Cell Therapy, Regenerative Biomaterials, and Tissue Engineering Emerge as High-Potential Sectors Amid Accelerated Commercialization and Technological Substitution

Preface

Immortality is one of humanity's timeless pursuits.

From the alchemical pursuit of elixirs of immortality during the reign of Qin Shi Huang to modern technologies that extend human lifespan through various means.In the field of medicine extending human lifespan, it can be divided into three stages:

In the first phase, the chemical industry extended human life by approximately 20 to 30 years. In the second phase, biological agents further extended lifespan by 10 to 20 years. In the third phase, technologies in cell biology, materials science, genetics, and tissue engineering will extend human life by another 10 to 20 years; this constitutes the era of regenerative medicine.

Unlike the traditional logic of using drugs and devices to treat damaged tissues,, regenerative medicine is the holistic and systematic replacement of damaged human tissues。

This article is an excerpt from the “2022 Regenerative Medicine Industry Report.” To obtain the full report, please scan the QR code to add our assistant. If you have already added the assistant, please proactively reach out for assistance.

# Core Viewpoints

New products based on novel cell engineering platforms, such as chemically induced cells and adult stem cells, will continue to emerge.

Material Modification and In-Depth Collaborative Development of Regenerative Materials by Different Medical Application Fields Will Become a Trend

Specific Commercialization Pathways in Tissue Engineering to Gradually Become Clearer Over the Next Three Years

Over the next decade, commercialized products for more than 50% of human tissues and simple organoids will emerge.

Traditional medical devices, AI technology, and other niche sectors will gradually extend into and integrate with the regenerative medicine industry.

Regenerative medicine is the use ofTheories and methods from multidisciplinary fields such as life sciences, engineering, and computer science, integrated with multiple modern biotechnologies including materials science, cell technology, tissue engineering, and genetic engineering., to achieveRepair, ReplacementandEnhancementTechnology for damaged, diseased, or defective tissues and organs in the human body.

Through interviews and surveys with experts in China’s regenerative medicine sector, VCBeat Research Institute has identified that the narrow definition of regenerative medicine primarily coversTissue Engineering, Regenerative Materials, and Stem Cells, this report will primarily focus on discussions around the aforementioned three tracks.

Cell Technology: Stem cells are widely used in the medical field, with some pipelines already in clinical trials

In many complex disease areas where conventional medicine has limited options, such as chronic diseases like diabetes, neurological disorders like Parkinson’s syndrome, and the field of tissue and organ regenerative induction, stem cell technology holds vast potential and is alsoOne of the critical foundational technologies in regenerative medicine that cannot be overlooked.

The history of stem cell development spans merely a century, with significant scientific breakthroughs achieved only in recent times. In 1999, Science magazine selected and announced the Top Ten Scientific Advances, with embryonic stem cell research ranking first among them. In the same year, China’s first stem cell invention patent was granted and approved for project initiation, marking the beginning ofof adult stem cells in ChinaThe New Era of the Stem Cell Industry.

Intensifying Competition Among Immune Cells; Stem Cell Sector Sets Sail

In contrast to the fiercely competitive field of immune cells, the stem cell sector is quietly accumulating strength. The gap in research progress between China and other countries is narrower for stem cells than for immune cells. Currently, mesenchymal stem cells (MSCs) are the most extensively studied, with 10 products approved globally. Based on their mechanisms of action and approved indications, MSC products can be categorized into two major classes: tissue repair and immunomodulation.

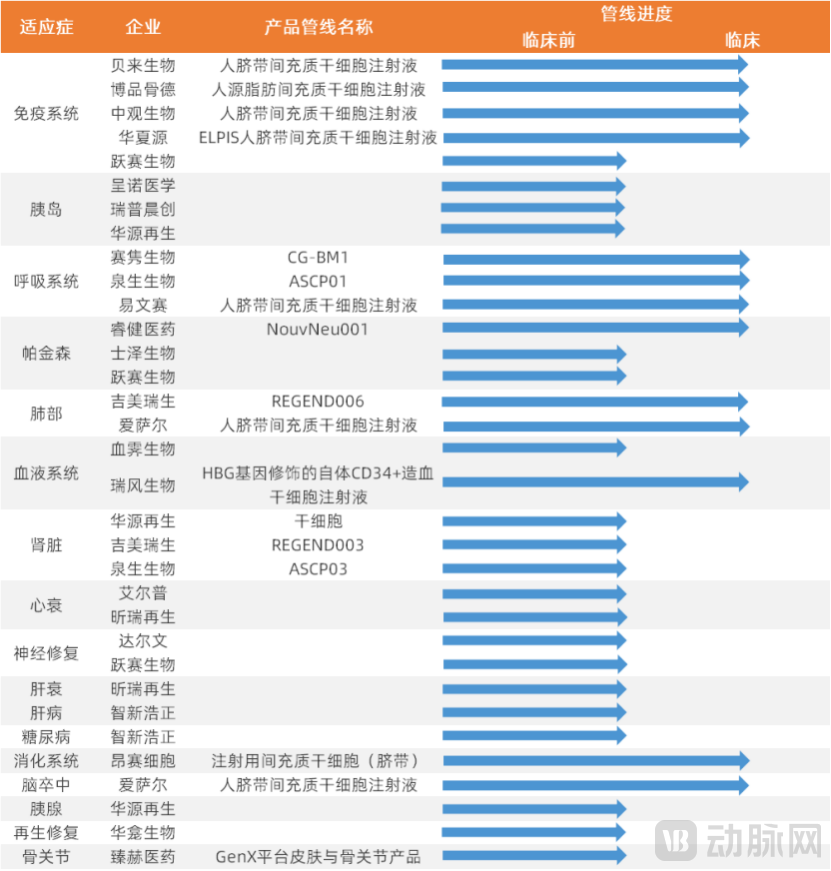

From China's perspective, currentlyThe company's product pipeline in the field of cell technology covers a wide range of indications., the indications for products in the clinical trial pipeline are predominantly concentrated in the fields of the immune system, respiratory system, and nervous system (degenerative diseases).

