Chengshu Investment Founder Lou Min: Avoiding Greed and Haste, Capturing Deterministic Investment Opportunities That Weather Bull and Bear Markets

Chengshu Investment, established 13 years ago, is akin to the "Sweeping Monk" in the capital markets.

It appears to deliberately avoid drawing attention to itself. Apart from a few scattered mentions on the official website of Chengshu Investment and in corporate financing news, it is difficult to obtain more information about this investment firm from other public channels.

Chengshu Investment: Focused on Growth-Stage Investments in Life Sciences and Consumer Healthcare, having navigated the industry for many years, its investment portfolio is not particularly large in terms of quantity. Yet it possesses a remarkably keen eye, capable ofSmileAlign Dental, Baiying Bio, Sailuo Medical, Genetron HealthIt brought more than ten star projects under its wing in their early stages, and continuously increased investment and integrated industrial resources to boost corporate growth during the development process, providing the most enthusiastic support to enterprises like an external CEO.

Chengshu Investment's Investment Cases

Recently, VCBeat andLou Min, Founder of Chengshu InvestmentWe engaged in an in-depth conversation and were privileged to document this “low-key powerhouse’s” first public interview.

Lou Min, Founding Partner of Chengshu Investment

Lou Min holds a Bachelor’s degree in Economics from Fudan University and a Master’s degree in Monetary Banking from the Financial Research Institute of the People’s Bank of China. With over 30 years of experience in the financial investment industry, he has led investments in a number of industry-leading enterprises, including Smartee Denture, Baiying Biotechnology, Wanji Technology (300552), Dinghan Technology (300011), Xianhe Environmental Protection (300137), Longma Sanitation (606686), Wind Information, and Caixin Media, achieving outstanding investment performance.

Formerly served as General Manager of the Investment Banking Department at Southern Securities, Vice President of Industrial Securities, Chairman of Xingye Venture Capital, and Member of the Third Investment Banking Committee of the Securities Association of China. Possesses extensive experience and resources in the capital markets. The investment banking team under his leadership has long maintained a leading position in China’s securities market and creatively achieved multiple “China’s firsts” in the capital markets, including the first private placement and the first put warrant.

Core Viewpoints of This Article:

1. Adhere toResearch Capability is Investment Capability, based on researchBottom-upto deeply explore potential sectors and enterprises.

2. We do not pursue scale in terms of quantity, nor do we excessively seek to maximize the size of individual investments or the assets under management (AUM) of our funds; instead, we adhere to“Less is More”investment philosophy.

3. Concentrated Investment with Aggressive Allocation, performing repetitive tasks within one's area of expertise.

4. Begin with the End in Mind, Prioritize Exit Strategies. Rigorous post-investment management processes ensure timely risk identification and the capture of exit opportunities.

5. Favorable Outlook for OwnershipEnterprises with globalized product or service capabilities.

Below is the dialogue between VCBeat and Lou Min:

VCBeat:From investment banking, to cross-industry equity investment, and then to focusing on life sciences and consumer healthcare, how did Chengshu Investment gradually adjust its “aim”?

