2022 Digital Health Annual Innovation White Paper: Three Key Areas and Five Major Trends Illustrating China's Digital Health Story

Regarding the traditional healthcare system, William Kissick, a professor at Yale University in the United States, proposed the famous “impossible trinity”: under given constraints, it is difficult for a country’s healthcare system to simultaneously achieve “improved quality of medical services, increased accessibility to medical services, and reduced costs of medical services.” To break the “impossible trinity” of the traditional healthcare system, it is essential to introduce new technological and model innovations. Consequently, the rapidly developing digital health sector is regarded as an “innovative prescription” for resolving the “healthcare impossible trinity.”

Over the past decade, the rapid advancement of digital technology in China has driven the development of digital healthcare, laying a solid foundation for informatization. Digital healthcare has gradually begun to play a role in medical interventions and is on the verge of advancing toward higher-order disruptive models.

To document the grand transformation of digital health and explore its vast future potential, VCBeat and VBInsight have compiled an analysis of the current landscape and development trends in digital health for 2022, producing the “2022 Annual White Paper on Digital Health Innovation.” This report aims to clarify how digital health innovation drove industry development in 2022, chronicle the “Chinese story” of digital health innovation, and establish a “Chinese model” for healthcare innovation.

(Note: To obtain the full report, please scan the QR code at the end of the article to add our assistant. If you have already added them, please proactively reach out.)

The following is a brief overview of the white paper.

The definition of digital health varies across different specific contexts. It is generally regarded as a novel healthcare model that applies modern digital information technology throughout the entire medical process, representing both the developmental direction and management objective of public healthcare.

In its early stages, digital healthcare was nearly synonymous with eHealth, representing the application of information and communication technologies in the medical field. In recent years, the concept of mobile health (mHealth) has been incorporated, expanding the scope to include advanced digital technologies such as big data applications and analytics, artificial intelligence, and the Internet of Things.

The Stanford Center for Digital Health posits that digital health encompasses five categories of digital health technologies: 1. Artificial Intelligence (AI), Machine Learning (ML), and various AI algorithms, including deep learning, image processing, and advanced analytics; 2. Healthcare informatics, infrastructure, and data management systems, including Electronic Health Record (EHR) systems; 3. Mobile and web applications, including SaaS platforms, cloud-based software tools, and social applications; 4. Emerging clinical care models, including telemedicine, patient engagement, and provider-patient interaction; 5. Wearable devices, sensors, and other Internet of Things (IoT) hardware devices.

Digital healthcare encompasses the treatment, control, diagnosis, prevention, and rehabilitation of diseases.

This has become the currently widely accepted scope of digital health, and is broadly recognized, adapted to specific circumstances, and applied in various scenarios. Drawing on these definitions, the scope of digital health covered in this white paper primarily includes the application of digital technologies in the processes of disease prevention, diagnosis, control, treatment, and rehabilitation management.

Digital health can bring significant benefits to healthcare. From mobile health applications and software that support clinicians’ daily decision-making to artificial intelligence and machine learning, digital technologies have been driving a revolution in healthcare. Overall, the introduction of digital health can enhance the accessibility, efficiency, effectiveness, and equity of healthcare services.

The Four Evolutionary Stages of Digital Health

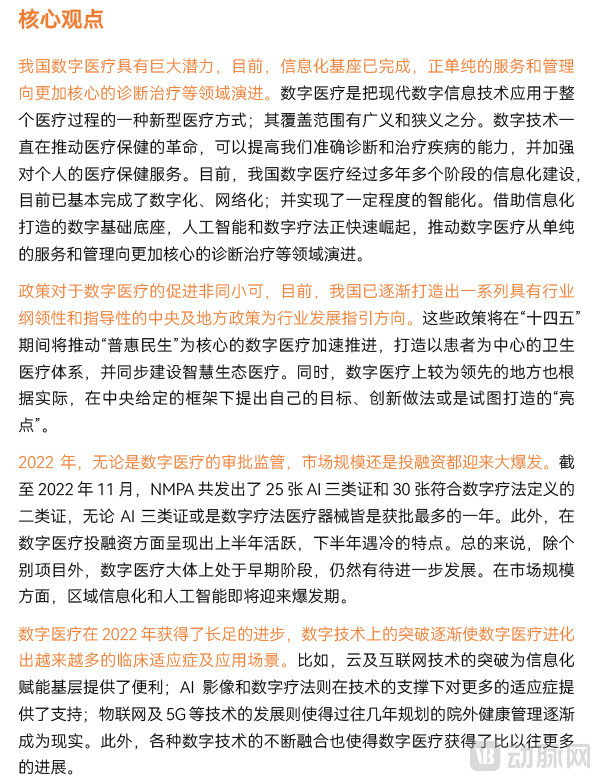

Specifically, digital healthcare is manifested in four aspects: the digitization and networking of medical devices, the informatization of hospital management, and the enhanced convenience and personalization of medical services. Broadly, it can be divided into four stages: digitization, networking, intelligence, and transformation of healthcare models.

