2022 Precision Diagnostics White Paper: Which Segment—Early Screening, MRD, Mass Spectrometry, or At-Home Testing—Will Drive the Next Growth Wave?

Amidst a capital winter and the transmission of pressure from the secondary market to the primary market, 2022 was a year of ups and downs for China’s precision diagnosis and treatment sector, marked by both excitement and disillusionment. Some niche segments, after years of abundant funding, exuberance, and frenzy, have entered a period of calm; industry bubbles are gradually dissipating, and companies are focusing more intently on strengthening their core competencies. Other segments, having lain dormant for many years, have stepped into the spotlight, entering a phase of capital returns and industrialization harvest. Still other segments, long constrained by challenges in standardized development, are being pushed closer to a breakout point by sustained high-level policy attention.

Some ride the waves, some break new ground, and others lie in wait. As we bid farewell to the ups and downs of 2022, we welcome a new year marked by vibrant growth and flourishing opportunities. What significant changes occurred in the precision diagnosis and treatment industry in 2022? How can we seize the new opportunities underlying these shifts? Which niche sectors deserve continued attention in 2023? VCBeat surveyed 15 precision diagnosis and treatment companies and interviewed 20 industry experts to jointly explore the answers.

(Note: To obtain the full report, please scan the QR code to add our assistant. If you have already added them, please initiate your inquiry.)

Below is a brief overview of the white paper.

In 2022, China’s precision diagnosis and treatment industry continued to deepen its development, emerging as a hotspot for capital investment and policy attention, with continuous advancements in technology, products, and commercialization.

Financing: Emerging Sectors and Differently Positioned Companies Are Favored by Capital

According to VCBeat’s statistics, the precision diagnosis and treatment sector completed a total of 106 financing rounds in 2022, with the total amount exceeding RMB 8.531 billion. The overall financing performance lagged behind previous years, primarily due to the prolonged COVID-19 pandemic, dynamic changes in the macroeconomic environment, and volatility in the pharmaceutical secondary market, which adversely impacted primary market investments.

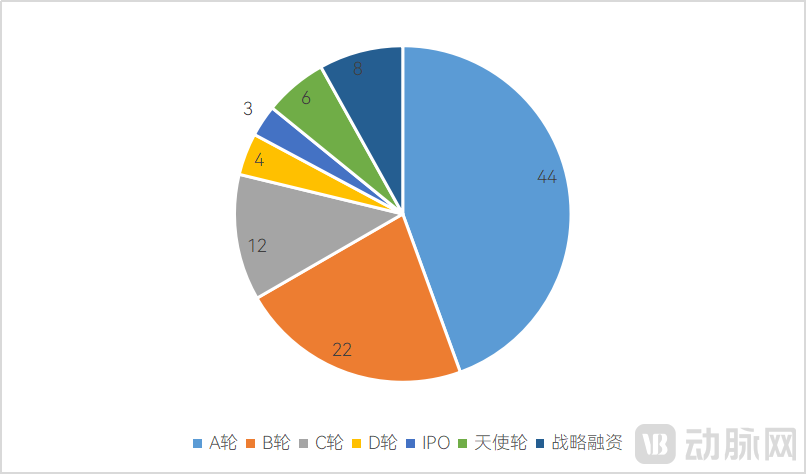

From the perspective of financing rounds, investments in the precision diagnosis and treatment sector in 2022 were skewed toward early stages, predominantly Series A. Financing from angel rounds to Series B accounted for 69% of the total. These companies are primarily concentrated in emerging subsectors without established market leaders, such as clinical mass spectrometry, microfluidic point-of-care testing (POCT), single-cell sequencing, single-molecule detection, and early cancer screening. They have entered the market by leveraging these emerging tracks and adopting differentiated positioning strategies.

Distribution of Financing Rounds for Precision Diagnosis and Treatment Companies in 2022

In terms of financing amounts, despite the capital winter, the strong continue to get stronger, with a significant number of funding rounds exceeding RMB 100 million. Platform-based enterprises, pathogen metagenomic sequencing, single-cell analysis, early cancer screening, upstream gene sequencing, and clinical mass spectrometry remain highly sought-after sectors.

Overall, the precision diagnostics and therapeutics sector is witnessing a changing of the guard, with some players exiting while others enter. Genomics remains the primary focus of capital investment, but emerging forces such as mass spectrometry, single-molecule detection, proteomics, metabolomics, and multi-omics are rapidly rising. In the future, the capital market will become more rational, adopting a diversified perspective on precision diagnostics and therapeutics by focusing on new technologies and application scenarios, as well as opportunities for industry chain integration, thereby promoting the healthy development of the sector.

Policy: Acceleration of Volume-Based Procurement and Standardization of Laboratory-Developed Tests (LDTs)

There has always been a clear demand in clinical practice and scientific research for large-panel and whole-exome sequencing tests. However, under the traditional regulatory framework, such innovative projects have not been fully utilized. The introduction of LDT-related policies in multiple regions in 2022 has been a significant boon to the industry, enabling companies to select appropriate business models without expending substantial time and resources on registration and certification.

