SD Biosensor Aims for Global Top Three IVD Position Through $1.53 Billion Meridian Bioscience Acquisition

SD Biosensor

Biological Diagnostic Technology R&D and Product Manufacturer

Meridian Bioscience

Developer, Producer, and Distributor of Clinical Diagnostic Kits for Infectious Diseases

SJL Partners

Equity Investment Firms

$1.53 Billion: Another Major M&A Deal Emerges in the IVD Raw Materials Industry

In July 2022, South Korean diagnostics company SD Biosensor and South Korean private equity firm SJL Partners acquired U.S. diagnostic test kit developer Meridian Bioscience in an all-cash transaction valued at approximately $1.53 billion. SD Biosensor stated that,This transaction is the largest merger and acquisition deal for a South Korean diagnostics company.

The merger will be executed through a reverse triangular merger. SD Biosensor and SJL Partners will jointly invest in Columbus Holding Company, after which Meridian will merge with Madeira Acquisition, a wholly-owned subsidiary of Columbus Holding, and all existing shares held by Columbus will be converted into Meridian shares.

SD Biosensor currently has a market capitalization of approximately KRW 3.2 trillion (about RMB 17.3 billion). Since its listing in 2018, the company’s revenue has grown continuously, achieving a growth rate of 2,211.01% in 2020. Its full-year revenue in 2021 reached KRW 2.93 trillion (about RMB 15.9 billion), accounting for approximately 2.3% of global IVD sales.

Meridian is a leading player in the upstream raw materials market for IVD in the United States, developing and manufacturing diagnostic test kits, rare reagents, specialty biological products, and components, with a current market capitalization of $1.456 billion.

SJL focuses on cross-border opportunities outside of South Korea and the Asia-Pacific region, with most of its members hailing from globally renowned investment banks, including JPMorgan Chase.

The acquisition is scheduled to close on January 31, 2023. Upon completion, SD Biosensor will hold approximately 60% of Meridian’s equity, while SJL will retain approximately 40% and provide operational support.

What synergies will SD achieve through this acquisition? What implications does this have for China’s IVD raw material market? VCBeat will analyze these two key questions in detail.

According to Arizton, the global IVD raw materials market is projected to achieve an incremental growth of $9.91 billion and an absolute growth of 40.73% by 2027. This growth is driven by increasing awareness of early diagnosis and disease prevention, as well as a surge in demand for IVD tests and equipment from hospitals.

Currently, due to the involvement of numerous technologies and processes, the global IVD raw materials market is characterized by a large number of participants with uneven individual scales. Consequently, many relevant companies worldwide have grown into industry leaders through activities such as product development, integration, mergers and acquisitions, and sales channel expansion.

Meridian Bioscience underwent a forty-year journey before addressing its product shortcomings and emerging as a leading industry giant. Back in the 1970s, Meridian, still in its nascent stage, was not even an IVD raw material supplier.

Founder William J. Motto initially worked as a salesman in the trucking industry. In 1966, a chance opportunity led him to join a company that sold products such as early pregnancy tests. Ten years later, Motto leveraged the network he had built over the decade with hospitals and research institutions to launch his own distribution business, becoming a distributor for the University of Kentucky’s rapid fungal tests.

To transport specimen samples to testing laboratories more efficiently,Motto conceived a plastic container for transporting patient samples. With this idea, he secured investment, used the funds to establish a company from his home, and completed development and testing in-house. This was the initial form of Meridian.

William J. Motto Image source: cincinnati.com

Over the subsequent forty-plus years of development, Meridian has continuously expanded and optimized its IVD raw material product portfolio through sustained R&D and M&A activities.

Meridian’s R&D expenses in 2022 amounted to approximately $24 million, accounting for 18% of its total annual operating expenses. During this period, the Diagnostics division launched two new products, while the Life Sciences division introduced 17 molecular products and established a new recombinant protein R&D facility in New Jersey. To further enhance its immunology R&D capabilities, Meridian also acquired selected assets from Estel Biosciences in October.

