Yibao Tech: Powering Inclusive Health Insurance Across 50+ Chinese Cities with Three Rounds of Funding in One Year

“There’s no need to introduce Yibao to me; I am well aware of what Yibao does, having experienced it firsthand.”

This is not the first time Li Xinyang has encountered such an interviewee. In recent months, conversations like this have become increasingly frequent in interviews.

The job applicant sitting across from Li Xinyang is from Changsha. In the past few months, his father was hospitalized in the ICU due to a stroke. After medical insurance reimbursement, the out-of-pocket expense for the 300,000 yuan in medical bills would have exceeded 100,000 yuan; however, thanks to Huiminbao (inclusive commercial health insurance), the family’s final out-of-pocket cost was reduced to just over 40,000 yuan.

AndYibao Technology, is precisely a party involved in the design and operation of Changsha Huiminbao, andIt is a business participant in the “Huimin Bao” (inclusive health insurance) programs across more than 50 cities nationwide. In commercial terms, leveraging digitalization, large-population technologies, and an operational platform, Yibao Technology has built a comprehensive “Huimin Insurance” service platform to promote the universal accessibility of insurance and healthcare, thereby supporting the development of multi-tiered urban medical security systems.

Frankly speaking, Yibao Technology has indeed achieved an impressive “track record,” not onlyServing over 25 million insured users, partnering with more than 30 insurance companies, and achieving a premium volume of RMB 2 billion, the company has also entered into a strategic cooperation with the Xuhui District Government of Shanghai and completed its Series A+ financing round by the end of 2022.

Yet, somewhat surprisingly, the company is quite young—founded in 2021, Yibao Technology became a leading domestic technology platform for Huiminbao insurance in less than two years.

In this regard, Li Xinyang, co-founder of Yibao Technology, candidly stated: “This is attributable to the rapid development of the Huiminbao industry in recent years, driven by policy guidance and collaborative efforts across the sector, as well as the industry expertise accumulated by our core team over many years, coupled with Yibao Technology’s digital insights and large-scale population operational capabilities. These advantages have enabled us to gain user trust more quickly, laying a solid foundation for our future growth.”

Indeed, the surging popularity of Huimin Bao over the past two years has been evident to all, and Yibao Technology’s achievements are clearly reflected in the aforementioned data. But why has a startup founded only two years ago managed to stand out? Let us begin with Yibao Technology’s founding team.

During her academic years, the founder of Yibao Technology participated in a research project involving a Shanghai breast cancer follow-up cohort. Witnessing firsthand how some patients were forced to abandon treatment or unable to opt for superior therapeutic regimens due to financial constraints, she recognized the critical importance of healthcare payment issues and subsequently made a career shift to join Ping An Health Insurance Technology.

During his tenure at Ping An Health Insurance Technology, the founder met the other founders of Yibao Technology. The founding team also gained exposure to “inclusive” health insurance and participated in the development, design, and promotion of specialized drug insurance products. As they steadily accumulated experience, they developed a deeper appreciation for the value of “inclusive” health insurance.

Taking Huiminbao as an example, from a national perspective, Huiminbao serves as an “intermediate layer” between basic medical insurance and reimbursement-based health insurance products such as “Special Drug Insurance” and “Million-Yuan Medical Insurance.” It effectively covers medical expenses that fall outside the National Reimbursement Drug List but are not included in “high-end” health insurance plans (characterized by higher premiums and broader coverage). This plays a crucial role in building China’s multi-tiered medical security system and helps reduce the incidence of poverty caused by illness to some extent. Therefore, the development of Huiminbao has received strong policy support and guidance.

On the other hand, for ordinary residents, Huiminbao (city-specific supplemental medical insurance) can provide secondary medical coverage beyond the scope of basic medical insurance, thereby alleviating out-of-pocket financial burdens. Furthermore, to enhance policyholders’ sense of value, many Huiminbao products have added health management and disease screening services. Even healthy individuals can assess their health status at a lower cost and access professional health management services upon enrollment.

Therefore, guided by policy and amid insufficient growth momentum for “high-end” health insurance, Huimin Bao has experienced explosive growth in recent years.