With the sequential realization of digitalization, networking, and intelligence, a corresponding foundation has been laid for the transformation of healthcare models. Through quantitative changes ultimately leading to qualitative leaps, healthcare systems and service delivery models will be transformed, service quality will be enhanced, and the ideal vision of digital healthcare at the current stage will be realized.

China started relatively late in the development of digital healthcare, and progress was initially slow due to limitations in digital capabilities. However, in recent years, China has achieved leapfrog development in information technology and communications technology, resulting in significant advancements in digital healthcare.

Currently, China’s healthcare informatization has entered the 4.0 stage, characterized by regional interconnectivity enabling big data analytics and AI-powered assisted diagnosis and treatment. It has achieved development from the individual to the population level, and from local to wide-area coverage, with enhanced connotations and functions, and continuously expanded service scope. This has solidified the foundation of digital healthcare in China.

The continuous accumulation of data has laid the foundation for the development of emerging digital healthcare modalities, such as artificial intelligence (AI) and digital therapeutics. Notably, AI-assisted diagnosis in medical imaging based on computer vision has attracted significant attention. Between 2015 and 2020, hundreds of companies entered this sector, with more than one hundred securing financing from the primary market.

Currently, as an increasing number of AI medical device certifications are approved, AI imaging has gradually entered the 2.0 stage. If the 1.0 era was characterized by broad-spectrum innovation, primarily aiming to cover as many fields as possible, then innovation in the 2.0 stage is point-specific innovation built upon the achievements of the 1.0 phase.

Just as with artificial intelligence, the continuous refinement of the digital foundation—comprising healthcare informatization and intelligent systems—has paved the way for the activation of digital therapeutics. This emerging field is being leveraged by researchers to directly intervene in disease treatment and improve clinical outcomes, giving rise to a diverse array of distinct digital therapeutic modalities that support disease screening, diagnosis, treatment, and rehabilitation. Nevertheless, overall, it remains in its early exploratory stage.

Overall, after years of multi-stage informatization development, China’s digital healthcare sector has largely achieved digitization and network connectivity, while attaining a certain degree of intelligence. Leveraging the digital infrastructure built through informatization, artificial intelligence and digital therapeutics are rapidly emerging, driving the evolution of digital healthcare from purely service- and management-oriented functions toward more core areas such as diagnosis and treatment.

What progress was made in the digital healthcare sector in 2022 regarding key external factors such as policy, market, and capital? What trends do these developments represent? In this chapter, we will analyze data on policies, investment and financing, and the market to illustrate these points.

China is a typical example of a "big government," with state involvement in matters both large and small. Meanwhile, public healthcare institutions account for an overwhelming share of medical services in China, and government-backed health insurance serves as the primary payer. Therefore, government policies are critically important to the development of digital health. Currently, thanks to years of continuous policy guidance, China has fostered a favorable environment for the growth of digital health, providing support for talent cultivation and enterprise development in related industries.

Central policies are primarily characterized by their industry-wide programmatic and guiding nature, aimed at setting the direction for industrial development. China’s digital healthcare construction plan exhibits distinct phased characteristics, closely aligned with the “Five-Year Plans,” around which a series of macro-level policies have been formulated. During the 14th Five-Year Plan period, policies will accelerate the advancement of digital healthcare centered on “inclusive public welfare,” build a patient-centric healthcare system, and simultaneously develop a smart ecological healthcare system.

