How Can Huiminbao, the Nationally Popular Health Insurance Covering Hundreds of Millions, Achieve Long-Term Sustainability?

MediTrust Health

Innovative Inclusive Health Medical Service and Security Platform

"Huiminbao," which has remained wildly popular for three years, continues to sweep across China.

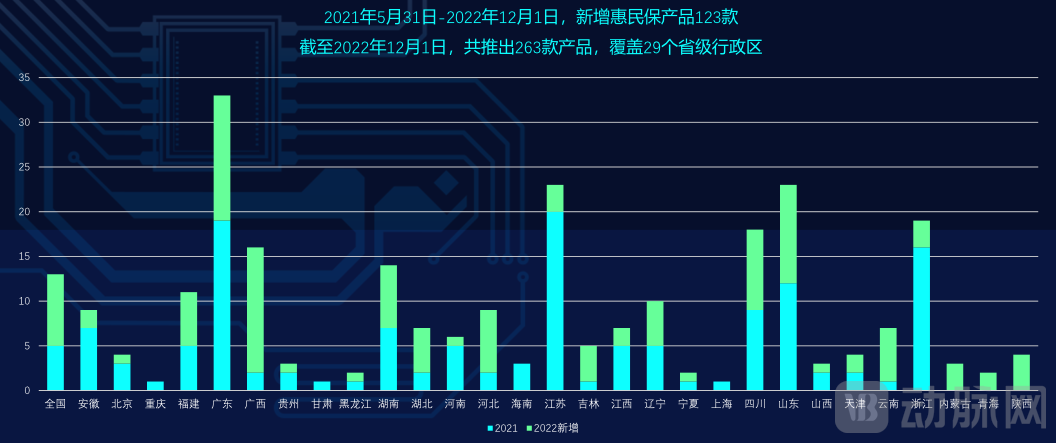

On December 14, the Insurance Innovation and Investment Research Center of the Fanhai International School of Finance at Fudan University released the “2022 Knowledge Graph of City-Specific Commercial Medical Insurance (Huimin Bao)” (hereinafter referred to as the “Knowledge Graph”). This “Knowledge Graph” dataData shows that as of December 1, 2022, 263 Huiminbao products had been launched, covering 29 provincial-level administrative regions.

Among them, Inner Mongolia, Qinghai, and Shaanxi have achieved a breakthrough from zero in the adoption of Huiminbao insurance.

(Latest Developments in Huiminbao Insurance; Source: Knowledge Graph)

(Latest Developments in Huiminbao Insurance; Source: Knowledge Graph)

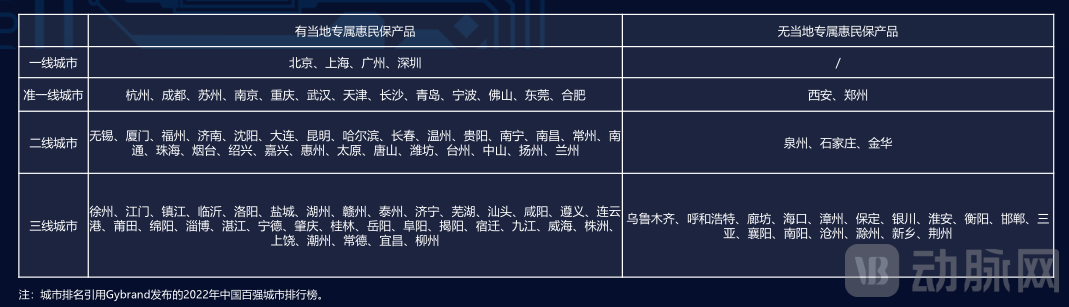

Moreover, having originated in the developed coastal cities of eastern China, Huiminbao (inclusive supplementary medical insurance) has gradually expanded to central and western regions as well as second- and third-tier cities. Localized Huiminbao products are now available in numerous second- and third-tier cities, including Wuxi, Xiamen, Fuzhou, Jinan, Shenyang, Yichang, Liuzhou, Zunyi, and Mianyang.

