Startups Thrive Amid Market Challenges as China's Secondary Market Shows Signs of Recovery: 2022 Global Healthcare Investment Report

Core Viewpoints

I. Affected by the macroeconomic environment, global healthcare financing cooled down overall in 2022; there were 164 financing deals exceeding $100 million in 2022, less than half of the 2021 figure, with capital consolidation easing and the pace of market differentiation slowing.

II. The financing boom in 2021 was plagued by overvaluation, leading to a slowdown in funding for digital health companies in 2022; within the biopharmaceutical and medical device sectors, innovative projects with proprietary technologies and substantial market potential are more likely to stand out in the early-stage market.

3. The global AI-driven drug discovery sector continues to demonstrate strong momentum; following the new round of drug review and approval reforms, the full implementation of the Marketing Authorization Holder (MAH) system in China has brought new development opportunities to the CXO industry; in 2021, the first domestically produced artificial heart with complete independent intellectual property rights was approved in China, drawing significant capital attention to the artificial heart sector in 2022 and establishing it as a promising long-term investment track; tight overseas medical resources have spurred growth in in-hospital digital collaboration and out-of-hospital remote care, while the head effect has become evident in China’s internet-based medical education and training sector.

IV. Investment institutions worldwide continue to maintain their focus on innovative drug-related companies; domestic investment firms have repeatedly increased their stakes in early-stage startups within the biopharmaceutical sector.

V. Healthcare financing heats up significantly in Israel and India, while the spillover effects of Jiangsu’s biopharmaceutical industry hub become evident.

6. Both the number and value of global IPOs declined; in the second half of 2022, there were clear signs of a rebound in China’s secondary market.

I. Trends in Global Healthcare Industry Financing from 2011 to 2022

1.1 Global Healthcare Financing Volume in 2022 Ranks Second Highest in History

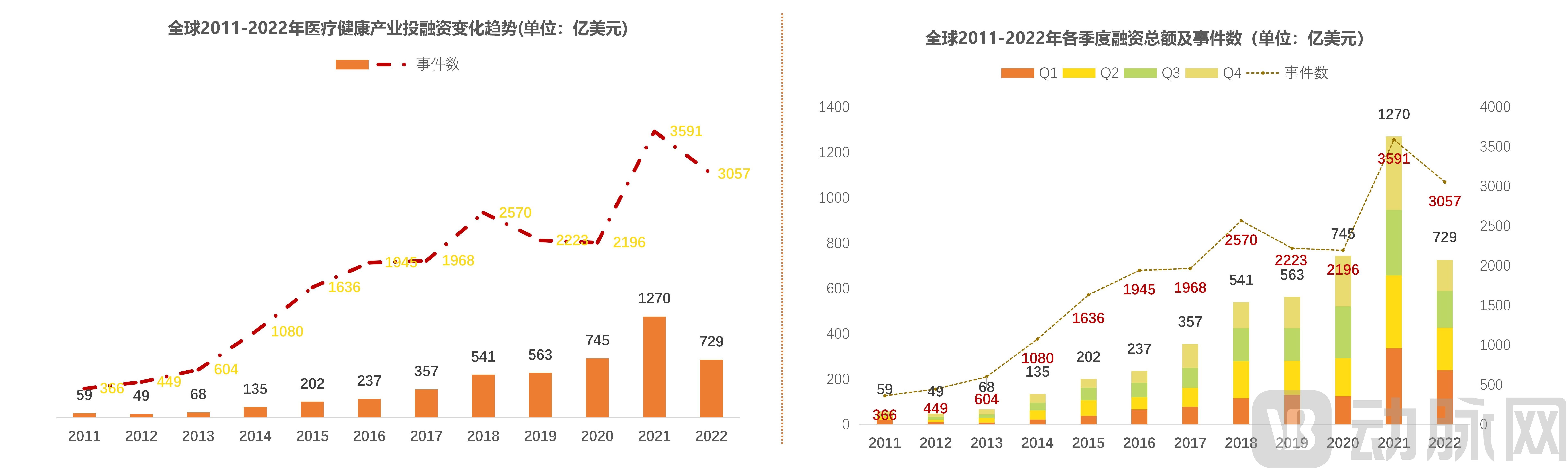

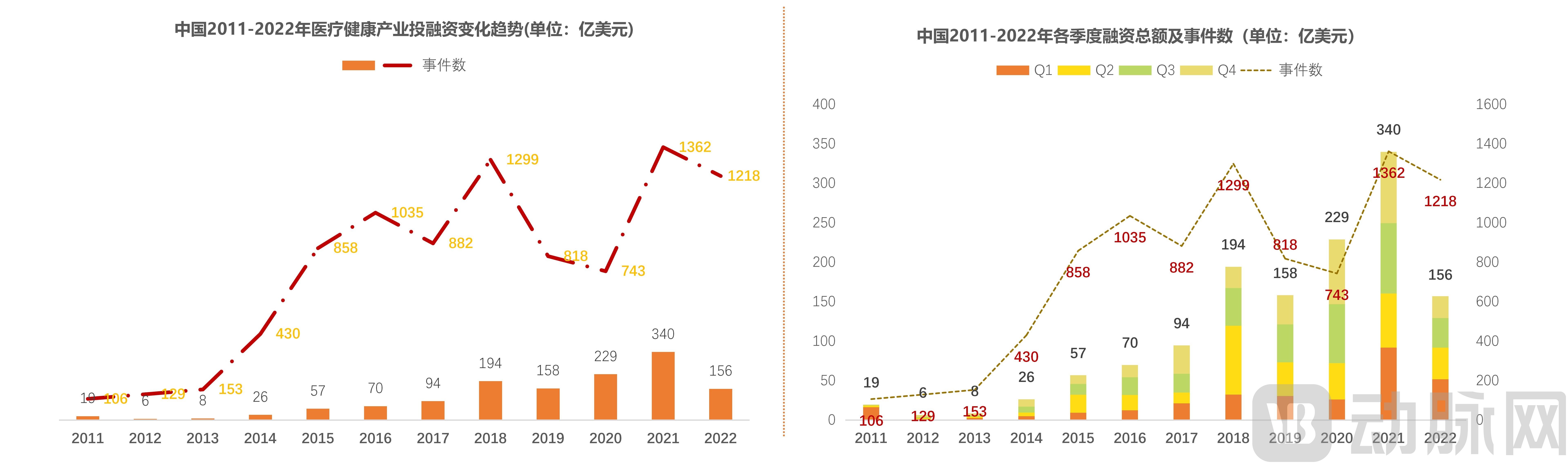

In 2022, there were 3,057 financing deals in the global healthcare industry, representing a decline from 2021. The total funding amount reached $72.9 billion (approximately RMB 502.9 billion), ranking third highest in history, but falling short of the levels seen in 2020 and 2021, indicating an overall trend toward caution and prudence. Although the total funding in 2022 was close to that of 2020, the capital landscape differed significantly.

In contrast to the pronounced herd investing seen in 2020, investors shifted their strategy in 2022 toward “early-stage and small-scale investments.” This trend is common in the hard-tech sector: given the high valuations of late-stage projects and subdued market expectations, institutions are more inclined to seek opportunities in early-stage ventures. Nevertheless, startups dedicated to addressing unmet needs in the healthcare industry are likely to attract capital attention first, enabling innovative companies to further penetrate blue-ocean markets where competitive landscapes have not yet solidified.