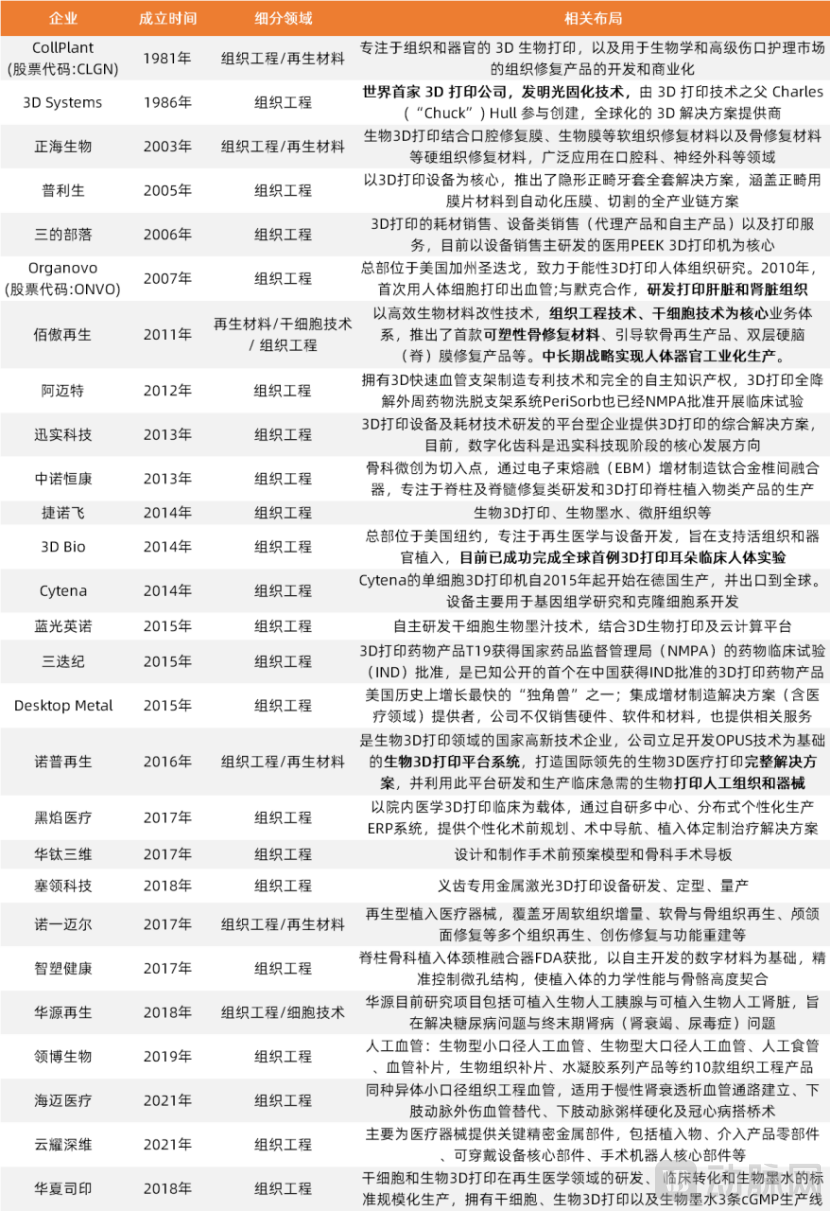

List of Pipeline Progress for Selected Companies in the Stem Cell Technology Sector (China)

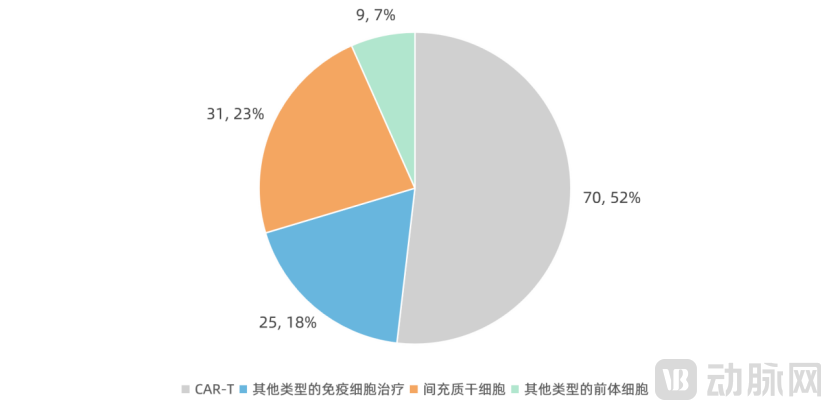

From the first half of 2022,Center for Drug Evaluation, National Medical Products AdministrationA total of 135 applications for various cell therapy products were accepted. Among these 135 applications, 70 were for CAR-T therapies, 25 for other types of immune cell therapies, and 31 for mesenchymal stem cells,Second only to CAR-T in the spotlight。

Distribution of the Number of Technical Pathways for Cell Therapy Products Accepted by the CDE

Among stem cells, mesenchymal stem cells have become a research hotspot in recent years due to their robust differentiation and regenerative capabilities as well as their immunomodulatory effects.

Integrating Technologies Such as Artificial Intelligence (AI) with Stem Cell Research to Enhance Efficacy

With the explosive growth of biological data, advancements in computing power, the emergence of next-generation in vitro models, and the automation of biological laboratories, an increasing number of impactful cases demonstrate that opportunities for applying artificial intelligence are maturing.In terms of technological pathways, some companies are choosing to leverage artificial intelligence (AI) to efficiently empower stem cell research and development.

Selected Companies in the Stem Cell Technology Sector (for details on each company’s technologies and features, please refer to the main text of the report)

Embedding digitalization and analytics into research and development is critical to driving project success and delivering value to patients. Artificial intelligence and advanced analytics will serve as key drivers in enhancing the return on R&D investment across the cell therapy value chain, by accelerating processes, reducing clinical failures, lowering costs throughout the entire R&D value chain, and enabling sustainable technology platforms.

Regenerative Materials: Innovative Technologies Unlock Greater Possibilities, with Mature Application Scenarios

Biomedical materials need to possess three key characteristics in tissue repair and regenerative medicine:

First, the material must possess biocompatibility or biosafety, eliciting a low host immune response, and be capable of supporting or enhancing cellular activities to promote tissue repair and regeneration. Second, the material should have an appropriate structure and good permeability to support the transport of oxygen and nutrients, thereby facilitating and maintaining cell–cell interactions. Third, regenerative repair materials must be biodegradable or absorbable, with a degradation rate that matches the rate of tissue regeneration.

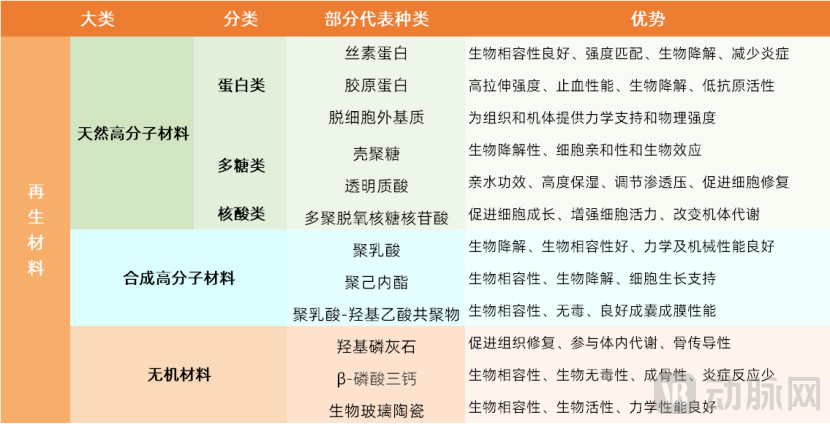

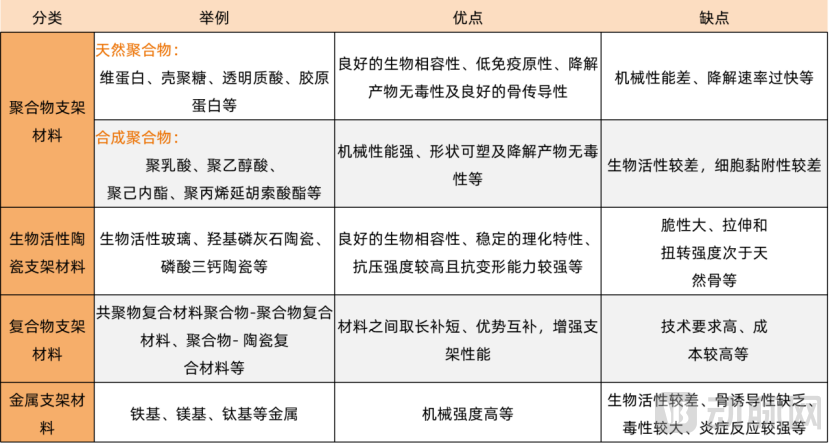

Currently, the types of regenerative materials involved in clinical and preclinical studies mainly fall into three major categories: natural polymers, synthetic polymers, and inorganic materials. Representative materials from each category exhibit their own advantageous properties in clinical applications.

Comparison of Advantages Among Representative Categories of Recycled Materials

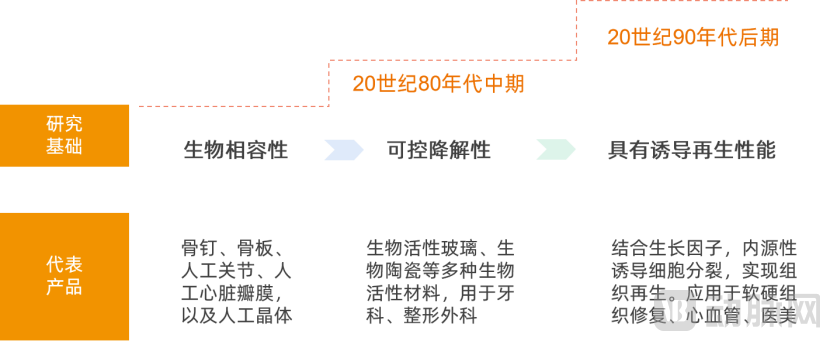

From the historical development of materials,Following the evolution from first-generation biomaterials to second-generation bioactive materials, the late 1990s witnessed the emergence of regenerative medicine,Third-Generation Biomaterials with Regenerative Induction Properties Have Become a Current Research Hotspot. Such materials can endogenously induce cell division to achieve tissue regeneration.