With such extensive geographic coverage, the number of insured individuals has also risen rapidly.According to data from the Insurance Association of China, the number of enrollments in Huiminbao (city-specific supplementary medical insurance) had already reached 140 million by the end of 2021, and this figure is expected to rise significantly in 2022.

Beyond user base expansion, Huiminbao (city-specific supplemental medical insurance) is also reshaping the entire healthcare industry, attracting numerous health insurance technology platforms and pharmaceutical companies to participate. Furthermore, leveraging its extensive coverage, Huiminbao holds unparalleled advantages in both data accumulation and customer acquisition channel reach.

But at the same time,Huiminbao Still Faces Severe Challenges.For instance, there is significant variation in insurance participation rates across cities, with the highest exceeding 80% while some regions report rates below 5%. Regarding renewal rates, VCBeat has learned that certain star products launched in 2022 have shown a continuing decline in the number of policyholders renewing their coverage.

We cannot help but ask: After three years of rapid expansion, sweeping up hundreds of millions of participants, how can Huimin Bao (city-specific supplemental medical insurance) maintain long-term, sustainable development?

From the perspective of facilitating common prosperity and enhancing the social safety net for low-income populations, inclusive insurance is receiving increasing policy attention.

What is inclusive insurance? On December 10, the China Banking and Insurance Regulatory Commission (CBIRC) released the “Guiding Opinions on Promoting the High-Quality Development of Inclusive Insurance (Draft for Comment),” which proposed that inclusive insurance encompasses two forms of coverage: insurance with an inclusive nature and exclusive inclusive insurance. Among them,Inclusive insurance primarily includes critical illness insurance, long-term care insurance, tax-advantaged health insurance, and agricultural insurance, as well as the currently popular Huiminbao.

“Huiminbao” is not a new phenomenon. Its development has spanned seven years, originating with the Shenzhen Critical Illness Insurance in 2015, experiencing explosive growth in 2020, and continuing to deepen its reach in 2022.

From the perspective of evolutionary trends, Huiminbao exhibits significant characteristics of “gradual market penetration into lower-tier markets and rapid product launches.”According to data from the Knowledge Graph, 123 new Huiminbao (city-specific supplementary medical insurance) products were launched in the market between May 31, 2021, and December 1, 2022. As of December 1, 2022, a total of 263 products had been introduced, covering 29 provincial-level administrative regions, with presence in first-, second-, and third-tier cities.

(Cities Covered by Huiminbao Insurance; Source: "Knowledge Graph")

(Cities Covered by Huiminbao Insurance; Source: "Knowledge Graph")

Behind the Rapid Market Penetration, Huiminbao Is Showing New Changes.

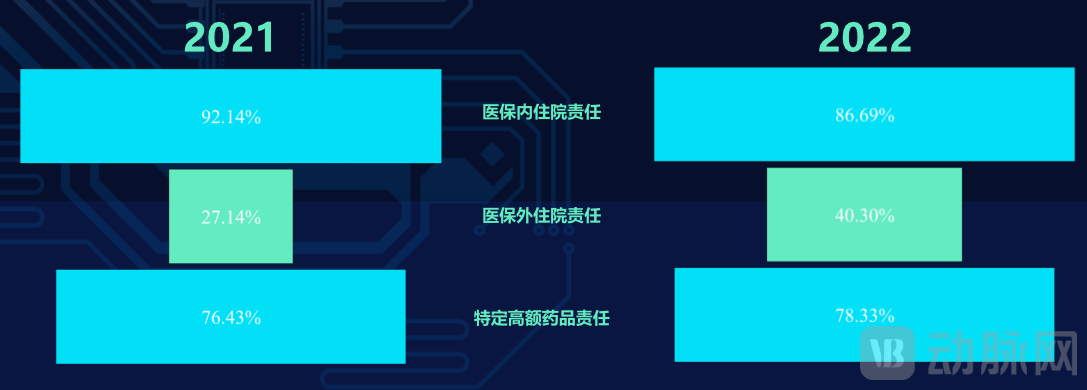

For instance, Huiminbao has continuously iterated and evolved its coverage responsibilities, forming a three-pillar structure comprising in-formulary benefits, out-of-pocket expenses for non-formulary items, and specialized drug coverage. This evolution has not only enhanced the product’s protective capacity but also expanded its reach to attract a broader user base.