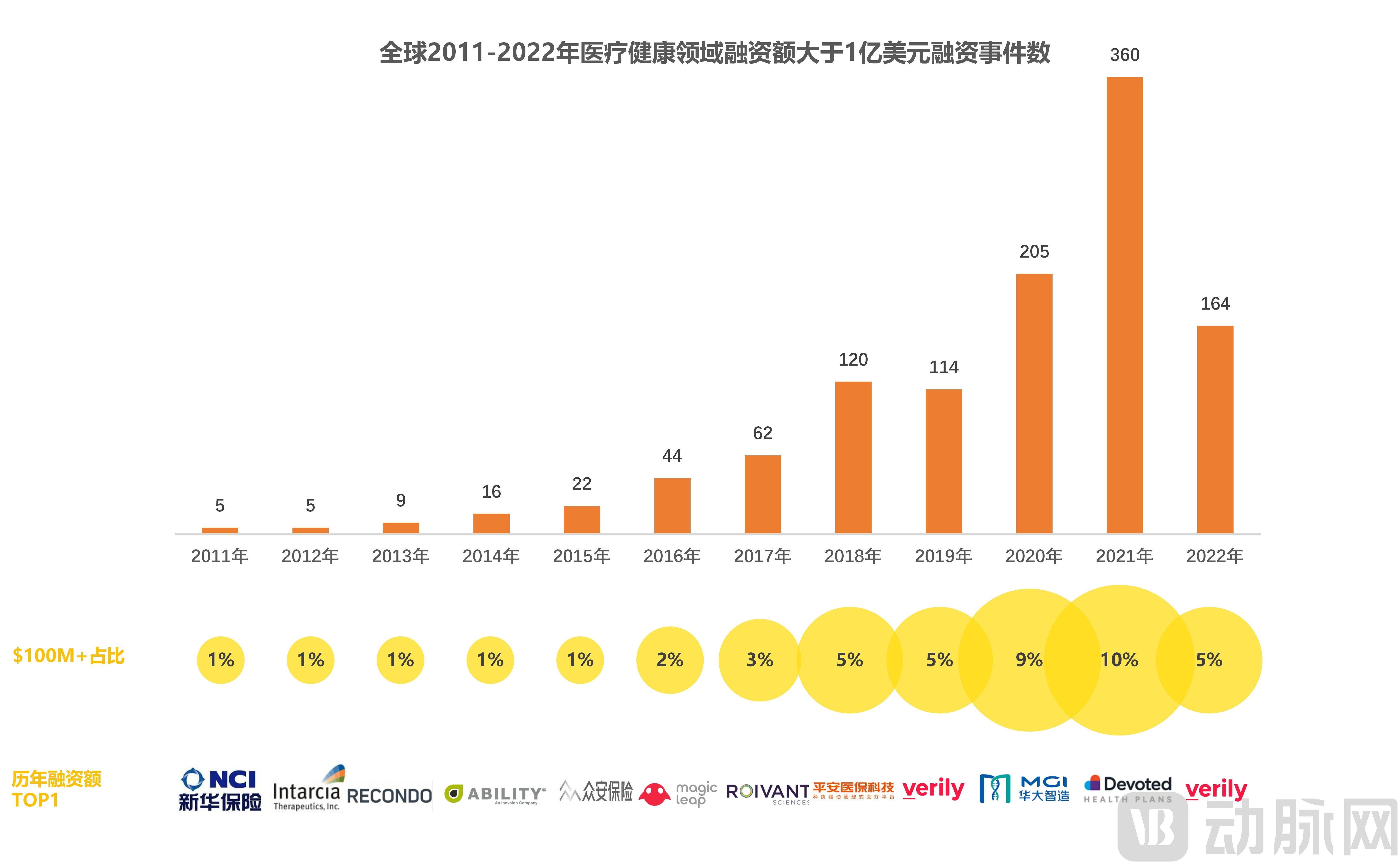

1.2 164 financing deals exceeding $100 million throughout the year, with loosening of capital concentration

In 2022, there were 164 deals with single-round financing exceeding $100 million, approximately half the number in 2021, indicating a notable easing of capital concentration.

According to statistics, the total financing raised by these 164 companies exceeded $29.7 billion. Compared with 2021, when nearly half of the capital invested in the healthcare industry was concentrated in less than 10% of enterprises, the distribution of funding in 2022 was more dispersed and diversified.

Among the top 10 companies in financing, five are biopharmaceutical firms. These five companies are primarily engaged in pharmaceutical CXO services.

As in 2021, the global economic outlook remained weak, but the defensive nature of the healthcare industry manifested differently, with less tight-knit cohesion. Meanwhile, 2022 continued the trend set in 2021, as market differentiation slowed further. The number of companies completing seed, angel, and Pre-A financing rounds increased significantly compared to 2021.

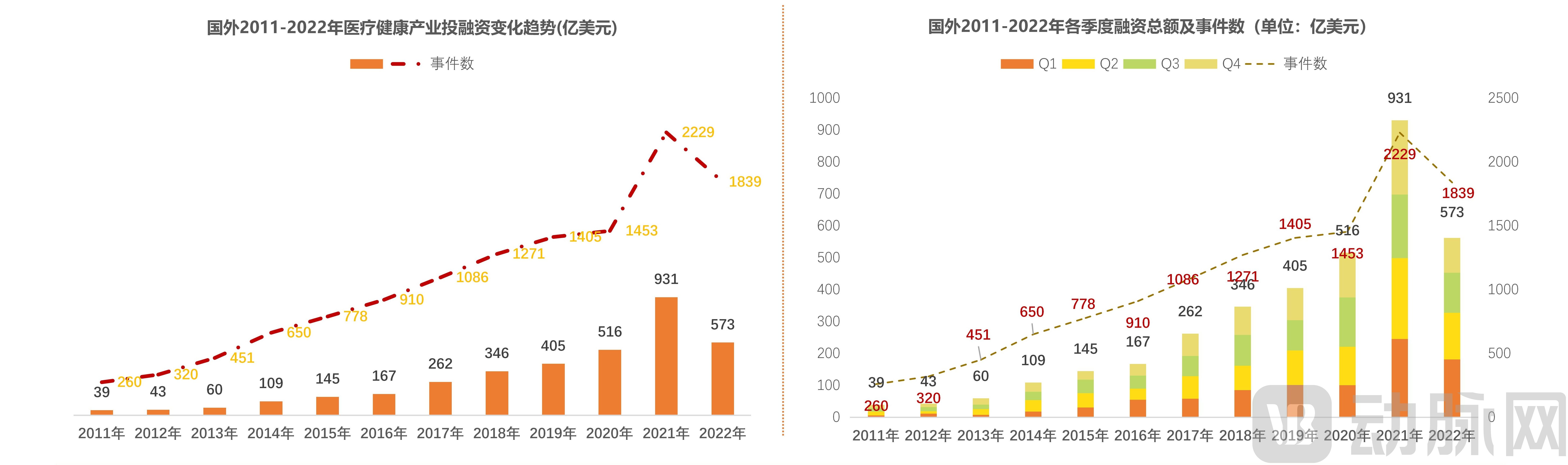

1.3 In 2022, the growth rate of overseas healthcare investment and financing declined, with both investors and growth-stage companies becoming increasingly cautious

The cautious stance toward overseas investment in 2022 interrupted the stable growth of financing that had continued for 11 consecutive years since 2011. However, it should be noted that, in addition to investors’ concerns, companies in their growth stage also postponed transactions due to factors such as a less-than-expected financing environment and availability of capital.

Furthermore, the COVID-19 pandemic catalyzed digital health financing in 2020 and 2021, encouraging more investors to scale up their investments and assume greater risks. Additionally, the Federal Reserve’s continued monetary easing policy in 2021 further drove up valuations in the healthcare industry, particularly for companies in the digital health sector.

Therefore, the downturn in 2022 was likely paving the way for a gradual recovery of capital in the following quarter: investors continued to accumulate cash reserves and prioritized competitive enterprises.

1.4 In 2022, financing activities among startups in China remained active, gradually extending into high-tech sectors

Although the total financing amount fell short of 2021 levels, China’s healthcare sector witnessed 180 early-stage investment and financing events (including seed, angel, and Pre-A rounds) in the first half of 2022, with cumulative funding nearing $900 million. These figures closely approach the full-year totals for 2021, which comprised 296 financing deals exceeding $1.194 billion (approximately RMB 7.76 billion). Driven by the demand for commercializing scientific achievements and domestic policy guidance, a wave of scientist-led startups has emerged. Innovative projects featuring original technologies and substantial market potential are more likely to stand out in the early-stage market.

