Cryofocus Biotech Successfully IPOs on HKEX with Backing from Hillhouse and YuanSheng: Exploring Growth Opportunities for Domestic Ablation Products

Cryofocus

Minimally Invasive Interventional Cryotherapy Device Developer

On December 30, Cryofocus successfully completed its initial public offering (IPO) on the Hong Kong Stock Exchange, with an offer price of HK$18.90 per share and a total market capitalization of approximately HK$4.4 billion.

Cryofocus, based in Shanghai, specializes primarily in the field of minimally invasive interventional cryotherapy. Its core products include bladder cryoablation systems, endoscopic anastomosis clips, and cardiac cryoablation products.

Cryofocus Lists on the Hong Kong Stock Exchange

Previously, MicroPort EP, the main competitor of Huitai Medical and Cryofocus, which focus on the cardiac electrophysiology sector, has successfully listed on the STAR Market. The IPOs of these three companies will undoubtedly bring more confidence to the cardiac electrophysiology market. According to a research report by Frost & Sullivan, the market share of domestically produced electrophysiological medical devices in China was only 9.6% in 2020, with a localization rate of less than 10%. Domestic manufacturers still need to find more new growth points.

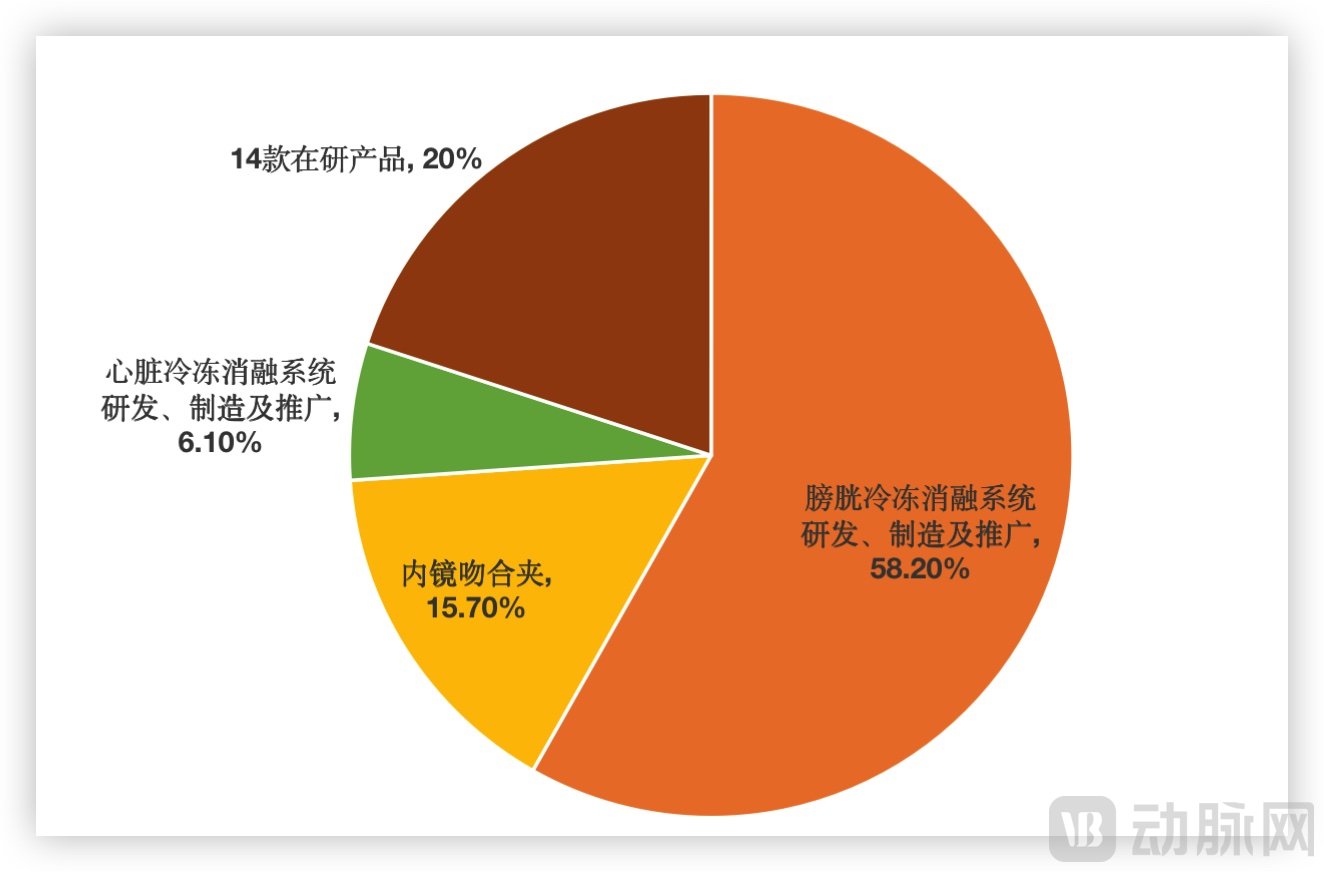

Proportion of Raised Funds Invested by Cryofocus in Key Projects, Source: Prospectus

Cryofocus intends to allocate approximately 65% of the proceeds from this public offering to the research and development, promotion, and manufacturing of its cryoablation system products, while 20% of the funds will be used to advance its existing 14 projects under development.

In the electrophysiology field, MicroPort EP has adopted a strategy centered on radiofrequency ablation combined with 3D mapping systems, while also expanding into cryoablation. Cryofocus, by contrast, has pursued a cryoablation-focused path while simultaneously laying the groundwork for pulsed field ablation (PFA) technology. With the advent of PFA, attention toward cryoablation has waned. How can new growth drivers be identified in the future? Clues may be found in Cryofocus’s prospectus.

Cryofocus was established in 2013. During its first six years, the company focused exclusively on cryoablation therapy for atrial fibrillation within the field of cardiac electrophysiology.

