Nature Biotech Study of 498 University-Linked Startups Reveals Acquisition Yields Far Higher Returns Than IPO

“Integration of Industry, Academia, and Research” and “Translation of Scientific Research” were high-frequency keywords in China’s biopharmaceutical industry in 2022, as an increasing number of Biotech companies have technologies originating from academic research at universities or are actively seeking licenses for university-based scientific achievements.

Among the startups recently reported by VCBeat, excellent examples of this type include Aiweide, an organ-on-a-chip company incubated by Southeast University; Huakan Bio, founded under the leadership of Professor Du Yanan from the School of Medicine at Tsinghua University; and Huida Gene, established by Professor Yang Hui from the Shanghai Institute of Neuroscience, Chinese Academy of Sciences.

"In today's industrial environment that emphasizes source innovation, this type of Biotech often quickly feels the enthusiasm of the capital market,"Investors are all pouring money into biotech startups founded by scientists, but whether these ventures will succeed remains anyone’s guess."An investor told VCBeat New Medicine."

What are the key factors influencing success for these biotech companies? For most investment firms already in the market, what is the return on investment?These are all issues of significant concern to China's biopharmaceutical industry at present.

In fact, due to the differing development timelines and driving forces behind the Chinese and U.S. biopharmaceutical industries, most U.S. biotech companies are built upon patent licenses transferred from universities. Therefore, by reviewing the development trajectories of these biotech firms and examining their fate in the U.S. market, we hope to provide insights that can inspire the growth of China’s domestic industry.

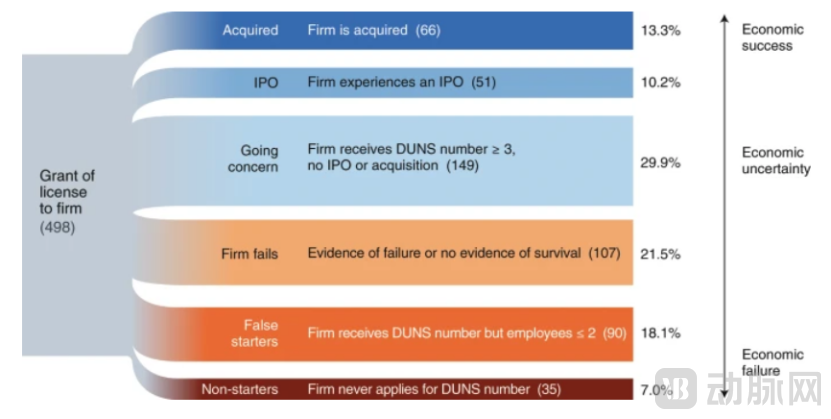

An industry study published in a Nature subsidiary journal conducted a census of university-licensed startups (ULS) founded between 1980 and 2013 by the 50 U.S. universities that generated the most patents from 1969 to 2008, providing highly reference-worthy answers to the aforementioned questions—among the 498 startups,10.2% of companies ultimately went public via IPO, 13.3% were acquired, and fewer than 30% of other biotech firms showed any signs of ongoing business activity.

Figure 1. Survival of ULS Company Samples

For investors, 41Only 12 IPO companies have achieved profitability, with an average time to profitability of 2.3 years. For investors, the return on investment from biotech acquisitions is significantly higher than that from IPOs.

The study also analyzed key factors influencing the success rate of biotech companies and warned against the rise of “non-substantive entrepreneurship.”

Site Selection in Industrial Clusters Doubles Success Rate

Since technology and talent are often anchored in universities, ULS companies face a strategic choice when selecting locations: Should they choose the university hubs where technology and talent reside, or opt for regions with concentrated industrial ecosystems?

For example, Huakan Biotech, founded under the leadership of Professor Du Yanan from the School of Medicine at Tsinghua University and established with the support of the school, faced a choice: should it be located in Beijing, or in the Yangtze River Delta region, where most cell and gene therapy companies are clustered? Huakan Biotech ultimately chose Beijing as its location.

In the early stages of the startup boom or during periods of active capital markets, site selection does not appear to be a critical factor for corporate success.

But now, entrepreneurs’ mindsets are beginning to shift. They seek locations that can enhance their startups’ survival odds during the capital cooldown period, thus exercising greater caution in site selection. Some entrepreneurs believe that isolated companies struggle to withstand risks, whereas firms embedded within industrial clusters are more likely to receive support.