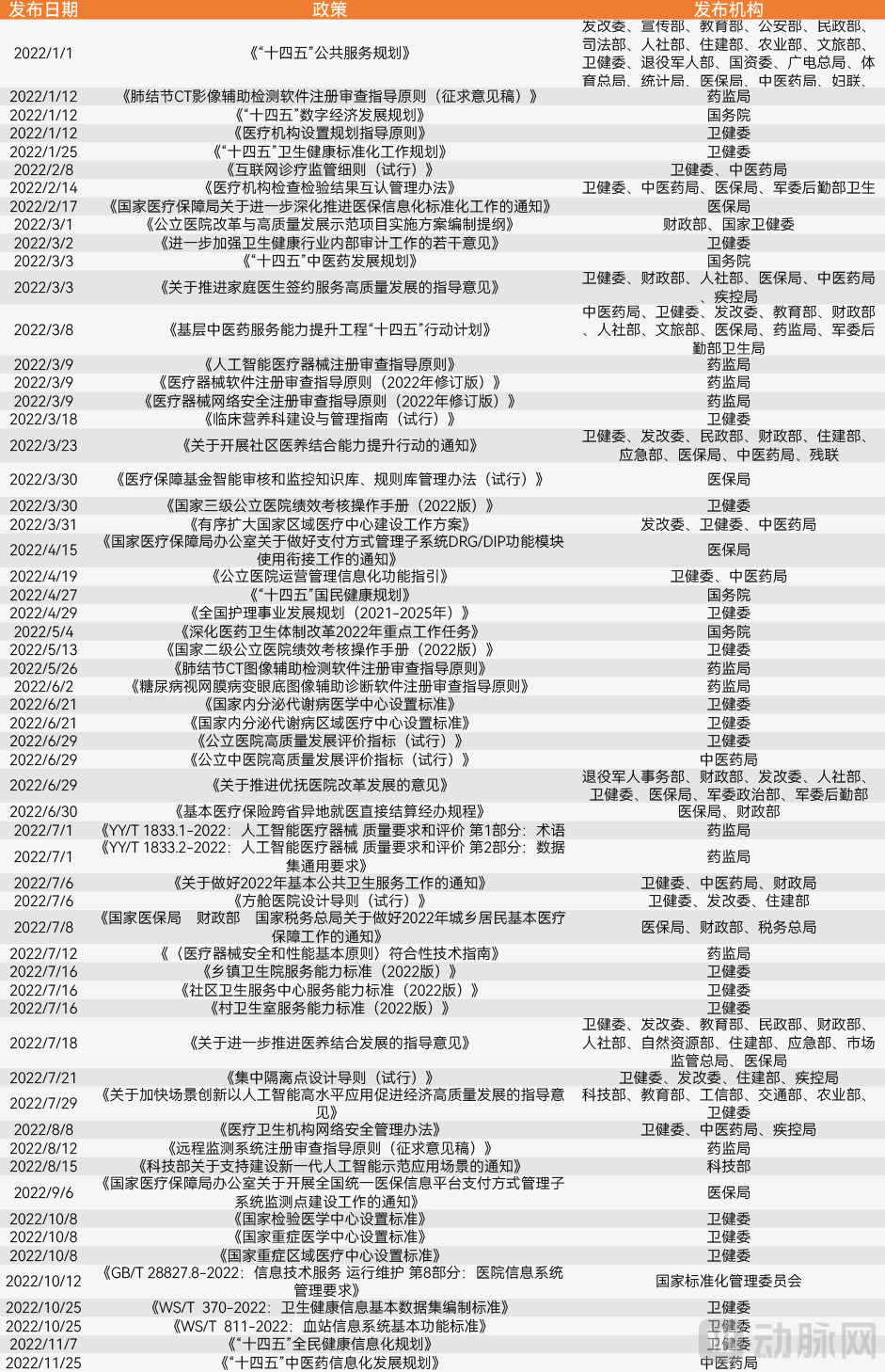

According to VCBeat data, as of November 10, 2022, the Chinese central government had issued a total of 59 policies related to digital healthcare in 2022. These policies primarily focused on accelerating the standardization and integrated development of platforms, deepening the application of new scenarios and technologies, and promoting the high-quality development of the healthcare system.

Incomplete Statistics of China’s Central Policies on Digital Healthcare in 2022

2022 was a critical year for the implementation of China’s 14th Five-Year Plan. A consensus has been reached in China on the importance of the digital economy, with digital healthcare being a key component. Accordingly, to advance the implementation of digital healthcare-related areas outlined in the 14th Five-Year Plan, the Chinese central government issued multiple policies in 2022, including the “14th Five-Year Plan for Public Services,” the “14th Five-Year Plan for Digital Economy Development,” the “14th Five-Year Plan for Informatization Development of Traditional Chinese Medicine,” the “14th Five-Year Plan for Standardization Work in Health,” and the “14th Five-Year Plan for National Health Informatization.”