In 2010, Meridian completed the acquisition of the Bioline Group. Bioline is a manufacturer in the field of molecular biology, with its SensiFAST One‑The Step Kit is compatible with all real-time instruments and meets the demand for higher throughput and faster detection in qPCR technology.

Subsequently, Meridian completed the acquisitions of Magellan Diagnostics, GnePOC, Exalenz Bioscience, and BreathTek. Through these acquisitions, Meridian achieved comprehensive product portfolio coverage in point-of-care analyzers, molecular diagnostics, digestive and liver disease testing, and Helicobacter pylori testing, leading to a sustained increase in net revenue. For instance, the BreathTek product line contributed to a 27% growth in net revenue for Meridian’s non-molecular diagnostic products in 2022.

As a key participant in the IVD raw material supply chain, Meridian has a distribution network spanning more than 70 countries and regions worldwide. In 2017, Meridian established a wholly-owned subsidiary in China (Beijing Meridian Bioscience Technology Co., Ltd.), primarily focusing on products within its Life Sciences segment.

Meridian’s robust technical capabilities and comprehensive business layout enable it to seize opportunities amidst the tides of change.

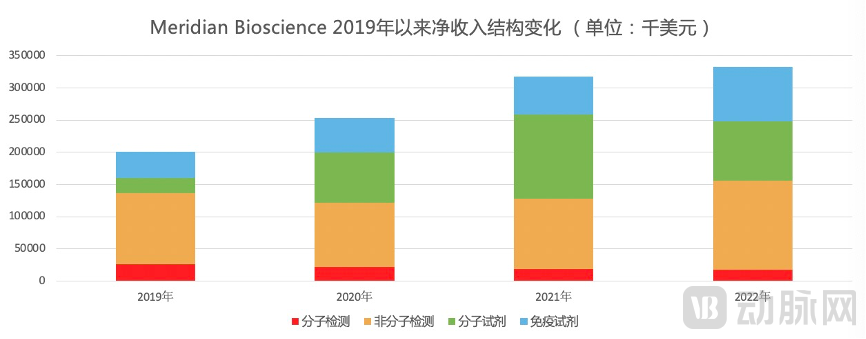

In 2020, the Life Science segment of Meridian Bioscience reported a 106% year-over-year increase in revenue, with molecular reagents growing by 237% and immunoassay reagents increasing by 32%. The primary growth drivers were heightened market demand for molecular components, such as RNA master mixes and dNTPs used in SARS-CoV-2 PCR testing, as well as recombinant antigens utilized in antibody tests and monoclonal antibodies employed in antigen tests.

Changes in Meridian’s Net Income Structure Since 2019 | Chart by VCBeat

In 2022, driven by declining market demand for COVID-19 testing, net revenue in Meridian’s Life Science segment decreased by 7% year over year. Specifically, sales of molecular reagents dropped by 30%, while immunoassay reagents grew by 43%, primarily because rapid antigen tests had replaced molecular assays as the predominant method for COVID-19 detection.

Supplemented by substantial revenue from non-molecular testing products, Meridian maintained strong financial performance despite significant shifts in market demand, achieving a full-year net revenue of $333 million in 2022, a 5% year-over-year increase.

SD Biosensor, founded in 1999, has developed and manufactured multiple world-first kit products (Malaria Ag ELISA kit, SARS diagnosis kit, Dengue Duo, H1N1 pandemic diagnosis kit, etc.), and established South Korea’s second-largest factory in 2013.

At the onset of the COVID-19 pandemic, SD Biosensor, as one of the first companies globally to promote COVID-19 antigen testing, saw its profit margin surge from 4.32% in 2019 to 36.34% in 2021, achieving remarkable worldwide success through its partnership with Roche.

