2022 Medical Services White Paper: Patient-Centric Care from Concept to Practice

Currently, China is facing the social realities of an aging population and a declining birth rate, which have had a direct impact on the healthcare service system. Compounded by the effects of the pandemic, the healthcare service system underwent multifaceted changes in 2022. Active innovations were introduced across various segments—including healthcare providers, pharmaceuticals, and insurance—to increase resource supply and promote the restructuring and integration of resources. Consequently, the concept of “patient-centered care” has gradually transitioned from theory to practice.

This white paper, based on industry research and interviews, aims to observe and document innovative practices in the healthcare services sector across dimensions such as service models, technology applications, and user coverage.

(Note: To obtain the full version of this report, please scan the QR code at the end of the article to add our assistant. If you have already added them, please initiate your inquiry proactively.)

In 2022, the healthcare services industry underwent changes in policy and capital markets, yet the overall direction remained focused on increasing the supply of medical resources and improving healthcare quality.

Accelerating Volume Expansion and Quality Improvement Remains the Overall Policy Direction; Surgical Management Undergoes Significant Changes

In 2022, policies in the healthcare services sector primarily focused on building a high-quality service system, generally adhering to the principles of supplementing overall capacity and enhancing quality. The Notice of the General Office of the State Council on Issuing the 14th Five-Year Plan for National Health pointed out that by 2025, the health and wellness system would be further improved, with significantly enhanced capabilities in health science and technology innovation. Life expectancy at birth was projected to increase by approximately one year from the 2020 level, with healthy life expectancy rising proportionally. The increase in life expectancy, coupled with population aging, has imposed higher demands on the treatment and rehabilitation of tumors, chronic diseases, and other conditions. Therefore, it has become increasingly urgent to continuously supplement corresponding high-quality medical resources and to innovate payment mechanisms to improve the accessibility of these resources.

Regarding privately operated medical institutions, encouraging their development as an important supplement to the public healthcare system remains the overarching direction. In the Guiding Principles for the Planning of Medical Institution Establishment (2021–2025), the National Health Commission proposed expanding the scope for privately operated medical institutions, with no planning restrictions on their regional total volume or spatial distribution; exploring various forms of collaboration between privately operated medical institutions and public hospitals; and removing planning and layout restrictions on clinic establishment, implementing a filing-based management system. Privately operated medical institutions remain a significant force in effectively increasing the supply of medical resources and meeting the public’s multi-level and diverse needs for medical and health services.

Furthermore, the policy imposes higher requirements on standardized services and healthy development in areas such as internet-based medical consultations, pharmaceutical e-commerce, and commercial health insurance.

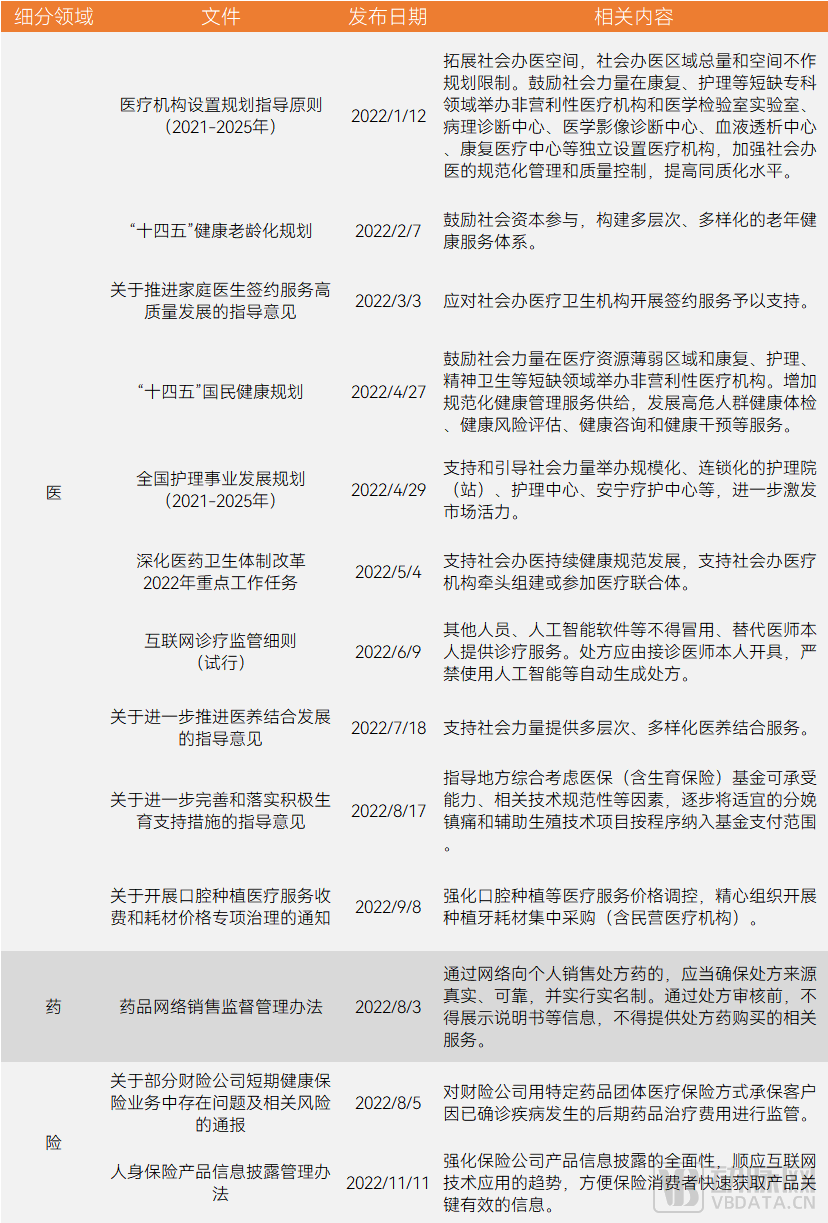

Overview of Policies in the Healthcare Sector in 2022, Source: National Health Commission and National Healthcare Security Administration Websites

In 2022, significant changes were made to the policy on tiered surgical management. The performance of surgeries at different levels is no longer tied to the accreditation level of medical institutions or the professional titles of physicians. The decentralization of surgical privileges has provided medical institutions with greater flexibility and more opportunities to enhance their technical capabilities and influence.