Atrial fibrillation (AF) is one of the most common clinical arrhythmias. According to “Prevalence and Risk of Atrial Fibrillation in China: A National Cross-Sectional Epidemiological Study,” the age-standardized prevalence of AF in China is 1.6%, with an estimated 20 million affected individuals. Severe conditions caused by AF, such as thromboembolic events (e.g., stroke, mesenteric artery embolism, and limb artery embolism) and heart failure, pose significant health risks.

The electrophysiological treatment of atrial fibrillation is marked by a “battle between ice and fire,” representing the competition between cryoablation and radiofrequency ablation technologies. Cryofocus has bet on cryoablation.

From a technical perspective, radiofrequency ablation works by raising the temperature to dehydrate abnormal atrial tissue structures, leading to coagulative necrosis and thereby restoring regular heart rhythm. In contrast, cryoablation utilizes a catheter integrated with a cryoablation system to deliver ablative energy to the abnormal tissue structures, causing a rapid drop in temperature around the ablation target site. This blocks electrical signal conduction at specific locations, thus achieving the therapeutic goal.

Number of Atrial Fibrillation Ablation Procedures, Source: Prospectus

Cryoablation was previously regarded as an innovative procedure. Compared with radiofrequency ablation, cryoablation enables simultaneous treatment of all target sites in a single session, making the procedure simple and efficient and, to some extent, reducing operative time. However, current indications for cryoablation are limited. Consequently, radiofrequency ablation remains the mainstream approach in actual market practice, while cryoablation occupies a relatively niche position.

Although cryoablation technology has been in existence for many years, it was not until 2010 that Medtronic launched the world’s first cryoballoon system for treating paroxysmal atrial fibrillation, which remains the only such product marketed in China. Nevertheless, Medtronic holds no more than a 10% share of the domestic market, which continues to be dominated by Johnson & Johnson and Abbott in the field of radiofrequency ablation.

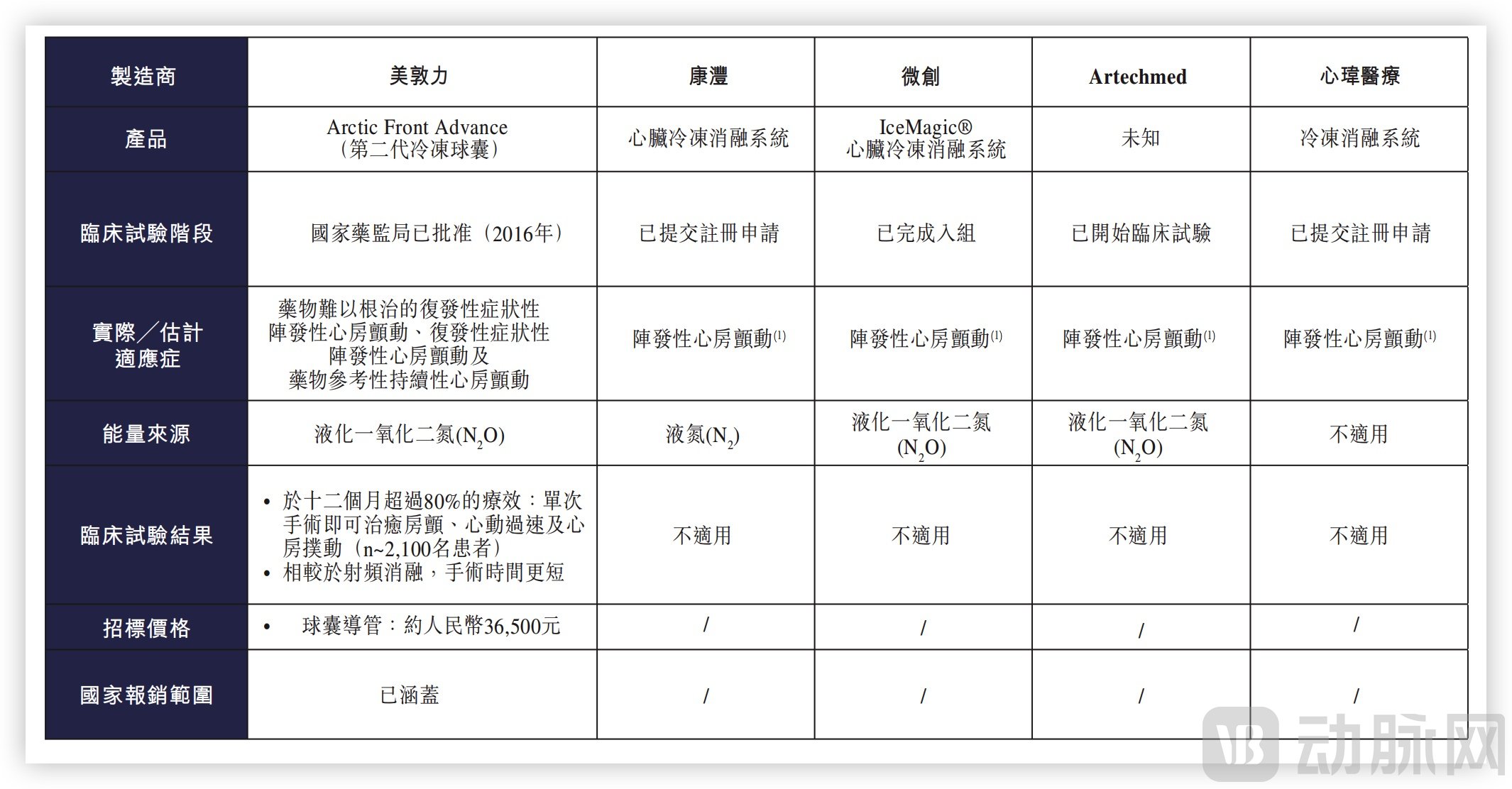

Domestic Atrial Fibrillation Cryoablation Products, Image Source: Prospectus

According to the prospectus, four domestic companies currently have atrial fibrillation cryoablation products in clinical trials. However, instead of facing traditional competitors using radiofrequency ablation, they may now be confronting pulsed field ablation (PFA). Medtronic and Johnson & Johnson had their related products approved for clinical research in 2020, while Boston Scientific has also made strategic moves through acquisitions.