“Huiminbao initially targeted primarily healthy individuals. Industry claims data indicate that these plans mainly cover liabilities within the scope of basic medical insurance; however, the reimbursable portion refers to the out-of-pocket expenses remaining after basic medical insurance reimbursement, rather than entirely self-paid costs.” A senior industry observer with long-term expertise in the health insurance sector told VCBeat that as Huiminbao continues to evolve, it has increasingly covered individuals with pre-existing conditions and gradually expanded to include out-of-pocket expenses outside the basic medical insurance scope, as well as specific high-cost drugs, significantly boosting consumers’ willingness to purchase Huiminbao policies.

“Knowledge Graph” survey data corroborates this shift. Currently, the proportion of inpatient coverage for expenses outside basic medical insurance under basic liability has risen significantly, jumping from 27.14% in 2021 to 40.3% in 2022.

(Trends in Non-Covered Responsibilities of Medical Insurance Outside Hospitals Source: "Knowledge Graph")

(Trends in Non-Covered Responsibilities of Medical Insurance Outside Hospitals Source: "Knowledge Graph")

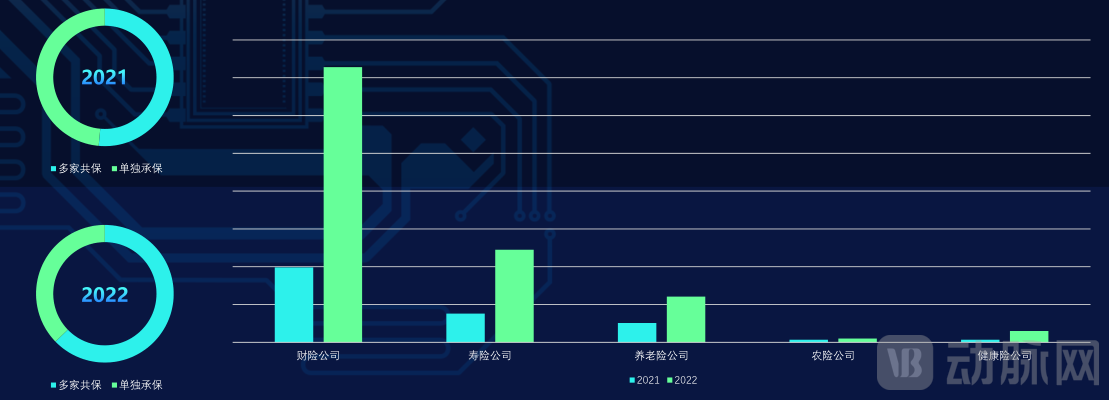

Furthermore,The structure featuring one or two lead underwriters and multiple co-insurers has become the prevailing trend for insurers participating in Huimin Bao.“Knowledge Graph” data shows that the co-insurance ratio among multiple insurers rose from 51% to 62% in 2022, marking a rapid increase. Among them, property and casualty insurance companies continue to maintain an absolute leading advantage.

Taking “Beijing Jinghuibao” as an example, in October this year, it was announced that “Beijing Jinghuibao” would expire and cease sales on November 30, with follow-up services for existing policies still to be provided through its official WeChat account. Meanwhile, Beijing Life Insurance, one of the underwriting insurers for “Beijing Jinghuibao,” will join the co-insurance consortium of “Beijing Puhui Health Insurance.” Beijing has thus officially transitioned from a “multiple insurance plans per city” model to a new stage of “one insurance plan per city.”

Based on market feedback, compared to the initial model of multiple insurers in a single city,The advantages of co-insurance involving multiple insurers lie in: first, enhancing the overall operational stability of Huiminbao projects; and second, fully leveraging the professional expertise of each participating entity, which also helps alleviate, to some extent, the severe homogenization currently seen in Huiminbao products.