History of the Development of Regenerative Materials

Third-generation biomaterials can be applied to skin defect repair, soft tissue repair, articular cartilage repair, vascular and catheter coatings, medical aesthetics, and other areas, demonstrating significant development potential.

Compared with biomaterials possessing other properties, bio-regenerative materials offer numerous distinct advantages. Currently, the primary materials utilized by enterprises in China's regenerative materials industry includeComposite hyaluronic acid, collagen, polylactic acid, silk fibroin, decellularized matrixetc.

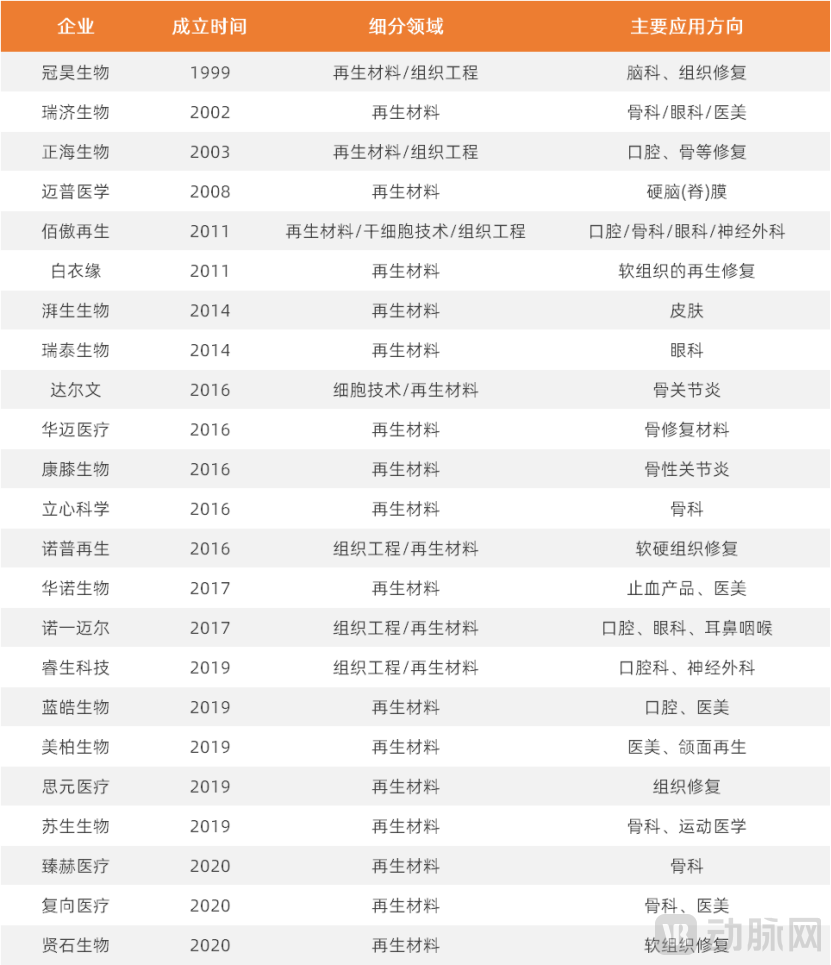

List of Selected Companies in the Regenerative Materials Sector (For details on each company’s technologies and features, please refer to the tables in the main body of the report)

Collagen: A High-Frequency Choice in R&D and Clinical Applications for Regenerative Material Companies

2022 was the year collagen stepped into the spotlight.

In August, Bloomage Biotech held a product launch event for its collagen offerings, officially releasing collagen raw materials such as animal-derived collagen and recombinant humanized collagen. In November, Giant Biogene successfully listed on the Hong Kong Stock Exchange, following Jinbo Bio’s initial public offering on the Beijing Stock Exchange. Meanwhile, Jiangsu Wuzhong, originally a pharmaceutical company, is accelerating its entry into the market, with its self-developed repair dressing soon to be launched. Utilizing Type III recombinant humanized collagen, the product addresses the needs of sensitive skin repair and post-procedure recovery after photoelectric medical aesthetic treatments. Additionally, according to Imeik’s annual report, the company is also actively pursuing R&D projects in gene-recombinant proteins.

Representative Companies and Their Technologies in the Collagen Field

Currently, the most mature medical applications of collagen are in dermatology, biological membranes, biological patches, and medical aesthetic products.

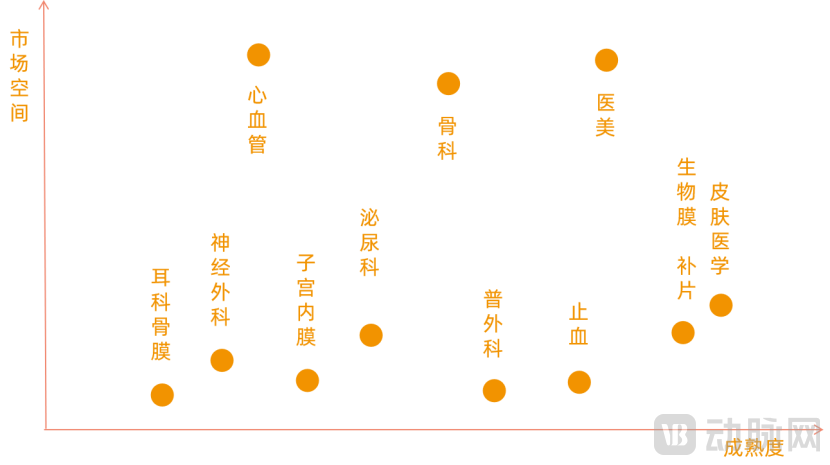

Among these, orthopedics and cardiovascular care boast broad future market prospects; however, in terms of maturity, their product pipelines are predominantly in the research and development stage.Taking orthopedics as an example, collagen for bone repair can be combined with hydroxyapatite. Meanwhile, collagen has broad application prospects in meniscus regeneration, Achilles tendon replacement and regeneration, and anterior cruciate ligament reconstruction. Although the market sizes in neurology, endometrial applications, and otologic periosteum are relatively smaller compared to orthopedics and medical aesthetics, they hold significant growth potential in the future.

Maturity and Market Size of Collagen Application Fields

Polylactic Acid: Biodegradable with Excellent Performance, Copolymers Open Up a Blue Ocean of Innovation for Recycled Material Applications

In terms of biocompatibility, polylactic acid is highly safe for the human body and can be absorbed by tissues; furthermore, it possesses excellent physical and mechanical properties,It can be used in vivo as a carrier for controlled drug release, as well as in dental materials, orthopedic materials, ophthalmic implant materials, and tissue engineering scaffolds.

In the field of orthopedics,With the application of various enhancement techniques and the increase in the molecular weight of PLA, new-type screws composed of PLA (polylactic acid)/HA (hydroxyapatite), as exemplified by absorbable screws, offer superior fixation and higher regeneration-inducing activity compared to traditional bone screws.

