Fate Therapeutics Ends Collaboration with Johnson & Johnson, Refocuses on Core iPSC-Derived Cell Therapy Pipeline

Fate Therapeutics

Cellular Immunotherapy Developer

Another “breakup” hits the cell therapy sector. On January 5, iPSC star company Fate Therapeutics (NASDAQ: FATE) announced that it had rejected a proposal from Janssen Pharmaceuticals, part of Johnson & Johnson, with all collaborations set to end in the first quarter of 2023.

The following day, Fate Therapeutics’ stock price plummeted by 48%. The company decided to discontinue the majority of its pipeline programs and lay off more than 50% of its workforce, with cash on hand expected to last until 2025.

Fate Therapeutics reached its all-time high stock price of $121 in January 2021, with a peak market capitalization exceeding $10 billion. As a benchmark for numerous iPSC companies, it once had six investigational projects simultaneously enter Phase I clinical trials. VCBeat has repeatedly analyzed Fate Therapeutics’ growth trajectory and its pipeline progress.

In a similar vein, Century Therapeutics recently announced that it would lay off approximately 25% of its workforce and deprioritize the development of CNTY-103 for glioblastoma, as well as its discovery programs for hematologic malignancies; TCR2 Therapeutics stated that it would reduce its staff by 25% and scale back its ongoing clinical trials.

From high expectations to the current development impasse, it is not only Fate, with its valuation plummeting to just $400 million, that has suffered; the entire cell therapy sector has faced significant setbacks over the past year. News of pipeline cuts and layoffs has emerged one after another from various companies, with some pessimistic voices even suggesting that the entire strategic direction of cell therapy may have been misguided.

Is “brutal” really the right word to describe cell therapy over the past year? Let’s first revisit the termination of the collaboration between Fate Therapeutics and Johnson & Johnson.

Rejecting a "Fate" That Is Co-opted

The collaboration with Janssen represents the first partnership that Fate Therapeutics has entered into with a major pharmaceutical company. Janssen will contribute its proprietary antigen-binding domains for four tumor-associated antigen targets, while Fate will leverage its iPSC platform to research and develop iPSC-derived CAR-NK and CAR-T cell candidates.

The primary pipeline resulting from the collaboration between the two companies is FT555, an iPSC-derived CAR-NK cell candidate targeting GPRC5D. Prior to the termination of the partnership, the companies were preparing an Investigational New Drug (IND) application to advance first-in-human clinical studies of FT555 as a monotherapy and in combination with the CD38-targeting monoclonal antibody daratumumab for the treatment of multiple myeloma.

Everything appears to be going smoothly, and Fate Therapeutics is also buzzing with activity.

However, the collaboration between the two parties may have encountered difficulties, as no public results have been released for their CAR-T cell candidate products. The development and commercialization of iPSC-derived T-cell therapy candidates present significant challenges. iPSC-derived T cells do not undergo thymic selection and are therefore immature, akin to inexperienced soldiers. Although these T cells possess cytotoxic activity, they still require further “training” to enhance their killing potency, a goal that remains challenging to achieve with current technologies.

Industry insiders speculate that Fate Therapeutics is facing technical bottlenecks in its delivery to Janssen. Particularly, after the departure of core scientists represented by Dan Kaufman, the company has encountered significant challenges in sustaining R&D innovation. Meanwhile, slow progress in process development and capacity expansion has led Fate Therapeutics to part ways with major pharmaceutical companies under pressure.

In his statement on the matter, Fate Therapeutics’ President and CEO Scott Wolchko highlighted several key points: the company was unable to “reach an agreement” on the collaboration proposal put forward by Janssen, and it would “prioritize” its own clinical programs.

Industry insiders interviewed by VCBeat’s New Medicine channel stated that the termination of the partnership appeared to be a proactive choice by Fate Therapeutics to avoid being constrained by large pharmaceutical companies. It is possible that Janssen proposed terms unacceptable to Fate, potentially including the transfer of Fate’s technology platform.

Fate’s technology represents the culmination of years of corporate accumulation, with its iPSC platform backed by an intellectual property portfolio comprising over 300 issued patents and 150 pending patent applications. Setbacks in T-cell research and development have not hindered its progress in other areas, such as NK cells; therefore, Fate is not inclined to “put itself up for sale.”