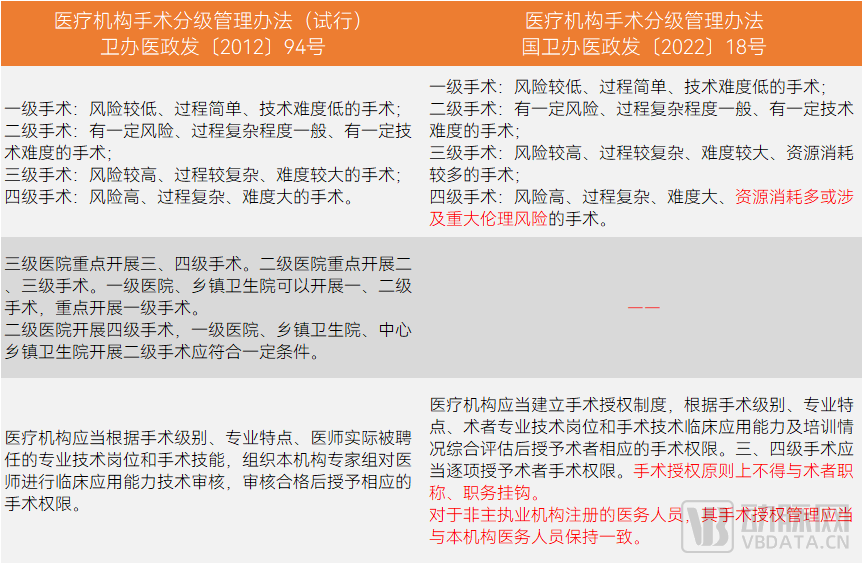

In December 2022, the General Office of the National Health Commission issued the “Administrative Measures for the Hierarchical Management of Surgeries in Medical Institutions” (hereinafter referred to as the new “Measures”).

The newly released Measures aim to continuously strengthen the primary responsibility of medical institutions in areas such as medical quality and medical technology management, stimulate their initiative to enhance self-management, and guide them in continually improving the scientific, refined, and standardized levels of their management. The previous model for classifying and managing medical technologies and surgeries based on the tiering of medical institutions no longer meets the requirements for high-quality development of medical institutions in the new era.

Comparison of Old and New Policies on Surgical Classification Management, Source: National Health Commission

Compared with the "Administrative Measures for the Hierarchical Management of Surgeries in Medical Institutions (Trial)" (hereinafter referred to as the "Old Measures"), which came into effect in 2012, the new version of the "Measures" adds the phrase "high resource consumption or involving significant ethical risks" to the definition of Level 4 surgeries; removes the provision linking surgical privileges to the classification level of medical institutions; and explicitly states that, in principle, surgical authorization shall not be tied to the surgeon's professional title or administrative position.

The decoupling of surgical privileges from the tier of medical institutions and the professional titles of surgeons has become the most impactful change for the industry in the new version of the Measures.

In recent years, the state has vigorously promoted the balanced allocation of medical resources, requiring high-quality resources to flow from higher-tier medical institutions to primary care facilities, and from developed regions to less-developed areas. Various regions have established Medical Alliances and Medical Consortia, encouraging highly skilled physicians from superior hospitals to provide targeted support at the grassroots level. In accordance with the new version of the "Measures," advanced technologies and new techniques can be more effectively disseminated to lower tiers. Subject to practical conditions, primary hospitals and grassroots medical institutions are now able to perform higher-level surgeries. This not only enables local patients to receive better treatment within their communities but also helps drive the improvement of local medical technical capabilities.

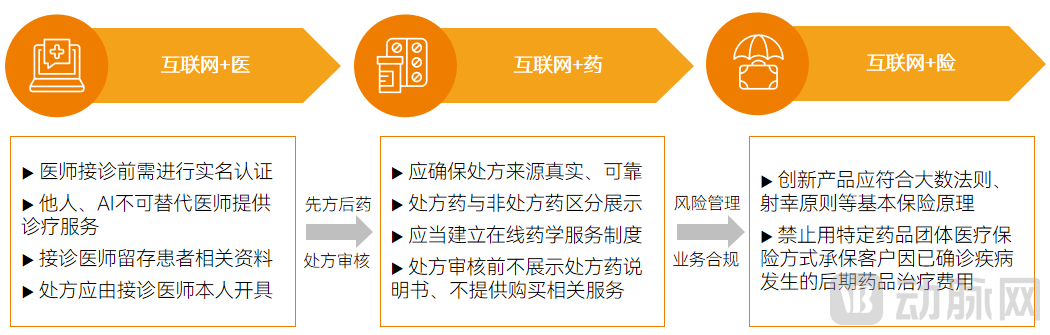

Furthermore, with the implementation of regulatory measures, the “Internet+” healthcare, pharmaceutical, and insurance sectors have entered a stage of standardized development.

As new business models in the healthcare services sector, internet-based medical and pharmaceutical services, as well as integrated healthcare-pharmaceutical-insurance services, were subject to regulatory policies in 2022, accelerating industry standardization and healthy development.

Key Points of Regulatory Policies for “Internet+” Healthcare, Pharmaceuticals, and Insurance; Source: Official Websites of Local Healthcare Security Administrations and Public Reports

In recent years, innovative models integrating the internet with pharmaceutical insurance have emerged in the industry. To enhance access to medical care and medications and effectively alleviate patient burdens, it is essential to focus on iterative updates under compliant frameworks.

Scarce Resources Drive Active Specialty Financing; Physical Medical Institutions Accelerate Consolidation

From the perspective of primary market transactions (categorized by target), 2022 saw active financing in specialized medical services, such as rehabilitation and integrated medical-nursing care, as well as in internet-based healthcare services and insurance services. Mergers and acquisitions targeting physical medical institutions were also vigorous, with traditional listed companies and internet giants continuing to expand their presence, as various stakeholders joined forces to address uncertainties such as the pandemic.