The sluggish performance in China during the second half of the year was significantly impacted by pandemic control measures and the initial wave of SARS-CoV-2 variants, which forced a slowdown in economic activities. As economic activities recover, China’s healthcare industry is poised to embrace new opportunities in 2023.

II. Hot Sectors in Global Healthcare Investment and Financing in 2022

2.1 Global Distribution of Financing by Sector: Biopharmaceuticals Reclaims Top Spot, While Funding Interest in Digital Health Declines Sharply

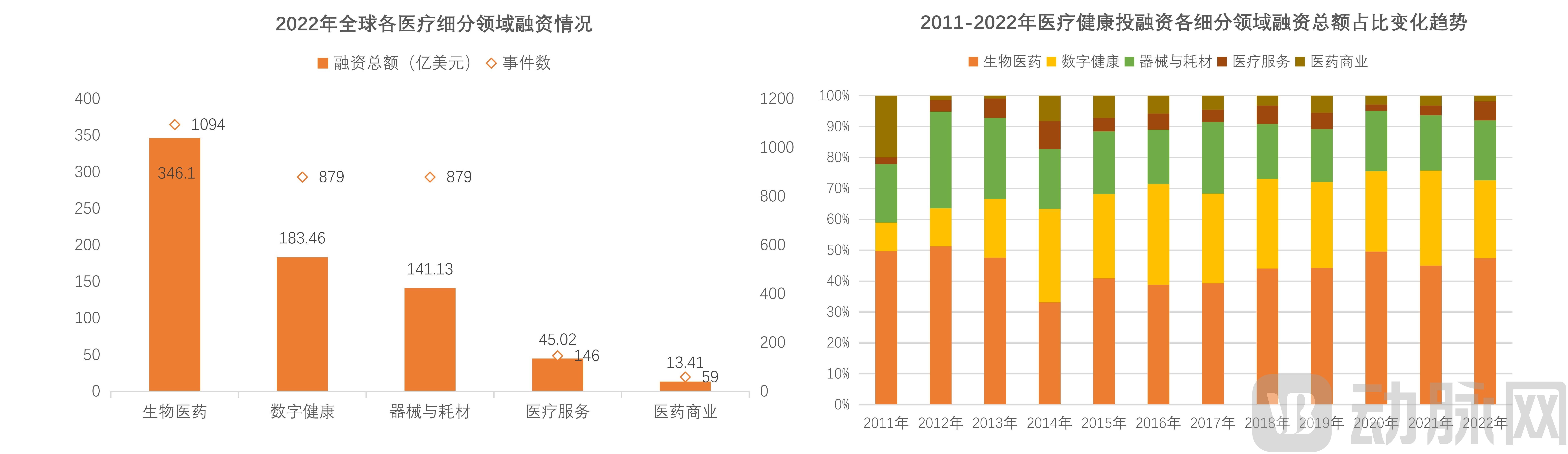

In 2022, the global biopharmaceutical sector maintained a strong lead over other sub-sectors with 1,094 financing deals and a total funding amount of approximately $34.61 billion, once again topping the financing rankings. The digital health sector followed closely with $18.346 billion, while medical devices and consumables ranked third.

In terms of the proportion of financing amounts across five major sub-sectors, the share of total financing in digital health declined significantly in 2022, while the shares for biopharmaceuticals and medical devices saw slight increases. In absolute terms, the digital health sector recorded 879 financing deals in 2022, with a total amount of approximately $18.346 billion. Financing was primarily concentrated at the tens-of-millions and millions of U.S. dollars levels. Compared to the previous year, the number of deals decreased by 165, the total financing amount dropped by 53% year-over-year, and the average deal size fell by more than $15 million. This challenging financing environment for digital health companies in 2022, characterized by an overall slowdown in capital flow, may be attributed to overheated financing activity and inflated valuations in 2021.

2.2 Outstanding Performance in Innovative Fields Such as Cell Therapy and Therapeutic Devices; Domestic Industrial Transformation Is Expected to Drive New Growth Points

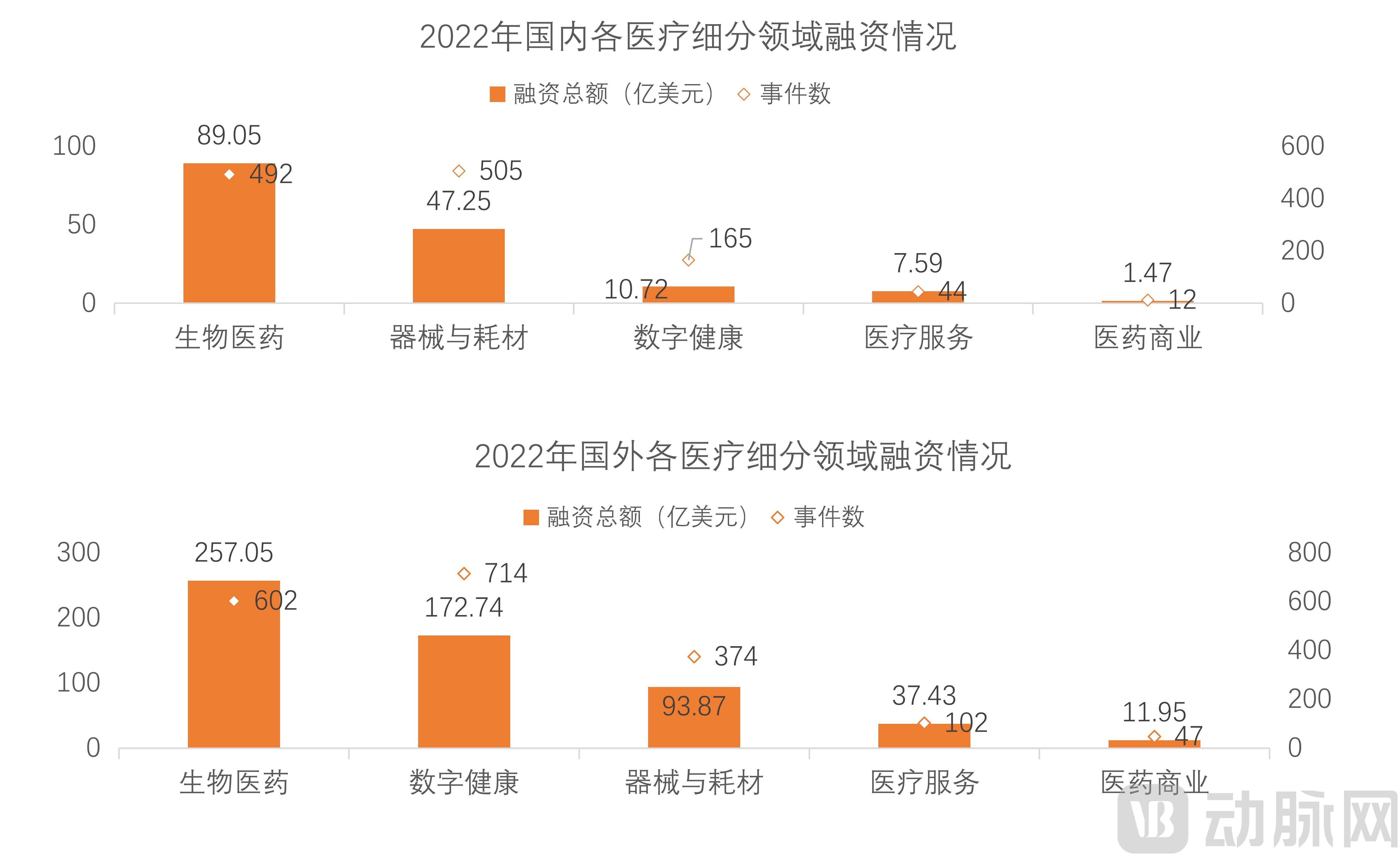

In 2022, the biopharmaceutical sector achieved notable financing results in both domestic and international primary markets.

In China, the biopharmaceutical sector remains firmly in first place, followed closely by the medical device sector. Notably, due to a higher number of financing deals involving startups, the medical device sector has rarely surpassed the biopharmaceutical sector in terms of deal count. Financing activity in the digital health sector has declined significantly, nearly leveling with that of the healthcare services sector.

