EQRx Files Prospectus to Disrupt Global Pharma with 'Me-Too' Strategy and $36.5B Valuation After 18 Months

GV

Google's Investment Fund

EQRx

New Drug Research and Development, Manufacturer

In January 2020, a “disruptor” claiming it would “mass-produce and launch patented new drugs at low prices” emerged, causing a major stir at the J.P. Morgan Healthcare Conference.

“Professional Architect of Biotech Companies” Alexis Borisy founded EQRx (NASDAQ: EQRX), a pharmaceutical company pursuing a “me-too” strategy. EQRx, short for Equal Quality Rx, aims to introduce drug pipelines as a “fast follower,” launching new competitive drugs within existing therapeutic categories and selling them at prices lower than those of patented drugs, thereby acting as a disruptive “catfish” in the pharmaceutical market.

Is the goal to produce cheaper generic drugs? No, EQRx has greater ambitions. At the company’s inception, Alexis Borisy declared that over the next decade, he aims for EQRx to initiate the development of 50 different experimental drug candidates, launch its first drug within five years, and bring 10 drugs to market within ten years.

EQRx’s future plan is to create a global buyer’s club that attracts public buyers (such as healthcare insurance systems) and individual buyers with homogeneous, low-priced patented drugs. By connecting global healthcare product suppliers and demanders, it aims to build a globally networked platform company to address the most significant contradiction in the global healthcare sector—poor patient access to innovative drugs.

Five years have passed halfway. What has EQRx experienced so far? Where does it stand now?

It secured $800 million in cumulative funding across two rounds, completed a SPAC merger and listing with an oversubscription of $1.8 billion, and advanced five pipeline candidates into Phase III clinical trials.

The drug’s market launch plan may be realized ahead of schedule next year, but it is still too early to claim that EQRx has already validated its business model...

Alexis Borisy, who founded 15 star companies including Blueprint Medicines, Relay Therapeutics, and Foundation Medicine, and has 25 years of entrepreneurial and investment experience in the biotechnology sector, quickly made EQRx a new favorite in the capital markets.

EQRx Financing Information Summary (Source: Crunchbase)

Prior to completing its SPAC transaction, the company had closed two rounds of financing, raising a total of approximately $700 million. Major institutional investors—including Google Ventures, ARCH Venture Partners, Arboretum Ventures, and Casdin Capital—participated consecutively in both rounds. Notably, after securing a $200 million Series A financing at its inception, EQRx doubled that amount in its Series B, raising $500 million. This trajectory unequivocally demonstrates the strong capital market favor enjoyed by EQRx.

After securing $200 million in Series A financing, the company targeted cancer indications with poor accessibility to innovative therapies and rapidly initiated pipeline acquisitions. In July 2020, EQRx spent $100 million to acquire exclusive rights for the development, manufacturing, and commercialization of Hansoh Pharmaceutical’s third-generation EGFR-TKI, aumolertinib, outside China. Three months later, EQRx also acquired the ex-Greater China rights to Sugemalimab, a PD-L1 inhibitor, and Nofazinlimab, a PD-1 inhibitor, from CStone Pharmaceuticals (HKEX: 2616).

The pipelines of two Chinese pharmaceutical companies propelled EQRx into a period of rapid growth. In January of the following year, the company completed a $500 million Series B financing round. Six months later, on August 6, 2021 (Eastern Time), the company announced that it had entered into a definitive business combination agreement with the life sciences SPAC company CM Life Sciences III, Inc. (NASDAQ: CMLTU). The transaction generated $1.8 billion in cash proceeds at a price of $10 per share, significantly exceeding the original target of $1.2 billion. The SPAC deal saw strong subscription demand, valuing EQRx at $3.65 billion.

Over the two years from its founding to its IPO, this “me-too” strategy company has remained in the spotlight. Some believe that once EQRx’s business model proves viable, it will bring transformative benefits to patients, health insurance payers, and commercial insurers. However, many experts and pharmaceutical companies argue that such a model is unlikely to succeed easily, with some even dismissing it as little more than prolonged hype.

But since the financing and IPO did indeed take place, what story did EQRx tell the capital markets?