In the realm of general and specialized healthcare, rehabilitation and integrated medical-elderly care services have attracted significant investor enthusiasm.

In 2022, there were 23 financing events in the comprehensive and specialized medical sectors, with a total financing amount of approximately RMB 4.3 billion. Among these, rehabilitation institutions such as Oriental Speech and Rice & Millet secured new rounds of funding; meanwhile, elderly care and health management enterprises including Tianyu Elderly Care, Fuli Health, and Fushoukang also obtained financing. These two sectors primarily focused on health care and rehabilitation services for “the elderly and children,” two demographic groups characterized by substantial demand and strong willingness to pay. Additionally, orthopedic rehabilitation institutions such as Fudong Musculoskeletal and Jidi Care attracted significant capital interest.

In the financing round, Asia Healthcare completed a $400 million Series D funding, marking the largest transaction by amount. Its subsidiary, Wuhan Asia Heart Hospital, has become a model for private healthcare providers due to its excellent capabilities in diagnosing and treating cardiovascular diseases. In addition to operational scale, medical technical expertise is also a crucial factor in attracting capital investment.

In the internet healthcare sector, large-scale financing rounds are scarce, with capital favoring companies that focus on specialized medical disciplines or specific patient populations.

In 2022, WeDoctor secured over RMB 1 billion in financing, led by a state-owned industrial investment fund. This was primarily driven by the rapid replication of its Digital Health Community model across Shandong, Tianjin, Fujian, Shanghai, and other regions. In Tianjin, the grassroots-level Digital Health Community, operated under the leadership of an internet hospital, achieved a daily patient volume exceeding 10,000 and monthly revenue surpassing RMB 100 million within just 30 months of operation.

As the industry has matured, leading companies have emerged; they are either rushing toward an initial public offering (IPO) or have already established a certain degree of self-sustaining profitability, prompting capital to adopt a more rational approach in selecting enterprises.

Furthermore, the merger and acquisition (M&A) and integration of brick-and-mortar medical institutions are accelerating as they join forces to address uncertainties. Among the M&A targets, there are multiple maternal and child healthcare institutions, a trend closely linked to the current market environment.

Consumer Healthcare and Internet Health Services Show Strong Performance, with a Surge in IPOs

From the perspective of IPO activity, 2022 witnessed a surge in consumer healthcare, with companies in the “golden eyes and silver teeth” sectors going public in rapid succession, while hair transplant providers accelerated their push into the secondary market. The internet healthcare sector also delivered impressive performance, with two companies successfully listing on the stock exchange.

Both ophthalmology and dentistry reached significant milestones in 2022, breaking the “one-company dominance” pattern in China’s A-share market as a wave of companies went public. Specifically, He Eye Hospital, Purui Eye Hospital, and Huaxia Eye Hospital all listed on the ChiNext board within a nine-month period, joining Aier Eye Hospital to form a “four-pillar” competitive landscape in the A-share market.

Arrail Group’s IPO on the Hong Kong Stock Exchange broke the long-standing deadlock in which no dental chain had listed on the main board since TCS Medical, making it the first publicly listed national dental chain brand in China. Meihao Dental (formerly China Oral Healthcare Services Group) also successfully listed on the Hong Kong Stock Exchange, having previously submitted six listing applications since 2020.

Furthermore, the successful IPOs of Zhiyun Health and Dingdang Health mark a new phase of development for internet-based medical healthcare.

From the perspectives of healthcare providers, pharmaceuticals, and insurance, the medical services sector in 2022 primarily focused on innovation or deeper exploration in areas such as care delivery models, service workflows, customer segments, and channels. These initiatives were largely centered around the philosophy of “patient-centricity.”

Expansion of the Scope of Diseases Covered by Multidisciplinary Diagnosis and Treatment, Exhibiting Online Characteristics

As an integrated diagnostic and care model vigorously promoted in the healthcare services sector, the Multidisciplinary Team (MDT) model is characterized by an expanding range of applicable disease conditions and enhanced efficiency driven by digitalization.

Since 2018, China’s multidisciplinary team (MDT) approach for digestive system tumors has achieved significant results through pilot programs. The number of pilot hospitals implementing MDT has increased year by year, with a corresponding rise in the number of cases managed. Furthermore, these pilot hospitals have played a leading role within their respective regions.

In 2022, the "14th Five-Year Plan for National Health" pointed out the promotion of multidisciplinary diagnosis and treatment. The General Office of the National Health Commission issued the "Interim Provisions on Outpatient Quality Management in Medical Institutions," stating that medical institutions should actively promote multidisciplinary (MDT) outpatient services, where MDT outpatient clinics are conducted by relatively fixed teams of experts at designated times and locations.

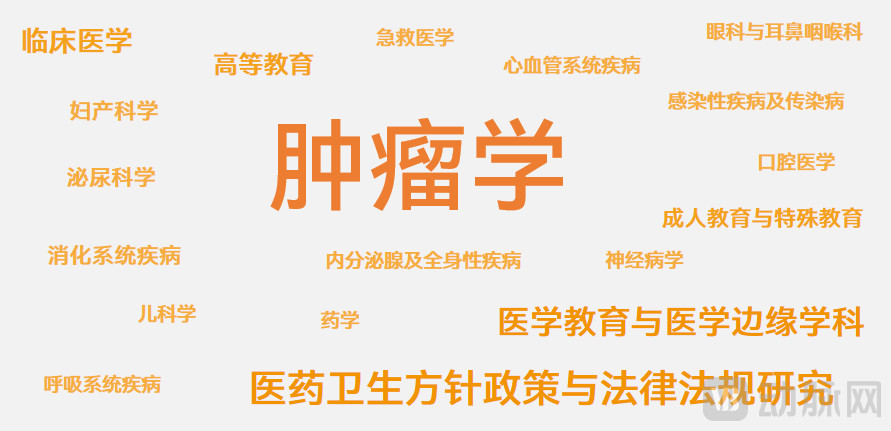

With the promotion of MDT within the healthcare system, this model has been applied to the diagnosis and treatment of a wider range of diseases. Literature data from CNKI shows that, in addition to oncology, MDT is being vigorously implemented in disciplines such as obstetrics and gynecology, urology, otolaryngology, and neurology.