The series of data demonstrated by the company in its early stages has gradually paved a way for iPSC-NK cell therapy through previously uncharted territory. The product offers the cost advantage of manufacturing off-the-shelf cell therapy products akin to antibody production, and its capacity for repeated dosing expands the scope of existing cell therapies. This has garnered widespread market recognition and empowered the company to confront greater uncertainties with confidence. Although there have been minor flaws in recent clinical trial designs, these do not overshadow the overall merits, and the future remains promising.

In collaborations with a single multinational corporation (MNC), biotech companies often face additional demands and acquisition pressure from the MNC when milestone progress falters, IND submission deadlines loom large, and pipeline uncertainties persist. While some biotechs choose to compromise, Fate Therapeutics is clearly not among them.

As of the end of 2022, Fate Therapeutics had $475 million in cash on its balance sheet, sufficient to sustain the company for three years following a series of streamlining measures. While a three-year cash runway is not particularly ample for an ambitious biotech company, it does provide Fate with enough flexibility to retain its most promising pipeline assets and achieve further proof-of-concept (PoC) for its products.

Leaving Behind Best-in-Class, Fate Remains the Pioneer

In fact, this is not the first time Fate Therapeutics has faced such a situation.

Fate Therapeutics was initially focused primarily on adult stem cell regeneration research. After eight years of R&D, its adult stem cell therapy ProHema, which had advanced to the clinical stage, was discontinued by the company in late 2015. The company’s stock price plummeted to rock bottom, bringing it to the brink of bankruptcy; it barely survived for two years by relying on private placements of shares and debt financing. In 2016, Fate Therapeutics’ stock price fell as low as $1.46 per share.

Fortunately, Fate Therapeutics has consistently invested in its iPSC-derived cell platform and initiated a collaboration with the University of Minnesota in 2015 on iPSC-derived NK cells, enabling the company to recover during challenging times.

Fate, which has even executed pivot strategies for survival, is certainly capable of cutting costs to survive.

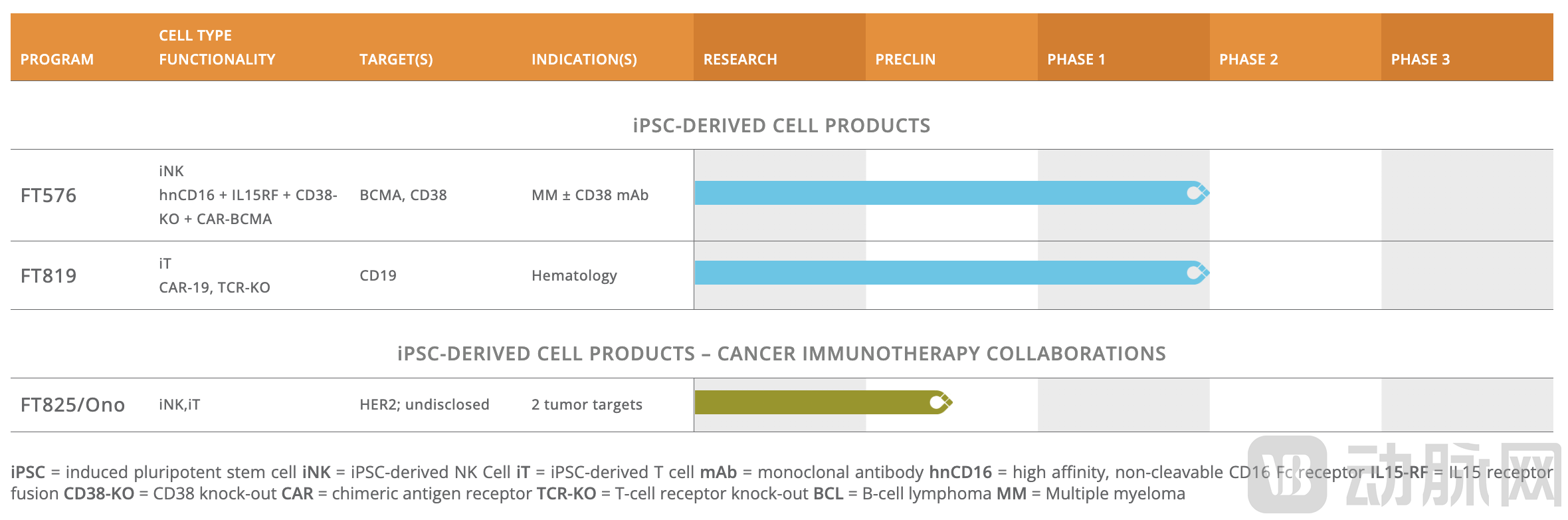

Currently, Fate Therapeutics’ official website lists only three pipelines: multiple myeloma (FT576 ± anti-CD38 monoclonal antibody combination), B-cell lymphoma (FT819), and solid tumors (FT825). The two collaborative projects with Janssen have been completely discontinued, while the joint development partnership with Ono Pharmaceutical continues.