In September 2021, Alexis Borisy publicly stated that three-quarters of the company’s valuation, amounting to $2.7 billion, was derived from CStone Pharmaceuticals’ PD-L1 inhibitor, sugemalimab, a novel monoclonal antibody targeting the PD-L1 ligand for the treatment of non-small cell lung cancer (NSCLC). Mr. Borisy argued that, given lung cancer is one of the most prevalent cancers worldwide and the global market for PD-(L)1 inhibitors is projected to exceed $500 billion, the $2.7 billion valuation is conservative, assuming sugemalimab captures 15% of the global market based on its sales rights outside Greater China.

By reducing the price of sugemalimab to one-third that of existing drugs, annual sales could reach approximately $1.5 billion. Including upfront and milestone payments of up to $1.3 billion, Alexis Borisy views this as a highly cost-effective deal.

Similarly, Alexis Borisy believes that Hansoh Pharmaceutical’s third-generation EGFR-TKI (epidermal growth factor receptor tyrosine kinase inhibitor), Aumolertinib, can generate annual sales of approximately $500 million in a market sized at around $5 billion, while the cost to acquire this pipeline was less than $200 million.

Combined with the development plan to launch 10 products over 10 years, $3.65 billion does not seem like an excessively high starting valuation for EQRx.

So, what secret weapon does EQRx have that the hundreds-of-billions-dollar biopharmaceutical industry lacks?

“The greatest technological innovation is usually the solution process, not the product.”

Take Amazon as an example: by building a different type of retailer from the ground up and embedding technology throughout the process, it was able to achieve faster product delivery at lower prices and higher margins. What EQRx is doing is reimagining how drugs are developed, tested, and commercialized by redesigning the “system” itself.

Global Buyer’s Club (Image from the official EQRx website)

EQRx has established a platform—the “Global Buyers Club”—in collaboration with payers, distributors, health system partners, and other stakeholders. This platform aims to coordinate and positively incentivize the entire innovative drug ecosystem by increasing the availability of high-quality, low-cost patented innovative medicines, thereby enhancing patient access to these therapies and helping the “Buyers Club” achieve its goal of reducing expenditure. The greater the accessibility of innovative drugs and the broader the range of such products involved, the more significant the cost savings for the “Buyers Club” and the more pronounced the promotional effect on the “ecosystem.”

EQRx’s vision was soon validated. At the J.P. Morgan 40th Annual Healthcare Conference on January 10, President and Chief Operating Officer Melanie Nallicheri announced that the platform had established collaborations in 2021 with multiple institutions and health authorities, including Blue Cross and Blue Shield of North Carolina, Horizon Healthcare Services in North America, and the UK’s National Health Service, covering a population of approximately 70 million.

In early 2022, the company will welcome heavyweight partners such as CVS, the largest drug retailer in the United States; Geisinger, the most comprehensive integrated healthcare service provider in the United States; and Blue Cross Blue Shield of California. These collaborations will expand EQRx’s population coverage to approximately 180 million people, directly targeting a market worth hundreds of billions of U.S. dollars.

In addition to EQRx providing high-quality innovative drugs at lower prices to “Buyers Club” members, the commercial support that members offer to EQRx is also highly enviable. CVS has incorporated EQRx’s medications into its pharmacy retail operations, pharmacy benefit management services, and health plans, helping EQRx establish regional influence in the United States. Meanwhile, CVS has also enhanced its oncology services by simplifying prescription processes, promoting cancer screening, and identifying eligible clinical trial patients, thereby providing multi-dimensional and robust data support for the advancement of EQRx’s clinical pipeline. Geisinger, renowned for the quality of its care services, operates a hospital system, health plans, and provider networks. It will provide project support to EQRx both during early-stage clinical trials and in post-marketing studies.

By transforming scientific research risks into execution risks, EQRx enables early engagement across the entire healthcare value chain and eliminates friction between systems through in-depth collaboration. After reassuring partners with its “high quality at low cost” promise, the innovative drugs that EQRx places on its platform have become the primary focus of attention.

EQRx projects that by the mid-2030s, global pharmaceutical spending will reach $1 trillion, with half—$500 billion—driven by oncology and immune-mediated inflammatory diseases such as rheumatoid arthritis and psoriasis.