Furthermore, since 2022, there has been a significant number of cross-border mergers and acquisitions in the healthcare industry, with assets in cell therapy and innovative therapeutic devices being particularly favored. Meanwhile, China’s pharmaceutical industry is undergoing structural transformation, which is expected to drive new growth points and sustain the active performance of certain innovative enterprises.

2.3 Nearly 50% of Financing Rounds Are in Early Stages, as High-Potential Startup Biopharmaceutical Companies Secure Significant Capital Infusions

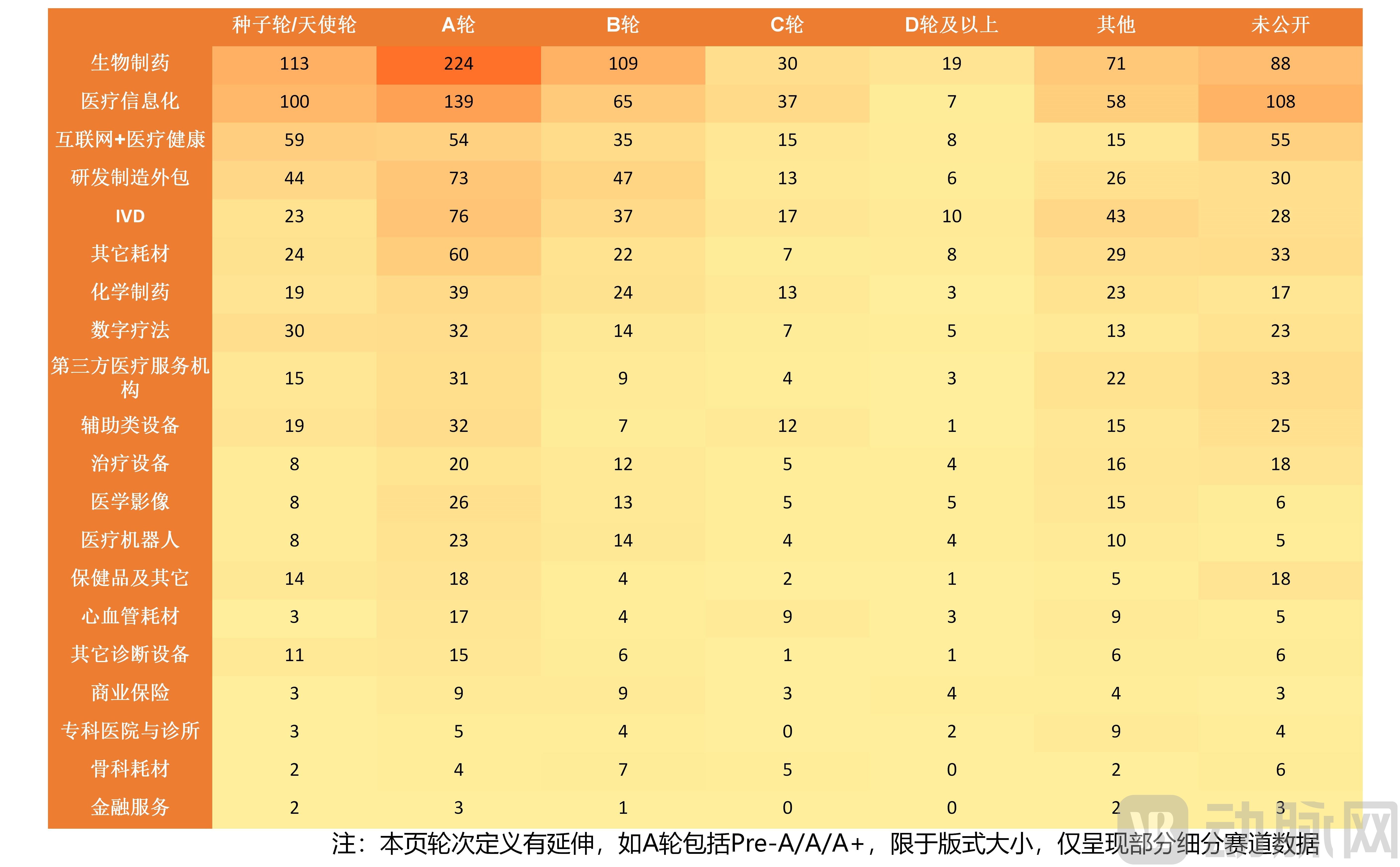

In 2022, the sectors of biopharmaceuticals, healthcare IT, “Internet + Healthcare,” and R&D and manufacturing outsourcing witnessed high levels of market interest.

From the perspective of funding round distribution, capital is heavily concentrated on early-stage projects, with early-round financing events accounting for 46% of the total number of events.

Series A financing rounds were the most frequent in 2022, with a total of 904 deals concentrated in the biopharmaceutical sector. Meanwhile, 13 biopharmaceutical companies secured mega-rounds exceeding $100 million, indicating that capital continued to focus on early-stage startups with high growth potential in 2022, with investors willing to provide substantial funding to accelerate the development of these early-stage projects.

III. Highlights of Global Healthcare Investment and Financing Tracks in 2022

3.1 The AI-Driven Drug Discovery Sector Heats Up, with Technology Fueling Sustained Growth

In 2022, a total of 76 financing deals occurred globally in the AI-driven drug discovery sector, with cumulative funding amounting to approximately USD 3.392 billion (around RMB 23.7 billion). Specifically, China’s AI-driven drug discovery sector saw 32 financing deals, totaling approximately USD 589 million; overseas, the immune cell therapy sector completed 44 deals, raising nearly USD 2.803 billion.

With the rapid advancement of technologies such as machine learning, deep learning, and natural language processing, AI is being widely applied in various stages of drug R&D, including target discovery, molecular generation, activity prediction, compound screening, and crystal form prediction, with its advantages becoming increasingly prominent. Today, AI technology is gradually integrating into every aspect of drug development, as both academia and industry explore the use of AI to assist in drug R&D, seeking new impetus for the discovery and development of novel drugs.

AI-driven drug discovery has arguably been one of the most high-profile sectors in recent years. Since the establishment of China’s first batch of AI-powered pharmaceutical companies, including Yudo Bio, Insilico Medicine, and XtalPi, the sector has pursued an aggressive growth strategy. In terms of financing rounds, global funding in the AI-driven drug discovery field remains dominated by early-stage investments, with Series A rounds being the most numerous, totaling 24 deals.

3.2 Domestic Biopharmaceutical Sub-sectors: Frontier Biotechnology Remains Active, and the CDMO Sector’s High Prosperity Is Expected to Continue

In addition to the increasingly popular AI-driven drug discovery sector in the past two years, frontier biotechnology sectors such as immune cell therapy and gene therapy have remained active, becoming the primary drivers of steady growth in domestic biomedical financing in 2022. Among these, immune cell therapy products for solid tumors have garnered greater attention.

Meanwhile, the fervor surrounding CROs has cooled somewhat this year. However, driven by supportive policies, the engineer dividend, and the rise of the emerging CGT CDMO sector, the development of the CDMO industry has been further accelerated. Following the new round of drug review and approval reforms, China’s investment in biopharmaceutical innovation has increased year by year. The full implementation of the Marketing Authorization Holder (MAH) system has brought new development opportunities to the CXO industry, holding significant importance for promoting innovative reforms within the ecosystem of China’s pharmaceutical industry.