Fate Therapeutics’ Pipeline Displayed on Its Official Website

Rather than calling it a “warrior severing his own wrist,”Rather, this represents a rapid pipeline optimization by biotech companies amid tight funding: retaining only best-in-class (BIC) assets and those with high certainty, while swiftly discontinuing “transitional” pipeline candidates (non-BIC) that have already yielded preliminary results, thereby completing resource reallocation.

Looking back at the evolution of Fate Therapeutics’ pipeline, it has been a journey of pioneering exploration, akin to crossing a river by feeling the stones.

(1) FT500 was the first iPSC-derived NK cell product to enter clinical trials, demonstrating safety but only modest efficacy; Fate Therapeutics announced the termination of its development.

(2) Fate Therapeutics subsequently introduced the improved product FT516. FT516 cells demonstrate superior therapeutic properties in vitro, including sustained CD16 expression, enhanced antibody-dependent cellular cytotoxicity (ADCC) of NK cells, and reduced suppression of NK cells by the tumor microenvironment. In combination with rituximab, FT516 shows preliminary efficacy comparable to CAR-T therapy, with a significantly better safety profile than autologous CAR-T; however, its long-term efficacy is inferior to that of CAR-T.

(3) FT596 incorporates IL-15RF and CAR-19. Clinical study data demonstrate that monotherapy with this agent exhibits durable tumor clearance and prolonged in vivo survival.

(4) Although FT538 lacks CAR expression, CD38 was knocked out on the basis of FT596, and it was found that combination therapy with a CD38 monoclonal antibody yielded superior therapeutic efficacy.

At this point, Fate Therapeutics has identified the optimal combination of iPSC-NK cell modifications currently available: CD16 engineering, incorporation of IL-15RF, CD38 knockout, and addition of a CAR cytotoxicity domain. Based on this platform, Fate Therapeutics launched FT576. FT576 is a BCMA-targeted CAR-NK cell therapy for the treatment of relapsed/refractory multiple myeloma.

A series of modifications, including CD16 engineering, along with BCMA-directed CAR targeting of plasma cells, enhance the potency and durability of FT576 and enable multi-antigen targeting when used in combination with antibodies. Furthermore, BCMA is a well-validated target, offering biotech companies greater certainty at this stage.

Through the continuous advancement of clinical trials over the past few years, Fate Therapeutics has identified its optimal pipeline to date. Given that FT516, FT596, and FT538 are transitional products exploring gene-editing strategies and entail high clinical trial costs, it is reasonable for Fate Therapeutics to discontinue these “transitional” candidates, along with other NK cell pipelines carrying target-related risks, following the loss of support from Janssen, while retaining only FT576.

Another retained in-house pipeline, FT819, is indicated for the treatment of B-cell lymphoma. A key reason for its retention is that it offers greater certainty and a higher success rate compared to solid tumors.

Fate has temporarily abandoned its diversified strategy and is striving for focused breakthroughs and rapid validation. The dose-escalation study of FT576, administered as monotherapy and in combination with CD38-targeted monoclonal antibody (mAb) therapy across multiple doses, will continue. Clinical research on FT819 will focus on evaluating standard single-dose regimens versus novel split-dosing schedules. If the company can leverage its remaining cash to clinically validate both pipelines and advance them to the threshold of commercialization, it will successfully navigate another critical survival cycle, likely attracting interest from another multinational corporation (MNC).

Fate Therapeutics remains the pioneer, boldly advancing its best-in-class offerings by leveraging cutting-edge technology.

“In response, an entrepreneur in the iPSC sector commented, ‘iPSC represents a wholly new track, and Fate Therapeutics has single-handedly propelled it to its current stage of development; encountering technical challenges is therefore quite normal. The iPSC field is advancing, and I believe it is now entering the deep-water zone.’”