From 2020 to 2021, EQRx in-licensed more than 10 asset pipelines, half of which were in clinical trial stages and the other half in early-stage R&D, covering approximately one-fifth of the “$500 billion” market. In 2022, the company plans to select pipelines from biopharmaceutical companies worldwide, doubling its investment portfolio to over 20 assets and expanding coverage to a broader range of disease categories.

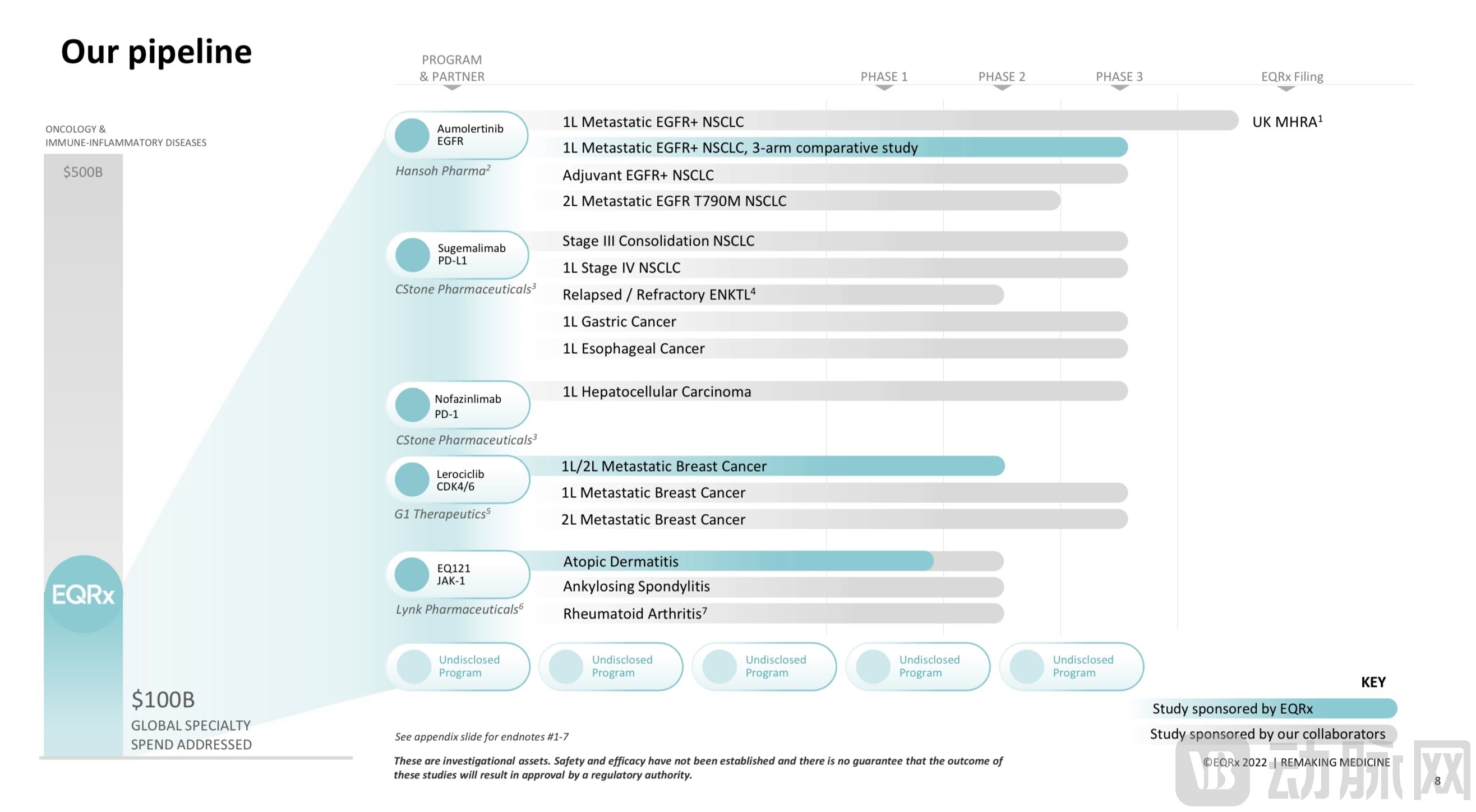

EQRx’s Latest Pipeline Update (Image from EQRx’s Official Website)

According to EQRx’s currently disclosed pipeline data, among the 15 indications under investigation across five drug pipelines in mid-to-late-stage clinical trials, one Phase III clinical trial has been completed, and nine Phase III clinical trials are ongoing (one of which is sponsored by EQRx).