According to the “2022 Knowledge Graph of City-Specific Commercial Medical Insurance (Huiminbao)” released in December 2022 by the Center for Insurance Innovation and Investment Research at Fudan University’s Fanhai International School of Finance, as of December 1, 2022, a total of 263 Huiminbao products had been launched, covering 29 provincial-level administrative regions. Moreover, as early as the end of 2021, Huiminbao had already enrolled 142 million participants, with substantial growth observed in 2022.

While the founder and other co-founders of Yibao Technology were building their careers at Ping An Technology, Li Xinyang, another co-founder of Yibao Technology and a serial entrepreneur who graduated from the Department of Computer Science and Technology at Tsinghua University, was continuously reflecting on the social value of entrepreneurship. From mobile internet to new retail, and then to medical artificial intelligence, Li Xinyang’s entrepreneurial endeavors have consistently aligned with the industry’s focal points at each stage. Amidst the hustle and bustle, this entrepreneur couldn’t help but ponder: Could we do something more meaningful?

The booming Huiminbao insurance has fully aligned with Li Xinyang’s aspirations.

“In the healthcare ecosystem, health insurance serves as the hub, not only commanding greater appeal and influence among a broader population but also exerting a strong connective role across the pharmaceutical industry chain,” said Li Xinyang. “Therefore, I proactively transitioned from an industry that initially chased hot trends to one that places greater emphasis on value creation.”

When the two founders came together, a health insurance technology company was established with the vision of “making inclusive health insurance accessible to more people.”

Yibao Technology has focused on “city-customized commercial insurance,” namely Huiminbao, from the very beginning.

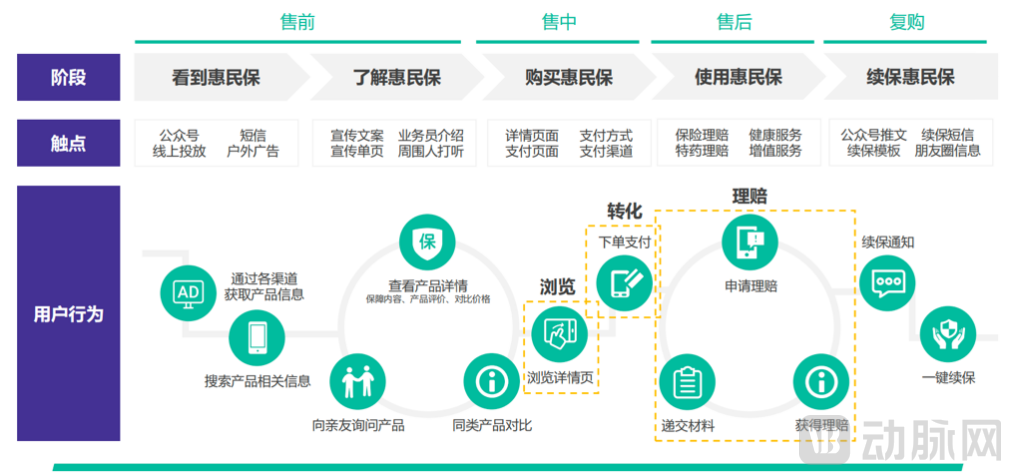

On one hand, leveraging data insights, analytical capabilities, and large-scale population management technologies, Yibao Technology can provide a comprehensive, one-stop suite of services for local Huiminbao (inclusive health insurance) products, covering actuarial product design, digital marketing, intelligent underwriting, end-to-end claims processing, sales and marketing, and after-sales support.

On the other hand, Yibao Technology collaborates with insurance companies, innovative pharmaceutical firms, and innovative healthcare service providers to offer insured individuals a range of health and medical services, including screening, internet-based healthcare, rehabilitation and nursing care, and consumer healthcare.

Overall, Yibao Technology’s business in the Huiminbao sector can be summarized into two aspects—technology and services.

In this regard, during the interview, Li Xinyang first introduced to VCBeat the technological attributes of Huiminbao. The so-called technology refers to digitalization.

“Huiminbao is a natively digital insurance product.”Li Xinyang stated,The term “born-digital” primarily encompasses two meanings: Hui Min Bao has been highly digitalized since its inception, and the entire process—from product design and actuarial risk control to marketing and claims settlement—is fully digitalized.