Pulsed Field Ablation (PFA) technology treats atrial fibrillation by selectively ablating myocardial tissue through the mechanism of irreversible electroporation. The PFA system can precisely eliminate pathological cells without damaging surrounding critical structures such as nerves and blood vessels, thereby enhancing therapeutic safety and efficacy while reducing surgical complications. Furthermore, the PFA system offers advantages including rapid ablation speed, ease of operation, and high controllability. Consequently, pulsed field ablation is regarded as the future direction of development in the field of electrophysiology.

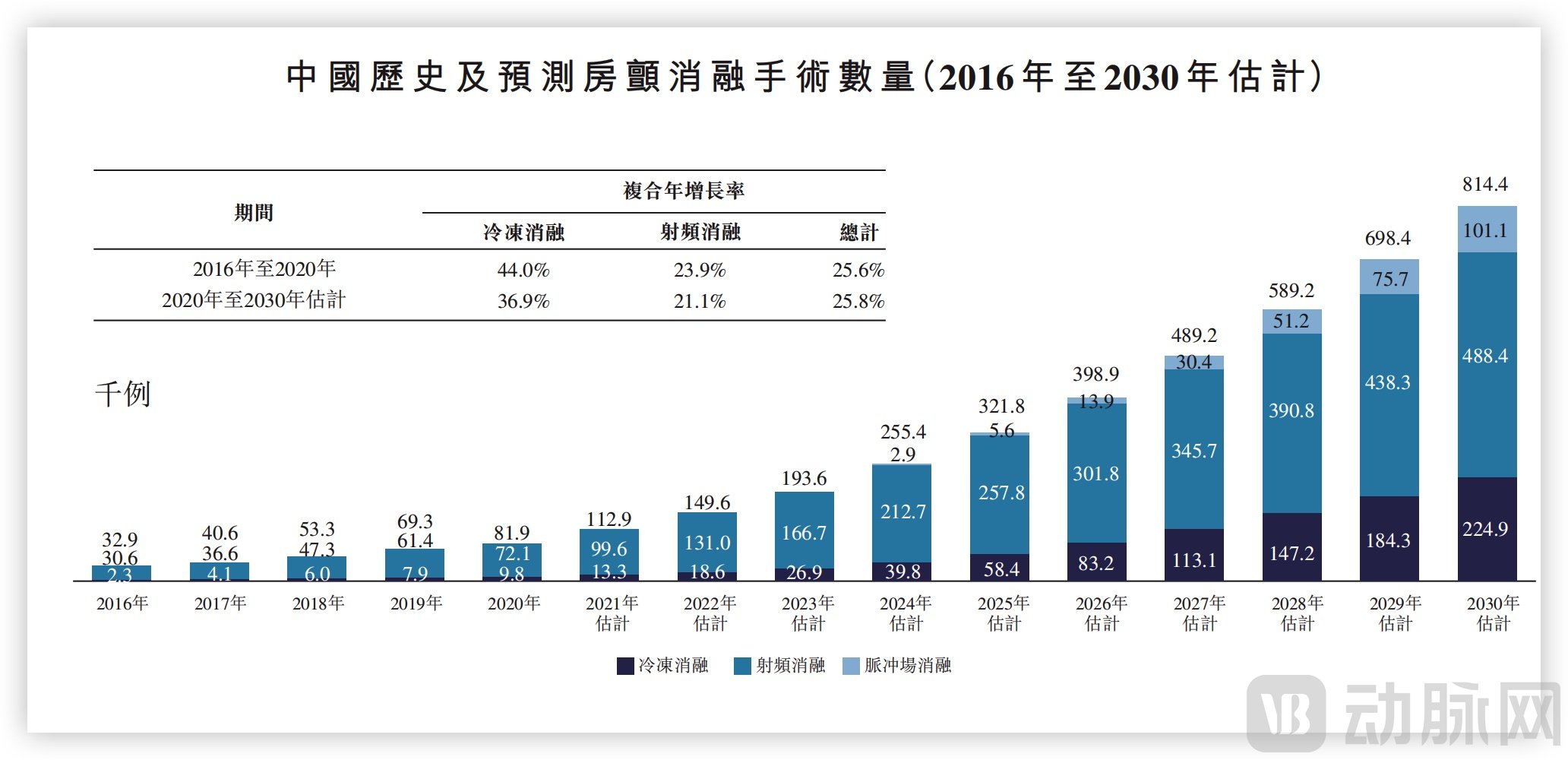

Even without the disruption caused by pulsed field ablation (PFA), it would still be challenging for cryoablation to prevail in the “battle of ice and fire.” According to Cryofocus’s prospectus, a total of 81,900 atrial fibrillation ablation procedures were performed in China in 2020, among which only 9,800 were cryoablation cases, while radiofrequency ablation accounted for 72,100 cases, holding an absolute advantage.

Therefore, in addition to deploying new technologies such as PFA, Cryofocus has also completed the establishment of a minimally invasive cryoablation treatment platform by acquiring Shengjiekang, which specializes in tumor cryoablation and endoscopic/laparoscopic minimally invasive procedures. This move has enabled cryoablation technology to enter a highly promising niche market—the tumor interventional ablation market.

Beyond the traditional triad of cancer treatment—surgery, chemotherapy, and radiotherapy—interventional therapy has gradually emerged as the fourth major modality for tumor treatment, driven by advances in imaging technology. Currently, tumor ablation has become the fastest-growing segment within interventional procedures.