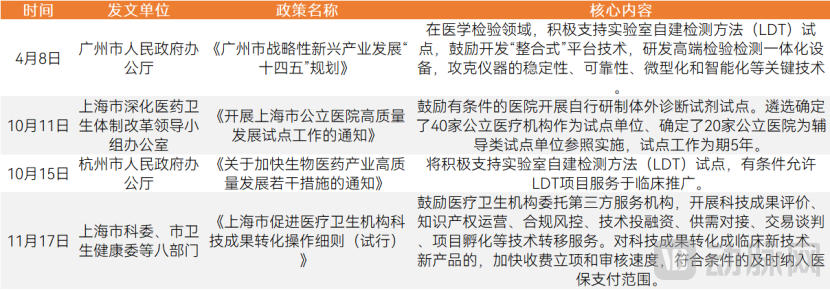

2022 LDT-Related Policies

Hospitals are the primary entities conducting LDT pilots, enabling more controllable regulation.“Notice on Launching the Pilot Program for High-Quality Development of Public Hospitals in Shanghai” proposes selecting 40 public medical institutions as pilot units and designating 20 public hospitals as guided pilot units for reference implementation, with the pilot program lasting five years. The policy clarifies that hospitals, rather than third-party clinical laboratories, are the primary entities responsible for Laboratory Developed Tests (LDTs), thereby making LDT regulation more controllable.

Regulatory authorities have demonstrated an encouraging and supportive stance, providing a certain basis for the legitimacy of LDTs.LDTs will accompany IVDs to become an important component of the precision diagnosis and treatment industry, playing a more significant role in sectors characterized by rapid technological iteration and flexible application scenarios. It is worth noting that the government has not yet issued specific management regulations; many issues remain to be discussed, such as the scope within which LDTs should be conducted, which hospitals are permitted to develop their own in vitro diagnostic reagents, and what criteria LDT products must meet to be included in medical insurance coverage. The policy does not signify a deregulation of LDT business; rather, it aims to clarify the boundaries between IVD and LDT operations, establishing a framework dominated by IVDs with LDTs in a supplementary role, thereby promoting standardized industry development.

In 2022, the scope of centralized procurement for in vitro diagnostics (IVD) continued to expand, with more provinces participating and a greater variety of products included.

Policies Related to the Centralized Procurement of In Vitro Diagnostics (IVD) in 2022

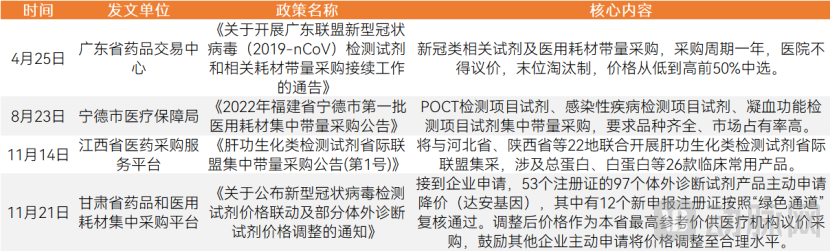

In 2022, the centralized procurement policy for in vitro diagnostics (IVD) became more mature and flexible, serving as a model.Compared with the experimental volume-based procurement conducted in Anhui Province in 2021, the “Announcement on Inter-Provincial Alliance Centralized Volume-Based Procurement of Liver Function Biochemical Testing Reagents (No. 1)” issued by the Jiangxi Provincial Pharmaceutical Procurement Service Platform features more reasonable rule-making. For the same product category, no distinction is made based on methodology; instead, products are classified into milliliter (mL) groups and test groups. These are further divided into two bidding groups, Group A and Group B. Enterprises that commit to fulfilling 70% of the procurement volume are placed in Group A, while others are placed in Group B. Enterprises that commit to supplying products to the entire alliance and whose declared prices do not exceed 0.6 times the maximum valid declared price are added as proposed winning bidders.

Although centralized procurement for in vitro diagnostics (IVD) has not yet reached the scale and systematic level seen with pharmaceuticals and high-value consumables, it has become an irreversible trend in the IVD sector and will reshape the market landscape. Under the pressure of centralized procurement, IVD companies must reduce costs and improve efficiency, while also expanding overseas to seek broader market opportunities.

Price is the “last mile” in determining the accessibility of precision medicine, and breakthrough progress was made in 2022 regarding the inclusion of tumor genetic testing technologies, such as next-generation sequencing (NGS), in medical insurance coverage.

Policies on the Inclusion of Oncology Genetic Testing in Medical Insurance in 2022

On October 12, the National Healthcare Security Administration (NHSA) released its “Reply to Suggestion No. 4221 from the Fifth Session of the 13th National People’s Congress,” providing an official response regarding the inclusion of tumor genetic testing services in medical insurance coverage and their participation in volume-based procurement. The NHSA pointed out that certain regions have already incorporated selected genetic testing items into the scope of medical insurance reimbursement. Furthermore, relevant authorities are guiding local governments to include, through established procedures, genetic testing services that are safe, effective, cost-appropriate, and have clearly defined charging standards into their local medical insurance reimbursement scopes.

The Fujian Provincial Healthcare Security Administration’s inclusion of NGS technology in its medical insurance coverage is of significant importance.In guiding medication use, many targeted therapies have been included in the national medical insurance scheme and centralized volume-based procurement programs, leading to a significant drop in prices. However, the accompanying genetic testing still relies on out-of-pocket payments, with cost becoming the primary barrier. Due to high fees—ranging from thousands to tens of thousands of yuan—oncology genetic testing has not been widely covered by medical insurance. Previously, only a few regions, such as Beijing, had included more mature technologies like PCR and FISH in their insurance coverage. The Fujian Provincial Medical Insurance Bureau took a significant step forward by being the first to include next-generation sequencing (NGS) technology in its insurance scheme. The clinical value of oncology genetic testing in guiding treatment, monitoring recurrence, and enabling early screening and diagnosis is now well established. It requires collaborative efforts from both enterprises and government agencies: companies should actively drive further reductions in sales expenses and testing costs, while medical insurance policies should provide clearer support for the value of oncology genetic testing, thereby expanding insurance coverage to include more technologies.