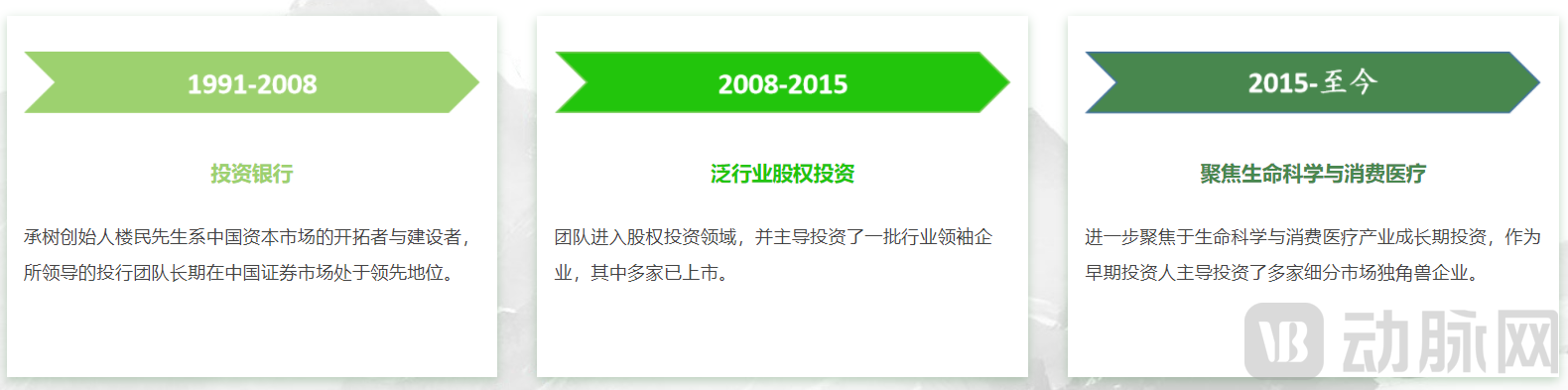

The Growth Journey of Chengshu Investment

Lou Min:Once investment banking reaches a certain level, there is a desire to trace back to the source. To help companies smoothly enter their maturity stage, one must move forward and provide support directly through equity investments. Moreover, we discovered at that time that there are several critical steps in the early stages of corporate development; missing these opportunities and participating at a later stage actually has limited significance for the company.

If one attempts to cover every industry, it becomes impossible to develop profound insights within specific niche sectors. Therefore, during the first few years after founding Chengshu, we continuously adjusted our strategic positioning and narrowed our scope of industry observation, ultimately focusing on life sciences and consumer healthcare.

For instance, we consider consumer healthcare to be a classic “long slope, thick snow” sector. It addresses higher-order needs such as improved quality of life and emotional well-being—including love, social interaction, social recognition, and self-gratification—often exhibiting characteristics of affordable luxury consumption, with substantial market potential.

VCBeat:What major events occurred or what honors did Chengshu Investment receive in 2022?

Lou Min:We have deliberately avoided participating in external award evaluations. One achievement we take particular pride in is the successful exit and distribution of certain projects within a fund during the Shanghai lockdown in March this year. Our limited partners (LPs), confined to their homes, were delighted to receive actual cash distributions of principal and returns. This outcome has brought us great satisfaction.

VCBeat:Which projects has Chengshu Investment invested in this year?

Lou Min:We made an exclusive investment in a new project and increased our holdings several times in existing projects. Chengshu Investment hopes to accompany the growth of outstanding enterprises and entrepreneurs for the long term, continuously increasing its investment to become a co-creator of long-term sustainable value.

VCBeat:Which niche sectors has Chengshu Investment recently focused on, and how did it identify these sectors?

Lou Min:Life sciences and consumer healthcare are our primary battlegrounds. I am personally tracking developments in CGT (cell and gene therapy) and nucleic acid drugs, among related areas. However, when it comes to investment, it may still be too early, or rather, our preparations are not yet sufficiently robust; we need to continue strengthening our research in this area.

VCBeat:Given the highly complex environment currently facing the life sciences and consumer healthcare sectors both in China and globally, compounded by the disruptions caused by the pandemic, what adjustments has Chengshu made to its investment philosophy or strategy?

Lou Min:We have not made any major adjustments in this regard. Our overall strategy is bottom-up, meaning we place greater emphasis on the conditions of specific niche sectors, the particular development stage and fundamental status of individual companies, and the underlying fundamentals themselves. This focus on intrinsic conditions forms the core logic of our investment approach.

What has shifted slightly is that, at this stage, we place greater emphasis on companies with global operational and market capabilities—those that can not only operate in the Chinese market but also deliver their products and services worldwide.

VCBeat:There are also many investment firms in the industry that focus on life sciences and consumer healthcare. What differentiates Chengshu Investment from other VC firms?

Lou Min:Differences in philosophy are more prevalent. Chengshu may differ from the majority in three aspects.

First, we adhere to the investment strategy of “less is more.” We do not pursue a high volume of projects, nor do we excessively seek large individual investment sizes or an expanded fund size under our management. Instead, we aim to deepen our engagement with a relatively limited number of investees, accompany them over the long term, and capture returns from their sustained growth through multiple rounds of increased holdings.