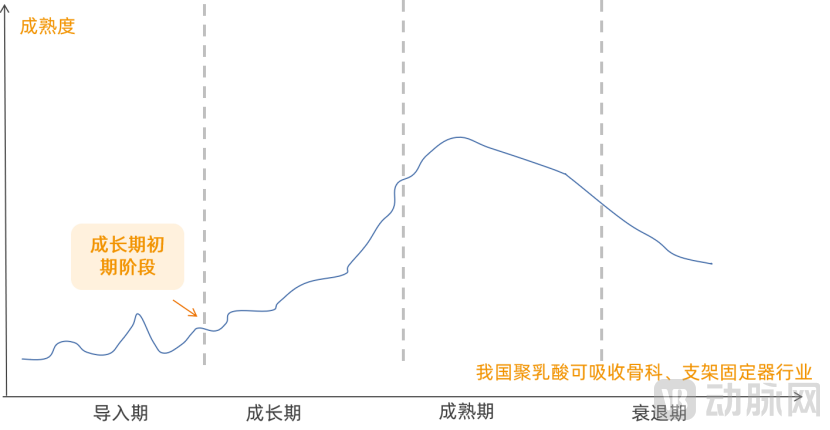

Over the past two decades, a variety of polylactic acid (PLA) internal fixation products have been developed to meet the needs for fixation of both cancellous and cortical bone, including bone plates, screws, bone tissue scaffolds, composite artificial bones, and plate underlays. Overall, the application of PLA in orthopedics in China is still in the early growth stage of the industry.

Development Stages of Polylactic Acid Applications in Orthopedics

The Core Technology of Polylactic Acid Lies in the Preparation Technology of Microspheres, i.e., the size of the microspheres.If the microspheres are too large, they may cause adverse reactions after implantation; if they are too small, they risk being phagocytosed by macrophages, thereby compromising product efficacy. Furthermore, the fabrication techniques used for the microspheres can result in variations in their morphology and density.

Domestic Regenerative Aesthetic Medical Products

Silk Fibroin: The All-Powerful Dream Factory of a Classic Material—Sports Medicine, Medical Aesthetics and Skincare, Brain-Computer Interfaces

Silk fibroin, derived from silkworm cocoons, exhibits excellent biocompatibility and cell adhesion properties, and can induce cell differentiation and tissue regeneration. Meanwhile,Biodegradable, reducing the risk of inflammation and secondary surgery。

Although derived from insect protein, the silk-spinning glands of silkworms are relatively independent, and silk contains no cells; it is a fibrous long-chain protein free of contaminating proteins. Furthermore, since the primary structure of fibroin—i.e., its amino acid sequence—lacks the characteristic telopeptides found in collagen, it does not require telopeptide removal when used as an implantable regenerative material in humans, thereby exhibiting extremely low immunogenicity within the human body.

Key Technologies of Silk Fibroin

Based on silk fibroin-relatedCorporate research interviews indicate that, in regenerative medicine, the primary application of this material is currently in tissue engineering repair. One of the goals of tissue engineering repair is to utilize degradable materials with unique three-dimensional structures, implant living human cells within them, and leverage scaffold loading.Growth Factor-Assisted DeviceTissue regeneration, where regenerated tissues or organs can be used to repair or replace the function of damaged tissues or organs.

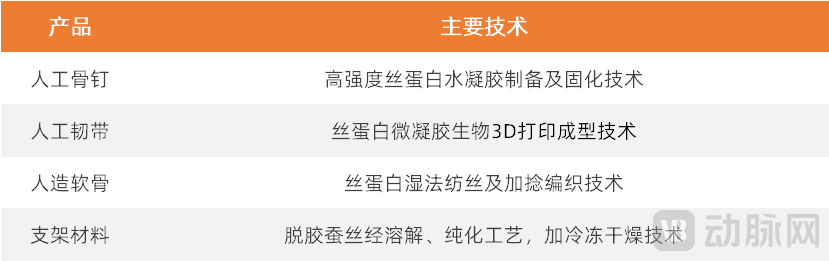

Silk fibroin is currently applied in the medical field for hemostatic materials,Artificial cartilage/ligaments, silk fibroin bone screws, artificial dura mater, cardiovascular stents, and other areas。

Tissue Engineering: Significant Technological Advantages and Integrated Development with Materials Science and Cell Technology

In the repair and replication of human tissues, if cell technology provides the "content" and regenerative materials provide the "scaffold," thenTissue engineering encompasses the contents, scaffolds, and the process of their combined fabrication.

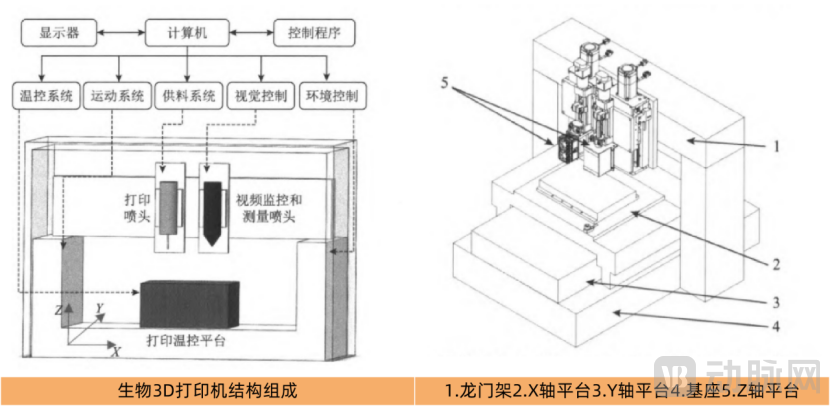

3D Bioprinting Is a Key Pathway for the Realization of Tissue Engineering.

Since the development of the first bioprinter in the early 21st century, bioprinting has been applied to fields such as the production of pathological models, tissue design for drug screening, and the regeneration of soft and hard tissues and organs.

Structure of a Bioprinter, Image Source: Chinese Society for Tissue Engineering

Globally, approximately 2 million people require organ transplants each year, with an average global supply-to-demand ratio for organs ranging from 1:20 to 1:30. In China, around 300,000 patients annually need organ transplants due to organ failure, yet only slightly more than 10,000 transplant surgeries are performed each year, indicating a severe imbalance between supply and demand. Bioprinting offers another potential solution for tissue defects and organ shortages.。

Biological 3D Printing Market Size Data Source: SmarTech

Both autologous and allogeneic transplantation suffer from disadvantages such as high surgical risk and limited sources of transplantable tissue. 3D bioprinting represents a significant innovation over traditional tissue engineering methods, enabling high-precision, high-complexity macro- and micro-scale printing, while offering advantages such as high yield rates and personalization.

3D bioprinting was initially employed for the fabrication of medical models and customized rehabilitation devices. Currently, within the field of medical 3D printing applications, product offerings span both research and therapeutic domains, encompassing a wide range of specialized sectors.Involving orthopedic implants, prosthodontics, in vitro models, preoperative planning, cardiovascular surgery, tissue engineering scaffolds, transplanted tissues and organs, oral and maxillofacial surgery, ophthalmology, neurosurgery, etc.。

Advantages and Disadvantages of Tissue Engineering Scaffold Materials

Currently, in terms of the development progress of enterprises in the field of bio-3D printing, overseas companies generally hold a leading advantage. According to incomplete statistics, there are currently 133 entity service providers in the U.S. bio-3D printing sector, including 47 hardware (bioprinter) manufacturers, 41 material (bioink) suppliers, and 59 service providers (including university bio-printing laboratories).The International Gap Is Narrowing。