(Changes in Multi-Insurer Co-Underwriting and Sole Underwriting of Huiminbao from 2021 to 2022; Source: “Knowledge Graph”)

(Changes in Multi-Insurer Co-Underwriting and Sole Underwriting of Huiminbao from 2021 to 2022; Source: “Knowledge Graph”)

Notably, in line with this trend, the stakeholders of Huiminbao (city-specific supplementary medical insurance) have established a development model featuring joint participation by “government agencies + insurance companies + third-party platform providers.”For example, in the Shanghai “Hu Hui Bao” project, the Shanghai Municipal Healthcare Security Administration serves as the guiding authority, the co-insurance consortium provides system operation support for the entire project, and MediTrust Health, as a third-party company, delivers specialty drug services for Hu Hui Bao.

In addition to coordinating and complementing resources, the multi-stakeholder collaboration model leverages the medical services and technological capabilities of third-party companies to facilitate information and experience sharing among co-insurance consortia, thereby delivering greater added value to users.

In the 2022 edition of “Hu Hui Bao,” the third-party company MediTrust Health not only expanded the number of covered specialty drugs for claims to 25, but also further improved the accessibility of new specialty drugs, including added coverage for CAR-T therapy and 15 overseas specialty drugs.

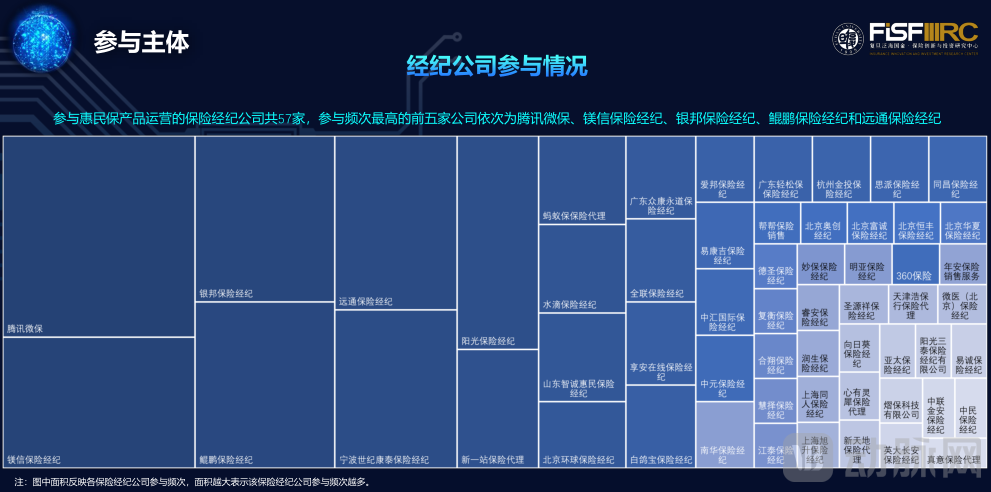

(57 insurance brokerage firms, including Tencent WeSure and MediTrust Insurance Brokers, participate in the operation of Huiminbao. Image source: "Knowledge Graph")

(57 insurance brokerage firms, including Tencent WeSure and MediTrust Insurance Brokers, participate in the operation of Huiminbao. Image source: "Knowledge Graph")

Additionally, VCBeat has observed thatSince 2022, the government has significantly strengthened its guidance over Huiminbao.Notably, local healthcare security administrations are actively standardizing and guiding Huiminbao-related products, thereby strengthening government involvement—a significant departure from the situation in 2020 and 2021. Among these efforts, departments responsible for agriculture and rural affairs as well as rural revitalization have also increased their participation in providing guidance and support for Huiminbao initiatives.

“The higher the level of government involvement, the more positively it can contribute to the standardized development of Huiminbao (city-specific supplemental medical insurance), thereby avoiding excessive market competition,” said a senior expert in the health insurance industry.