Some investors also commented, “If Fate Therapeutics is truly on the right track and current data looks promising, its stock price will rebound once its product is developed.”

True Gold Fears No Fire: Stock Prices Are Not Necessarily the Bellwether for Biotech Companies

The precipitous drop in market capitalization reflects the broader predicament facing the cell therapy sector, with most cell therapy companies experiencing declines of over 80% from their peak valuations; Fate Therapeutics’ stock price has fallen to below $6.

However, stock prices reflect investors’ expectations for biotech companies and are not necessarily a barometer of their performance.

Over the past year, many pioneer companies in novel drug modalities have suffered significant setbacks, including Rubius in red blood cell therapy, Carisma in CAR-M, Silverback in ISAC, and Instil in TIL therapy. While the scientific concepts behind companies like Rubius are compelling, the harsh reality of biotech is that a product holds no value until it is successfully developed.

In the current environment, clinical validation of products and their ability to truly address clinical needs are paramount. During a market downturn, negative news is amplified excessively. The over-optimism of the past created a bubble, and the ongoing process of deflating this bubble is both healthy and necessary.

Fate Therapeutics’ CAR-NK cells continue to offer fundamental advantages, including a favorable safety profile, lower costs, and the characteristics of off-the-shelf products, making clinical exploration worthwhile. If Fate Therapeutics and other iPSC-based companies can successfully develop products targeting major disease indications, their stock prices are bound to return to high levels, much like Moderna’s rise to prominence with its mRNA vaccines during the COVID-19 pandemic. Of course, Moderna’s success was inextricably linked to the infectious drive of its CEO, Stéphane Bancel, as well as its flexible and bold negotiations and collaborations with various multinational corporations (MNCs).

Although Fate has displayed a somewhat unyielding stance toward MNCs on this occasion, its ability to reach its current position undoubtedly reflects relatively strong external operational capabilities. Otherwise, it would not have emerged as a pioneer in translating iPSC-based products from the laboratory stage to industrially manufactured cell therapies, a process that requires coordinated collaboration among regulatory authorities, the pharmaceutical industry, and the scientific research community.

“With every company engaged in cutthroat competition, the industry’s margin for error has shrunk, leading to the current landscape,” a senior investor told VCBeat New Medicine. “The iPSC field remains highly promising, with substantial room for growth. Currently, therapeutic outcomes in tumor immunology and regenerative medicine—such as for Parkinson’s disease, diabetes, and osteoarthritis—are encouraging. An outstanding platform-based biotech company must not only have products that achieve breakthroughs in specific areas but also possess robust platform development capabilities. This will provide the necessary resilience to hedge against risks in today’s uncertain and high-risk environment.”

Meanwhile, leading companies such as Fate Therapeutics are scaling back operations and facing tight cash flows.This also presents an opportunity for domestic cell therapy companies, as startups can leverage this window to capitalize on the cost and efficiency advantages of clinical trials and compete at a world-class level.

He Zhiyong, CEO of iCell Bioscience, an iPSC company, stated, “China’s dual-track regulatory model, based on risk assessment and stratification, has fueled the robust growth of the CGT industry and will inevitably continue to support Chinese innovative drug companies in pursuing a differentiated development path in frontier fields such as iPSCs. In terms of addressing scientific challenges, Chinese companies with core foundational technologies are even leading their U.S. counterparts in these underlying technologies. Pioneers like Fate Therapeutics have paved the way, highlighting the scientific issues and potential risks that need to be addressed in product development within this sector. As newcomers to the industry, we respect the warnings offered by these pioneers and are committed to carving out our own unique path for Chinese biotech firms.”

“As the industry flourishes, greater focus must be placed on the technology itself. Due to the complexity of manufacturing processes, iPSC-derived products impose stringent requirements on the quality and viability of reprogrammed cells; overlooking this aspect will pose significant crises and risks in future industrialization.”

Over the past two years, China has witnessed a surge in iPSC financing events, underscoring strong market and investor confidence in this emerging technology and high expectations for high-quality products. This trend also presents Chinese companies with an opportunity to overtake competitors on the curve in the future.

Partnership breakups, business adjustments, and declining market capitalization are not the exclusive “fate” of Fate Therapeutics; navigating hardships is the “fate” of scientific research and all biotech companies.

True gold fears no fire; look past current stock prices. Time will filter out superior products, and the market will ultimately pay for high-value offerings.