominantly serving the domestic market may face greater risks of declining demand due to tightened R&D spending by some downstream clients.

Geopolitics Will Not Reverse the Long-Term Upward Trend

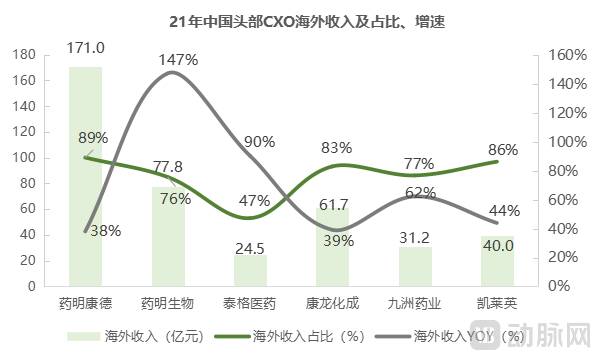

Even as escalating Sino-U.S. tensions led to a sustained slump in the performance of numerous new drug and medical device companies on Hong Kong’s secondary market, and President Biden’s September 2022 executive order aimed at expanding U.S. biomanufacturing capacity sent chill winds through China’s CXO sector, leading Chinese CXO firms still maintained high proportions of overseas revenue. In the first half of 2022, WuXi AppTec generated RMB 11.9 billion from U.S. clients, a year-on-year increase of 104%, accounting for 67% of its total revenue, up from 50% in 2021. During the same period, WuXi Biologics recorded RMB 3.9 billion in revenue from North America, a 78% year-on-year increase, representing 54% of its total. In 2021, the overseas revenue shares for Tigermed, Pharmaron, Jiuzhou Pharmaceutical, and Asymchem were 47%, 83% (with 64% from North America), 77%, and 86%, respectively, all reflecting year-on-year growth exceeding 35%.

Data Source: Wind, Company Announcements

In the long term, China’s upstream biopharmaceutical market accounts for less than 20% of the global share, making international expansion a long-term strategic choice for domestic companies. During the pandemic, some Chinese manufacturers of reagents, consumables, and equipment promptly responded to R&D demands related to COVID-19, achieving breakthroughs in the international market. Leading upstream IVD companies such as Vazyme and Sansure Biotech benefited significantly from the pandemic; in the first half of 2022, their revenues from COVID-19-related businesses (including diagnostic raw materials and end-user testing kits) grew by 30%–100% on a high base. Similar trends were observed among protein reagent companies such as Sino Biological, ACROBiosystems, and Nearshore Protein.

Cost Advantages Are a Key Factor in Global Biologic Drug Manufacturing Capacity Choosing China

In the first half of 2022, Pfizer’s COVID-19 therapeutic Paxlovid generated $9.6 billion in revenue, with the combined order value for WuXi AppTec, Asymchem, and Porton Pharma Solutions estimated at less than $2 billion. This reflects the relatively low value captured by Chinese CXO (Contract X Organization) firms within the global pharmaceutical industry chain. According to data from Zheshang Securities, the overseas market share of nine leading domestic CXO companies was only 9.13% in 2021, remaining at a low level. Although the technical proficiency of Chinese engineers is now comparable to that of their counterparts in Europe and the United States, their average compensation is only one-third as high. Consequently, Western pharmaceutical companies have strong incentives to outsource production to Chinese CXO firms that offer greater efficiency and lower costs, suggesting significant room for growth in overseas market share. Driven by the “engineer dividend” in China, the shift of global biopharmaceutical manufacturing capacity to China is an inevitable outcome of industrial division of labor and resource optimization. Despite short-term fluctuations caused by the pandemic and geopolitical tensions, this long-term trend is expected to persist.

Many Domestic CXOs Are Actively Expanding Overseas Production Capacity

Chinese CXO companies are mitigating the risk of client attrition due to geopolitical tensions by expanding their overseas production capacity, which also facilitates the acquisition and undertaking of projects from international biopharmaceutical clients. In February 2022, GenScript officially commenced operations at its production and R&D facility in Singapore, which is equipped with highly automated protein production and gene synthesis services spanning over 30,000 square feet. In July 2022, WuXi AppTec announced plans to invest S$2 billion (approximately RMB 9.7 billion) over the next decade to establish R&D and production bases in Singapore. Additionally, other Chinese enterprises, including Chia Tai Tianqing Pharmaceutical Group, Fosun Pharma, and Singleron, have also chosen to build production capacity in Singapore.

Overall, short-term fluctuations driven by the pandemic and international policies have cooled the biopharmaceutical industry, prompting structural adjustments in the production supply chain. China’s technological reserves in the upstream segment are expected to enable core reagents and consumables—previously difficult to replace—to rapidly scale up production capacity as policy benefits are realized, creating opportunities for locally produced upstream products with cost advantages. From a capital market perspective, the cooling of various investment sectors has not dampened overall industry demand. Judging by the net profit attributable to shareholders of CXO companies, leading firms continue to maintain double-digit growth, and their overseas revenue continues to rise despite geopolitical tensions. Furthermore, bolstered by China’s unique engineer dividend and an increasing number of upstream enterprises expanding into international markets, import substitution and even globalization of China’s upstream biopharmaceutical industry will undoubtedly be long-term trends shaping the industry landscape.