In addition, regarding premium rates, there was a slight overall increase for Huimin Bao in 2022, but the majority of products remained concentrated in the RMB 60–100 range.

In summary, as Huiminbao continues to deepen its market penetration, it has undergone significant changes, naturally bringing forth new opportunities: enhanced product competitiveness, a broader user base, more standardized development directions, and a more diverse range of participating entities.

Yet, like two sides of the same coin, as Huimin Bao races ahead, it faces formidable challenges. The Knowledge Graph specifically highlights the difficult issue of “how to break the death spiral” facing Huimin Bao.

What Is the “Death Spiral”? It refers to a scenario in which the proportion of non-standard risks among insured individuals continues to rise, driving up the product’s loss ratio. Meanwhile, only a small number of policyholders under inclusive supplementary medical insurance (Hui Min Bao) products actually receive claims payments, resulting in a significantly low sense of benefit for those who do not receive payouts. Consequently, insurers, unable to bear the mounting claims pressure, are forced to discontinue these products. This not only undermines consumers’ legitimate rights and interests but also erodes public trust in Hui Min Bao and hampers its future sales.

How Should the Story of Huiminbao Be Told Next in the Face of Current Challenges?

As previously mentioned, Huiminbao faces particularly severe challenges in its rapid expansion.

A look at the current market reveals that the “death spiral” of Huiminbao (city-specific supplemental medical insurance) in some cities has begun to emerge. For instance, certain cities have gradually started raising coverage limits due to insufficient pool sizes. In other cities, losses have led insurers to withdraw from Huiminbao operations one after another. As a result, enrollment rates across cities have become polarized: while some cities boast enrollment rates exceeding 30%, others fall below 1%, with most generally remaining under the 15% threshold.

Therefore,To ensure the long-term sustainable development of Huiminbao, it is crucial to resolve the “death spiral” challenge.

Multiple industry insiders told VCBeat that the key to helping Huiminbao (city-specific supplemental medical insurance) escape its predicament lies in increasing enrollment rates and expanding the premium pool. To this end, some cities have lowered the reimbursement threshold for their Huiminbao plans, stipulating that it must not exceed RMB 15,000, while others have introduced policies providing free insurance policies to impoverished households.

However, these measures can only address the symptoms.In the long run, addressing the root causes requires further deepening of health management services.The reason is that only by providing high-frequency, truly valuable, and perceptible health services can insurers enhance policyholders’ sense of gain, reduce lapse rates, and improve renewal rates.

How to Deliver Effective Health Management Services and Coverage? The Industry Has Made Notable Explorations. Taking MediTrust Health as an example, by bridging the insurance and pharmaceutical sectors, it has enhanced medication accessibility for Huiminbao (city-specific supplemental medical insurance) and helped fill health coverage gaps for individuals with pre-existing conditions. To improve patient access to high-cost medications, MediTrust Health has collaborated with relevant enterprises to launch a series of affordable care initiatives, making high-value drugs accessible and affordable to a broader patient population.

For example, to alleviate the financial burden on patients undergoing CAR-T therapy, MediTrust Health has joined forces with multiple insurance companies to establish strategic partnerships with two major domestic pharmaceutical manufacturers of CAR-T therapies. To date, MediTrust Health has incorporated innovative CAR-T therapies into the “Hui Min Bao” (inclusive supplementary medical insurance) programs in 27 cities, cumulatively reducing treatment costs for lymphoma patients by over RMB 10 million, thereby building a dual protection network of “affordable coverage + health services” for a broad patient population.

Taking the newly launched “Su Hui Bao 2023” program as an example, MediTrust Health has expanded the list of specific high-cost self-pay drugs and medical devices to 38 items, established a dedicated local biopharmaceutical database for Suzhou, and increased the maximum reimbursement ratio to 90%.

In addition, “Su Hui Bao 2023” has added coverage for 75 overseas-specific drugs, while continuing to provide benefits for hospitalization allowances for severe malignant tumors, proton and heavy ion medical insurance, and CAR-T therapy insurance, further meeting the pharmaceutical protection needs of local residents.