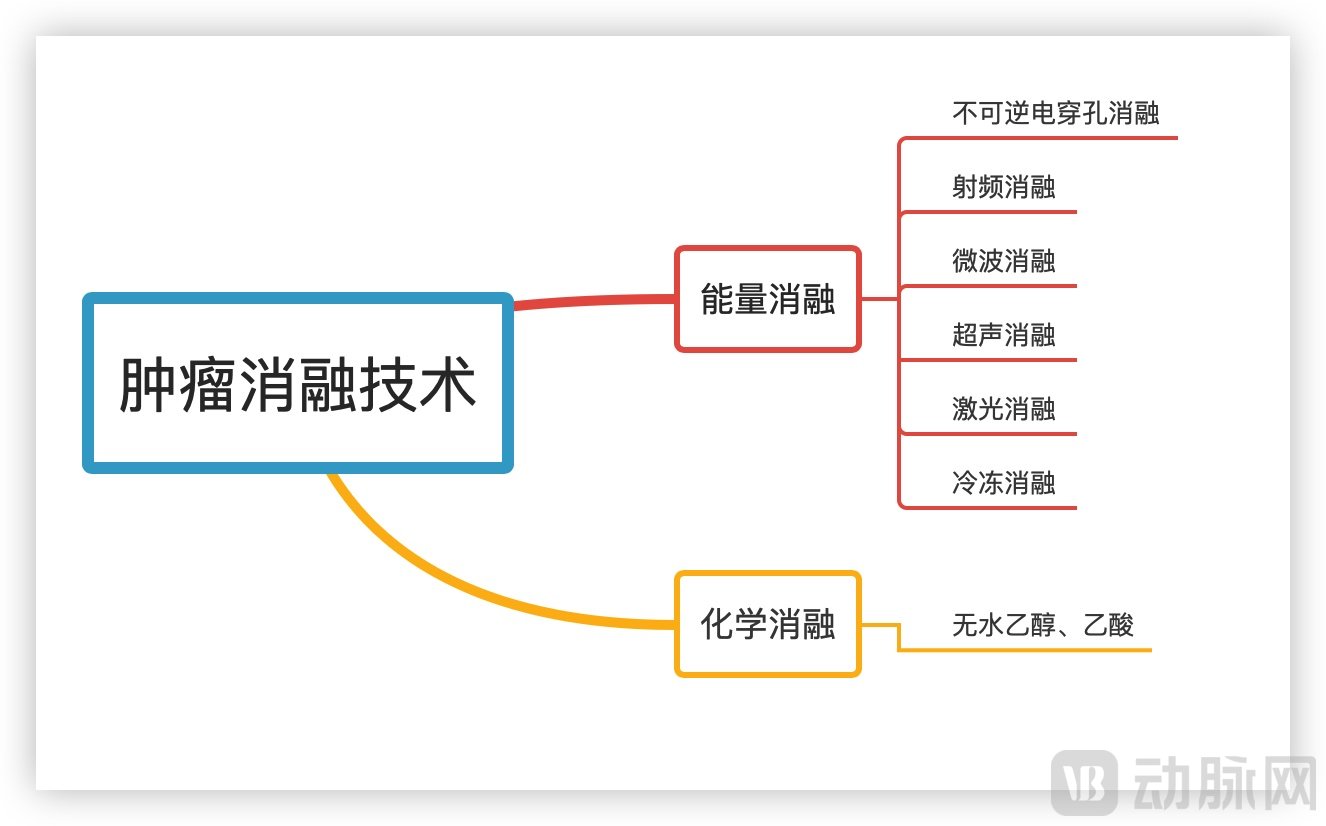

Tumor ablation technology is a minimally invasive therapeutic technique that inactivates cancerous tissue by percutaneous puncture or transnatural orifice access to the tumor site under the guidance of imaging equipment such as ultrasound, CT, and MRI. Currently, the most commonly used tumor ablation methods are chemical ablation and energy-based ablation.

Tumor Ablation Roadmap

Tumor ablation technology is currently primarily applied in the treatment of liver cancer, lung cancer, pulmonary nodules, breast tumors, uterine fibroids, and thyroid nodules. Microwave and radiofrequency ablation are the mainstream techniques in the current market. Among these, radiofrequency ablation has been established as a first-line curative treatment for early-stage liver cancer. Meanwhile, with advancements in microwave technology and the introduction of cooled-tip electrodes, the clinical application of microwave ablation continues to expand, gaining recognition from clinicians for its safety and efficacy.

Cryoablation can be used to treat pain and other symptoms associated with the spread of abnormal tissue. When the risks of surgical tumor resection are prohibitively high, cryoablation balloons can be employed to alleviate cancer-related symptoms and serve as part of a comprehensive treatment regimen. Therefore, cryoablation is beneficial for patients who are not candidates for surgical tumor removal.

Compared with traditional thermal ablation, cryoablation technology offers the advantages of minimal invasiveness, simple operation, clear ablation margins that allow physicians to easily delineate the ablation zone, and a high safety profile.

Cryogenic ablation products for tumors marketed in China are categorized into two types: percutaneous and transnatural orifice. Unlike competitors who opt for percutaneous intervention, Cryofocus has chosen the transnatural orifice approach. The cryoballoon can be inserted through a resectoscope or cystoscope sheath, thereby preventing bladder wall injury and reducing the risk of tumor dissemination.