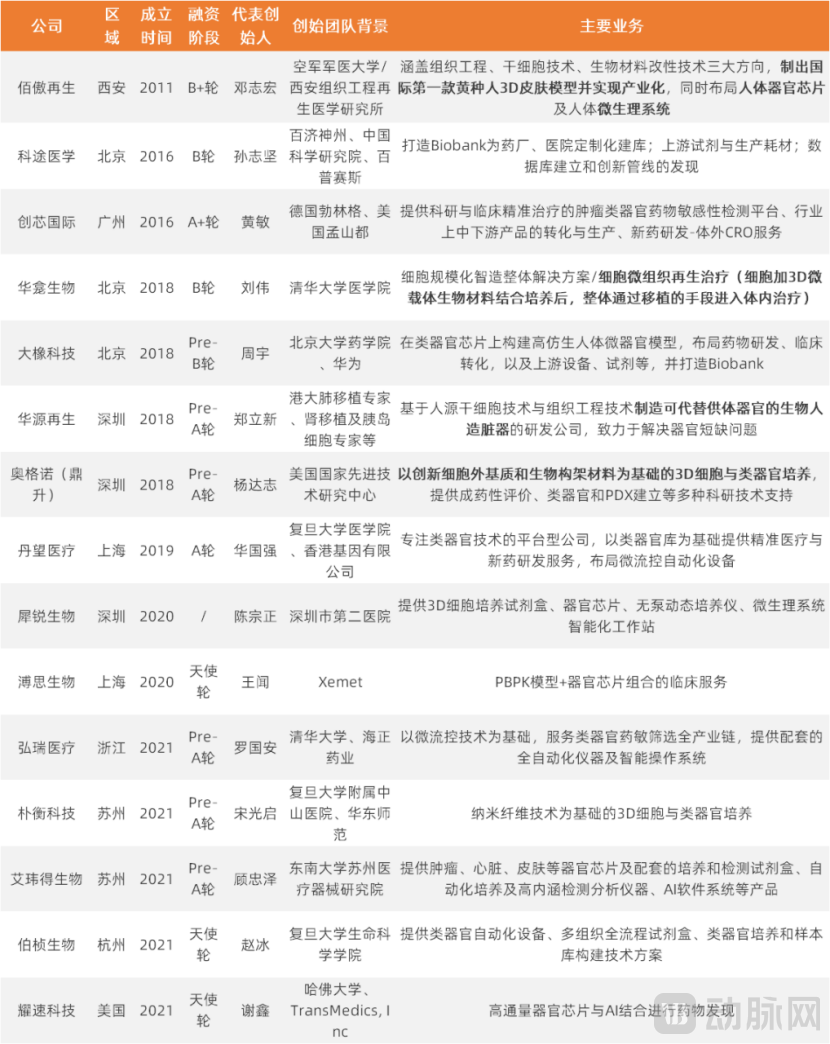

Representative Companies in the Field of Tissue Engineering

Regenerative Medicine Industry Chain and Commercialization Exploration

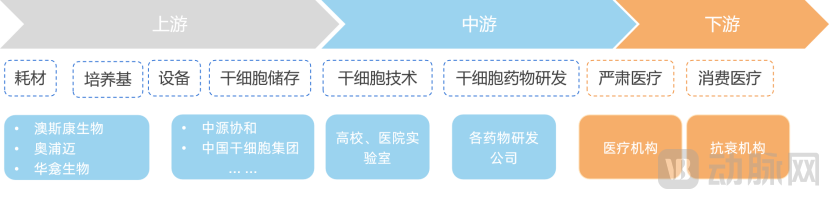

Upstream cell culture media and related business models are more mature than those in the mid- and downstream sectors.

The development of the stem cell medical industry chain encompasses stem cell storage, stem cell drug development, and stem cell therapy. According to research data from QYResearch, the compound annual growth rate (CAGR) of China’s stem cell medical industry market size was approximately 15% from 2020 to 2026. In the coming years, China’s share of the global stem cell medical market is expected to rise further. The market size of China’s stem cell medical industry is projected to reach RMB 32.5 billion by 2026.

The upstream sector comprises medical devices and consumables, the midstream focuses on stem cell drug development, and the downstream encompasses the stem cell application market, including healthcare institutions and medical aesthetic clinics. Currently, the application fields of China’s stem cell therapy industry have not yet been fully developed.The downstream application market of the industrial chain has enormous growth potential.。

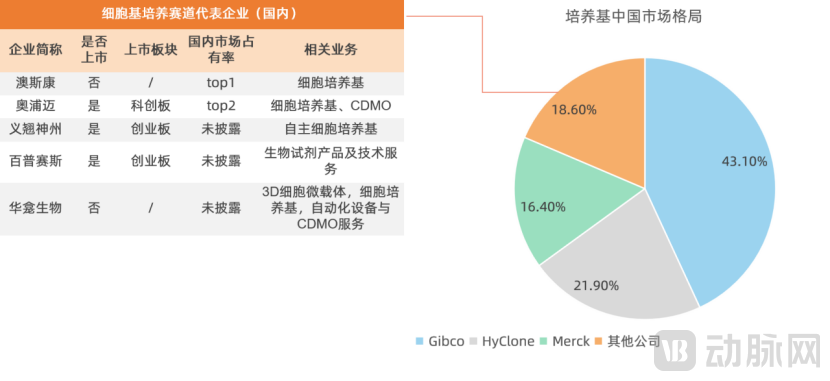

Compared to the cell storage business,High barriers to entry in the upstream cell culture media segment,However, foreign companies currently account for more than half of the market share in China.Research indicates that the competitive landscape of China's cell culture media market is dominated by imported brands. The three major international players—Thermo Fisher Scientific, Danaher, and Merck—collectively hold over 60% of the market share. However, driven by technological breakthroughs among domestic brands and intensifying international trade sanctions, the growth rate of these market leaders' shares has gradually declined over the past two years.Domestic Substitution Is Accelerating Its Expansion。

From the perspective of downstream customer demand,The Demand for Custom-Developed Culture Media Is Continuously Increasing。Upstream service providers with customization capabilities are adopting strategies to develop culture media based on customer needs, aiming to increase biopharmaceutical yields and reduce production costs.

R&D Institutions in the Midstream of the Recycled Materials Industry Chain Drive Changes in the Downstream Market

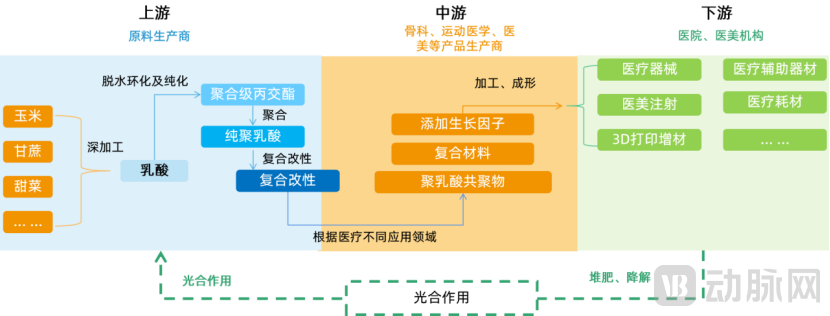

Upstream of the regenerative materials industry chain consists of raw material production and supply enterprises, midstream comprises technology R&D enterprises, and downstream includes end-users such as medical institutions and medical aesthetic clinics. The upstream segment of the industry chain is relatively mature,Taking the upstream sector of polylactic acid (PLA) as an example, although PLA production in China is still in its early stages, with few production lines built and put into operation and most of them being small in scale, numerous listed companies have already entered the field, such asHisun Biomaterials (68203.SH), Fengyuan Bio, Wanhua Chemical, etc.

andR&D activities and product iterations by midstream enterprises significantly influence the market landscape of downstream medical and medical aesthetic institutions.

Taking Imeik as an example, after the launch of its polylactic acid injection product, the company’s third-quarter 2022 financial report showed that its revenue and net profit in the third quarter increased by 55.15% and 41.55% year-on-year, respectively, while the gross profit margin rose slightly quarter-on-quarter to 94.61%.According to Huadong Medicine’s 2022 interim report, the sales of “Girl’s Needle” in the first half of the year were also impressive, reaching approximately RMB 271 million.

In the field of orthopedics and stents, the fourth-generation bioresorbable cardiac stent (Xinsorb), developed by Weigao Orthopedics (688161.SH) with independent Chinese intellectual property rights, was launched in March 2020. This cardiac stent uses polylactic acid as the base material and has achieved favorable results in clinical trials.

From the perspective of the industrial chain, midstream medical R&D enterprises will continuously drive changes in the structure and landscape of the downstream market, while also validatingR&D capability is a key driver for midstream recycled material companies to realize commercial value.