Disciplinary Distribution of MDT-Related Literature, Source: CNKI

Currently, the academic community has established expert consensus on multidisciplinary team (MDT) diagnosis and treatment for elderly cardiovascular diseases, obesity, Gaucher disease, and other conditions to standardize patient care. In practice, medical institutions are also continuously exploring the application boundaries of MDT.

In the field of rehabilitation medicine, Gulian Medical has established multidisciplinary team (MDT) collaborative diagnosis and treatment along with rehabilitation assessment, integrating departments such as Rehabilitation, Neurology, Neurosurgery, Orthopedics, Critical Care Medicine, Cardiology, Traditional Chinese Medicine, and Clinical Nutrition. This approach avoids the limitations of single-specialty diagnoses, reduces disability rates and medical costs, and accelerates patients’ functional recovery.

In the field of mental health, Youmian Lifestyle Medicine Center vigorously promotes multidisciplinary diagnosis and treatment. A team of medical experts from various disciplines collaborates to address conditions such as insomnia, anxiety, depression, and child and adolescent psychiatric disorders, leveraging its specialized clinical strengths centered on “clinical diagnosis and treatment, psychological counseling, physical therapy, and integrated traditional Chinese and Western medicine.”

RenShu Medical specializes in ophthalmology, otolaryngology, and an international ambulatory surgery center. However, through big data analysis during service delivery, it was found that patient conditions often overlap. Therefore, the hospital has established departments with significant cross-disciplinary relevance to ophthalmology and otolaryngology, such as adolescent gynecology, pediatric surgery, and breast surgery, to provide multidisciplinary diagnostic and treatment services.

The emergence and widespread adoption of telemedicine, internet hospitals, and other models have accelerated the digital transformation of multidisciplinary teams (MDTs) and, to some extent, improved their efficiency.

Hospitals under the Yingkang Yisheng umbrella are not only continuously promoting the Multidisciplinary Team (MDT) diagnostic model but also leveraging remote MDT platforms to continually expand the scope and boundaries of hospital services. For instance, Sichuan Friendship Hospital has established a 5G-enabled remote consultation center, connecting with experts from renowned Grade A tertiary hospitals across China and other hospitals within the Yingkang Yisheng system, to collaboratively develop optimal treatment plans for patients across different regions.

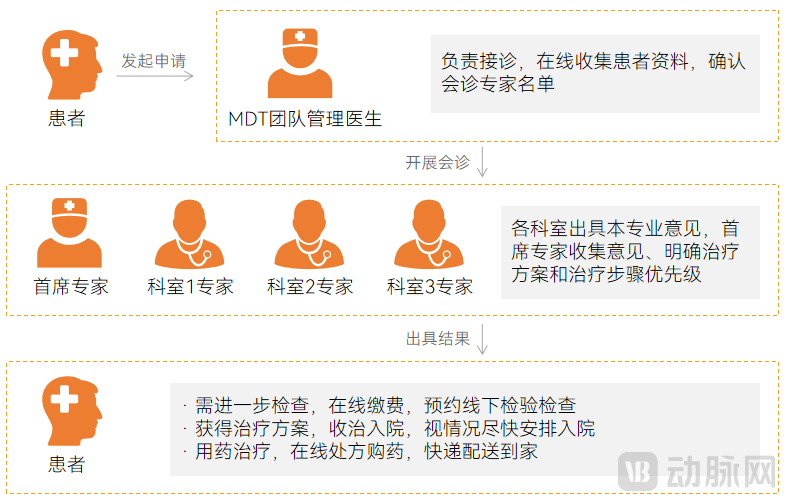

Online MDT Consultation Process, Source: Public Reports

Online multidisciplinary team (MDT) consultations break down disciplinary barriers, transcend temporal and spatial constraints, prevent unnecessary referrals and redundant tests for patients, enable precise diagnosis and personalized treatment, and facilitate greater convenience for physician participation.

Process Reengineering: Building Continuous Medical Services Through Whole-Course Disease Management

Historically, healthcare services—from spatial layout to process design—were centered around medical institutions and healthcare professionals, requiring patients to navigate their care around such configurations. Currently, service processes are being restructured to center on patients’ disease-related needs, providing them with whole-course disease management.

Whole-Course Disease Management refers to a patient-centered approach that adheres to medical guidelines and various clinical consensuses. It focuses on the golden period of postoperative care, monitoring and intervention for patients with chronic diseases, and establishes a multidisciplinary team comprising specialist physicians, rehabilitation therapists, dietitians, psychotherapists, and professional follow-up managers. This team provides continuous care throughout the pre-admission, hospitalization, and post-discharge phases, while maintaining patient health records to form a tightly coordinated closed-loop management system. Multiple academic studies have demonstrated that the whole-course disease management model has achieved certain effectiveness in the fields of malignant tumors, mental disorders, and clinical education.

By integrating tiered diagnosis and treatment with whole-course disease management jointly operated by social forces, all participants can achieve corresponding benefits and maximize value. Core participants are predominantly large hospitals, which typically have numerous departments and high patient volumes but face human resource constraints. Implementing whole-course disease management allows feasible rehabilitation and nursing care to be transferred outside the hospital, thereby shortening patients’ length of stay, accelerating bed turnover, and improving operational efficiency. Additionally, it facilitates data accumulation to support scientific research, thereby enhancing medical quality and the hospital’s influence. For allied or lower-tier medical institutions collaborating with core hospitals, this model helps expand their patient base.

Enterprises participating in whole-course disease management can provide hospitals with technical and operational services, supplementing manpower and optimizing management processes, thereby generating corresponding service revenues.