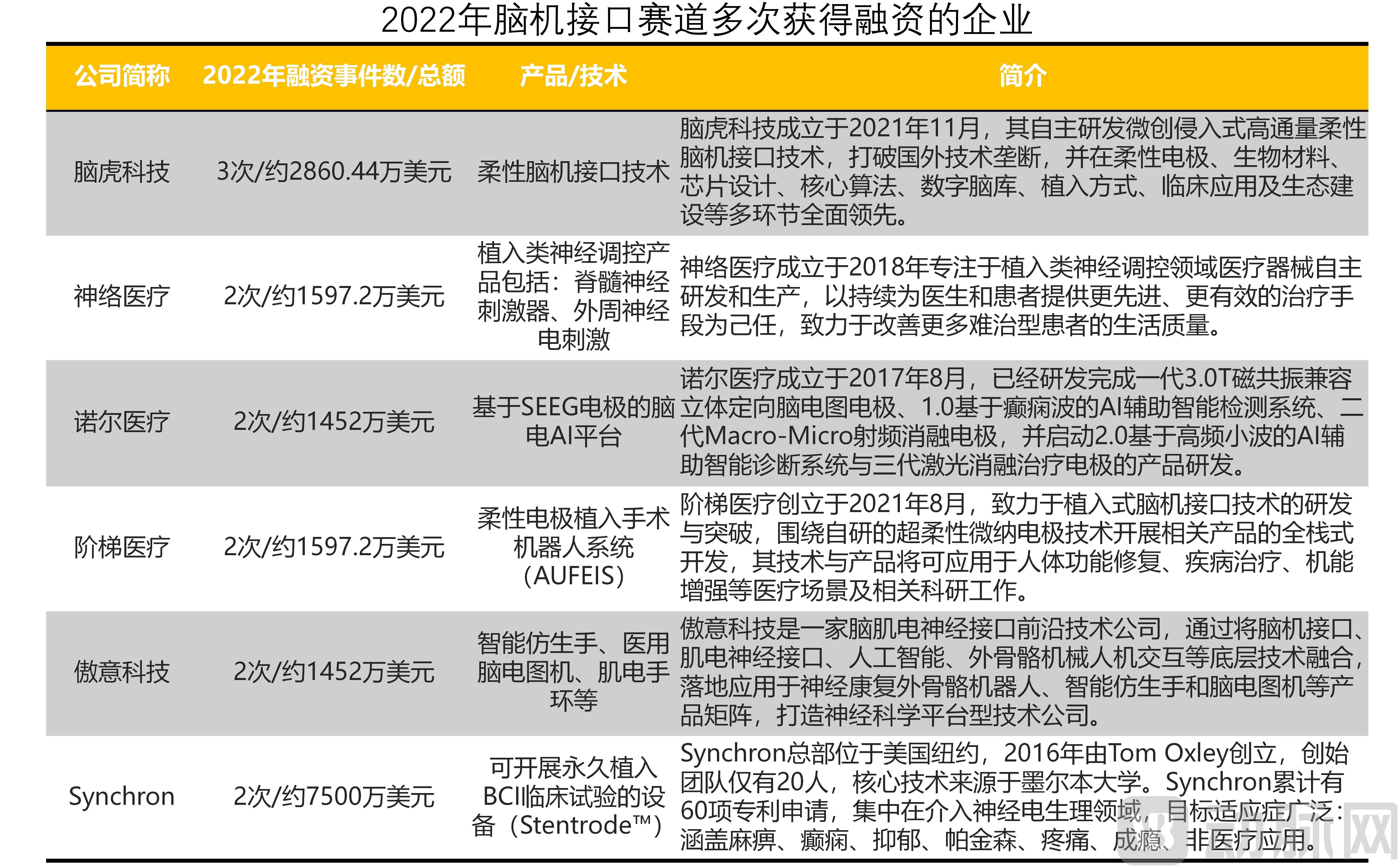

3.3 Six BCI Companies Secure Multiple Rounds of Funding, with Flexible Electrode Implantation Technology Garnering Strong Investor Interest

In 2022, the global brain-computer interface (BCI) sector saw a total of 39 financing rounds, with the total funding amount reaching approximately $650 million. The financing activities were mainly concentrated in Series A rounds, accounting for 8 rounds; the majority of the funding amounts were at the tens of millions of dollars level, with 21 rounds falling into this category.

Globally, six companies have attracted significant investor attention and received multiple rounds of funding. Notably, NeuroXess, a developer of flexible brain-computer interface technology, secured financing three times in 2022, with each round seeing additional investments from Sequoia Capital China, Lianxin Capital, and Shanda Capital.

NeuroXess is dedicated to minimally invasive, high-throughput, flexible brain-computer interface (BCI) technology. Also focusing on flexible electrode implantation technology is Jieti Medical, which secured two rounds of financing in 2022. The funding round in late December 2022 was jointly led by two prominent investors, OrbiMed and Yuanhe Yuandian. Unlike NeuroXess, Jieti Medical employs ultra-flexible micro-nano electrodes. Another company developing ultra-flexible micro-nano electrodes abroad is Axoft, which also received additional capital injection in August 2022.

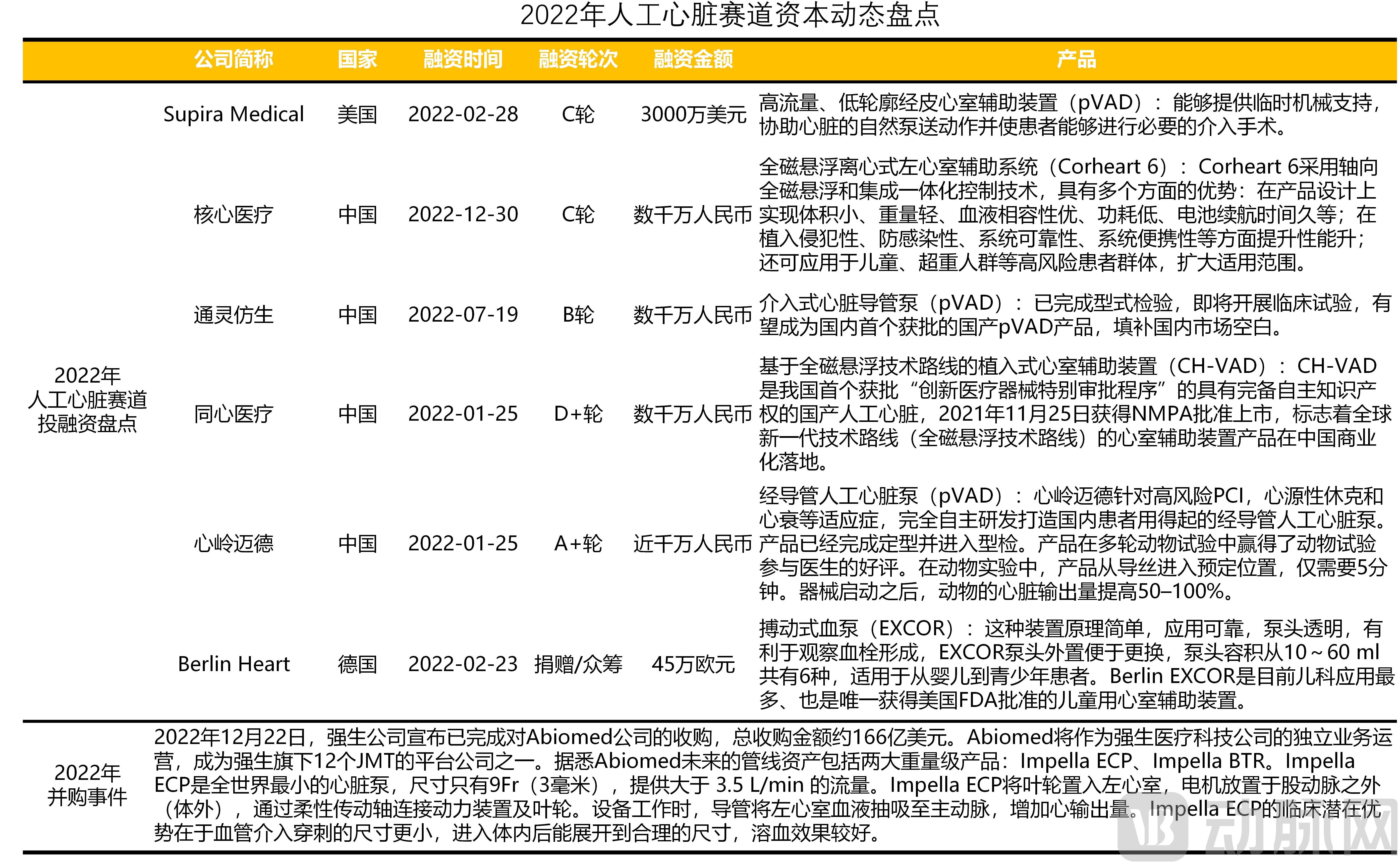

3.4 First Domestically Produced Artificial Heart with Complete Independent Intellectual Property Rights Approved, Making Artificial Hearts a Hot Sector with Long-Term Growth Potential

In 2022, the global artificial heart sector saw a total of six financing rounds, with the total amount raised reaching approximately $88.56 million.