Tissue Engineering: Robust Growth in the Midstream, and Commercial Exploration of Downstream Organoids Underway

Upstream in the tissue engineering sector are printing hardware and consumables; the advancement of such equipment has a certain impact on the successful completion of midstream product solutions.From the perspective of upstream commercialization strategies, bundling equipment with printing materials facilitates market entry and eases commercial implementation.How Midstream Bio-3D Printing Business Models Are Focusing, as Industry Giants Actively Lay Out Their Strategies.Three leading overseas companies involved in midstream operations—BICO, 3D Systems, and Desktop Metal—have each adopted distinct commercial pathways (see the main body of the report), providing valuable references and insights for the commercialization efforts of domestic bioprinting-related enterprises.

Organoids represent a downstream branch of tissue engineering, a key technological approach for organ regeneration. According to research conducted by VCBeat,At the current stage of development in China, organoids are primarily in the form of in vitro microtissues.,Widely used in drug screening, the transition of bio-3D printing from tissue printing to organ printing still requires a period of development and continuous in-depth research in the field of basic science.

Commercialization Momentum: Insurance Mechanisms to Stimulate Market Vitality, Intensifying Industry Standard Interactions

The commercialization of regenerative medicine requires the introduction of insurance coverage, and collaboration with insurers will further promote product adoption.Taking stem cell-based drug products as an example, regulatory approval for market launch is undoubtedly the long-awaited milestone for every new drug developer. However, to gain market acceptance, the more critical factor may well be the drug’s cost-effectiveness.

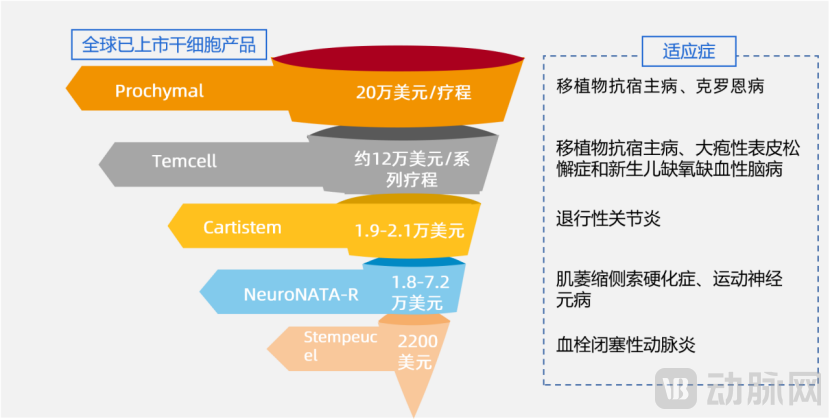

Among stem cell products, Temcell, the best-selling one, has benefited from its inclusion in national health insurance coverage. Originating from Japan, Temcell primarily utilizes bone marrow-derived mesenchymal stem cells, with a current price of approximately $120,000 per treatment course. According to JCR’s financial reports, Temcell generated sales revenue of around $18 million in 2018 and approximately $28 million in 2019.

To promote the development of regenerative medicine, Japan will include regenerative medical products in its national health insurance coverage after they are launched on the market. A single dose of Temcell costs 868,680 yen, and a full course of treatment amounts to approximately 13.9 million yen. With health insurance subsidies, patients are only responsible for 10–30% of the cost.

Between 2014 and 2017, four cell/gene therapies—Provenge, Glybera, Chondrocelect, and MACI—were withdrawn from the market or suspended in the European Union. This was not due to safety concerns, but rather because they failed to persuade governments and insurers to cover their costs. Whether stem cells will enjoy a broader market in the future depends not only on intrinsic factors such as technology and R&D, but also on the policy environment,The payment structure also holds a significant position.。

Given the early-stage nature of regenerative medicine, companies in the industry can actively participate in the development of industry standards, enablingEnterprises, industry associations, and regulators engage in high-frequency interactions.,Establishing a Robust Information Communication Platform。

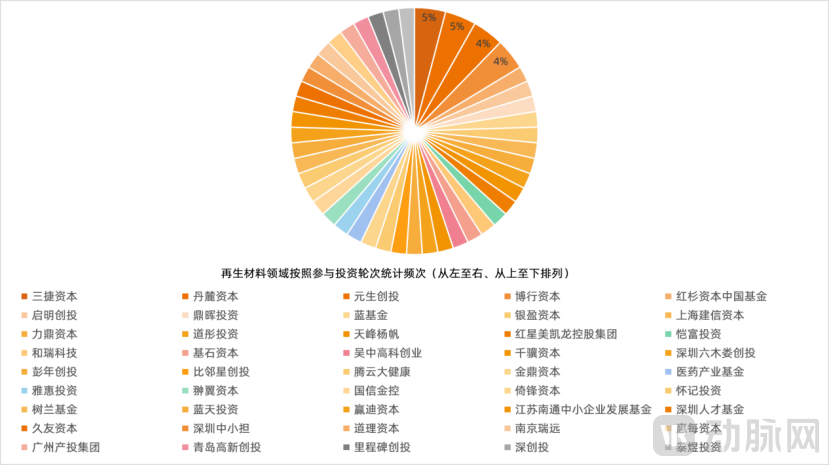

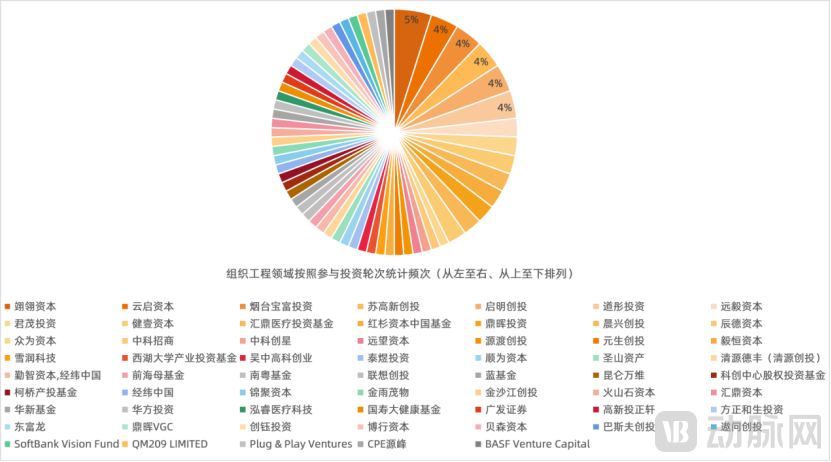

Investment and Financing

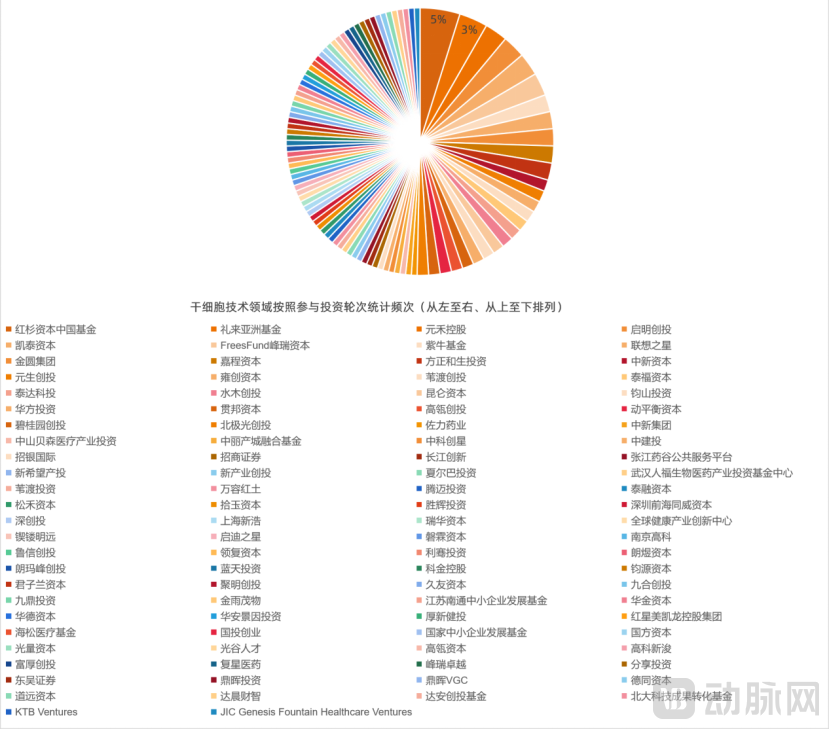

According to ARM statistics, financing in the field of regenerative medicine reached $23.1 billion in 2021. Additionally, according to Statista, the global market size for regenerative medicine was approximately $16.9 billion in 2021 and is projected to reach $95.5 billion by 2030, with a CAGR of 21.22%.