Product Technology: Upstream Original Innovation Explodes, Downstream Products More Diverse

Upstream Barriers Are Being Broken Down as the Domestic Gene Sequencer Market Heats Up.Previously, upstream gene sequencers were considered one of the most difficult import-monopolized sectors to break through. In recent years, with breakthroughs in upstream technologies, lowered entry barriers, increased cost pressures downstream, and stricter regulations, domestically produced sequencers have been launched at an accelerating pace. Against the backdrop of domestic substitution and continuously expanding demand in downstream application areas, the market prospects for domestically produced sequencers are promising. Sequencer manufacturers now need to plan appropriate development paths tailored to different application scenarios and types of testing projects, ensuring that their instruments operate effectively in both research and clinical markets.

Newly Released Domestic Gene Sequencing Systems in 2022

Downstream, application scenarios and technologies are more diversified.Companion diagnostics, infectious disease testing, genetic disease testing, early cancer screening, and minimal residual disease (MRD) detection are the primary application scenarios for precision diagnosis and treatment. The product portfolio continues to expand; for instance, Genetron Health announced the launch of its pan-cancer MRD detection product, Weishibo, while New Horizon Health initiated the PANDA study, a pan-cancer early screening and diagnosis cohort project in China. Meanwhile, technological innovations such as clinical mass spectrometry, exhaled volatile organic compound (VOC) detection, nanopore sequencing, single-cell sequencing, multiplex fluorescent immunohistochemistry, and artificial intelligence (AI) are being applied in these fields. Examples include fourth-generation nanopore-based early cancer screening technology, qPCR platform-based solid tumor MRD detection, NIPT PLUS, and Berry Genomics’ thalassemia detection product based on third-generation sequencing. Emerging scenarios, such as neurological disease testing and home-based testing, are also experiencing rapid development driven by technological advancements and policy support.

Commercialization: Accelerating Global Expansion to Drive New Growth Momentum

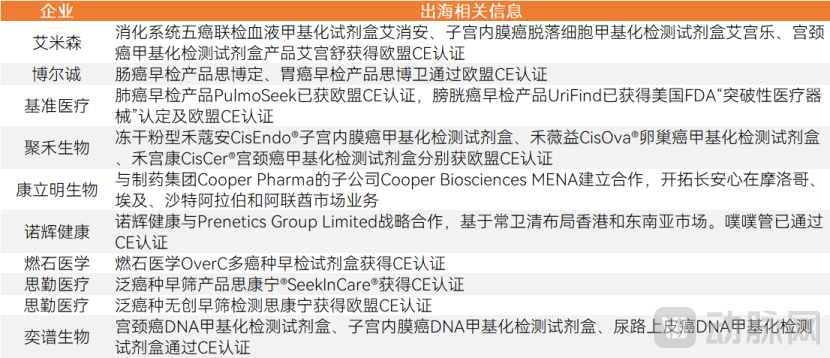

"Going global" was one of the key themes for the precision diagnostics and therapeutics sector in 2022. Impacted by the COVID-19 pandemic, companies in this field have been expanding overseas to varying degrees and at different paces.In 2022, many companies made tangible market entry moves overseas, with enterprises making relevant attempts in both IVD products and LDT testing services. For instance, New Horizon Health entered into a strategic partnership with Prenetics Group Limited to expand into the Hong Kong and Southeast Asian markets based on its ColoClear product. Geneseeq reached a strategic cooperation agreement with Hospital de Base in Brazil to jointly establish an in-house NGS laboratory and advance clinical research in oncology.

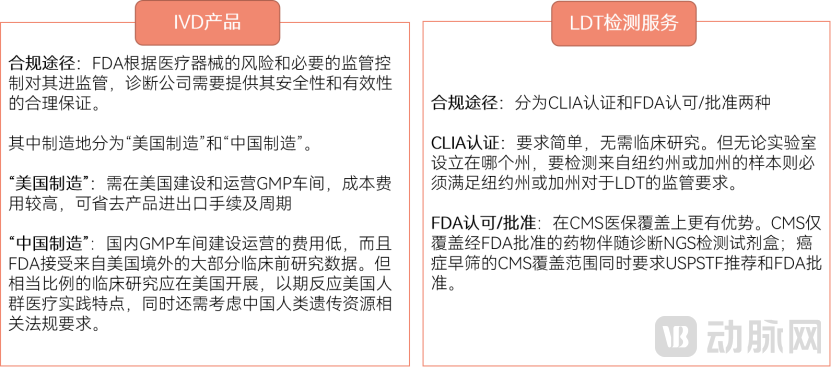

U.S. Regulatory Requirements for IVD Products and LDT Testing Services

Most encouraging is the remarkable success achieved overseas by companies specializing in at-home COVID-19 antigen self-tests; early cancer screening and point-of-care testing (POCT) are emerging as promising new frontiers for international expansion.According to statistics from the China Chamber of Commerce for Import and Export of Medicines and Health Products, in the first half of 2022, China’s export value of major in vitro diagnostic (IVD) reagents reached approximately USD 7.909 billion, a year-on-year increase of 288%. Among this, exports of self-test reagents amounted to USD 6.888 billion, accounting for as high as 87.09%. The success of COVID-19 antigen self-tests has effectively opened a market entry point. In the United States, which represents the largest market opportunity, the laboratory testing sector has long been dominated by leading companies such as Abbott, Beckman, and Roche, while their presence in the point-of-care testing (POCT) market remains relatively limited. Given the mature “family physician” model in the U.S., Chinese enterprises can target the primary care segment, with cancer early screening, home-based testing, and POCT products serving as suitable entry points.