Second, we adopt a concentrated investment approach with significant capital allocation. Chengshu Investment pursues investment returns based on in-depth research, long-term tracking, and the conviction to make repeated bets, rather than focusing on the quantity or scale of investments. We maintain substantial positions in select assets deemed highly core, often exceeding the concentration levels typical of most institutional investors. To date, we have consistently adhered to this strategy without any failures.

Third, adopt an end-in-mind approach and prioritize exit strategies. Before making an investment, we anticipate the endgame, such as determining the appropriate stage and method for exit. Moreover, Chengshu’s core team has weathered over 30 years of fluctuations in the capital markets. We leverage our extensive experience and rigorous post-investment management processes to ensure timely risk identification and capture of exit opportunities.

VCBeat:The concepts of “less is more” and “moderately concentrated investment” that you mentioned differ somewhat from our understanding of venture capital. It is widely acknowledged that venture capital is largely a numbers game, where a larger portfolio tends to yield a higher hit rate. Chengshu Capital maintains a relatively concentrated portfolio, which inherently entails greater risk. How, then, does Chengshu Capital enhance its precision and success rate?

Lou Min:“Venture capital” is actually a misinterpreted term. As an imported concept, venture capital is more accurately translated as “entrepreneurial investment,” which involves providing capital to help startups succeed. Startups are not necessarily synonymous with high-risk enterprises, and venture capital is not equivalent to playing the odds.

We do not endorse the logic of “venture capture,” which posits that making more investments is necessary to diversify risk. As I have just stated, if your investment judgments are accurate, there is no need to improve hit rates through diversified investing. The more dispersed the investments, the more diluted the investor’s attention becomes, leading to reduced focus and concentration, which ultimately amplifies rather than mitigates risk.

Returning to your question about whether concentrated investment increases risk, we believe it does not.

The projects we invest in are all identified through industry-specific patterns and a bottom-up approach. We maintain a highly focused strategy, building unique resource networks and insights within niche sectors. This significantly enhances our ability to secure high-quality deal flow while mitigating risk. When making investment decisions, we always anticipate the worst-case scenario; we proceed only if all potential risks are deemed manageable.

Moreover, our initial investment is typically not substantial. Of course, if we lack confidence in our ability to mitigate risks, we may choose not to invest and adopt a wait-and-see approach. In fact, the decision not to invest is more common for us.

After making the initial investment, as we observed the company growing on schedule—even exceeding expectations—and as our understanding of this niche sector and its product-service direction deepened, along with a more comprehensive appreciation of the team, we found ourselves with ample time and sufficient composure to determine the appropriate level of investment in the next or subsequent funding rounds. Apart from the founders, we may well be the party with the deepest insight into the company. In such circumstances, we are more confident and better positioned to make significant, concentrated investments.

VCBeat:How did Chengshu Investment successfully back star projects such as Zhengya Dental, Future Vision, and Baiying Biologics? Could you share your specific experience in selecting investment targets?

Lou Min:It’s not so much about experience, nor is it overly complex; we secure projects through systematic research and comprehensive coverage of niche industries.

We have specific criteria for selection. First, the companies must rank among the top three in their respective niche markets. Second, they are required to validate their business models and product offerings. Finally, we apply relatively stringent criteria to founders and their teams—what we internally refer to as our “NO” criteria, which enumerate disqualifying factors one by one. Only if a team avoids all such disqualifying factors can it enter our selection framework.

VCBeat:Have you ever invested in projects that were initially viewed with skepticism? How did you approach your thinking process during that time?

Lou Min:Not really. In fact, there are numerous cases where we initially held high expectations, only to discover after a period of follow-up that our initial assessments were inaccurate. This is quite common. Therefore, it is rather interesting. Perhaps our ability to say “no,” encompassing a comprehensive state of intuition, remains fairly accurate.

However, this “yes” is not so easily uttered, as it is subject to constant scrutiny. In the end, many “yes” responses cannot withstand such challenges, whereas saying “no” is generally easier. Of course, our “no” may sometimes be mistaken, but we will not regret it for that reason.