The Frequent Emergence of Ecosystem-Based Service Organizations: Solving the Challenge of Acquiring C-End Customers

High customer acquisition costs for private medical institutions have become increasingly pronounced amid the growing number of such providers. To address this challenge, a rising number of enterprises are evolving into ecosystem-based service organizations, leveraging specialized departments with similar focuses and interconnected channels to facilitate customer conversion.

In 2021, Jinxin Fertility acquired Jinxin Women and Children’s Hospital to integrate its assisted reproductive services and expand into full-cycle fertility care, encompassing preconception care, IVF, prenatal care, delivery, and postpartum services. In the first half of 2022, synergies between the assisted reproduction and women’s and children’s healthcare segments became evident. In Chengdu, the number of patients who successfully conceived through ART treatment at Chengdu Xinan Hospital in the first half of 2022 and subsequently registered for obstetric care at Jinxin Women and Children’s Hospital increased by 125% year-on-year. Meanwhile, the number of initial consultations from patients referred from the infertility department of Jinxin Women and Children’s Hospital to Chengdu Xinan Hospital for IVF treatment rose by 108% year-on-year.

From the perspective of business formats, ecosystem-based services primarily involve models such as tiered diagnosis and treatment and OMO. Tiered diagnosis and treatment refers to a "hospital + clinic" model that enables mutual referrals between the two, while OMO mainly integrates online and offline channels to facilitate mutual referrals.

Expanding Customer Channels: Aggressively Developing the B2B Market for Corporate Health Management

B2B clients are also a key focus for the expansion of medical services. Particularly in internet healthcare, with resources such as medical care, pharmaceuticals, and insurance already integrated on the supply side, B2B channels have become a critical battleground. In 2022, corporate health management emerged as a hot sector within B2B operations.

As the pace of modern life accelerates and chronic diseases affect younger populations, the health status of corporate employees is far from optimistic. Previous workplace health surveys have consistently highlighted the severity of this issue.

Large enterprises in China have begun to implement employee health management programs. However, traditional health management approaches suffer from numerous shortcomings. For instance, they tend to prioritize screening and treatment over prevention and rehabilitation. Health check-up services often lack adequate pre- and post-examination support, particularly in terms of post-examination data analysis and the formulation of follow-up intervention plans. There is also a lack of long-term tracking and analysis of employees’ health status. Continuous comparison of employee health data can directly reflect the level of health risks and the effectiveness of health interventions, among other factors.

To address these shortcomings, internet-based healthcare can provide more comprehensive, continuous, and dynamic solutions for corporate health management.

Employee Health Management Process Based on Internet Healthcare, Source: Public Reports

In 2022, Ping An Health launched the “Yi Qi Jian Kang” product suite for enterprises, featuring two core offerings—“Check-up+” and “Health Management+”—along with four customizable solutions: Flexible Configuration, Workplace Wellness, Smart Medical Room, and Employee Benefits Redemption Platform. These services provide tailored health management plans for corporate employees of different genders and age groups, based on their specific needs.

Building on its prior experience serving insurance companies, UJia Health has expanded its client channels. Addressing pain points in corporate health services—such as fragmented offerings and inconsistent user experiences—and centering on employee benefits, the company has developed a one-stop employee benefits platform integrating “medical care, wellness, check-ups, and insurance,” thereby providing enterprises with a comprehensive, closed-loop medical and health management service.

Under the Trend of Specialized Retail, "Drugs + Services" Has Become the Standard Configuration

Amid trends such as the outflow of prescriptions from hospitals, the “dual-channel” policy, the growth of specialty pharmacies, and the catalytic impact of the pandemic, the scale of out-of-hospital prescription drug sales has expanded. Patients increasingly demand professional pharmaceutical care, making the combination of medications and services a standard offering in pharmaceutical retail. Moreover, these services extend beyond one-time medication guidance, focusing more on disease management and the long-term maintenance of patient relationships.

Currently, pharmaceutical retail enterprises are vigorously developing specialized pharmacies to enhance their capacity to absorb prescriptions flowing out of hospitals. Specialized pharmacies have become a significant force in the retail market; beyond DTP (Direct-to-Patient) pharmacies, this category includes chronic disease medical insurance pharmacies, specialty/critical illness medical insurance pharmacies, and “dual-channel” pharmacies.

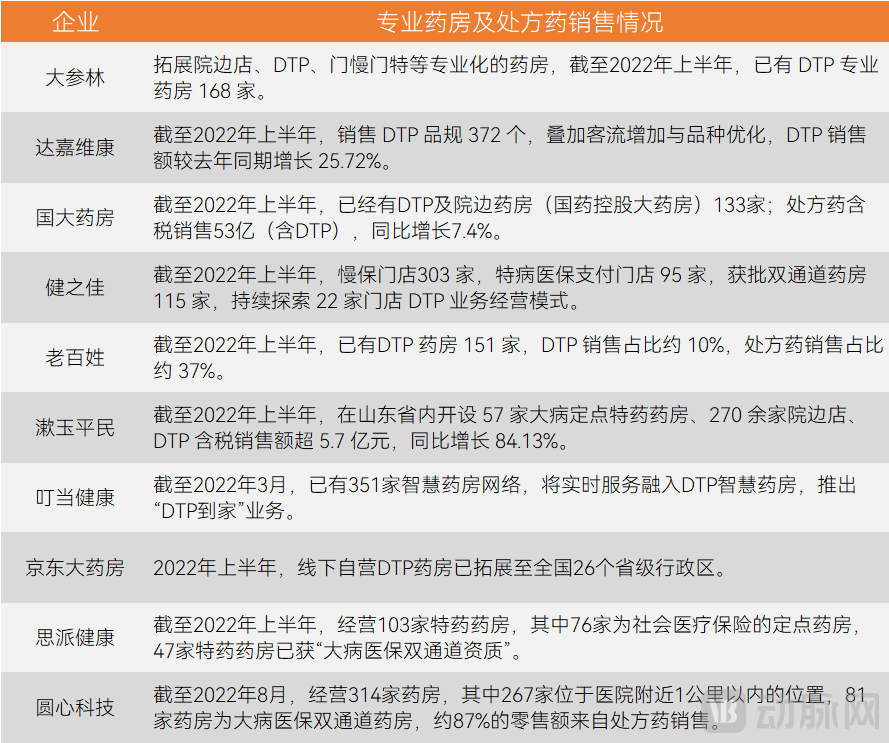

Operational Performance of Specialty Pharmacies at Selected Retail Enterprises; Source: Company Prospectuses and Financial Reports

Growth in specialty pharmacies and the expansion of prescription drug sales necessitate that companies strengthen their professional service capabilities. Particularly accelerated by the pandemic, out-of-hospital prescription drug purchases have become more widely adopted among the general public. On the other hand, there is insufficient public awareness regarding safe medication practices, with issues such as indiscriminate stockpiling and irrational polypharmacy posing health risks. Currently, the integration of “medications plus services” has become a standard offering for retail enterprises.