Global expansion remains in its early exploratory stages, with most enterprises lacking sufficient capabilities for international operations; however, efforts to expand overseas are expected to intensify following the relaxation of pandemic controls.Overseas markets, particularly those under the stringent regulatory oversight of the U.S. Food and Drug Administration (FDA), present significant challenges. These include meeting rigorous regulatory requirements, selecting appropriate products for market entry, accurately gauging target market dynamics, and formulating sound market strategies. Currently, many companies’ international expansion efforts are limited to establishing commercial partnerships with overseas firms; substantial long-term commitment and resource accumulation will be required for deeper market penetration.

Through interviews and research on China’s precision diagnostics and therapeutics sector, VBInsight focuses on five subfields that underwent significant changes in 2022: tumor next-generation sequencing (NGS), early screening, minimal residual disease (MRD) detection, clinical mass spectrometry, and point-of-care testing (POCT).

Tumor NGS: Returning to the Essence of Value

In 2022, two companies in the oncology NGS sector filed their prospectuses.Following the NASDAQ listings of Burning Rock Biotech and Genetron Health in 2020, the market saw renewed IPO activity in 2022 after a prolonged lull. In May, Geneseeq Technology submitted its prospectus to the STAR Market of the Shanghai Stock Exchange, and in September, Zhenhe Technology filed its prospectus with the Hong Kong Stock Exchange. As highly sought-after players in the primary market, both Geneseeq and Zhenhe have secured substantial financing and established representative business layouts within the industry. Their strategic moves often signal industry trends and can significantly influence short-term market dynamics. However, overall, the pioneering efforts of leading tumor NGS companies have not proceeded smoothly. The expansion of the tumor NGS market appears to have encountered some substantive challenges in 2022.

2021 Revenue Performance of Genetron Health and Zhenhe Technology

Tumor NGS companies have yet to escape the profitability dilemma, with persistent issues such as high sales expenses and difficulties in achieving profitability remaining unresolved.Stock prices of listed companies offering tumor NGS services have been underperforming. Prospectuses reveal that neither Geneseeq Technology nor Zhenhe Biotech has yet carved out a clear path to sustainable profitability; both companies are currently operating at a loss. Moreover, Geneseeq’s sales expenses reached RMB 250 million, while Zhenhe Biotech’s amounted to RMB 253 million, indicating that both firms are engaging in cash-burning strategies to expand their market share.

Returning to the Essence of Value: The Strong Momentum in Tumor NGS Development Lies in Cost Reduction.For many years, the development of tumor next-generation sequencing (NGS) was excessively rapid, leading to resource strain. 2022 marked a year for the industry to return to its core value proposition, requiring companies to remain focused and dedicated to addressing practical industry challenges. During the explosive growth phase, broad market coverage was the choice for most enterprises; however, as the industry enters a mature stage, reckless expansion has ceased. Clear division of labor is now essential, with companies needing to focus on their areas of expertise and concentrate resources. This will result in a market landscape dominated by a few comprehensive leading enterprises alongside multiple specialized firms. Furthermore, while the clinical value of tumor NGS is well-established, sample volumes have fallen short of expectations, largely due to cost issues. Cost remains one of the primary barriers preventing tumor NGS from being included in national medical insurance programs. Currently, the few regions that have incorporated genetic testing for tumors into their medical insurance schemes do not cover NGS technologies. Measures such as obtaining regulatory approvals for hospital entry, promoting compliance, and adopting upstream domestic sequencing platforms are effective strategies for reducing costs. It is anticipated that some enterprises will be the first to break free from these cost constraints.

Accelerated Innovation in Early Cancer Screening: Technological and Commercial Breakthroughs

The tumor-guided medication segment is approaching saturation, with severe homogenization competition among lung cancer small-panel products; identifying new high-demand application scenarios has become an urgent priority. In recent years, extending upstream to focus on early-stage cancer patients and establishing a presence in early cancer screening, as well as expanding downstream to monitor postoperative patients through minimal residual disease (MRD) testing for recurrence surveillance, have emerged as key trends.

Technical approaches are becoming more diversified, with metabolomics and proteomics playing an increasingly in-depth role in early cancer screening.The technological landscape for early cancer screening is expanding beyond DNA methylation-based approaches to include other modalities, such as circulating tumor cell (CTC) detection. Given the extremely low abundance of CTCs in blood and the resulting challenges in their capture, higher-sensitivity technologies are enabling precise CTC detection. Additionally, metabolomics leverages the significant metabolic differences between tumor cells and normal cells for early screening. However, these emerging technologies are generally in their early stages and require further clinical validation.

In 2022, companies specializing in early cancer screening continued to explore commercialization strategies and, leveraging the strong overseas performance of COVID-19 antigen test kits, began expanding into international markets.