EQRx’s financial report for the third quarter of this year indicates that a U.S.-led, randomized, three-arm Phase IIIb clinical trial is currently underway. This trial evaluates the safety and efficacy of aumolertinib in combination with chemotherapy versus aumolertinib and osimertinib reference groups as first-line treatment for EGFR-mutated non-small cell lung cancer (NSCLC). The results from this trial may support the use of both aumolertinib combination therapy and monotherapy, with the potential to seek U.S. approval in 2027. Meanwhile, the UK Medicines and Healthcare products Regulatory Agency (MHRA) is reviewing the Marketing Authorization Application (MAA) for this drug in the treatment of EGFR-mutated NSCLC, and the company plans to submit the MAA to the European Medicines Agency (EMA) in 2023.

Lerociclib, a novel oral small-molecule cyclin-dependent kinase 4/6 (CDK4/6) inhibitor licensed from G1 Therapeutics, is undergoing multicenter Phase II clinical trials as a first- and second-line treatment for metastatic breast cancer, with a U.S.-led Phase III clinical trial for advanced endometrial cancer planned to commence in the first half of 2023.

What, then, of sugemalimab, which was once touted as accounting for three-quarters of the company’s market capitalization? In February this year, Richard Pazdur, Director of the Office of Oncologic Diseases at the FDA, stated that sugemalimab had undergone clinical trials only in China by CStone Pharmaceuticals, lacking evidence from “multicenter clinical trials,” which made it difficult for regulators to accept the relevant application. Furthermore, the drug had only completed efficacy comparisons with chemotherapy and had not been tested against approved PD-(L)1 immunotherapies in non-small cell lung cancer (NSCLC). Consequently, the FDA ultimately rejected the marketing application for the drug and requested a redesign of the relevant Phase III clinical trials.

EQRx, which had been advancing rapidly and undeterred by challenges, now appears to have hit a bottleneck.

EQRx's stock price plummeted sharply in the wake of this event.

In February, when the Director of the FDA’s Oncology Center of Excellence cited a lack of “multicenter clinical trials,” the stock price fell consecutively for one month from $4.90 to $2.80 per share. After eight months of sluggish growth and volatility, the third-quarter financial report released in November disclosed that the FDA had rejected the marketing application for Sugemalimab. The stock price subsequently declined continuously from $5.56 to $2.15 (as of December 27), hitting its lowest level since EQRx’s listing.

EQRx stated that, in light of FDA feedback, the company will discontinue commercialization efforts for sugemalimab in the treatment of NSCLC in the United States, but will continue to seek marketing approval in countries outside the U.S. based on limited data. The company plans to submit a Marketing Authorization Application (MAA) to the MHRA by the end of the year and will file an MAA with the EMA in 2023 for sugemalimab in the treatment of stage IV NSCLC.

On the other hand, EQRx will continue to discuss with the FDA the approval application for Sugemalimab in the treatment of relapsed or refractory ENKTL. Previously, Sugemalimab had received Breakthrough Therapy Designation from the FDA for ENKTL in 2020.

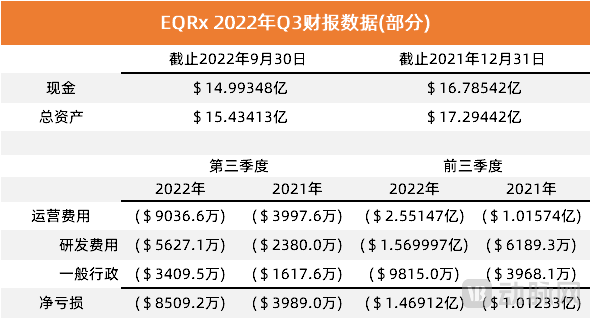

Despite EQRx’s interventions to mitigate the outcome from multiple angles, the recent turmoil has still resulted in substantial losses. According to the third-quarter financial report, the company’s R&D expenditure this year was 2.5 times that of the same period in 2021, and the increase in R&D personnel has correspondingly raised administrative expenses. Considering only the cash outlay, the company’s losses amounted to tens of millions of dollars, not to mention the abandoned U.S. non-small cell lung cancer (NSCLC) market.