In addition to the macro-level policies centered on the 14th Five-Year Plan, healthcare regulatory authorities—including the National Health Commission, the National Administration of Traditional Chinese Medicine, the National Medical Products Administration, and the National Healthcare Security Administration—must issue supportive policies within their respective jurisdictions. These policies, covering specific regulations, systems, and standards for artificial intelligence, informatization, and digital therapeutics in digital healthcare, are essential to fulfilling their regulatory mandates and driving the continuous development of digital healthcare.

In line with the implementation and deepening of central government policies, numerous local policies targeting digital healthcare have been developed and adapted based on local conditions. These local policies specify implementing agencies, clarify task allocations, and set timelines for execution in their detailed implementation rules.

Furthermore, localities have also proposed their own targets, innovative practices, or sought to create “highlights” based on actual conditions within the framework established by the central government. For instance, Beijing issued multiple policies in 2022 related to elderly care and rehabilitation, all of which emphasized vigorously leveraging digital health to enhance service efficiency and quality. Shanghai has placed greater emphasis on industrial support and development; as artificial intelligence is a priority pioneering industry for the city, its integration with healthcare scenarios has been fully reflected in numerous local policies. Zhejiang has adopted a pragmatic approach, focusing on patients and striving to improve the convenience of medical services through one-stop solutions. Hainan has identified digital therapeutics as a key focus for the future development of its health industry and has released several corresponding policies.

In 2022, AI-based medical imaging and digital therapeutics, which had already entered the clinical field, also experienced a surge in regulatory approvals.

According to incomplete statistics compiled by VCBeat from the official website of the National Medical Products Administration (NMPA), a total of 25 Class III AI medical device certificates had been issued by the NMPA as of November 2022, marking the highest annual approval count on record. With increasingly standardized regulatory frameworks, the approval process for Class III AI medical devices is accelerating. Leading companies have demonstrated outstanding performance, with some securing multiple Class III AI certificates. It is evident that the once highly fragmented landscape of the AI healthcare industry is gradually evolving toward greater market concentration.

In the field of digital therapeutics (DTx), the industry is still in an exploratory phase with some diverging views; however, a consensus is gradually emerging that DTx products require medical device approval. Indeed, whether under the strictest or broader definitions, obtaining medical device certification lends greater credibility to digital therapeutics. According to VCBeat’s statistics based on publicly available information, as of November 2022, the National Medical Products Administration (NMPA) had issued a total of 30 Class II medical device certificates that meet the definition of digital therapeutics, marking the year with the highest number of DTx medical device approvals to date.