2022 Overview of Chinese Early Cancer Screening Companies Expanding Overseas

Early cancer screening expansion overseas is still in the exploratory stage, with Southeast Asia and Africa being the primary destinations.Currently, the internationalization efforts of most early-stage tumor screening companies remain largely confined to product market access. While these companies are actively pursuing EU certifications, few have made substantial progress in actual market implementation. In 2022, New Horizon Health and ColonClear Biotechnology took significant initial steps in global expansion, both launching colorectal cancer early screening as their flagship products. This choice was driven by the technology’s maturity, the high incidence of colorectal cancer, its high early-stage cure rate, and the limitations of existing screening methods. According to research by LeadLeo Research Institute, emerging markets hold a generally more favorable perception of Chinese brands. Both leading companies have temporarily avoided the highly competitive European and American markets, instead focusing on Southeast Asia and Africa, where public healthcare resources are relatively scarce. Although competition is less intense in these regions, considerable efforts are required for market education and establishing payment mechanisms.

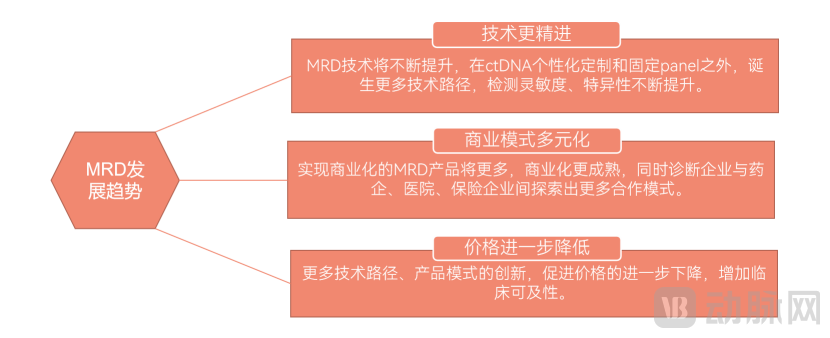

Accelerated Validation of the Clinical Value of MRD

In 2022, the MRD market saw further product diversification, covering hematologic malignancies, colorectal cancer, lung cancer, and pan-cancer indications. Compared with other products, pan-cancer MRD testing is not limited to specific cancer types, thereby benefiting a broader patient population. Furthermore,MRD Technology Awaits Innovation: Multi-Omics Combined Detection Strategies Beyond Conventional Approaches Deserve Attention.Domestic MRD products largely follow overseas technical approaches, employing either personalized ctDNA assays or fixed panels. They lack substantial innovation in technical pathways and have not yet adequately addressed the challenge of extremely low ctDNA levels, necessitating broader and more diverse strategies. According to the latest research and frontier trends from academic forums, multi-omics integrated approaches represent a new opportunity to improve detection accuracy. Existing studies have demonstrated that methylation can serve as a biomarker for MRD detection in colorectal cancer.

Cost price is a key factor that MRD products need to focus on in the next stage.In addition to analytical performance, the high cost remains a major barrier to the clinical implementation of MRD testing. Currently, most MRD products are developed using hybrid capture-based NGS methods combined with mutation profiling. These approaches involve complex methodologies, long turnaround times, and high costs, making them difficult to implement in hospital settings. Huisuan Genomics has identified a methylation marker (named BF Marker) that influences the initiation and progression of multiple solid tumors through changes in its methylation status, exhibiting a consistent methylation pattern across 17 types of solid tumors. Leveraging the BF Marker on a qPCR platform, Huisuan Genomics has developed an MRD detection product for solid tumors. This solution offers superior ease of use and clinical feasibility compared to NGS-based platforms, significantly reducing the cost of MRD testing.

MRD Development Trends

The Rising Popularity of Mass Spectrometry

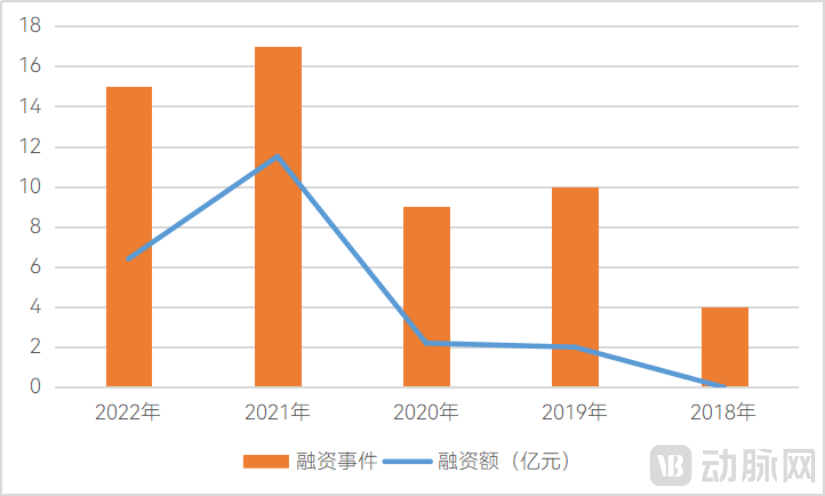

Capital interest in the clinical mass spectrometry sector remains strong, with 15 financing deals closed in 2022, totaling over RMB 640 million.Since 2020, investment institutions have made intensive moves in the clinical mass spectrometry market. However, compared with 2021, financing activities in the clinical mass spectrometry sector did not reach new highs in 2022. The capital market places significant emphasis on the definitive clinical applications of mass spectrometry technology. Currently, mass spectrometry enjoys relatively high clinical recognition in areas such as newborn screening and microbial identification, achieving a certain testing volume, but it has yet to establish a monopolistic advantage. Moving forward, companies in the clinical mass spectrometry field need to make greater strides in demonstrating the certainty of clinical applications and achieve killer-app status in clinical practice at an early stage.