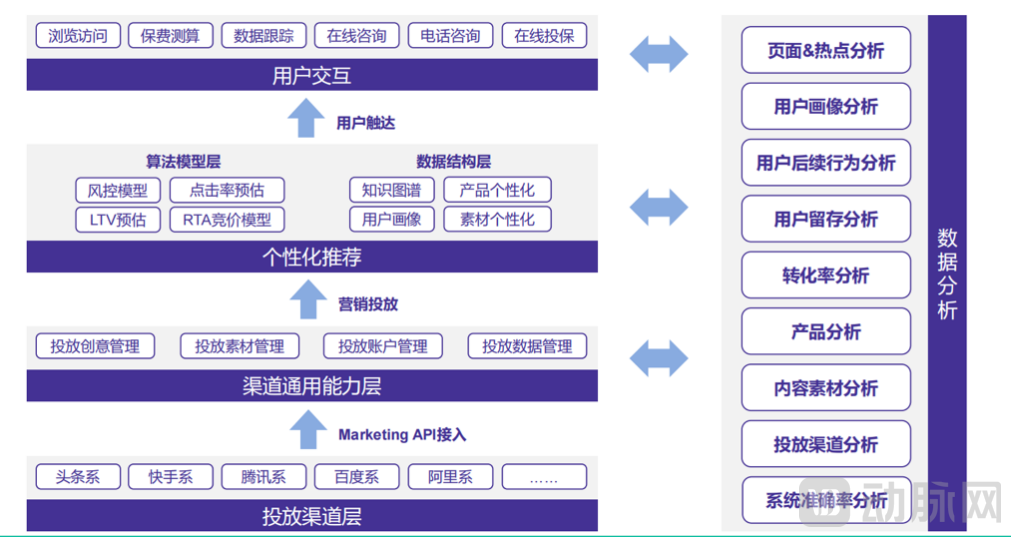

And in accordance with the meaning of native digitalization,Huiminbao technology platform companies should compete on AI algorithm capabilities such as actuarial risk control, underwriting and claims adjudication, product design capabilities, and digital marketing capabilities (large-population management capabilities).

How to Evaluate Yibao Technology’s AI Algorithm Capabilities and Product Design Competence? Let’s First Focus on Yibao Technology’s Team.

As previously mentioned, the founders of Yibao Technology not only possess medical backgrounds but also have work experience at well-known insurtech companies in the industry. The other founder has been deeply involved in the computer industry for many years. After the strong alliance of the two founders, they have also gathered a group of talents who graduated from prestigious universities and have rich industry experience.

VCBeat has learned thatAmong the 100 employees of Yibao Technology, approximately 15% are graduates of Tsinghua University, Peking University, Fudan University, and Zhejiang University, with holders of doctoral and master’s degrees also accounting for more than 15%.

Not only that,Yibao Technology’s team includes many members from well-known domestic insurance companies such as Ping An Insurance and ZhongAn Insurance; major internet or medical device companies including ByteDance, Meideng Technology, Baidu, Alibaba, and Infervision; as well as healthcare service providers like Shanzhen and Guokang.The team is not only highly experienced but also possesses diverse capabilities.

Prior to the launch of a Huiminbao (inclusive commercial health insurance) product, the acquisition of real-world data serves as the foundation for all subsequent processes and is essential for bringing such a product to market. However, according to Li Xinyang, this phase typically receives robust support from local healthcare security administrations under policy guidance and promotion. Consequently, in this regard, insurtech companies and insurers involved in the design and operation of Huiminbao products start on an equal footing.

Not only that,At the pure technology level, the systems and technologies used across the industry are largely consistent. What truly differentiates players is their accumulated industry experience.

“Fundamentally, the systems and software used in the industry are all general-purpose. However, as the number of clients and projects grows, system functionalities and configurations must undergo iterative upgrades. For instance, determining how to segment insured users, designing tailored marketing strategies for different user personas, and optimizing recall rate statistics all require extensive industry expertise,” said Li Xinyang.