Currently, MediTrust Health has provided professional product design, pharmaceutical services, and technical support for multiple products such as "Su Huibao," "Xihu Yilianbao," "Huiqubao," "Hu Huhubao," and "Beijing Puhui Jiankang Bao." Its services have covered more than 100 cities across China, including Beijing, Shanghai, Hangzhou, and Suzhou, accumulating nearly 100 million service instances and delivering tangible benefits to the public. In the development of city-specific supplementary medical insurance (Huiminbao), MediTrust Health’s role has continuously transformed and upgraded from a specialized drug service provider to a comprehensive service operator.

Certainly,As an innovative model for the integrated development of commercial health insurance and social security, how Huiminbao paves the way for medical insurance reform and achieves greater social value constitutes its intrinsic driving force for sustainable development.

In new initiatives, Huiminbao has been actively exploring the aforementioned directions. For instance, survey data from *Knowledge Graph* shows that seven drugs included in the 2021 version of Shanghai’s Huhuibao special drug list were also covered by the National Basic Medical Insurance Drug Catalog, thereby serving as a pioneering pilot to promote the reform and development of basic medical insurance.

(Inclusion of Special Drugs in Shanghai Huhuibao into the National Basic Medical Insurance Drug Catalog (Source: "Knowledge Graph"))

(Inclusion of Special Drugs in Shanghai Huhuibao into the National Basic Medical Insurance Drug Catalog (Source: "Knowledge Graph"))

Another trend is that the purchase methods for Huiminbao products have gradually shifted from being limited to individual purchases to allowing deductions from and payments via personal medical insurance accounts. Additionally, individuals are encouraged to purchase coverage for family members, electronic medical record channels for claims have been opened, and payout information from basic medical insurance and critical illness insurance has been integrated to promote one-stop claims settlement. These developments have played a positive role in accelerating the integration of the multi-tiered medical security system.

In terms of delivering greater social value, several Huiminbao (city-specific supplemental medical insurance) schemes have successively expanded their coverage to include “new citizens” this year. For instance, the 2022 edition of Guangzhou’s “Sui Sui Kang” covers individuals who have held a Guangzhou residence permit for at least two years, as well as those recognized in Guangzhou for acts of courage and justice. Similarly, the 2022 edition of Shanghai’s “Hu Hui Bao” targets industries such as logistics distribution and food delivery/courier services that made outstanding contributions during the pandemic response, incorporating “new citizens” into its coverage on the principle of “enterprise-level coordination and individual voluntary participation.”

Additionally,Expanding coverage from healthy individuals to substandard risks and those with pre-existing conditions, thereby encompassing a broader population of patients, is also a key manifestation of the social security value of Huiminbao.Taking “Hui Min Bao,” in which MediTrust Health participates, as an example, it not only covers various out-of-pocket expenses such as inpatient treatment costs both within and outside the national medical insurance catalog, as well as outpatient fees for special diseases, but also includes 30 types of specific high-cost drugs covering lung cancer, leukemia, breast cancer, gastric cancer, and other prevalent and rare diseases.

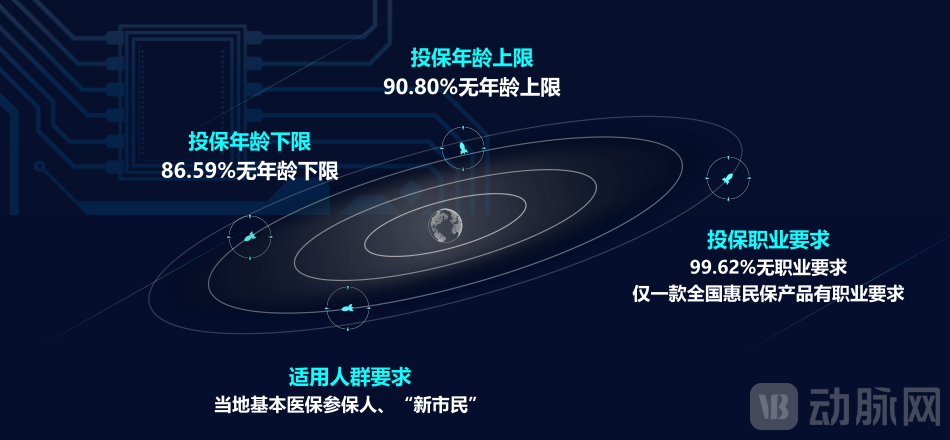

(Basic Requirements for Insuring in Huiminbao at Present. Image Source: "Knowledge Graph")