Amid the Reshaping of the Distribution Market, Digital Marketing Deepens Patient Management

As measures such as centralized drug procurement, national reimbursement drug list (NRDL) negotiations, and the “two-invoice system” become routine, the pharmaceutical distribution market is being reshaped. This transformation is cascading upstream, driving changes in pharmaceutical companies’ marketing strategies and creating an urgent demand for more cost-effective and efficient marketing approaches. In the wake of the digital wave, digital marketing has become a natural progression for pharmaceutical enterprises. In 2022, digital marketing in the pharmaceutical industry continued to deepen, extending further from physician outreach and education to patient management.

Currently, technology companies, internet healthcare enterprises, pharmaceutical e-commerce platforms, and online physician platforms are all actively expanding into digital marketing services for pharmaceutical companies, while traditional marketing firms are also leveraging digital technologies to transform. In terms of specific product features and service offerings, customer relationship management (CRM) systems, virtual representatives, online academic conferences, post-diagnosis follow-up platforms, and patient education all fall within the scope of digital marketing for pharmaceutical companies.

During the rapid development phase, digital marketing service providers have equipped pharmaceutical companies with more efficient tools to reach physicians, facilitating academic promotion and thereby enabling physicians to prescribe medications to appropriate patients. These services also provide patients with easier access to medicines, particularly prescription drugs.

The emergence of digital tools has made more efficient out-of-hospital management possible. Digital marketing service providers are placing greater emphasis on patient management by assembling medical and auxiliary teams focused on specific disease areas, building digital platforms, and providing services such as online consultations, medication guidance, follow-up visit reminders, regular follow-ups, and medical science popularization to enhance patient adherence.

Digitalization enables enterprises to achieve more precise service matching. Leveraging its pharmaceutical big data capabilities and proprietary algorithms, Yuemi Technology has built a data-driven, integrated operation system for doctor-patient services. By employing its own machine learning algorithms to perform user clustering and behavior prediction for doctors and patients, the company facilitates precise matching among “doctor-patient users–medical information–promotion scenarios,” thereby enhancing the efficiency of academic promotion and patient management.

Through continuous and efficient patient interventions, digital-based patient management has demonstrated tangible results. In 2022, Jingli Technology launched a multi-touchpoint follow-up service model leveraging its GemLife intelligent follow-up platform. In one project served by Jingli Technology, the follow-up reach rate exceeded 90%, the duration of treatment (DOT) for enrolled patients increased significantly, reasons for dropout were tracked in real time, and some patients who had dropped out were even re-engaged through subsequent follow-up actions.

Multi-tiered Payment: Huiminbao and Health Insurance Accelerate Coverage for Non-Standard Risks

As a vital component of China’s multi-tiered medical security system, commercial health insurance expanded its coverage in 2022, primarily reflected in the growth of Huiminbao (city-specific supplementary medical insurance) products and medical insurance products for individuals with non-standard health conditions.

"Hui Min Bao" is a special form that combines the dual attributes of basic medical security and commercial health insurance. Currently, the participants in "Hui Min Bao" have formed a development model involving joint participation by "government departments + insurance companies + third-party platform companies."

However, Huiminbao (city-specific supplementary medical insurance) also faces unfavorable factors. For instance, the proportion of non-standard risks among the insured population is steadily increasing, leading to a continuous rise in loss ratios. Meanwhile, only a small number of policyholders actually receive claim payouts, resulting in a significantly low sense of benefit among those who do not receive compensation. This undermines public trust in Huiminbao and hampers its future sales.

In 2022, third-party companies such as Magi Health and Yuanxin Technology conducted more in-depth explorations of product innovation while participating in Huiminbao (city-specific supplemental medical insurance) projects. By integrating online and offline medical and health service resources, they strengthened health management for insured individuals, thereby enhancing their sense of benefit while striving to achieve effective control of disease risks.

Other commercial health insurance products are facing a slowdown in premium growth. According to statistics from the China Banking and Insurance Regulatory Commission (CBIRC), the health insurance sector experienced a period of rapid development from 2018 to 2020, with original premium income surging by 29.7% year-on-year in 2019. However, this growth rate dropped to 7.75% in 2021.

In the first half of 2022, the original premium income from health insurance reached RMB 534.1 billion, a year-on-year increase of 4%, with the growth rate further slowing down compared to previous years.

Large-scale non-standard risk populations have become a key target for expanding the market potential of health insurance. In the future, products designed for non-standard risks must also strengthen health management services, similar to Huiminbao (city-specific supplemental medical insurance), and focus on sales conversion in scenarios where these populations are concentrated, thereby accelerating volume growth.

The growth and expansion of healthcare institutions is a long-term process, and innovation in medical services cannot be achieved overnight; various innovative models also exhibit characteristics of continuity. In the future, medical services will continue to seek new breakthroughs amidst this ongoing evolution.

High-quality resources in rehabilitation, integrated medical and elderly care, and oncology remain scarce and need to be rapidly expanded.

The accelerating pace of population aging is met with persistent shortages in healthcare resources; to address this demographic shift, high-quality specialized medical services—particularly in rehabilitation, integrated medical and elderly care, and oncology—will garner significant market attention.