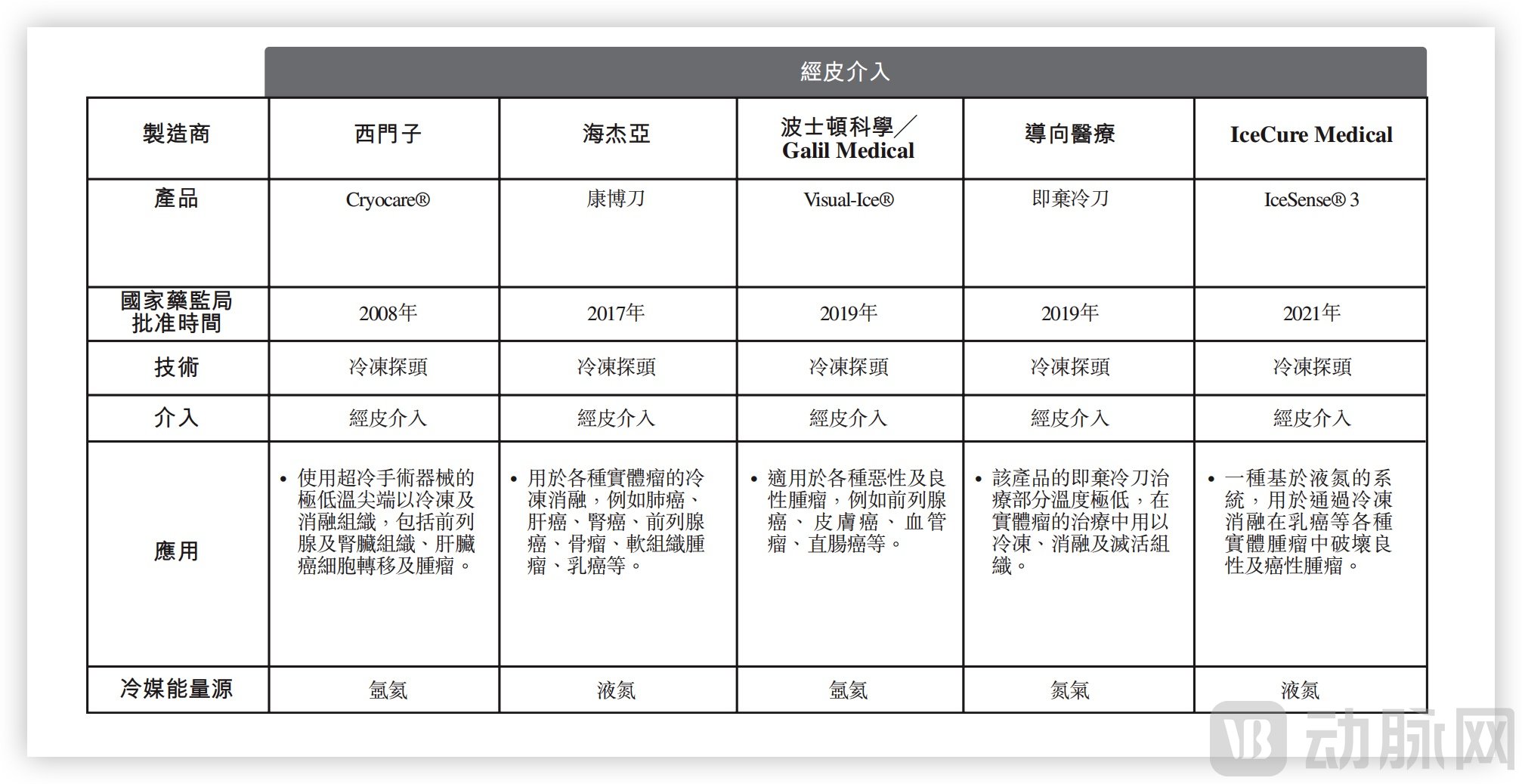

Currently, products commercialized in China utilize cryoablation catheters that are percutaneously inserted into the body to freeze and thaw target tissues, a procedure involving incisions on the skin. Key players in the percutaneous cryoablation market include Siemens, Haijieya, Boston Scientific, Guided Medical, and IceCure Medical. The indications for these companies’ products are broad, covering breast, prostate, kidney, and liver cancers, among others.

Tumor Cryoablation Products Currently on the Market in China, Source: Prospectus

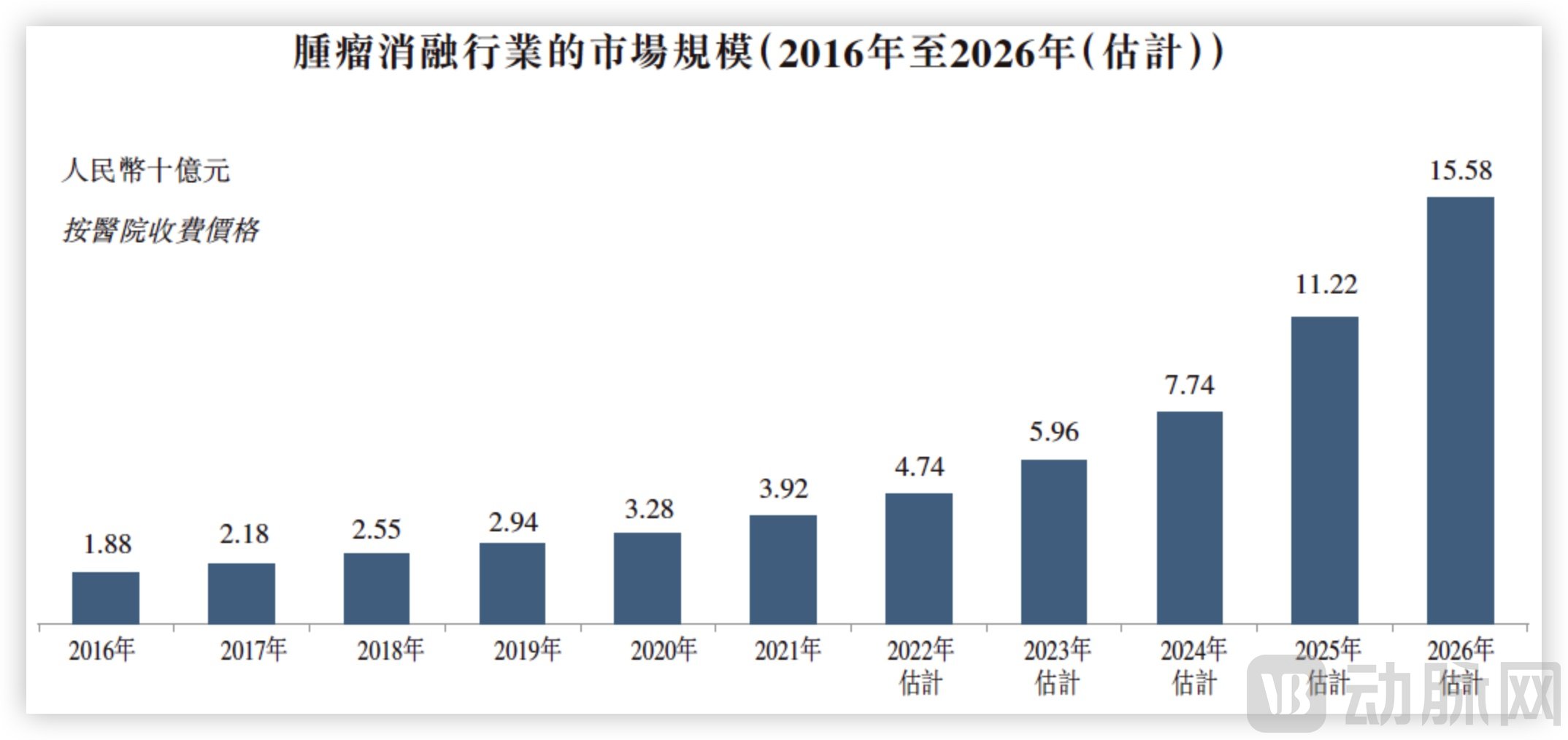

According to Frost & Sullivan, the market size of China’s tumor ablation industry (calculated based on hospital charging prices) increased from RMB 1.88 billion in 2016 to RMB 3.92 billion in 2021. Given the continuous rise in the number of newly diagnosed cancer patients in China and the increasing adoption of ablation therapy in hospitals, minimally invasive procedures are being accepted by a growing number of physicians and patients, making ablation treatment one of the common therapeutic modalities for tumors.