(Basic Requirements for Insuring in Huiminbao at Present. Image Source: "Knowledge Graph")

It is not difficult to see that, in breaking the “death spiral” dilemma and achieving long-term sustainable development,In 2022, Huiminbao (city-specific supplemental medical insurance) conducted more in-depth explorations, moving beyond traditional risk-loss compensation. It made beneficial attempts to deepen health management services, pave the way for medical insurance reform, and realize greater social value, thereby better serving the public interest.

However, innovation knows no bounds, and Huiminbao is still in a phase of rapid development. Therefore, all stakeholders must continue to actively explore new avenues to unlock greater potential for Huiminbao.

As the aging of the population accelerates, a gap persists between China’s existing basic medical security system and commercial health insurance, making it difficult for low-income and elderly populations to mitigate health risks through individual means.

As a form of supplementary medical insurance, Huiminbao will serve as a bridge between basic medical insurance and commercial health insurance, driving the development of health insurance to a new level.

It is important to note that although the health insurance sector has experienced rapid growth in recent years—with premium income reaching RMB 880.36 billion in 2021, making it one of the most sought-after insurance categories alongside life and auto insurance—its claim payouts amounted to just over RMB 400 billion. This figure accounts for less than 6% of the total national health expenditure, which exceeded RMB 7.5 trillion for the year, indicating a limited role in providing supplementary coverage. Huimin Bao (city-specific supplemental medical insurance) has undoubtedly opened up new prospects for the broader adoption of health insurance.

On the other hand,The pioneering risk-sharing coinsurance model of Huiminbao has set a precedent for the insurance industry to underwrite policies through collective industry efforts., this will bring more practical applications of innovative products for subsequent industry co-insurance pools in the promotion of health insurance, such as volume-based procurement of commercial insurance formularies.

Moreover, the evolutionary logic of Huiminbao reveals that the industrial integration of healthcare and insurance has also become a trend in industry development.In the future, an increasing number of insurance companies will partner with third-party enterprises to deliver pharmaceutical services and health management, expanding value-added services related to critical illnesses and chronic diseases. This strategy aims to achieve multidimensional development across insurance coverage, medical services, and health services, thereby comprehensively addressing residents’ challenges in health management and accessing medical care. International experience, such as the practices of UnitedHealth Group and Kaiser Permanente, has demonstrated the feasibility of this approach.

It can thus be seen that,Amid continuous iteration and innovation, the health insurance industry has brought more value growth points to social medical services and coverage.

In October 2022, the Report to the 20th National Congress of the Communist Party of China specifically pointed out thatAdvancing the Healthy China Initiative by prioritizing the protection of people’s health as a strategic priority, we must improve the social security system. This entails establishing a multi-tiered social security system that covers all citizens, integrates urban and rural areas, ensures fairness and uniformity, adheres to safety and regulatory standards, and remains sustainable, while expanding the coverage of social insurance.

Undoubtedly, commercial health insurance, represented by the inclusive “Huimin Bao” (city-specific supplemental medical insurance), has become a crucial component of the multi-tiered medical security system. This not only aligns with the health service objectives outlined in “Healthy China 2030,” but also serves as an indispensable element in achieving “common prosperity in health.”

Therefore, as each small step in the development of the health insurance industry gradually converges, it will provide impetus for a major leap forward in the construction of China’s multi-tiered medical security system.

Although this path is fraught with challenges, concerted efforts across the industry will surely pave the way forward.