According to the "Report on Cardiovascular Health and Diseases in China 2020," there are approximately 330 million people with cardiovascular diseases in China, including about 8.9 million patients with heart failure. Heart transplantation is an effective treatment for heart failure, but the shortage of donor hearts has shifted attention toward artificial hearts. As the most complex and precise medical device, requiring the highest manufacturing standards and imposing significant demands on medical staff, artificial heart technology had long been monopolized by developed countries. This landscape changed with the emergence of domestic products such as "Yongrenxin," "China Heart," and "CH-VAD," which attracted substantial capital interest to this sector. In November 2021, China’s first domestically produced artificial heart with complete independent intellectual property rights (Tongxin Medical’s CH-VAD) received approval from the National Medical Products Administration (NMPA), ushering in a new era for heart failure treatment in China and making domestic artificial hearts a hot investment track.

3.5 Overseas Clinical Optimization and Premium Home Care Work in Tandem to Alleviate Strain on Medical Resources

Taking the United States as an example, a wave of respiratory illnesses—including respiratory syncytial virus (RSV), COVID-19, and influenza—is sweeping across various regions. This situation has further exacerbated the already challenging circumstances faced by hospitals, which are grappling with resource shortages and nursing home closures. Data from the U.S. Department of Labor shows that in September 2022, more than 500,000 workers resigned from the U.S. healthcare and social assistance sector. Furthermore, a report released by the American Medical Association in early 2022 indicated that one in five physicians planned to leave the medical field within two years.

The contradiction between ever-increasing healthcare demand and a shortage of professional medical personnel has shifted market attention toward intelligent solutions: capital is flowing predominantly to the hospital sector, particularly into digital services that can effectively enhance clinical efficiency. Furthermore, significant financing rounds are frequently seen in areas such as premium home-based care, and the prevention and rehabilitation of specialized conditions among the elderly and children, aiming to achieve at-home health management while alleviating pressure on hospitals.

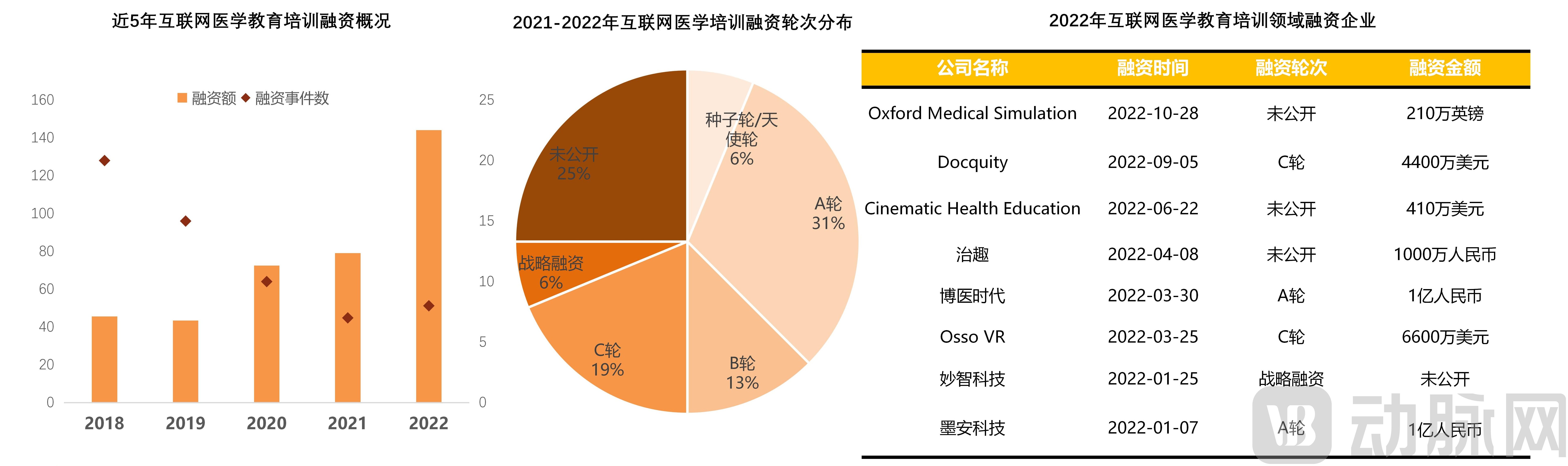

3.6 Internet-based medical education and training are becoming increasingly profitable, with the head effect growing more pronounced

Unlike the broader digital health sector, where financing activity failed to match the capital surge seen in 2021, global funding for online medical education and training reached a five-year peak in 2022. However, compared with startups, investors have focused more on growth-stage companies that are gradually refining their business models.

In addition to the shortage of healthcare professionals in recent years caused by pandemic-related pressures, the widespread adoption of online learning tools has itself driven the expansion of the internet-based medical education and training market. Furthermore, factors such as the growing elderly population, increased health awareness and spending power among residents, the urgent need for primary care physicians to reduce misdiagnosis rates, and the academic, employment, and research demands of medical students have all contributed to incremental growth in this market. In China, the introduction of policies such as the “Healthy China 2030” Planning Outline, along with the maturation of mobile internet technologies like big data and cloud computing, has diversified models of medical communication. Notably, health and medical topics accounted for 63.16% of search volume among the eight major science popularization categories, ranking first. These multifaceted drivers have increasingly underscored the necessity of accessing specialized medical content online.

IV. Analysis of Active Investment Institutions in Healthcare in 2022

4.1 Domestic Investment Institutions’ Activity Surpasses Overseas Counterparts Again; Sequoia China Increases Bets on Innovative Drugs Sector

In 2022, Sequoia Capital China was the most active investor in the global healthcare sector, making a total of 49 investments throughout the year and leading 22 financing rounds. The majority of its investments were in early-stage projects, including 21 Series A financings and 11 seed/angel rounds. Its investment portfolio primarily focused on biopharmaceutical companies, with particular emphasis on China’s innovative drug sector. Notable examples include Fangtuo Bio, a developer of innovative gene therapy drugs; Pufang Bio, a developer of macromolecular targeted therapies; Shize Bio, a researcher and developer of novel stem cell therapies; and Huiliao Bio, a developer and manufacturer of nucleic acid-based drugs.

RA Capital is the most active institution in overseas investments in the healthcare sector. Its investment portfolio focuses primarily on drug development, while also covering medical devices, diagnostics, services, and medical research. In 2022, its IPO exits included HilleVax, a novel vaccine developer; PepGen, a developer of therapeutics for neuromuscular diseases; and Third Harmonic Bio, a developer of oral KIT inhibitors.

4.2 Chinese investment institutions have repeatedly increased their investments in early-stage startups in the biopharmaceutical sector

In 2022, the most active domestic institutions investing in global healthcare were Sequoia Capital China, Qiming Venture Partners, and Yisheng Capital.

Specifically, the top 10 most active investment firms in China are particularly focused on early-stage projects in the biopharmaceutical sector.

Gebio Therapeutics is dedicated to the research and development of innovative small-molecule protein degraders, focusing on previously “undruggable” pathogenic protein targets by developing next-generation molecular glues and PROTAC drugs for targeted protein degradation. The company completed three rounds of early-stage financing in 2022, with Hillhouse Investment Capital and Qiming Venture Partners leading successive rounds, while Cathay Capital, Lilly Asia Ventures, and Qiming Venture Partners participated in two follow-on investments.

Shize Bio, a company dedicated to the research and development and industrialization of iPSC-derived cell therapies, completed two rounds of financing in 2022, each time securing investment from Qiming Venture Partners, Lilly Asia Ventures, and Sequoia Capital China.