I believe that no matter how successful an investor or investment firm may be, it is impossible for them to fully grasp every investment opportunity around them. No investment group is perfect; we are all ordinary people, or rather, a gathering of ordinary individuals, so it is inevitable that not every decision will be correct. However, I feel that as long as we can reduce the probability of making mistakes, we have already achieved more than half of success.

VCBeat:Over the years, has there been any project you missed that still makes your heart ache and leaves you slapping your thigh in regret whenever you think of it?

Lou Min:No. Although we missed out on many opportunities, what’s done is done, and there is little to regret. At the time, our understanding of the industry and our grasp of the companies involved may not have been sufficient. From another perspective, not making that decision was not necessarily wrong, as we had not yet developed a comprehensive intuition.

We can only attribute it to our insufficient expertise and inadequate judgment at the time. However, certain decisions cannot be made correctly solely based on sufficient expertise or thorough grasp; sometimes, chance also plays a role, making things hard to predict. But as I always say, even the smartest investment firms will inevitably miss many so-called good companies and promising deals. There is no need for regret; this is normal—perfectly normal.

VCBeat:There are countless niche sectors and projects in the consumer healthcare and life sciences fields, such as aesthetic medicine.The portfolio includes medical lasers, injectable products, pharmaceuticals, massage devices, and more. How has Chengshu Investment precisely identified its key areas of focus amidst an increasingly crowded and dazzling competitive landscape?

Lou Min:In fact, we have been reflecting on this issue, but there is no clear answer yet. Why? Take the medical aesthetics sector as an example: professionals in my age group must learn alongside younger generations, as our perceptions and experiences are inevitably less accurate and aligned with current trends than theirs. Therefore, we need to continuously gauge market response and understand young people’s attitudes toward these offerings.

Until we gain a clear understanding of these directions, we must engage in continuous learning, constantly updating information and integrating resources from various channels. It is imperative to achieve thorough comprehension and conduct rigorous research. If a task exceeds our capabilities, we must decline it. We should only proceed with updates when they are within our capacity. However, in certain fields, such as life sciences, our insights have become more focused and direct.

In fact, most new investment opportunities in China involve identifying products and technologies that are already mature abroad but have not yet been commercialized in the Chinese market. If domestic companies are already making efforts in this area, we should engage and collaborate with them at an early stage.

VCBeat:Looking back, how has Chengshu Investment’s strategy changed from its initial establishment to the present stage, and what principles has it consistently upheld?

Lou Min:The fundamental change is that we are now more focused, with a clearer understanding of what lies within our capabilities and control, and what remains beyond our grasp or currently unattainable.

What remains unchanged is our core investment philosophy and values. First, we manage the capital entrusted to us by investors as if it were our own money—a principle we have consistently upheld over the years. Second, we treat every member of our team as a partner.

VCBeat:In the post-pandemic era, which niche segments within the life sciences and consumer healthcare sectors do you consider most promising?

Lou Min:In the consumer healthcare sector, what we are currently very interested in is commonly referred to as “medical aesthetics.” However, I believe the term “anti-aging” is more appropriate. All so-called medical aesthetic procedures are essentially about “anti-aging”—slowing down the aging process of the human body. This direction is particularly intriguing.

Next, there are factors related to an individual’s physical and mental well-being, such as pet ownership. We have made initial forays into this area, but given that we are not yet entirely confident in its viability, we have proceeded with caution. We continue to monitor the space closely, aiming to build a more solid foundation before taking substantial action.

The life sciences sector is more complex. We believe that, at least in the near term, the industry will likely need to endure volatility driven by industrial or capital cycles. From a commercial perspective, we place greater emphasis on opportunities in the upstream segment of the life sciences industry, as these areas are better positioned to withstand current cyclical shocks.

VCBeat:What Is the Current Financing Environment, and What Recommendations Are There for Entrepreneurs Adjusting Their Fundraising Strategies?

Lou Min:For companies with confidence and solid fundamentals, Chengshu Investment is currently helping them build a more robust and secure capital structure from multiple angles, such as combining equity financing with a reasonable debt financing structure.

From a policy perspective, the state also encourages and supports these directions; enterprises should still utilize diverse financing instruments to address their development challenges.

"Stockpiling more bullets and saving food for the winter are both reasonable strategies, but there’s no need to take them to extremes. Personally, I remain relatively optimistic."