Meanwhile, with the further popularization of tumor ablation therapy and its increasing coverage by medical insurance across more regions in China, the market size of China’s tumor ablation industry will continue to maintain an upward trend. It is expected to reach RMB 15.58 billion by 2026, representing a compound annual growth rate (CAGR) of 34.7% from 2022 to 2026.

Market Size of the Tumor Ablation Industry, Data Source: Frost & Sullivan

Another major application scenario for cryoablation is in respiratory intervention. Currently, interventional cryoablation for the respiratory system includes two categories: spray cryotherapy and bronchial cryoballoon ablation. The currently approved products for interventional respiratory cryoablation are from Erbe and Beijing Kulang. Through bronchoscopy, cryoprobes can be used to remove foreign bodies, mucus plugs, necrotic tissue, and benign and malignant tumors, as well as to perform biopsies.

According to Frost & Sullivan data, the global market size for interventional cryotherapy catheters in respiratory medicine has grown steadily from USD 2.5 million in 2016 to USD 4.5 million in 2020, representing a compound annual growth rate (CAGR) of 16.4%, and is projected to expand rapidly to USD 2,032.3 million by 2030.

The market size of interventional cryotherapy catheters for respiratory diseases in China is also on an upward trend. According to Frost & Sullivan, it grew from RMB 0.9 million in 2016 to RMB 2.1 million in 2020, with a compound annual growth rate (CAGR) of 24.4%. With the development of new technologies, this market is expected to expand further. The market size of interventional cryotherapy catheters for respiratory diseases in China is projected to reach RMB 109.8 million by 2025.

Although cryoablation has a wide range of application scenarios, similar to the field of cardiac electrophysiology, its application in other areas also faces competition from ablation using other energy sources.Cryoablation technology must identify the disease indications and products that best leverage its advantages to achieve a breakthrough.。

Currently, Cryofocus has established a deep presence in the two major fields of natural orifice endoscopic surgery and vascular intervention, creating a comprehensive product portfolio.

Cryofocus’s product pipeline comprises various cryoablation systems and surgical consumables, including two core products—the Bladder Cryoablation System and Endoscopic Anastomotic Clips—14 other products under development, and six commercialized non-cryoablation products. Among these, four products have been recognized as “Innovative Medical Devices” by the National Medical Products Administration (NMPA) or its provincial counterparts; this group includes the two core products: the Cardiac Cryoablation System (currently under registration application) and the Cryofocus Cryoablation System (in clinical trials).

Cryofocus’s Current Product Pipeline Layout. Source: Prospectus

Core Products: Bladder Cryoablation System and Endoscopic Anastomosis Clips, both have received marketing approval from the National Medical Products Administration (NMPA). Among them, the endoscopic anastomosis clip was commercialized in October, while the bladder cryoablation system is scheduled for commercialization in December. In addition, the indications targeted by the current R&D pipeline represent a substantial market opportunity, and with the progressive commercialization of these products, there is significant growth potential in the future.