V. Review of Healthcare IPOs Listed in 2022

5.1 Difficult Exit Environment Leads More Overseas Companies to Delay IPOs

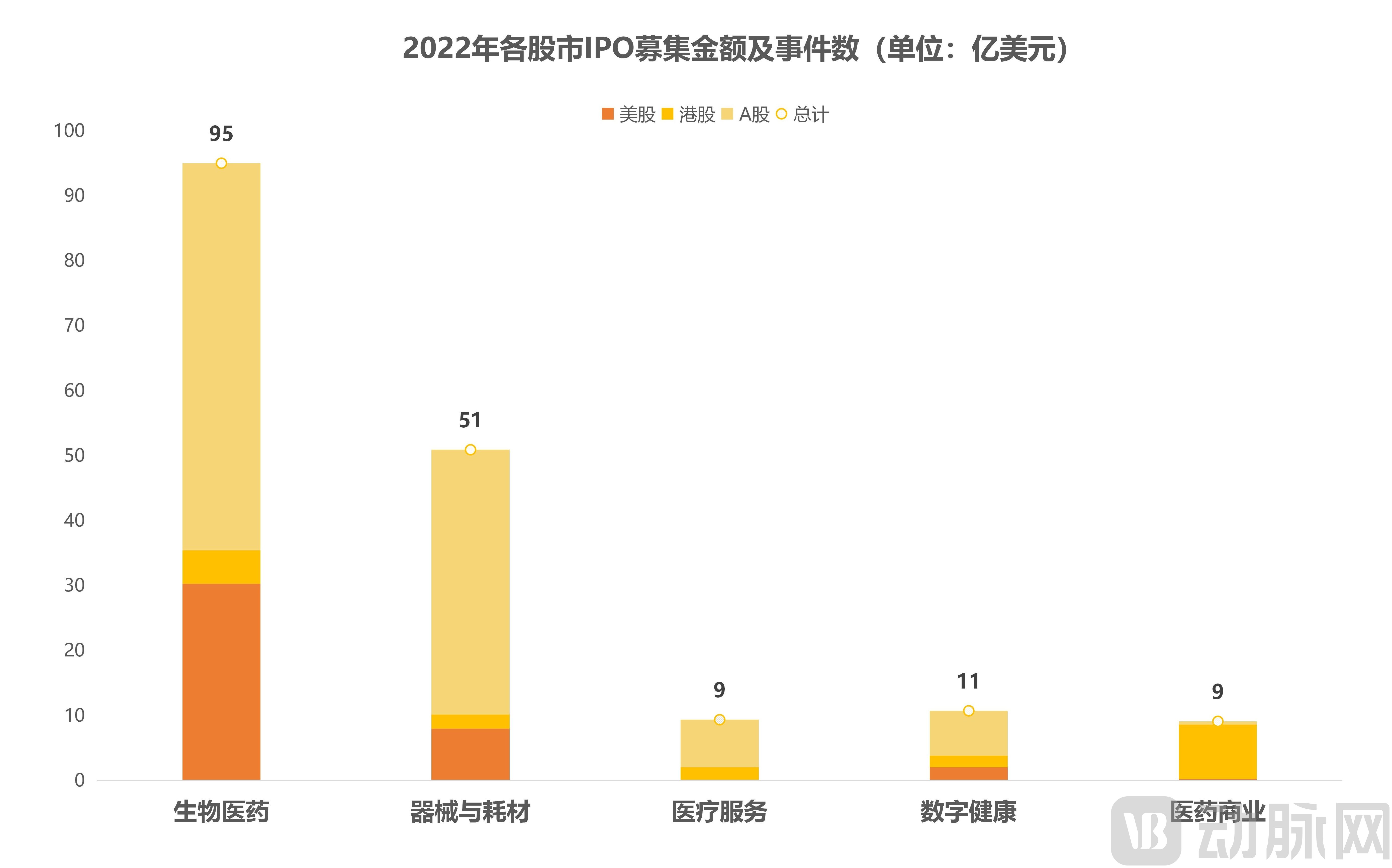

According to VBInsight, a total of 178 companies listed on the A-share, U.S., and Hong Kong stock markets raised over $17.9 billion in 2022, approximately one-third of the amount raised in 2021.

More than 50% of the companies, totaling 93, are listed in the United States, raising over $17.9 billion, a year-on-year decrease of approximately 44%, yet still exceeding the combined total of the other two stock exchanges.

In 2022, a total of 93 companies in the biopharmaceutical sector went public, a figure significantly lower than that of 2021 and representing a decrease of 30 compared to 2020. This trend is also attributable to the challenging exit environment overseas in 2022; rather than pursuing IPOs, more companies prioritized securing additional financing.

5.2 Secondary Market Rebounds in H2, Number of Medical Device IPOs Catches Up with Pharmaceutical Sector

In 2022, the number of Chinese companies going public on the three major stock exchanges declined, a trend that differed from overseas markets. On one hand, regulatory and policy changes slowed the pace of Chinese concept stocks listing in the U.S. starting in the second half of 2021. On the other hand, pandemic control measures led to operational suspensions for some healthcare companies in Beijing and Shanghai, resulting in setbacks for both financing and IPOs in China during the first half of 2022.

In the second half of 2022, China welcomed 54 new listed companies, approaching the historical high of 63 recorded in the second half of 2021, with pharmaceutical and medical device companies performing on par. In fact, the IPO processes of healthcare companies collectively accelerated toward the end of the first half of 2022, with a record-breaking 126 new applications accepted by the STAR Market and the ChiNext Board.

As more companies pivot to Hong Kong and A-share listings following setbacks in their U.S. IPO bids, and given that secondary market conditions often influence primary market dynamics, the healthcare sector’s secondary market is poised for a new landscape at the start of 2023.

VI. Regional Distribution of Global Healthcare Investment and Financing Hotspots in 2022

6.1 Global: The United States Leads the World, with Booming Development in Digital Healthcare Infrastructure

In 2022, the five countries with the highest number of global healthcare financing events were the United States, China, the United Kingdom, Israel, and India.

In 2022, the United States led the world with 1,257 financing deals and $4.403 billion (approximately RMB 30.8 billion) in funding, followed closely by China. Together, the U.S. and China accounted for 75% of the total global financing amount and 81% of all financing deals.

Moreover, the rise of medical innovation forces in Asia is notable. In particular, Israel and India have seen a significant surge in healthcare financing, ranking among the top five hotspots. Similar to India, digitalization has also been a crucial factor supporting Israel’s healthcare sector; among its subfields, health information technology has experienced the fastest growth.

From the perspective of investment hotspots, biopharmaceuticals and digital health are the areas of global focus this year.