Moreover, during the interview, Li Xinyang cited another example to illustrate this point: concurrency issues are highly likely to arise between consumer-facing systems and agent systems during policy renewal. Only enterprises that have encountered such problems have the opportunity to address them; “however, if a company has not experienced such scenarios, it will be at a loss when these issues occur. In reality, only a handful of systems in the market have truly been tested and refined. Fortunately, Yibao is one of them.”

Compared with various “high-end” commercial health insurance products, Huiminbao has a larger and broader insured population base. However, given its “public welfare” nature, the profit margin for insurance companies and even third-party service providers is limited. This necessitates that third-party service providers involved in operations must possess strong “large-scale population management capabilities.”

In simpler terms, it meansFaced with a population of millions in a single city and limited profit margins, enterprises must consider how to reduce costs and improve efficiency. This is what is known as "mass population management capability." Taking marketing as an example, companies need to consider channel coverage and management, ROI evaluation, assessment of coverage effectiveness, and strategy adjustment, among other factors.

In response, Yibao Technology has developed a comprehensive marketing strategy that covers the entire user journey—from awareness and consideration to purchase, usage, and policy renewal. This strategy spans hundreds of channels, including those under the Toutiao, Kuaishou, Tencent, Baidu, and Alibaba ecosystems, and has established a relatively mature and robust marketing mechanism.

Moreover, this marketing mechanism has proven effective. According to Li Xinyang, “In the Hui Min Bao projects participated in by Yibao, many cities have actually achieved an enrollment rate of 15%-25%., i.e., assuming the city has a population of 1 million, 150,000 to 250,000 residents are insured, and 60%–70% of the population have a thorough understanding of the city’s Huimin Bao.

While requiring enterprises to possess the capability for “large-population management,” Huiminbao also demands strong data insight capabilities. In this regard, we can assess Yibao Technology’s competencies through its new product development and design, as well as its evaluation of service offering supply.

One of the foundational elements in the development and design of “Basic” Huiminbao is local medical insurance data, butAfter the iteration of Huiminbao products, what truly holds value is the claims data of these Huiminbao products.For Yibao Technology, which has participated in the design and operation of inclusive supplementary medical insurance (Hui Min Bao) projects in more than 50 cities, its accumulation of claims data is substantial, enabling a clear understanding of the health profiles of diverse local populations.

Therefore,Leveraging data insights and demographic profiling, Yibao Technology has partnered with insurance companies to launch inclusive commercial health insurance products—such as inpatient medical allowance insurance and student/child accident insurance—tailored to diverse population segments. Built upon the foundation of basic Huiminbao (city-specific supplementary medical insurance), these offerings have achieved notable success.

For example, Yibao Technology’s “Dongguan Citizen Insurance · Family Plan” ultimately secured over 22,000 policies, generated more than RMB 14 million in premium income, and added over 10,000 new followers to its official WeChat account. Meanwhile, the Guangdong Family Plan project accumulated RMB 800,000 in premiums within just four days of launch, with its policy conversion rate rising to 20.8%.

Not only that, based on insights into user personas,In addition to offering the internet-based medical care and health management services typically covered by standard Hui Min Bao insurance, Yibao Technology has also launched screening services for conditions such as diabetes, osteoporosis, and breast cancer.

On the one hand, adding such screening services can enhance product perception among insured individuals, especially healthy populations, laying the groundwork for policy renewals and subsequent access to medical consultations, treatments, and health management services (e.g., in cases where users are diagnosed through screening). On the other hand, these screening services target diseases with high incidence rates and frequent medical visits, which can invisibly expand the touchpoints between Huiminbao (city-specific supplementary medical insurance) and residents, thereby broadening its customer base.

Notably,At the end of 2022, Yibao Technology completed its Series A+ financing round, led by China Resources Pharmaceutical Group, China Resources Pharmaceutical Commercial Group, and China Resources Sanjiu, with participation from existing investors Boyuan Capital, SDAO Capital, and Yuanyi Capital. In the future, leveraging China Resources Pharmaceutical’s strengths in pharmaceuticals, pharmacy networks, and traditional Chinese medicine (TCM), Yibao Technology will launch services including specialty drugs and TCM.The entry of strategic investors not only recognizes Yibao Technology’s past achievements but also injects “new momentum” into its next-stage growth and the enhancement of its business ecosystem.