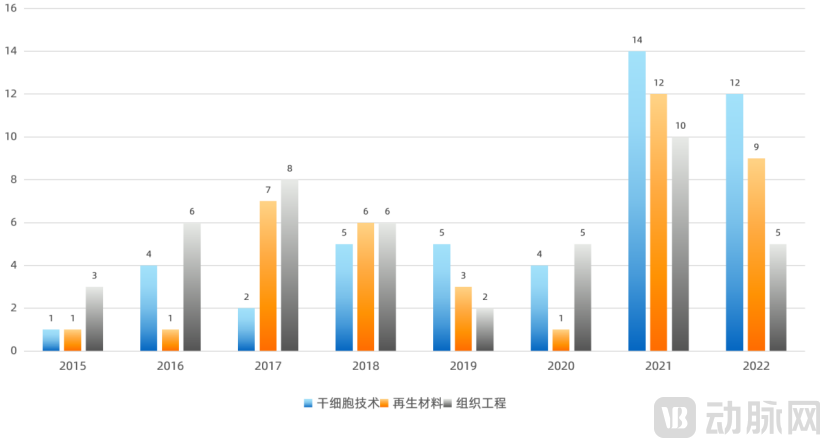

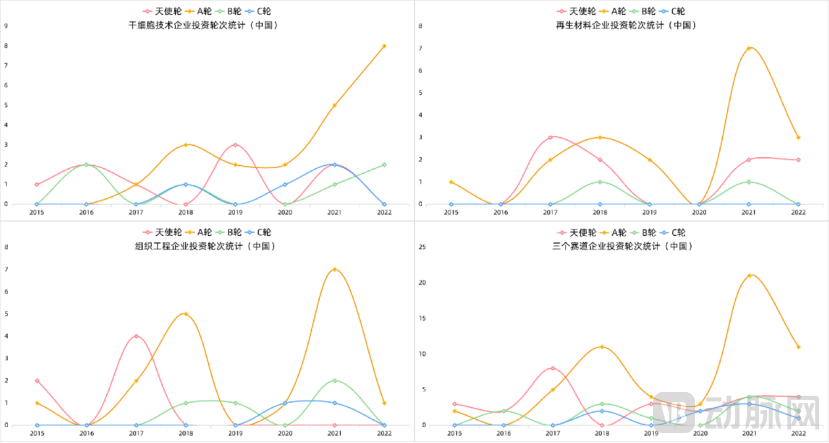

Over the past two years, despite a cyclical contraction in overall investment and financing activities, investor enthusiasm for the regenerative medicine industry has remained undiminished. We have categorized and compiled statistics based on stem cell technology, biomaterials, and tissue engineering.Following the trough in 2020, all three sectors have demonstrated a counter-trend rebound.。

Statistics on the Number of Investment and Financing Deals in the Regenerative Medicine Industry by Subsector (2015–2022)

Overall, the regenerative medicine industry has seen a wave-like upward trend in the number of Series A financing events over the past five years, rising to a peak in 2021 before declining somewhat in 2022. Specifically, among the three sectors (please refer to the main body of the report for detailed financing information on each sub-sector within regenerative medicine), the stem cell sector has exhibited a distinct trend compared to the other two, with continuous growth in both 2021 and 2022.

The underlying reasons are twofold: on the one hand, the gradual relaxation and increased support of China’s stem cell policies have facilitated the clinical translation of more research projects, thereby boosting investor confidence.

On the other hand, from an investment perspective, the CGT industry has seen frequent financing and investment activities in recent years, with a series of IPOs achieved recently. This has, to some extent, driven societal attention toward the broader cell therapy field. Meanwhile, as certain stem cell products in China have successively received approval to enter clinical trials over the past two years, they have attracted the attention of keen-sighted capital. Capital movements always precede market development; while the immune cell sector is already flourishing, these diligent investors have begun to focus their attention on the earlier-stage iPSC field.

Technology, Talent, Craftsmanship, and Management Are Key Dimensions in Investment Decision-Making

We interviewed Gu Cuiping, Managing Director at Sequoia China, to discuss the multidimensional criteria that Sequoia China prioritizes when investing in companies within the iPSC sector.

First, the technical background of the company's founding team.Second, the construction of corporate talent pipelines.Taking the manufacturing of cell therapy products as an example, scaling from small-scale experimental production to subsequent continuous and stable manufacturing involves complex processes that require the involvement of professionals with interdisciplinary backgrounds and comprehensive experience.3. Comprehensive understanding of product manufacturing processes.In the transition of iPSCs from technology to products, manufacturing processes and production facilities also play a critical role.4. Establish comprehensive Good Manufacturing Practices (GMP) for drug production and clear regulatory approval pathways, accelerate the clinical validation of products, a process that more comprehensively validates a company’s capabilities.

Mergers and Acquisitions Become a Strategic Approach for Expansion Among Leading Regenerative Medicine Companies

Acquisitions are also frequently occurring in the fields of cell therapy, biomaterials, and tissue engineering.

In the materials sector, in April 2022, Bloomage Biotech announced that it had signed an Equity Transfer Agreement with China National Coal Geology Group Co., Ltd. to acquire a 51% equity stake in Beijing Yierkang Bioengineering Co., Ltd. for RMB 233 million, formally entering the collagen industry. In August, Shiseido, the beauty giant, officially launched its special investment fund in China, with its initial investment targeting a company specializing in recombinant collagen raw materials.

In the field of bioprinting, Cellink announced on August 6, 2019, that it would acquire Cytena for €30.25 million. In August 2020, Bico acquired the German precision dispensing company Scienion and its subsidiary Cellenion for €80 million, further mastering cell-based 3D printing technology. 3D Systems (NYSE: DDD), founded in 1986 by Chuck Hull, known as the “Father of 3D Printing,” has also deeply entered the 3D bioprinting sector through acquisitions, mergers, and expansions. A key milestone was its acquisition of Allevi, a developer of 3D bioprinters with a mature bioprinting system, in May 2021.

From the perspective of corporate investment, tissue engineering, cell-based products, and regenerative materials involve relatively long development cycles and diverse portfolio combinations, creating significant pressure for capital exit among many investment institutions with short-term horizons.For companies in the regenerative medicine industry, founding teams are more inclined to partner with investors who have a relatively longer investment recovery horizon.

One of the Reasons Why Investment Institutions Favor the Regenerative Medicine Sector, lies in the fact that the regenerative medicine market is addressing previously unmet needs in healthcare,It lies in creating a new market, rather than replacing the market for traditional therapeutic approaches.Therefore, regenerative medicine faces an untapped incremental market, which isAttractionNumerous Investment InstitutionsContinued participation in thisThe Huge Momentum of the Track。

Industry Trends

Regenerative Materials, Cell Technology, and Tissue Engineering: Three Major Directions Will Continue to Drive Innovative Growth

(1) Specific commercialization entry points in the field of tissue engineering will gradually become clearer over the next three years

A survey by VCBeat reveals that practitioners in the field of tissue engineering generally believe that clear market validation for commercialization pathways will emerge within three years, identifying specific stages where such commercialization is most likely to occur. Achieving this goal also requires industry participants to collaboratively address and resolve key technical bottlenecks across all development phases.