Comparison Chart of Clinical Mass Spectrometry Financing Over the Past Five Years

In 2022, a total of 51 clinical mass spectrometry products received approval from the NMPA, accelerating regulatory compliance.Instruments are essential for conducting diagnostic applications in China’s clinical market. Among approved instruments, liquid chromatography-tandem mass spectrometry (LC-MS/MS) and time-of-flight mass spectrometry (TOF-MS) remain the two predominant types. On the reagent side, many companies have targeted the vitamin testing market, which is characterized by low penetration rates and substantial growth potential; 16 related products received approval in 2022. The importance of comprehensive vitamin profiling is increasingly recognized, with growing consensus on the need to comprehensively assess levels of essential vitamins to ensure adequate and balanced vitamin status in the body. Since Yingsheng Biology became the first to obtain registration certification for comprehensive vitamin testing reagents in 2021, the approval pace for comprehensive vitamin testing kits accelerated significantly in 2022. Fenghua Biology’s fat-soluble and water-soluble vitamin assay kits received approval, as did Kaluipu and Mass Spectrometry Biology’s fat-soluble vitamin assay kits. The number of registration certificates for therapeutic drug monitoring, newborn screening, and human trace element testing kits has also increased, attracting a growing number of companies to enter these fields.

Policy Push Accelerates the Adoption of POCT in Home Testing Scenarios

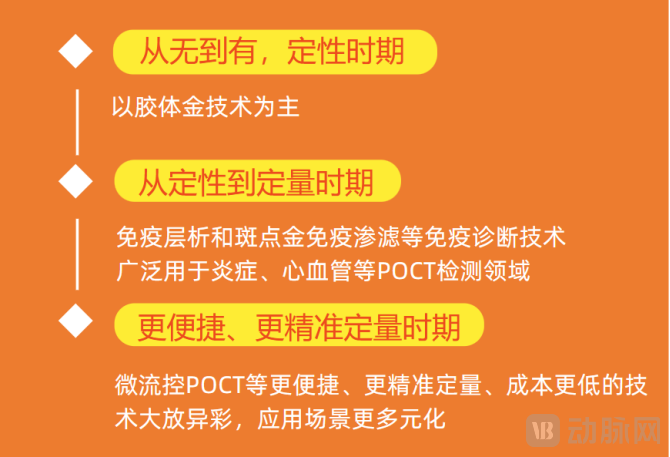

China's POCT Market Is Entering an Era of Greater Convenience and Precise Quantification, with Microfluidics Technology Leading the Technological Transformation in China's POCT Market.The Chinese POCT market can be divided into three stages. The first stage was characterized by the emergence of qualitative testing, primarily based on colloidal gold technology. The second stage marked the transition from qualitative to quantitative testing. The third stage represents a period of more convenient and precise quantitative testing, with microfluidic POCT technology at its core. Microfluidic POCT technology addresses the limitations of traditional techniques in precisely controlling the entire reaction process, enabling the detection of samples with very low molecular concentrations and achieving a significant leap in testing accuracy. Currently, China is in the early stage of precise quantitative testing, with relatively few approved microfluidic POCT products. In the coming years, microfluidic technology will lead technological innovation in China’s POCT market, driving POCT to play a substantial role in tiered diagnosis, telemedicine, and precision medicine.

Trends in Technological Transformation of the POCT Market

The large-scale application of microfluidic POCT products depends on stable mass production and cost control capabilities.Microfluidic chips are downstream application units of microfluidics technology. By leveraging micro-electro-mechanical systems (MEMS) technology, miniature biochemical analysis systems are constructed on the chip surface to rapidly and accurately process and detect proteins, nucleic acids, or specific targets. Key steps that traditionally require laboratory settings—such as sample pretreatment, immune reactions, and result detection—are integrated onto a single tiny chip, offering advantages including ease of operation, rapid detection, and high accuracy. However, two major challenges hinder large-scale adoption: high costs and difficulties in achieving stable mass production.Weikang Bio has successfully developed multiple platforms, including “Microfluidic Time-Resolved Immunofluorescence,” “Disc-Based Microfluidic Multiplex Immunoassay,” and “Modular All-in-One Microfluidic Molecular Diagnostics.” Weikang Bio is the first company in China to address the pain points associated with microfluidic POCT products, namely high costs, challenges in stable mass production, and difficulties in room-temperature storage. Furthermore, all raw materials, chips, reagents, and instruments for its microfluidic products are independently researched and manufactured by Weikang Bio. In terms of import substitution, its prices are more than ten times lower than those of imported chips.

Favorable policies are driving POCT products to open the door to home testing.The COVID-19 pandemic has reshaped the landscape of the home testing market. Previously, the overall home diagnostics market developed relatively slowly, consumers had not yet formed the habit of self-testing at home, and the household segment remained difficult to penetrate. On March 10, the National Health Commission issued a policy stating that antigen testing would be added as a supplement to nucleic acid testing. Community residents with needs for self-testing could purchase antigen test kits through retail pharmacies, online sales platforms, and other channels for self-administered tests. The liberalization of at-home COVID-19 antigen testing accelerated market education and maturity, igniting enthusiasm among numerous companies to enter the home testing sector. Projects such as infectious disease testing, women’s health, and chronic disease management are expected to see faster adoption in home settings.