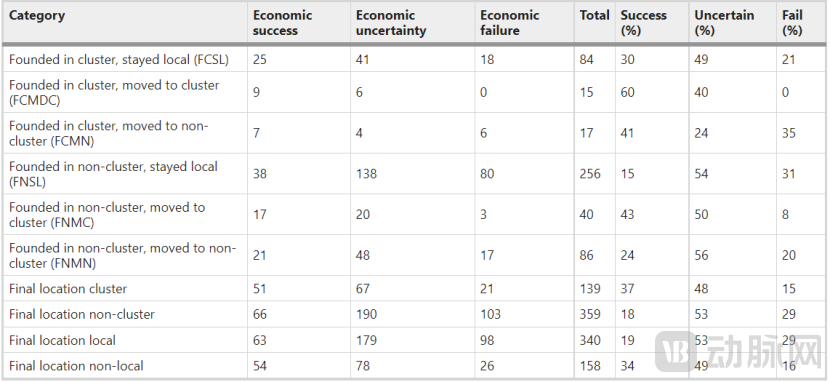

This view has essentially become an industry consensus. The aforementioned report examined the relationship between ULS migration, targeting, and success rates, showing thatCompanies located within clusters are twice as likely to succeed and fail as those located elsewhere.FrequencyRateis half that of enterprises located elsewhere.

Table 1 Relationship between Migration, Site Selection, and Success Rate of ULS

Research has found that regardless of where a startup is founded, its ultimate success hinges on the ability to secure follow-on resources. Clustered enterprises hold a distinct advantage in this regard. The benefit of being located within an economic cluster lies in the physical proximity between firms and other entities in the ecosystem. This closeness facilitates deep and rich communication and interaction, helping to resolve technical challenges and strengthen business activities.

Surprisingly, the success rate of companies founded in clusters and subsequently relocating to non-cluster areas was 41%.This data is difficult to explain solely by “cluster advantages”: Why did these companies relocate? Why did they abandon the resource agglomeration provided by the cluster?

The study further summarizes the concept of “selective matching,” meaning that success is often accompanied by relocation to the best-matched region.

What is “fit”? It essentially refers to a high degree of fit when an incoming company precisely fills a resource gap in a region, thereby increasing the likelihood of its success. An analysis of companies that were founded within clusters and subsequently relocated to non-cluster areas shows that these firms improve their chances of achieving optimal fit by actively seeking resources that meet their specific needs. Meanwhile, ULS companies that proactively relocate demonstrate higher success rates than those that remain in their founding locations.

Some enterprises have realized that site selection requires not only “industrial density” but also “resource alignment.”VCBeat recently interviewed a CXO company specializing in a niche sector. The company chose to relocate to Zhangjiang, Shanghai, where land is at a premium, to leverage the proximity to the Chinese Academy of Sciences and tap into a large base of established corporate clients. Meanwhile, an upstream organoid company opted to join an accelerator at Suzhou BioBAY, as the park has seen the emergence of more emerging biotech firms in the organoid space compared to Zhangjiang.

For companies, site selection does not necessarily need to be near their founding universities or major life science clusters; success is more readily achieved when locations are chosen based on proximity to the resources they require. For government industrial parks across various regions, attracting enterprises should similarly prioritize resource alignment. They can even develop resources and attract related companies around specific sectors, thereby emerging as leaders in those fields.

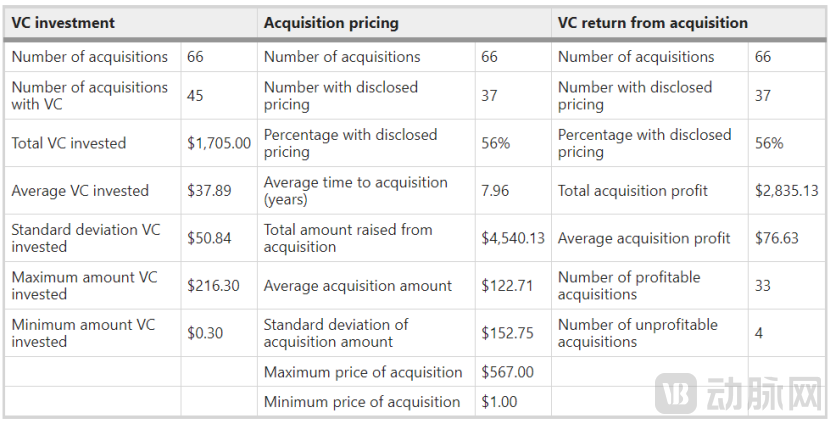

For investors, the return on acquisition is significantly higher than that of an IPO.

Behind enterprises incubated by universities, there are often scientist-entrepreneurs who tend to hold a more conservative attitude toward acquisitions. In reality, however, being acquired can generate far greater returns for investors than an initial public offering (IPO).

According to statistics, the number of transfer/acquisition events involving global biopharmaceutical companies doubled in 2022. The mindset of domestic Biotech founders is also shifting: in mature pharmaceutical markets such as Europe and the United States, the ultimate fate of most Biotech firms is acquisition by large pharmaceutical companies. This exit pathway is, in fact, just the tip of the iceberg of industrial division of labor and collaborative models, and it represents an inevitable trend toward market maturity. Consequently, this has become the predetermined development trajectory for the majority of Biotech companies from their inception.