Currently, China has entered a stage of mild population aging. Research indicates that the size and proportion of China’s elderly population will continue to grow until the mid-21st century, reaching a peak thereafter. By 2050, the population aged 60 and above is projected to reach approximately 480 million, accounting for 37.8% of the total population. On one hand, it is undeniable that population aging has led to increased prevalence of chronic diseases and cancer, necessitating corresponding diagnostic, therapeutic, and rehabilitation services. On the other hand, elderly care services will become an essential requirement in an aging society.

Therefore, the healthcare service system continues to be supplemented with: high-tech, affordable oncology diagnosis and treatment services; efficient, multi-tiered medical and elderly care services that encompass both quality and inclusivity; and rehabilitation services driven by new technologies and interdisciplinary construction.

Payment Policies May Drive Release of Assisted Reproductive Technology Demand, with Licensed Institutions Holding Clear Advantages

Fertility is a social issue closely linked to population aging. In the past two years, the Chinese government has introduced a series of measures to encourage childbirth, including the three-child policy. In the healthcare sector, the introduction of reimbursement policies for assisted reproductive technology (ART) in 2022 is expected to reduce the financial burden on patients and unlock corresponding demand, thereby providing significant advantages to medical institutions licensed to provide ART services.

In 2021, the number of live births for the year was 10.62 million, with a crude birth rate of 7.52 per 1,000 population, remaining below 10 per 1,000 (i.e., 1%) for two consecutive years. To promote long-term balanced population development, the state has introduced a series of fertility support policies targeting medical and health services, including assisted reproductive technology.

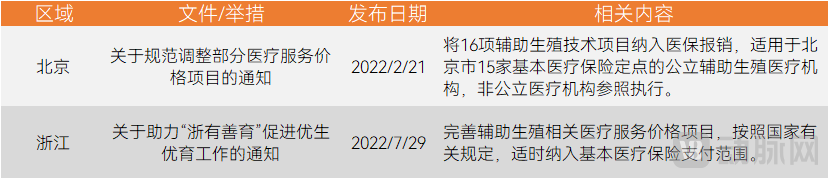

In 2022, the “Guiding Opinions on Further Improving and Implementing Proactive Fertility Support Measures,” jointly issued by 17 departments including the National Health Commission and the National Healthcare Security Administration, proposed that localities be guided to gradually include appropriate labor analgesia and assisted reproductive technology (ART) services in the fund reimbursement scope, following established procedures and taking into account factors such as the affordability of medical insurance funds (including maternity insurance) and the standardization of related techniques. Various regions have also achieved certain policy breakthroughs in the reimbursement of assisted reproductive technologies.

Payment Policies and Measures for Assisted Reproductive Technology Across Regions, Source: Official Websites of Local Medical Insurance Bureaus and Public Reports

Although the inclusion of assisted reproductive technology (ART) in medical insurance has not yet been practically implemented, the formulation of policy directions still helps to promote the establishment of a multi-tiered payment system, including encouraging commercial insurance to intervene more actively.

However, the high threshold for obtaining assisted reproductive technology (ART) licenses and the limited number of medical institutions already accredited remain significant barriers. Overall, the ART sector is poised to further expand its market potential under policy incentives. In the past two years, large healthcare service groups and listed companies have actively entered the ART field, engaging in frequent acquisitions. Medical institutions that have already obtained ART accreditation hold distinct advantages in both business operations and resource integration.

Shifting Disease Intervention Upstream: Specialties Such as Ophthalmology and Stomatology to Focus on Prevention and Control

The Healthy China initiative advocates for a shift in the healthcare service system from a "disease-centered" to a "health-centered" model. Healthcare institutions will proactively move their focus upstream, transitioning from disease treatment to prevention and control—a trend that will be particularly evident in consumer-driven sectors such as ophthalmology and dentistry.

In ophthalmology, optometric services have emerged as a new growth driver, drawing attention to optometry centers and optometry clinics.

Driven by the dual forces of clinical treatment and consumer demand, refractive surgery and cataract programs once dominated revenue in ophthalmic medical services. Under the influence of market demand and policy directives on myopia prevention and control, optometric services have emerged as a new growth engine for ophthalmology. Eye hospitals are increasingly establishing optometry centers as part of tiered diagnosis and treatment systems, leading to the proliferation of optometry clinics focused primarily on pediatric ophthalmology.

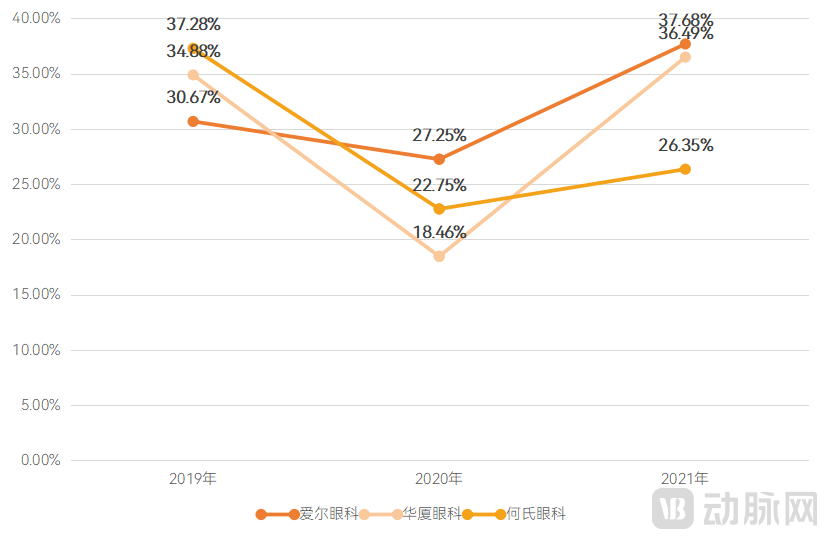

In recent years, the optometry services market has experienced rapid growth, as evidenced by the financial data of publicly listed ophthalmology chains. Building on their historical performance growth rates, these listed ophthalmology chains continue to accelerate the establishment of new optometry service institutions.