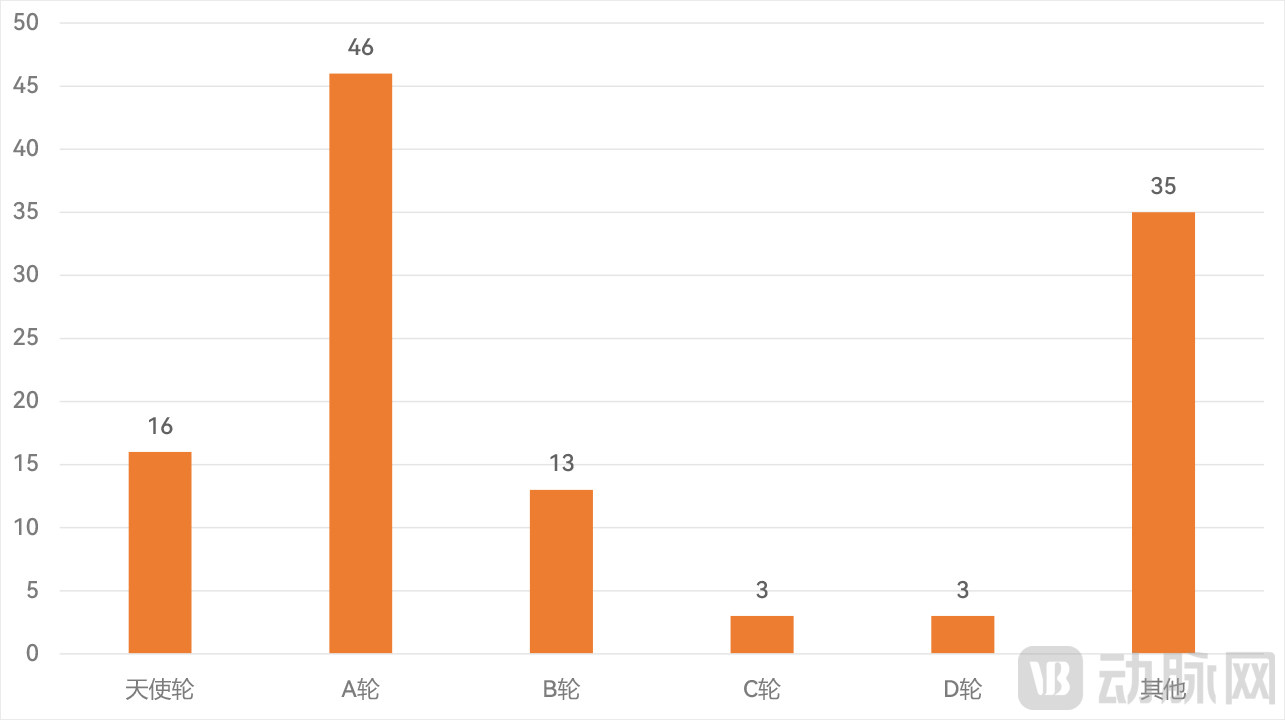

Furthermore, the digital health sector demonstrated robust performance in the primary market in 2022. According to incomplete statistics from VCBeat Orange Data, a total of 108 companies in the digital health field—primarily focused on health informatics, artificial intelligence, and digital therapeutics—that met the criteria of this white paper completed 125 financing transactions in 2022. Among them, 16 companies secured more than one round of funding within the year.

Among these, 81 financing events disclosed their investment amounts, with a total financing volume reaching RMB 4.29 billion. Twenty-five of these financing rounds involved amounts greater than or equal to RMB 100 million, accumulating to a total of RMB 3.475 billion. This accounts for as much as 81% of the total reported financing amount, fully reflecting the “80/20” principle.

Distribution of Digital Health Financing Rounds in China by Stage in 2022

In terms of financing rounds, Series A funding events were the most frequent, with a total of 46 occurrences; other financing rounds followed closely with 35 instances; angel and Series B rounds accounted for 16 and 13 occurrences, respectively; while Series C and D rounds were the least common, each with only 3 occurrences. The distribution of financing rounds clearly indicates that the majority of digital health companies remain in the early to mid-stage development phase.