Source: EQRx Third Quarter 2022 Financial Report

Fortunately, the company currently holds approximately $1.5 billion in total assets, including cash and short-term investments, which is expected to provide sufficient capital resources for its anticipated operations through 2028.

In the upcoming phase of rapid pipeline expansion, the company will face heightened execution risks. With the setback of its “cornerstone” pipeline, EQRx needs to promptly draw lessons from this experience to mitigate corresponding risks as much as possible.

What may have disrupted the original tranquility of this “Buyers’ Club” blueprint?

At the core of EQRx’s entire business logic lies the strategy of acquiring high-quality pipelines and bringing them to market at low prices. Consequently, determining which pipelines to acquire and how to execute their clinical development will be critical issues that EQRx must carefully consider and address.

EQRx primarily targets developed markets, where drug resources are abundant and, consequently, expectations for efficacy, safety, innovation, and cost-effectiveness are significantly higher. First, identifying high-quality drugs within a broad pipeline of innovative candidates that not only deliver superior efficacy but also possess the potential to rapidly capture market share requires the team to have strong and precise capabilities in pipeline value assessment.

Secondly, innovative drug development is also an empirical science that requires teams with extensive experience in clinical trials and regulatory approvals. Teams must be proficient in the regulatory registration procedures and key considerations associated with this highly regulated phase, and design and conduct clinical trials in accordance with the requirements of regulatory agencies such as the U.S. FDA.

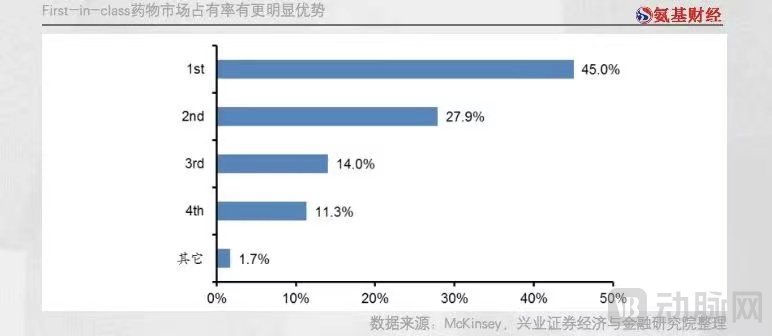

(Image from Aminocaijing)

In addition, the order of market entry plays a critical role in determining market share. Although innovative drugs in the United States currently command higher prices, First-in-Class drugs achieve an average market share of 45%. The primary reason is that prescribing decisions are made by physicians, who generally do not readily switch medications, particularly in the oncology market. Therefore, when evaluating pipeline in-licensing opportunities, teams must also consider first-mover advantage—specifically, whether the drug can capture a larger share of the market.

The above logic can be similarly applied to most innovative pharmaceutical companies adopting the License-in business model. In China, where small and medium-sized innovative drug developers currently predominate, fierce competition in the sector has made License-out an increasingly popular avenue for commercialization.

In 2021, BeiGene announced a collaboration and license agreement with global pharmaceutical giant Novartis for the development, manufacturing, and commercialization of its self-developed anti-PD-1 antibody drug, tislelizumab, in multiple countries, with a total transaction value exceeding $2.2 billion. According to available data, tislelizumab is the first domestically produced PD-1 monoclonal antibody to initiate overseas clinical trials and currently has the largest number of global clinical trials among such agents. At the time the agreement was reached, tislelizumab had already launched 15 registrational clinical trials worldwide, enrolling more than 7,700 patients globally, including approximately 2,500 patients from 20 countries and regions outside mainland China.

Tislelizumab was positioned for the global market from the outset of its development, and its comprehensive “multi-center clinical trial” strategy enabled it to set a record for the highest licensing transaction value for a single drug product in China. The cases of BeiGene and EQRx exemplify both sides of the argument, underscoring the critical importance of “global deployment” and “multi-center clinical trials” to the License-out business model.

If you’re asking whether EQRx’s business model can truly work, I believe it is still worth watching.

Driven by the fierce competition in the innovative drug pipeline, grounded in the genuine demands of “buying clubs,” and inspired by the noble vision of “ensuring patients have access to high-quality, low-cost innovative drugs.”