Approval Status of Domestic Companies' COVID-19 Home Testing Products

2022 Dynamics of Non-COVID Home Testing Products

VCBeat Research Institute believes that in 2023, key areas of focus should include the progress of clinical application of innovative technologies, the definitive advancements in companies’ global expansion, and the direction of relevant policies. In particular, technological innovation has become a strategic priority for companies across multiple segments of precision diagnosis and treatment. The industry currently exhibits a diversification of technologies, including exhaled volatile organic compound (VOC) detection, single-cell technology, multiplex immunohistochemistry (mIHC), clinical mass spectrometry, single-molecule immunoassays, and digital PCR, among others. While these innovations demonstrate strong technical novelty, they have not yet been widely adopted in clinical practice. Therefore, close attention should be paid to their clinical implementation, such as breakthroughs in the clinical application of exhaled VOC detection and single-cell technologies.

Exhaled VOC Testing Has Gained Official Recognition Overseas; Focus Should Be Placed on Domestic Progress

In 2022, the FDA granted Emergency Use Authorization (EUA) to the first SARS-CoV-2 diagnostic product based on breath volatile organic compound (VOC) analysis. This test can be deployed in diverse settings, including hospitals, physician offices, public spaces, and mobile monitoring stations. It requires only a breath sample and delivers results in under three minutes. This milestone represents official endorsement of breath VOC testing, clearly demonstrating its practical clinical applications.

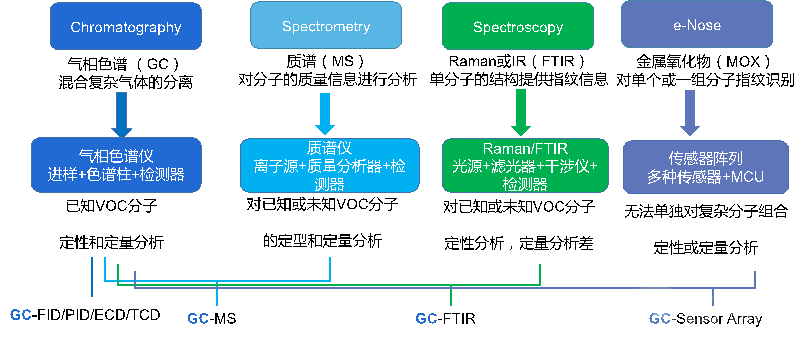

Mainstream Technologies for Exhaled Breath VOC Detection

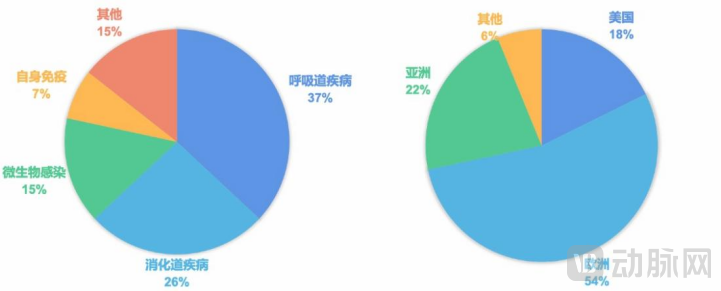

Exhaled VOC detection technology is set to be first implemented in the fields of gastrointestinal and respiratory diseases, with the most active deployment occurring in Europe and the United States.In terms of pipeline layout, according to statistics from Jingzhi Future, there are currently over 111 clinical pipelines worldwide focusing on exhaled volatile organic compounds (VOCs), primarily targeting respiratory and gastrointestinal diseases. Respiratory conditions account for 37% of these pipelines, while gastrointestinal conditions make up 26%, together comprising 63% of the total. Products in the fields of gastrointestinal and respiratory diseases are expected to achieve clinical implementation first. It is evident that companies are strategically focusing on diseases closely related to the respiratory system, such as asthma and lung cancer, particularly in areas where existing clinical technologies fall short. They are dedicated to overcoming challenges such as differentiating benign from malignant pulmonary nodules, early detection of asthma, and precision medication. In the future, more companies are expected to make breakthroughs in cancer, infectious diseases, and metabolism-related chronic diseases. Regionally, Europe is the most active in the field of exhaled VOC testing, accounting for 54% of all pipelines.

Global Distribution of Exhaled VOCs by Disease Area (Left) and by Region (Right)

In the future, focus can be placed on companies with three characteristics, first beingCompanies with Clinical-Grade Exhaled VOC Detection Products, the technologies of many enterprises still exhibit characteristics typical of research laboratory equipment; the devices are complex to operate, posing challenges for widespread clinical adoption. Second,Companies Capable of Performing Comprehensive Profiling Analysis of Exhaled Breath VOC Molecules, the relationship between VOC molecules and diseases requires breath analysis equipment that can perform both qualitative and quantitative analyses, thereby decoding the informational "black box" from multiple dimensions and clarifying the causal relationship between diseases and VOC molecules. Thirdly,Companies that Fully Leverage AI Technology to Empower Exhaled VOC AnalysisExhaled VOC analysis is complex and cumbersome, and the integration of AI technology significantly facilitates the identification and optimization of biomarkers. Jingzhi Future has developed a miniaturized POCT exhaled breath micro-gas chromatograph using MEMS technology, which enables rapid collection and analysis of patient samples at the bedside. Meanwhile, it employs artificial intelligence algorithms for automated interpretation of breath profiles, thereby addressing the limitations of traditional large-scale detection equipment, such as cumbersome operation, prolonged detection and data analysis time, and inapplicability to bedside and community settings.