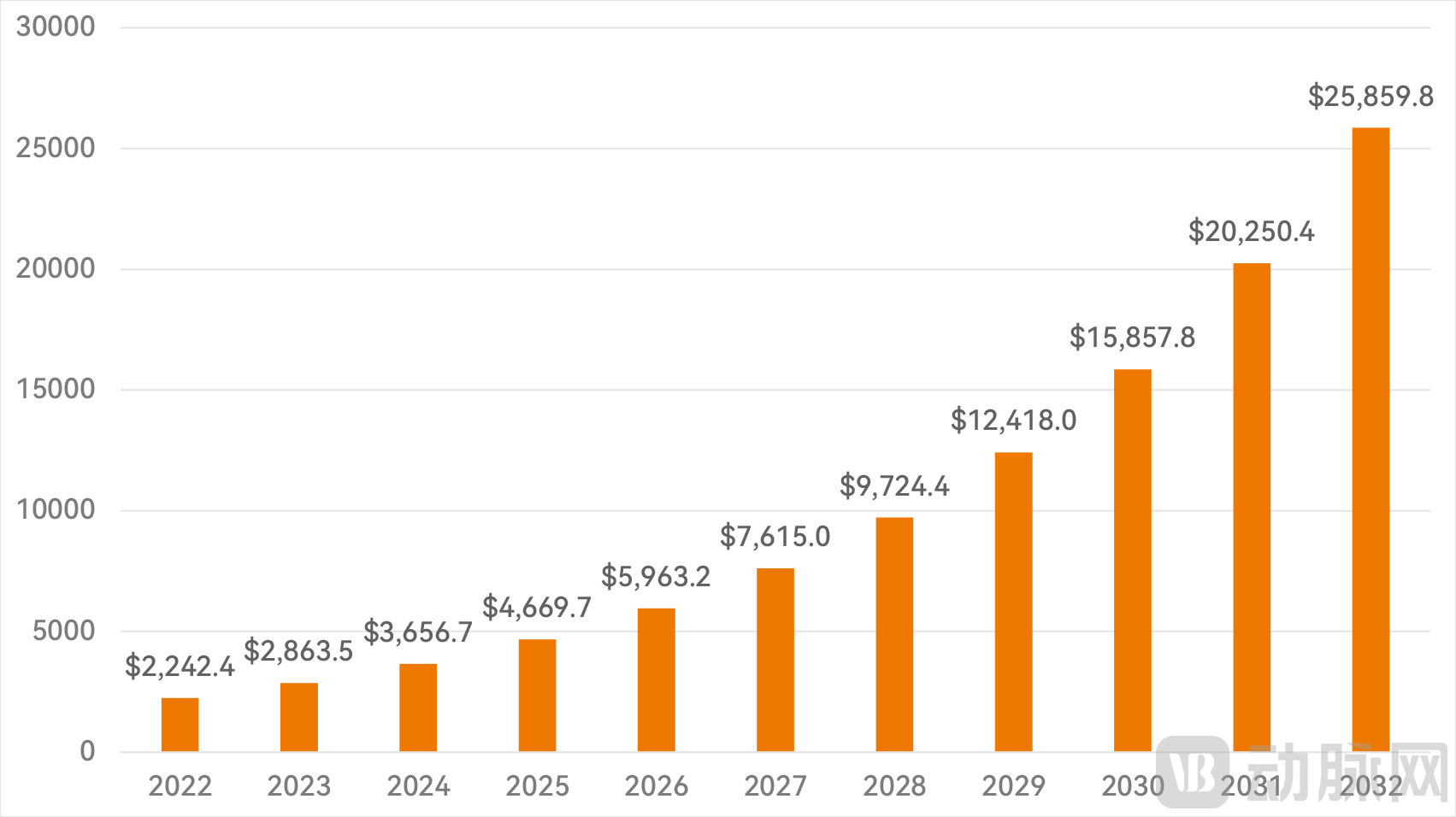

Global Digital Health Market Size Forecast (2022-2032) (USD 100 Million)

Although the market size of digital health varies depending on statistical methodologies, and its broad scope makes estimation challenging, statistical agencies generally highly recognize the enormous market size and significant development potential of digital health. According to data from Future Market Insights, the global digital health market size was $224.24 billion in 2022, and it is projected to grow at a compound annual growth rate (CAGR) of 27.7% from 2022 to 2032, reaching a substantial market size of $2,585.98 billion by 2032. This undoubtedly represents a massive market.

In 2022, digital healthcare witnessed significant growth. On one hand, it received increasing impetus driven by policy support. On the other hand, advancements in digital technologies such as big data, 5G, the Internet of Things (IoT), and AR/VR have enabled the implementation of digital healthcare solutions across a growing number of medical application scenarios. By examining key terms, we can outline the development trajectory of digital healthcare in 2022.

In terms of informatization, cloud architecture and the Internet are driving a new phase of digital transformation.

Currently, after years of policy-driven efforts, public tertiary hospitals have basically achieved the goal of in-hospital informatization, and the focus of informatization construction is gradually shifting towards regional and primary care informatization.

Cloud-based HIS based on the SaaS model is gradually emerging as a new approach to information technology construction in primary healthcare institutions. While delivering high-quality products and services, cloud HIS helps primary healthcare facilities control their IT costs by eliminating the need for substantial capital investment in hardware infrastructure such as server rooms and servers, which is required by traditional HIS. Furthermore, cloud HIS demonstrates advantages in data interoperability and connectivity, leading to its increasingly widespread application in regional healthcare informatization initiatives.

For example,NeusoftThe Xiangyang Health Information Technology Capacity Enhancement Project, which we undertook, is a typical representative of this process. The project vertically integrates medical institutions across four levels—city, county, township, and village—and horizontally covers various groups throughout the city, including residents, healthcare professionals, and administrative personnel. It is the first project in China to adopt a prefecture-level integrated design model for the development of business systems in secondary and lower-tier healthcare institutions.

Built on a cloud-native architecture,Huazhuo TechnologyProposed the concept of a “HaaS (Health as a Service)” platform for regional healthcare informatization. The platform comprises “One Cloud” (a regional healthcare hybrid cloud), “One System” (a cloud-native, hospital-wide information system), and “One Platform” (a healthcare big data platform), enabling coverage of business systems across all types of healthcare institutions in the region and achieving interconnectivity, collaboration, and shared data exchange.

In 2022, the construction and upgrading of public internet hospitals accelerated significantly. Currently, public internet hospitals account for approximately 70% of all internet hospitals in China, holding an absolute advantage in terms of quantity; the operations of public internet hospitals, represented by large Grade A tertiary hospitals, have also begun to gain momentum. On the other hand, with the adjustment of epidemic prevention policies at the end of the year, a surge in demand for remote consultations and prescriptions has become inevitable, and greater importance has been attached to internet hospital information systems than ever before.