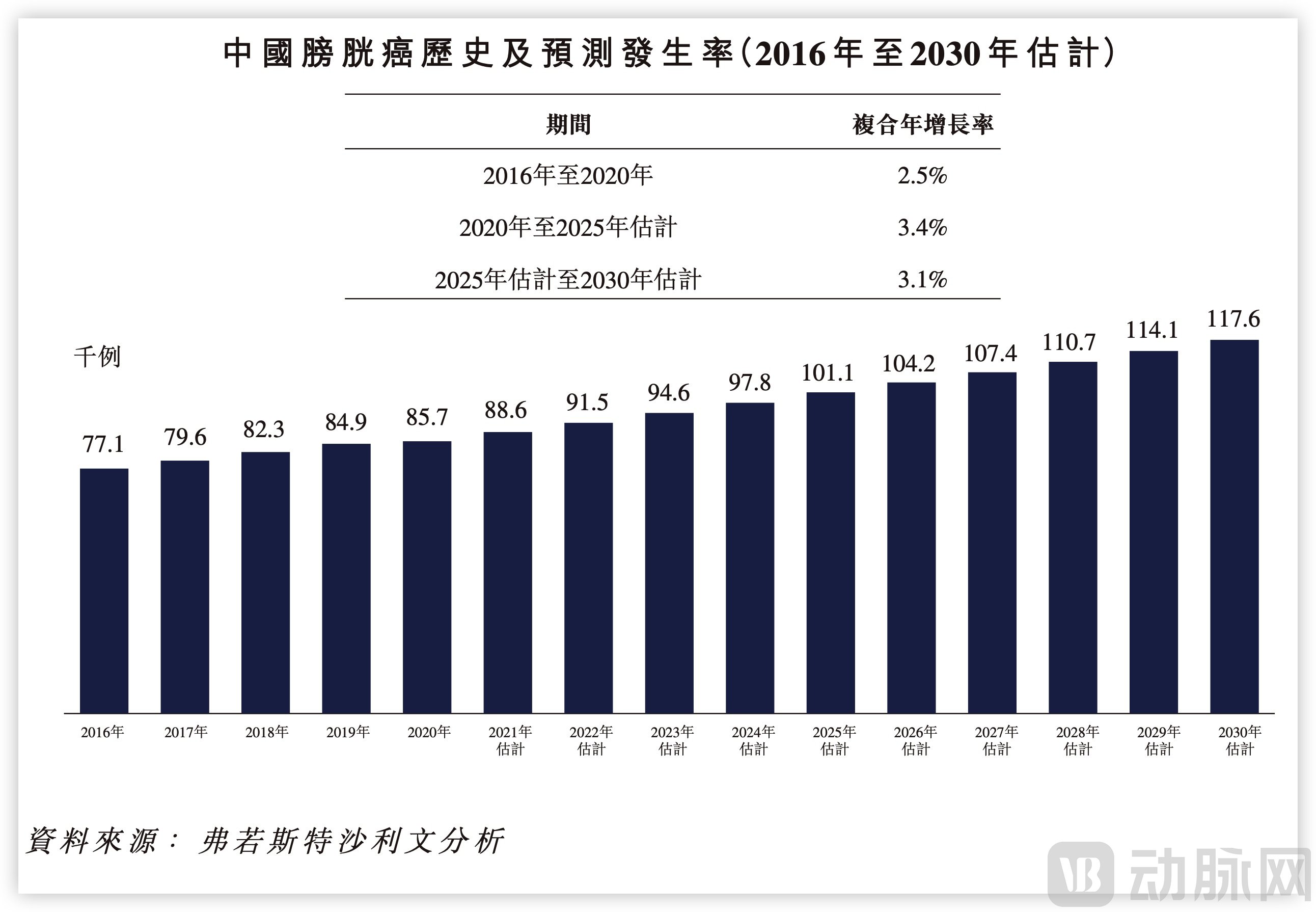

Bladder cryoablation systems can serve as an adjuvant therapy to transurethral resection of bladder tumor (TURBT) for the treatment of bladder tumors, offering multiple potential benefits. These include enhanced capability to reduce residual tumor burden, ease of use, physician-friendly learning process, a relatively short learning curve, shorter operative time, and a low incidence of complications. According to Frost & Sullivan projections, by 2030, approximately 45% of patients undergoing TURBT will receive adjunctive cryoablation therapy, with an estimated 44,900 procedures performed.

Bladder Cancer Incidence Forecast in China, Source: Prospectus

Cryofocus’s other core product, the endoscopic anastomotic clip, is used for the closure of soft tissues in the digestive tract and is indicated for perforations during gastrointestinal endoscopic procedures and full-thickness endoscopic suturing following natural orifice transluminal endoscopic surgery (NOTES). The endoscopic anastomotic clip received approval from the Zhejiang Provincial Medical Products Administration in August 2022 and commenced commercialization in October 2022.

Endoscopic clipping systems primarily consist of two types: endoscopic clips that pass through the instrument channel and super-wide-span clips. According to the prospectus, there are currently 32 commercialized endoscopic clips in China, with only three being super-wide-span clips. As the registration certificate for one of these three products has expired, Cryofocus’s super-wide-span clip faces only one actual competitor.

Currently, super-range clips are in the early stages of adoption and account for a relatively small share of the overall endoscopic clip market; however, they possess significant growth potential. Compared with conventional endoscopic clips delivered through the endoscope’s working channel, super-range clips offer several advantages, such as the ability to close larger wounds. In procedures involving the closure of large wounds, conventional endoscopic clips typically require a greater number of clips, whereas fewer super-range clips are needed under similar circumstances, resulting in relatively shorter procedure times. Consequently, these devices are increasingly recommended by clinical guidelines and academic publications. Frost & Sullivan projects that by 2030, the market size for super-range clips will reach RMB 544.9 million, with their share of the overall endoscopic clip market rising significantly to 48.5%.

Another key product under development is the cardiac cryoablation system., treats paroxysmal atrial fibrillation by freezing and destroying abnormal cardiac tissue responsible for arrhythmias during minimally invasive procedures. The Company has completed the multicenter clinical trial of its cardiac cryoablation system, issued the final clinical trial report in May 2022, and submitted the registration application to the National Medical Products Administration (NMPA) in July 2022. It is expected that the NMPA will approve this investigational product in or around the second quarter of 2023. There is only one cryoablation device approved for commercialization in China for the treatment of atrial fibrillation. Based on publicly available information, Cryofocus is one of the four companies in China conducting clinical trials on cryoablation devices for the treatment of atrial fibrillation, and it is the only company using low-pressure liquid nitrogen for cryoablation.

Furthermore, Cryofocus will alsoCryoablation for Renal Denervation (RDN), and in early December, it received Breakthrough Device Designation from the U.S. FDA. The system is primarily indicated for patients with resistant hypertension. As the world’s first cryoablation-based renal denervation system (Cryofocus RDN System), Cryofocus has previously passed the Special Review Procedure for Innovative Medical Devices of China’s NMPA and holds independent intellectual property rights worldwide. Featuring advantages such as 360° circumferential ablation, precise ablation positioning, and minimal endothelial damage, Cryofocus represents another significant advancement in domestically developed, original cardiovascular medical devices.