(2) It will become a trend to carry out material modification and in-depth collaborative development of recycled materials according to different medical application fields

Overall, recycled materialsdevelopment will exhibit a trend of integrating new and existing technologies. Meanwhile, the regenerative materials industry is advancing in recombinant collagen, composite hyaluronic acid, polylactic acid, acellular matrix, and silk fibroin.continuous innovation, research, and development of regenerative factors in a series of regenerative materialsthe integration, developing entirely new material formulations and manufacturing processes. On a global scale, China will also emerge as the leader in the new wave of materials technology.

(3) New products based on novel cell engineering platforms, such as those utilizing chemical induction and adult stem cells, will continue to emerge.

Chemical reprogramming technology is safeA series of technologies that are simple, easy to standardize, and easy to controlAdvantages: Overcoming the limitations of certain pluripotent stem cell preparation technologies, it is the next phase of fine-An Important Development Direction in Cell Technology That Cannot Be OverlookedLooking ahead, a variety of new products based on novel cell engineering platforms will continue to emerge, such as chemically induced intercellular transdifferentiation technology and various applications of adult stem cells. These innovations will unlock vast market opportunities in the field of regenerative medicine.

Regenerative medicine is still in its early stages globally, presenting Chinese enterprises with abundant opportunities for innovation and leapfrog development.

Overall,Regenerative medicine remains in its early stages globally and will continue to mature over the next 20 years.。In traditional fields such as vaccines, antibodies (large molecules), and small-molecule drugs, China has historically been in a catch-up position. However, in the field of cell and gene therapy (CGT), interviews with multiple industry practitioners and heads of investment institutions indicate that, due toTissue engineering, stem cell technology, and regenerative materials have relatively short development histories. Currently, China is experiencing robust growth in these areas, with the technological gap between China and overseas leaders being minimal.。

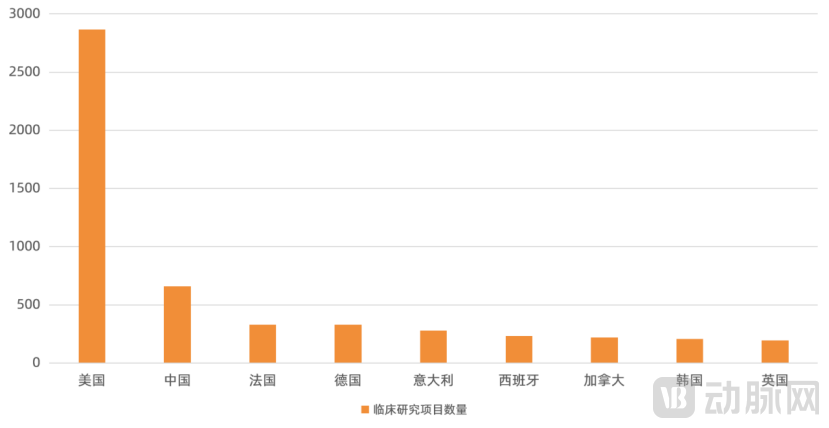

Distribution of the Number of Stem Cell Clinical Research Projects in Selected Countries

AI Technology and Traditional Medical Devices Will Converge with Regenerative Medicine, and Organoids Will Be Industrialized

(1) Over the next decade, commercialized products for more than 50% of human tissues and simple organoids will emerge.

According to FDA clinical data, 20% of human tissues have already been developed into commercialized products and are being sold.

Furthermore, cell and scaffold components for 70% of human organs have advanced to clinical trials at Phase II or beyond. The development and clinical timelines for organ products combining scaffolds with cells are relatively longer compared to the aforementioned two categories. Nevertheless, it is projected that over the next decade, more than 50% of human tissues and simple organs (including artificial kidneys, artificial blood vessels, and artificial pancreases) will see the commercial launch of products worldwide, thereby benefiting patients.

This trend requires the integrated development of three major fields in regenerative medicine—cell therapy, biomaterials, and tissue engineering—to be better realized. Currently, drug trials are conducted on cells and microcarriers; in the future, with the advancement of organoid technology, such trials will increasingly be performed on engineered tissues and organs. Replacing cell-based research models with organ- and tissue-based systems will also become a key direction for industry development.

(2) Sub-sectors such as traditional medical devices and AI technologies will gradually extend into and integrate with the regenerative medicine industry.

In the future, an increasing number of formerly implantable medical devices—namely, purely substitutive medical device products—will begin to incorporate technologies for tissue stimulation and regenerative repair, evolving into medical device products aimed at regenerative repair.

Meanwhile, the entire regenerative medicine industry chain will gradually unfold in the future, giving rise to numerous high-quality opportunities in specialized niches. Many technologies that disrupt existing frameworks will also emerge and integrate with the regenerative medicine sector. For instance, AI-assisted drug discovery is already a mature business model. Introducing AI technologies into cell manufacturing, material science and formulation, and tissue engineering design will generate multidimensional synergies, significantly accelerating the overall development of regenerative medicine.

Regulatory Pathways for Certain Subsectors of Regenerative Medicine Remain Unclear, and Ethics Will Also Impact Industry Development

Due to the innovative nature of the field of regenerative medicine and the emerging status of the entire industry, global regulations and standards are still in their infancy. CurrentlyThe regulatory pathways for submissions in certain niche sectors remain relatively unclear.For instance, the cell culture media industry still lacks a comprehensive quality regulatory system. Domestic enterprises demonstrate the robustness of their quality systems through DMF filings, GMP management system certification, ISO certification, medical device certification, and quality audit outcomes.

However, many respondents in the survey also indicated that,CDE's learning curve is very steep., how to formulate standards that are more suitable for China and regulatory rules that align with our national conditions. Through close communication with industry researchers and enterprises, and as an increasing number of U.S. products receive IND approvals, the openness, certainty, and clarity of domestic regulation are rapidly improving. The gradual clarification of regulations will become inevitable.

andIn the field of recycled materials, regulations will become stricter.Whether in the formulation of new material standards, the issuance of new regulations, or the release of regulatory guidance principles, China is currently clarifying requirements that were previously ambiguous within the industry, thereby raising the entry barriers to some extent. For enterprises, this elevation in barriers will eliminate a number of players, further driving those remaining in the market to pursue technological iteration and product innovation.

Furthermore, ethics will influence industry development to a certain extent. Compared with traditional fields,The field of regenerative medicine will spark more ethical discussions among all stakeholders and the general public.

Just as the widespread social impact of Dolly the cloned sheep transcended cloning technology itself, discussions on the ethics of human cloning from diverse perspectives have sparked intense societal debate. Similarly, the extent to which regenerative medicine—which also involves pathways for replicating human tissues—can be clinically applied in the future will be influenced, to some degree, by ethical deliberations, thereby shaping the industry’s development.

In a sense, the rise of regenerative medicine has opened up new avenues for disease treatment. Its significance lies not only in providing a novel therapeutic approach to alleviate patient suffering but, more importantly,Proposes a novel concept of “activating, replicating, and regenerating” tissues and organs to rejuvenate the human immune mechanism.

Undoubtedly,“The New Era of Regenerative Medicine” has arrived, and it is a “profound medical revolution.”

The above is an excerpt from the report. The report framework is as follows. Feel free to add the mini-program mentioned earlier to get the full report for free.

Acknowledgements

Special thanks to the following industry professionals for their strong support of this report.:

Jin Yan, Chief Strategic Advisor at Baihong Group/Baiao Regeneration

Gu Cuiping, Managing Director at Sequoia China

Luo Wangqian, Founder of Huafang Capital

Liu Yezhuo, CEO of FuXiang Healthcare

Zhang Jianjun, Founder of Siyuan Medical

Dong Xiang, Partner at Siyuan Medical

Yang Xi, Founder and CEO of Nuope Regenerative

Mr. Wei, Co-founder and CEO of Ruijian Pharma

Liu Wei, Co-founder & CEO of CytoNiche

Zheng Lixin, CEO of Huayuan Regenerative Medicine

Cheng Xin, Chief Scientist at Zhixin Haozheng

Rui Yunyun, Investment Manager at Suxin Venture Capital