For example, such asNaiteruiA typical internet hospital information system, similar to the Internet Hospital System, facilitates enterprise process optimization and enables patients to access medical care with ease by providing services such as appointment scheduling, online outpatient payment, text-and-image consultations, video consultations, remote consultations, and AI-assisted diagnosis. It integrates all patient-centric convenience services across the entire care continuum—pre-consultation, during consultation, and post-consultation—thereby helping enterprises and hospitals accelerate their transformation and upgrading in the “Internet + Healthcare” sector.

2022: AI Imaging Achieves New Breakthroughs

In 2022, AI-powered medical imaging products approved for market experienced a surge, both in terms of supported indications and underlying imaging modalities. The emergence of innovative solutions—such as CT-based detection of intracranial hemorrhage, head and neck CTA analysis, multi-type thoracic fracture assessment on CT, colonoscopy assistance, CT and MRI evaluation of cerebral ischemia, fundus imaging for glaucoma, chest X-ray screening for tuberculosis, and X-ray detection of intracranial aneurysms—has further expanded the scope of AI-assisted diagnosis, demonstrating the vast potential of digital healthcare.

Meanwhile, AI-based medical imaging devices for multiple indications are gradually emerging. Whether by further improving already-approved single-indication products to support additional indications, or by designing multi-indication support from the outset, it is evident that the application of AI across multiple indications will be the future trend.

Currently, AI is extending to the grassroots level, truly realizing the goal of leveraging digital healthcare to support primary care. For example,Jiufeng MedicalIn response to the current reality that X-ray equipment remains the dominant imaging modality in primary healthcare institutions, we have developed an AI-assisted evaluation software for pulmonary tuberculosis (TB) chest X-rays. This software not only secured China’s first Class III medical device certification for AI-based pulmonary tuberculosis diagnosis but also marked the first Class III certification for any AI-driven X-ray solution targeting lung diseases, thereby providing a breakthrough solution to address the weaknesses in TB prevention and control at the primary care level.

Furthermore, in addition to assisting physicians with disease triage, assessment, and diagnosis, the empowering and accelerating effect of AI on existing products should not be underestimated. For example,Shentou MedicalSupMR generally leverages AI technology to directly enhance the performance of existing MRI scanners, accelerating imaging processes while improving image quality and resolution. It seamlessly integrates with a wide range of current MRI systems, enabling product deployment and automated image enhancement without disrupting radiologists’ daily workflows. Such AI-enabled products are becoming increasingly prevalent and have gained widespread adoption among healthcare institutions.

Digital Therapeutics Advance into Clinical Practice, Taking Root and Flourishing Across More Indications

Digital therapeutics are gradually gaining attention and increasingly penetrating the core of clinical medical practice. By leveraging the integration of various digital technologies, digital therapeutics have gradually broken away from the stereotype of being effective only for specific indications, demonstrating potential across a broader range of conditions. Although still in its early stages, its robust vitality and nearly limitless possibilities cannot be ignored.

For example,BOTONG HEALTHAs China’s first digital health-enabled pain management platform, it has deployed multiple products targeting both cancer-related and non-cancer pain. The company has launched four product pipelines, including multidimensional pain assessment, wearable digital therapeutics for in-hospital and out-of-hospital pain management, and fracture risk prediction for patients with bone metastases or osteoporosis. Furthermore, it has pioneered the novel “PAINICU” concept and established the CPDP system to empower healthcare institutions.

Digital therapeutics can also effectively empower the diagnosis and rehabilitation of speech disorders, such asBethelThe DREAM Digital Therapeutics System for Pediatric Language Assessment and Intervention, an independently developed solution, is the first digital software tool for pediatric language assessment and intervention to be included in the National Health Commission’s “Specifications for the Diagnosis and Treatment of Mental Disorders.” Its preliminary efficacy in guiding personalized interventions was also the first to be published in the Chinese Journal of Pediatrics.

AsSumianOnline CBT-I digital therapeutics, similar to traditional CBT-I, accommodate multiple scenarios both within hospitals and at home. Patients can complete the treatment remotely and independently at home, effectively reducing time and transportation costs, thereby providing practical support for the implementation of CBT-I in China. Meanwhile, through collaborations with renowned tertiary hospitals, it offers integrated management solutions that enable personalized, one-to-many remote care services, resulting in higher management efficiency.

Bingpian Medical TechnologyA digital therapeutic targeting environmental allergen and irritant assessment and intervention for respiratory allergic diseases has established a comprehensive commercial closed-loop across in-hospital prescriptions, over-the-counter (OTC) channels, and the consumer market. Furthermore, by co-establishing a Digital Therapeutics (DTx) R&D platform and a real-world study data application platform with hospitals, it has laid a solid foundation for continuous research and development.