Frequent Advances in Single-Cell Technologies: Focus on Breakthroughs in Translating Research into Clinical Practice

Single-cell technology is hailed as the cornerstone of research services for the next decade. Its application in the scientific research market is currently relatively widespread. In 2022, multiple single-cell technology companies announced progress in their research-oriented product offerings. The market potential for research services is substantial; however, most enterprises rely on imported foreign systems to deliver services. Domestic self-developed solutions have not yet achieved scale, and no dominant market leaders have emerged.

The clinical implementation of single-cell technologies is key to the industry’s next phase of explosive growth; focus on their clinical applications.The market size for scientific research services is limited. In the clinical market, single-cell technology has held high expectations since its inception, yet it has not been fully implemented to date. Clinical application areas for single-cell technology include reproductive genetic health, oncology, neuroscience, immune system diseases, and infectious diseases. As intensifying competition in the scientific research services market leads to declining gross margins, attention in the coming years should focus on breakthroughs in the clinical application of single-cell technology. Specifically, companies that achieve advancements in clinical cohort studies, pricing, and end-to-end automation warrant close monitoring.

Monitor Substantive Policy Actions in Health Insurance and LDTs

Detailed regulatory guidelines for Laboratory Developed Tests (LDTs) are expected to be introduced. Currently, LDT models are best suited for projects addressing urgent clinical needs with well-established biomarkers.LDT services are important, but their management is highly complex. Overly stringent or overly lax regulations are detrimental to industry development; therefore, an appropriate balance must be struck. Taking genetic testing—where LDT implementation is relatively feasible—as an example, LDTs should have defined scopes of application. For instance, NIPT PLUS, which offers incremental improvements over the extensively market-validated NIPT, can be included within the LDT framework. In the oncology market, where large and small panels share many technical pathways, extended products based on existing offerings may also fall under the LDT scope. However, projects such as cancer early screening and minimal residual disease (MRD) detection involve significantly different biomarkers and are currently unsuitable for LDT-based management. It is anticipated that detailed LDT regulatory guidelines will soon be issued in China.

Focus on Business Model Iteration: Global Expansion Presents New Opportunities

Focus on companies that are emerging in overseas markets.The seller’s market that emerged under the impact of the COVID-19 pandemic has not only opened up overseas channels for domestic IVD companies but also unlocked significant potential in international markets. In the post-pandemic era, companies across various sub-sectors have set their sights on the vast overseas market and are accelerating their global expansion. Currently, while COVID-19 antigen self-test kits have achieved representative success in going global, the internationalization of other high-potential segments, such as early cancer screening and POCT, remains in its early stages. It is expected that some companies will soon be the first to establish comprehensive overseas operations systems and achieve commercial success.

"Band together to go global" will become a new trend.China’s precision diagnosis and treatment sector comprises numerous enterprises, predominantly small and medium-sized businesses. Domestically, the market is characterized by intense involution and fierce price competition. Internationally, collaboration has become a key strategy for Chinese companies expanding overseas. By integrating resources across products, technologies, and distribution channels to deliver comprehensive solutions tailored to different countries and regions, Chinese enterprises can secure pricing power and maximize value.

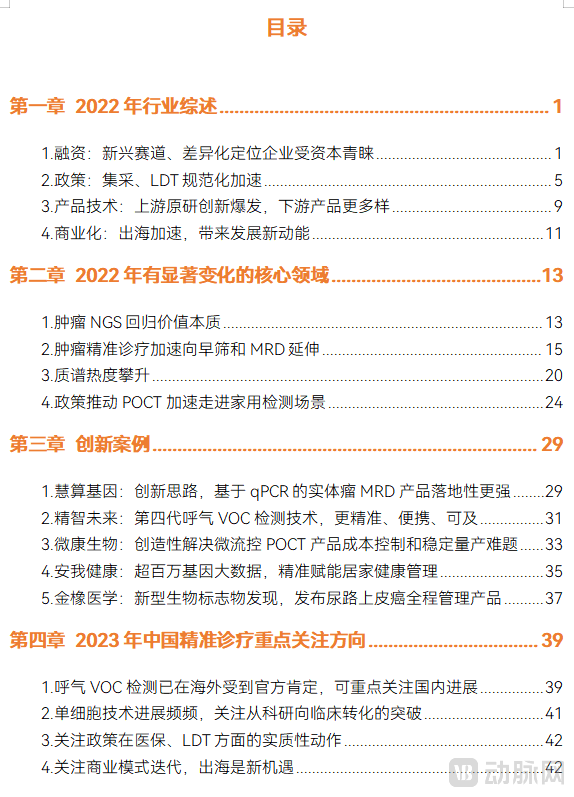

Table of Contents for the "2022 Annual White Paper on Digital Healthcare Innovation"

The above is an excerpt from the main content of the report. The complete framework of the report is as follows. Scan the QR code to add our assistant and obtain the full report; if you have already added the assistant, please proactively request the document.