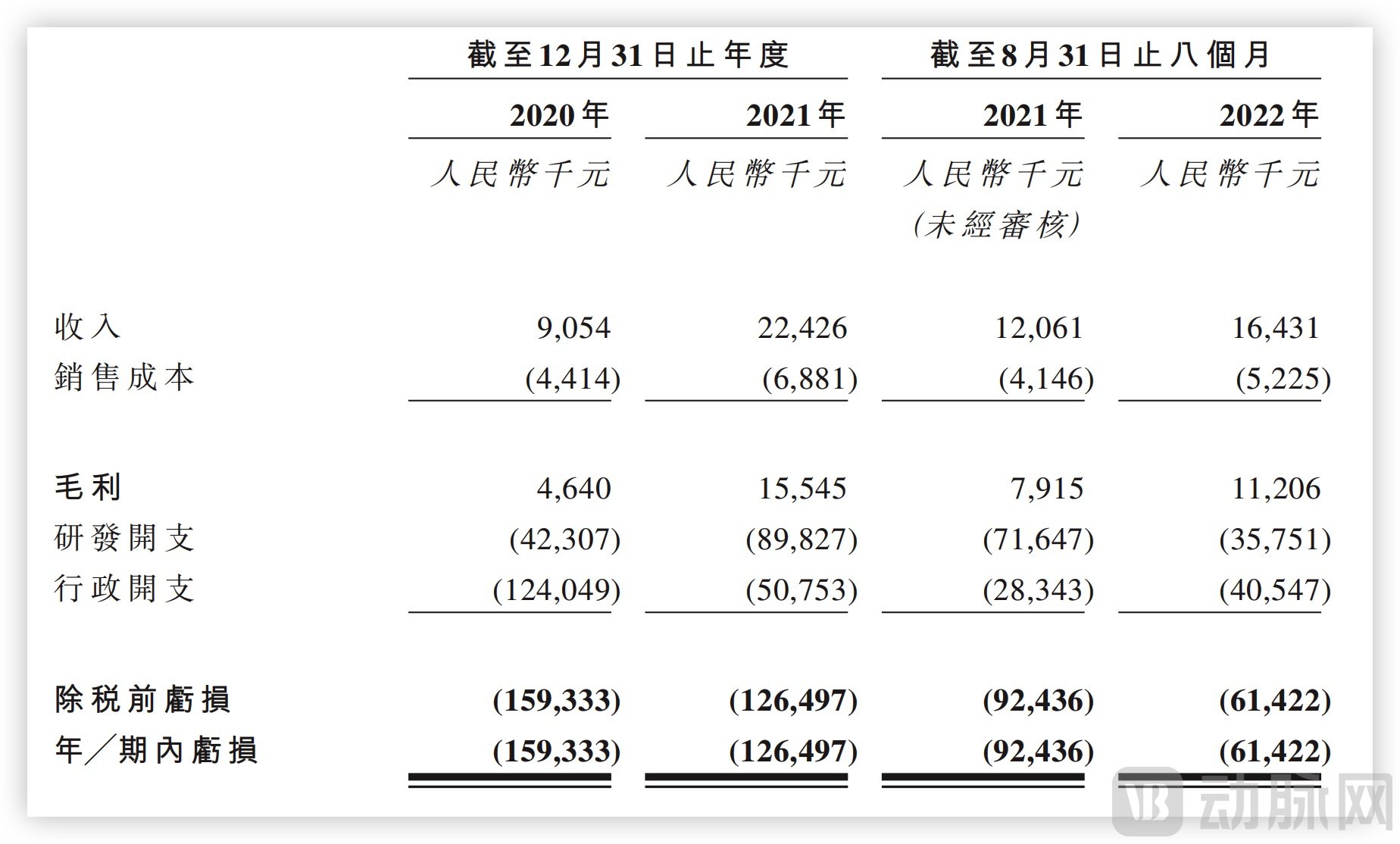

From 2020 to 2021, Cryofocus generated revenues of RMB 9.054 million and RMB 22.426 million, respectively, representing a year-on-year growth of 147.7%. In the first eight months of 2022, the company achieved revenues of RMB 16.431 million, a year-on-year increase of 36.2%. In recent years, revenue has been primarily driven by six commercialized surgical consumable products, mainly including pulmonary nodule localization needles and single-port multi-channel laparoscopic access systems. These two flagship products accounted for over 90% of total revenue.

Cryofocus’s Revenue Data in Recent Years, Source: Prospectus

As Cryofocus’s core products are still in the early stages of commercialization, the company as a whole remains unprofitable. Furthermore, with the majority of its pipeline still in the R&D phase, substantial investment in research and development is required. In 2020, 2021, and the first eight months of 2022, Cryofocus’s R&D expenditures amounted to RMB 42.307 million, RMB 89.827 million, and RMB 35.751 million, respectively, representing 467.3%, 400.5%, and 217.6% of its total revenue. As the commercialization of its core products progresses smoothly, the company’s performance is expected to enter a phase of rapid growth.

Prior to its IPO, Cryofocus secured investments from several renowned institutions, including Proxima Ventures, Hillhouse Capital, Yuansheng Venture Capital, and FutureX Capital. Among these, Yuansheng Venture Capital holds a 5.39% stake through Suzhou Xinjianyuan Phase II Venture Capital; Proxima Ventures holds a 3.53% stake via Hangzhou Proxima and a 3.32% stake via Suzhou Proxima; and Hillhouse Capital holds an 8.48% stake. These investors were drawn by the company’s vast growth potential.

The electrophysiology atrial fibrillation ablation market is experiencing rapid growth, with imports accounting for 90% of the share, leaving ample room for domestic companies. However, the dominant positions of Johnson & Johnson and Abbott remain difficult to challenge in the near term. Meanwhile, Medtronic and Boston Scientific are strengthening their presence in this field by investing significant revenue into cardiac electrophysiology. Furthermore, the pulsed field ablation products from Medtronic and Boston Scientific are expected to receive regulatory approval in China.

In other words, domestic enterprises face both opportunities and challenges. In addition to Cryofocus, MicroPort EP MedTech, and Huitai Medical, which are already listed, as well as Jinjiang Electronics, which has launched its IPO, and Xuanyu Medical, Antike, Xinuopu, Aikemai, and Zhouling Medical, which have each secured over RMB 100 million in financing over the past year or so, all these companies need to establish their own comprehensive solutions to ensure they remain competitive in the future market landscape.

Cryofocus operates in another promising sector: tumor ablation. Currently, approximately 300,000 tumor ablation procedures are performed annually in China. Thermal ablation, primarily utilizing microwave and radiofrequency technologies, accounts for 80% of the entire ablation market, while cryoablation represents approximately 10%. The domestic production rate for microwave ablation devices is relatively high. In the primary market, companies such as Haijieya, Nanjing Yigao, and Ruidi Biology have also secured substantial financing, suggesting that this field is poised to produce more publicly listed companies.

For Cryofocus, which specializes in minimally invasive interventional cryoablation therapy, sustaining competitiveness in the rapidly evolving healthcare market requires continuously advancing the clinical development and commercialization of its pipeline products, persistently innovating core and supporting technologies, and further expanding its product portfolio and indications based on its technology platform.