IoT Applications Make Smart Out-of-Hospital Health Management a Growing Reality

Out-of-hospital management, such as home- and community-based health management, has also ushered in a wave of practical implementation driven by breakthroughs in technologies like the Internet of Things (IoT). In 2022, application scenarios once considered merely ambitious blueprints—such as out-of-hospital chronic disease and health management, and smart health communities—have become reality. By leveraging the integrated use of various medical and healthcare IoT devices, entirely new models of out-of-hospital health management have even been created.

such asBOE Health TechnologyIts digital-intelligent health and elderly care solution focuses on multi-scenario health management in community and home settings, achieving smart connectivity among “people, devices, and services” through a health IoT platform and facilitating the construction of digitalized healthy communities. It also organically integrates professional medical services with community health management scenarios, enabling high-quality medical services to benefit community residents via internet and IoT technologies.

Elderly individuals, previously considered to have a natural divide with digital technology, have also achieved breakthroughs through the integration of the Internet of Things (IoT) and artificial intelligence. For example,Jianjian Home DoctorBy further strengthening its AI-powered Digital Health Brain, the core capability of its product ecosystem, the company has achieved mobile, tag-based, and intelligent management of elderly health conditions. It seamlessly connects family doctors, pharmaceutical and medical device suppliers, and integrated medical-rehabilitation-care service providers with elderly residents, family physicians, hospitals at all levels, and regulatory authorities.

The Wave of Technological Convergence Sweeps Through Digital Health Subsectors

Finally, the continuous advancement of digital technology is often a key factor enabling digital healthcare to be implemented in an increasing number of application scenarios. In particular, digital therapeutics rely heavily on a wide range of digital technologies, such as wireless networks, sensors, microprocessors and integrated circuits, artificial intelligence, cloud computing and big data, and VR/AR/MR technologies. The integration of these digital technologies with digital healthcare was also a major highlight of the digital healthcare landscape in 2022.

In the VR field,Ningdong MedicalThe psychological rehabilitation training software for specific phobias creates a virtual reality scenario, allowing physicians to select tasks of appropriate intensity based on the patient’s condition. This helps patients identify and correct irrational anxiety and fear, counteract avoidance responses, and undergo corresponding relaxation training, ultimately achieving therapeutic effects that alleviate anxiety and fear symptoms and improve quality of life.

In the field of AR,ShukangFor children aged 6–12 with delayed brain development, ADHD, and ASD, a digital therapeutic solution designed for comprehensive improvement of psychological, cognitive, and physical functions has been introduced. This solution incorporates AR interactions to enhance the adherence and engagement of remote interventions. Furthermore, by leveraging machine vision and auditory technologies—such as gesture recognition, eye-tracking, voiceprint identification, and movement safety and risk modeling—it helps patients ensure movement safety and achieve performance standards, thereby guaranteeing treatment efficacy.

Qiyi MedicalthenIn 2022, it consecutively won major awards in artificial intelligence competitions. Leveraging its AI R&D capabilities and a clinical data resource pool of nearly 10 million patients, Qiyi Medical has developed the Oneark platform, a machine learning algorithm framework. By integrating artificial intelligence, Qiyi Medical is focusing on addressing key pain points such as low public awareness, inadequate diagnosis and treatment, and insufficient patient management for chronic obstructive pulmonary disease (COPD).

In addition, such asFudong MusculoskeletalThe “Yue Action” remote rehabilitation system, centered on digital therapeutics and IoT sensors and empowered by artificial intelligence, can play a significant role in the rehabilitative treatment of orthopedic conditions and sports injuries. It enables integrated, precise rehabilitation delivery through interconnected devices, patients, and institutions, breaking through spatial and personnel constraints to provide remote rehabilitation support for physicians, therapists, and patients.

These explorations are undergoing a qualitative leap driven by quantitative accumulation. “Indeed, there was no path on the ground to begin with; but as more people walked, a path emerged.” These pioneering innovators in digital health are blazing a trail for those who follow through their concrete actions, thereby establishing a “Chinese model” for digital healthcare.

"2022 Annual Innovation White Paper on Digital Healthcare" Table of Contents

The above is an excerpt of the main content of the report. The complete framework of the report is as follows. Scan the QR code to add our assistant and obtain the full report; if you have already added the assistant, please proactively reach out to request it.