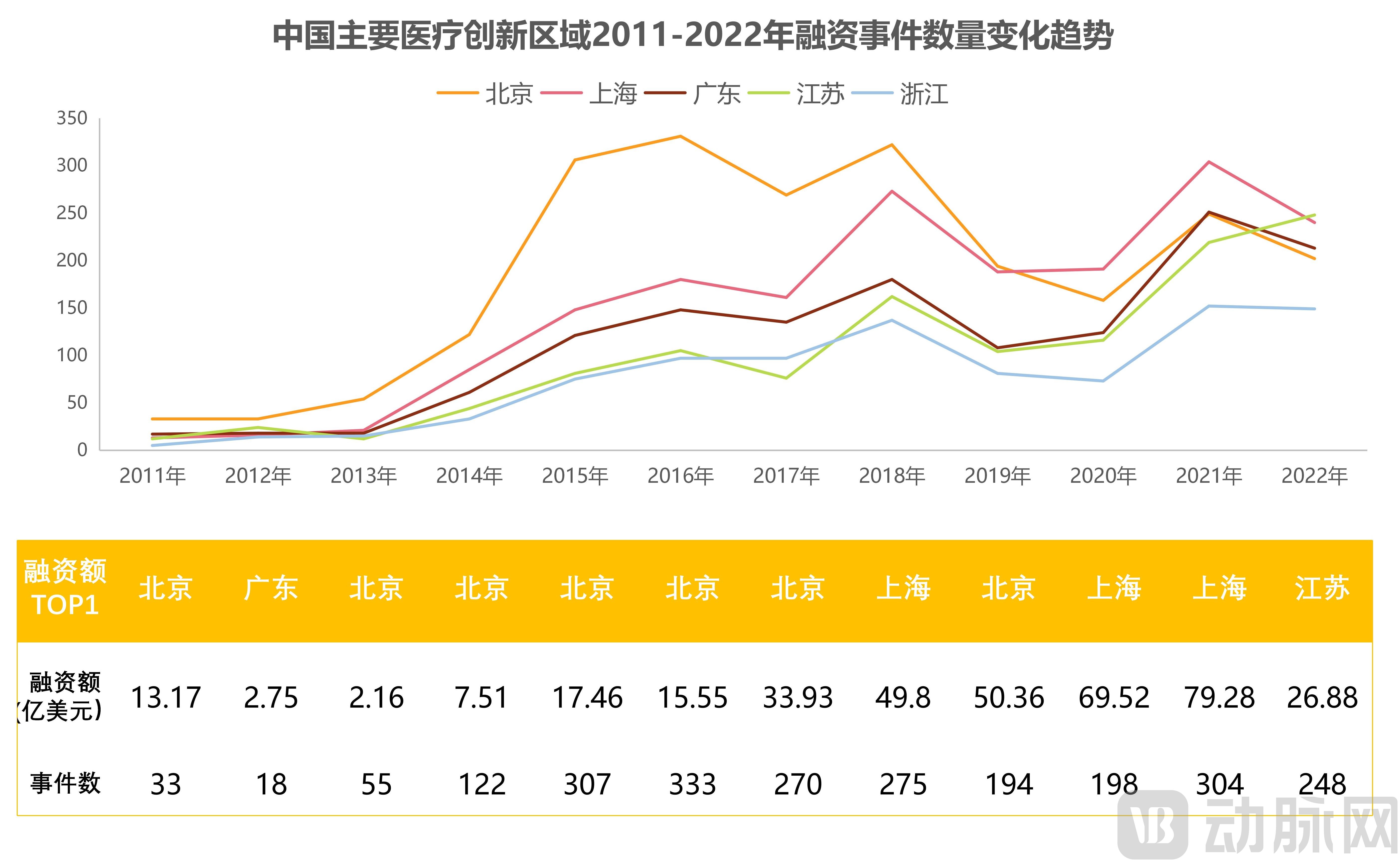

6.2 China: Jiangsu Tops the List, Demonstrating Spillover Effects as a Biopharmaceutical Industry Hub

In 2022, the five regions in China with the highest concentration of healthcare investment and financing activities were Jiangsu, Shanghai, Guangdong, Beijing, and Zhejiang, in that order.

Jiangsu’s biomedical industry, characterized by high-quality clustered development, has demonstrated significant spillover effects, emerging as the primary investment hotspot in the healthcare sector this year. With 248 financing deals, Jiangsu has once again surpassed Shanghai to become the most active region for primary market investments in healthcare, outpacing Shanghai, which ranks second with a cumulative total of 240 financing deals.

Overall, in 2022, healthcare financing remained concentrated in Beijing, Shanghai, and Guangzhou, regions characterized by a solidified foundation for the healthcare industry and a convergence of innovative resources. These areas accounted for 53% of all financing deals across China.

6.3 China: Jiangsu Overtakes Shanghai as the Hottest Region for Financing Projects

An Overview of the Geographic Distribution Trends in Healthcare Industry Investment and Financing Over the Past Decade: Beijing Has Long Maintained Its Dominant Position as China’s Primary Hub for Medical and Health Innovation.

Prior to 2020, Beijing had been the region with the highest number of healthcare and medical financing deals in China for consecutive years. In 2018, Shanghai surpassed Beijing for the first time to become the most active region in terms of financing deals.

In 2022, Jiangsu Province made its debut on the ranking with 248 financing deals, becoming the hottest region for healthcare and medical financing transactions in China.

VII. Top Financing Records of Healthcare Companies in 2022

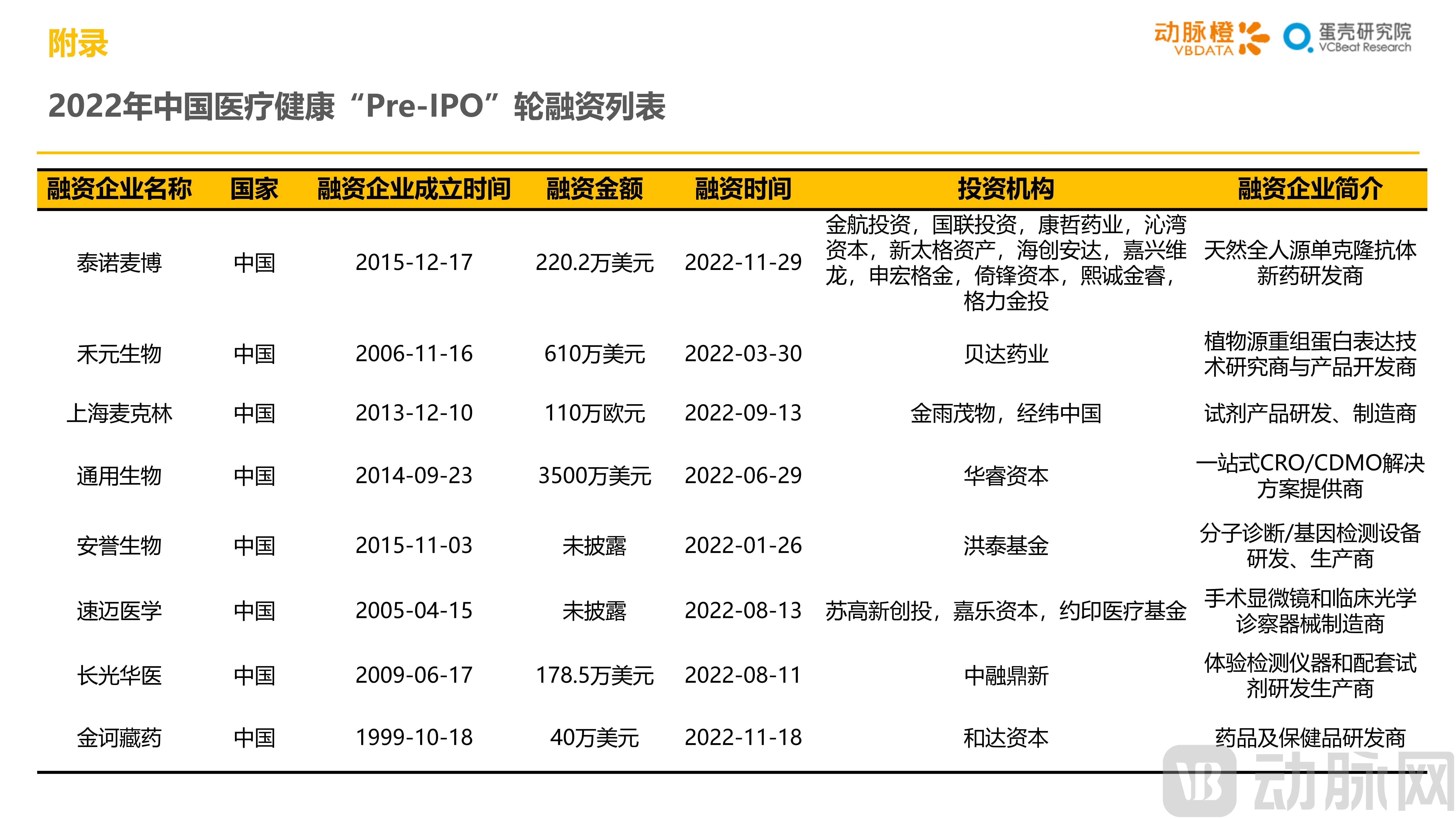

VIII. Appendix