However, it remains difficult to estimate the differences in returns between acquisition and IPO as exit strategies for investors. The report also points out that although overall investment returns are not particularly high, returns from acquisitions are significantly higher than those from IPOs.

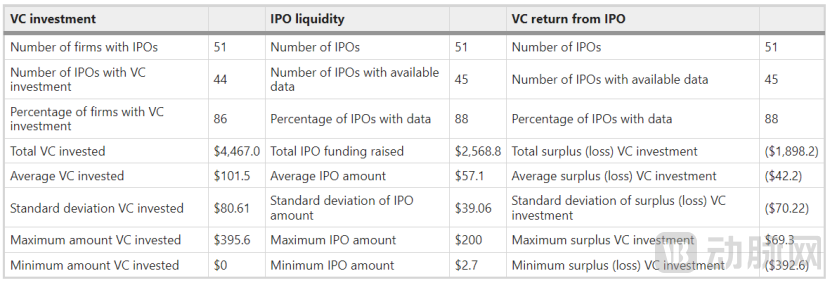

Companies seeking IPOs have consumed substantial amounts of venture capital, yet on average—and in most cases—have failed to deliver positive returns to investors. The total funds raised through IPOs were $2.57 billion less than the venture capital invested, resulting in an average funding shortfall of $42 million per company. Upon closer examination, researchers found that IPOs often serve merely as another round of financing, placing tradable equity on the balance sheet and paving the way for debt financing. In fact, among a sample of 41 IPO companies, only 12 achieved profitability, with an average duration of profitability of just 2.3 years. In contrast, acquisitions have generated profits for investors; deals with known prices (accounting for 60% of the total) yielded an average return of $76.6 million for investors.

Table 2 Returns to Venture Capital Investors from Acquisitions of ULS Companies (in millions of USD)

Table 2 Returns to Venture Capital Investors from Acquisitions of ULS Companies (in millions of USD)

Table 3 Returns to Venture Capital Investors from ULS’s IPO (in millions of USD)

Table 3 Returns to Venture Capital Investors from ULS’s IPO (in millions of USD)

Transformation Must Be Sustainable; Beware of “Non-Substantive Entrepreneurship” Growth

The Prosperity of America’s Innovation and Entrepreneurship Culture Is Linked to Four Factors: Researcher Freedom, Industrial Institutional Support, Mutual Mobility Between Academia and Industry, and Government Support in Key Areas.

Prosperity has sparked enthusiasm and expectations among academia, industry, and research institutions to participate in the commercialization of scientific achievements; however, merely completing company registration cannot serve as the ultimate value endpoint for innovation translation.

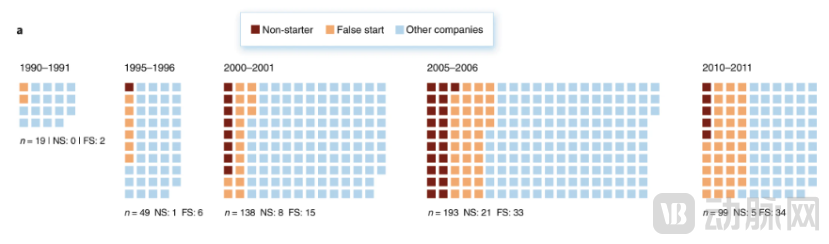

The aforementioned studies define companies with two or fewer employees as “False Starters” and enterprises with no business activities (such as employee records or transaction data) as “Non-starters.” Data on the growth in the number of such entities reveal that the proportion of “non-substantive entrepreneurs” is also rising in phases.

Figure 2 Growth of “Non-Substantive Entrepreneurs”

In 2008, the Technology Transfer Office (TTO) of the University of Utah established 20 new start-ups, a number comparable to that of the Massachusetts Institute of Technology (MIT). Subsequently, as disclosed by the local newspaper The Salt Lake Tribune, most of these 20 start-ups listed the university’s TTO as their corporate headquarters, with the TTO’s director serving as the registered agent or corporate officer. Other researchers have found that more than half of these companies were classified as “non-substantive entrepreneurs.”

The enthusiasm for translating academic research into practical applications at universities needs to be unleashed, the difficulties need to be alleviated, and the mechanisms need to be continuously explored. At the same time, more industrial talent and resources must be allocated, along with effective communication and interaction between academia and business circles. Only in this way can research achievements truly step out of universities, not stopping at the initial stage of "establishing a company," but enhancing the sustainability of entrepreneurship and promoting the growth of more substantive innovation and entrepreneurial value.

Reference Article

1.Godfrey, P.C., Allen, G.N. & Benson, D. The biotech living and the walking dead. Nat Biotechnol 38, 132–141 (2020). https://doi.org/10.1038/s41587-019-0399-1