Growth Rate of Optometry Service Revenue at Several Ophthalmology Chain Institutions, Data Source: Company Financial Reports or Prospectuses

In the field of dentistry, high-value services such as dental implants and orthodontics are experiencing rapid growth, while comprehensive dental care is extending towards disease prevention.

Currently, dental implants and orthodontics, characterized by high average transaction values, constitute the primary revenue drivers for dental healthcare institutions. Moving forward, these institutions must leverage innovative technologies and service models to prevent and control the occurrence of dental caries at the source.

The “Fourth National Oral Health Epidemiological Survey Report” shows that the prevalence of dental caries among children aged 5 and 12 in China has shown a significant upward trend, increasing by 6% and 10%, respectively. It is imperative to shift the focus of caries prevention and control to earlier stages. Meanwhile, the “14th Five-Year Plan for National Health” proposes strengthening oral health work with an emphasis on the prevention and control of common oral diseases such as dental caries and periodontal disease, aiming to keep the prevalence of dental caries among 12-year-old children below 30%.

Currently, more specialized pediatric dental institutions and comprehensive oral healthcare providers are actively exploring new approaches. For instance, Meowei Dental has intensified its investment in preventive care and basic diagnostic and treatment services, while leveraging digital technologies to build a one-stop platform for lifelong oral health management and tracking. By utilizing data models and information analysis, the platform offers value-added medical services that integrate disease prevention, risk prediction, personalized management, and patient engagement, thereby better promoting prevention over treatment.

Third-Party Medical Services and Capacity Building in Primary Care Institutions: Enhancing the Efficiency of the Healthcare Delivery System

Amid the impact of the pandemic, hospitals at all levels, predominantly public hospitals, have shouldered substantial responsibilities in patient care and epidemic prevention and control. Third-party medical service providers and primary healthcare institutions will further clarify their positioning and assume corresponding responsibilities to enhance the overall efficiency of the healthcare delivery system.

For years, third-party medical services have been a sector strongly encouraged by national policies. Leading third-party medical service providers that possess four key characteristics—standardization, economies of scale, high entry barriers, and replicability—will continue to be favored by the market.

Meanwhile, primary healthcare institutions that focus on high-demand core services, demonstrate strong cost-control capabilities, and play a practical role within the tiered diagnosis and treatment system are better positioned to mitigate objective adverse conditions such as pandemics, thereby maintaining robust operational performance or even achieving growth.

These two types of institutions not only enhance the operational efficiency of the healthcare service system under normal circumstances, but also strengthen its resilience to cope with uncertainties such as pandemics.

"Table of Contents for the 2022 Annual White Paper on Innovations in Healthcare Services"

Chapter 1: New Insights into Healthcare Services in 2022

1.1 Accelerating Volume Expansion and Quality Improvement Remains the Overall Policy Direction, Bringing Major Changes to Surgical Management

1.2 Active Financing in Scarce Specialty Resources Accelerates Consolidation of Physical Medical Institutions

1.3 Consumer Healthcare and Internet Medical Health Show Strong Performance, with a Wave of IPOs

Chapter 2: Interpretation of the Connotation of Innovation in Subsectors

2.1 Expansion of Disease Categories for Multidisciplinary Team (MDT) Care, Exhibiting Online Characteristics

2.2 Process Reengineering: Building Continuous Medical Services Through Whole-Course Disease Management

2.3 The Frequent Emergence of Ecosystem-Based Service Organizations Solves the Challenge of Acquiring C-End Customers

2.4 Expansion of Customer Channels: Broadly Developing the B2B Market Centered on Corporate Health Management

2.5 Under the Trend of Specialized Retail, “Drugs + Services” Has Become Standard

2.6 In the Context of Circulation Market Reshaping, Digital Marketing Deepens Patient Management

2.7 Multi-tiered Payment: Huiminbao and Health Insurance Accelerate Coverage for Non-standard Risks

Chapter 3 Case Studies on Innovation in Medical Services

3.1 Jingli Technology: Multi-Touchpoint Follow-Up Services Enhance Patient Adherence and Reduce Follow-Up Costs

3.2 GuLian Medical: Perfecting a High-Quality Rehabilitation Healthcare System and Accelerating National Comprehensive Rehabilitation Layout

3.3 Youmian: Building a Leading Lifestyle Medicine Brand Centered on Sleep Medicine and Mental Health

3.4 Ping An Health: Continuously Expanding Corporate Client Base and Customizing Personalized Employee Health Management Services

3.5 Youjia Health: Building the “Family Doctor Premium Care” Medical Service System and Customizing Diversified Services for Specific Scenarios

3.6 Meiwei Dental: Upgrading the Digital Platform to Drive Oral Healthcare Services Toward Digital Intelligence

3.7 Yuemi Technology: Integrated Doctor-Patient Solutions to Maximize Patient Benefits and Pharmaceutical Commercial Value

3.8 Yingkang Life: Focusing on Home Scenarios, “Yingkang Digital Intelligence Human” Delivers Hospital-Grade High-Quality Medical and Elderly Care Services

3.9 Renshu Medical: Upgrading Minimally Invasive Techniques, Introducing the Concept of Preemptive Analgesia, and Implementing an International-Standard Healthcare System

Chapter 4 Trends in the Medical Services Industry

4.1 High-quality resources in rehabilitation, medical care for the elderly, and oncology remain scarce and require accelerated supplementation

4.2 Payment Policies May Help Unlock Demand for Assisted Reproductive Technology, with Licensed Institutions Holding Clear Advantages

4.3 Shifting Disease Intervention Upstream: Specialties Such as Ophthalmology and Dentistry to Focus on Prevention and Control

4.4 Third-Party Medical Services and Enhanced Capabilities of Primary Healthcare Institutions Drive Efficiency Gains in the Healthcare Delivery System

The above is an excerpt of the main content from the report. The complete framework of the report is as follows. Scan the QR code to add our assistant and obtain the full report; if you have already added us, please initiate your inquiry proactively.