Roche Diagnostics’ reagent sales increased by 29% year-on-year in 2021, primarily driven by its COVID-19 testing portfolio, with all rapid diagnostic products supplied by SD Biosensor. This arrangement allowed Roche to avoid building its own rapid diagnostic line from scratch, thereby saving significant labor and material costs, while also directly addressing the question of the future direction of this business line in the post-pandemic era. Based on this collaboration model at the time, SD Biosensor’s role resembled that of a contract manufacturer for large multinational pharmaceutical companies.

But today, Cho Young-sik, Chairman of SD Biosensor, stated that,The company aims to achieve multiple synergies through the acquisition of Meridian, positioning itself as one of the world’s “Big Three” IVD companies.

As a leading in vitro diagnostics (IVD) company in South Korea, SD Biosensor will significantly accelerate its entry into the U.S. IVD market through this acquisition.

Excluding sales in the United States, SD Biosensor is the fifth-largest IVD company globally. However, an executive at SD noted that the U.S. is the world’s largest market, accounting for approximately 40% of the global IVD market, and a significant portion of the revenue for the current top ten IVD companies worldwide also comes from the U.S. Therefore, successfully entering the U.S. market will bring SD Biosensor closer to its goal of becoming one of the top three IVD companies globally.

However, the barriers to entering the U.S. IVD market are high.

Even U.S.-based companies face challenges in obtaining FDA approval. Even with FDA clearance, establishing a sales network to distribute diagnostic products remains a significant challenge.

In January 2022, SD Biosensor voluntarily recalled its STANDARD Q COVID-19 Ag Home Test in the United States because the test kit had not been approved by the FDA for distribution or use in the U.S. Subsequently, SD Biosensor conducted an investigation to determine how the product had been illegally imported into the United States and planned to strengthen contractual terms with distributors and enhance enforcement to prevent such incidents from recurring.

Meridian BioscienceHaving operated in the United States for over four decades, the company has accumulated substantial experience in securing IVD approvals and boasts a team of numerous FDA and regulatory affairs experts. Meanwhile, SD Biosensor will directly address its U.S. distribution network challenges through the acquisition of Meridian.

A company executive stated that this merger and acquisition deal will enable SD Biosensor’s distribution network to reach nearly all countries worldwide, including those in the Middle East and Africa.

SD Biosensor began trading on the Korea Composite Stock Price Index (KOSPI) in July 2021. According to Nikkei News, the company’s share price closed up 7% on its debut, making it one of the largest IPOs on the KOSPI that year.

The company used the proceeds of KRW 776.4 billion (approximately USD 679 million) to expand its diagnostic product portfolio and global manufacturing footprint. To date, SD Biosensor and Meridian have had minimal overlap in their overseas facilities.Therefore, both parties will also fully leverage their respective existing bases to achieve synergies.

Furthermore, the two companies possess distinct specialized product portfolios, which will facilitate mutual complementarity between the parties.

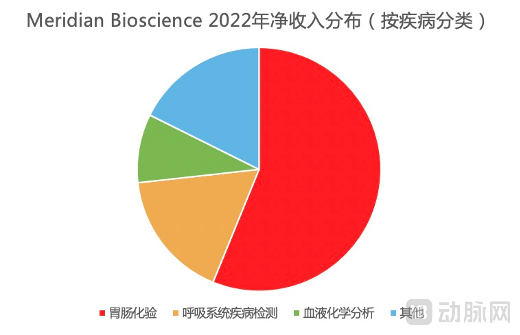

SD Biosensor holds advantages in diagnosing respiratory-related diseases, while Meridian Bioscience is competitive in diagnosing gastrointestinal disorders and possesses the only point-of-care diagnostic device for lead poisoning of the digestive system in the United States.

Meridian’s 2022 Net Revenue Distribution | Chart by VCBeat

Meridian CEO Jack Kenny stated in a press release that with declining market demand for COVID-19 testing, the company will leverage SD Biosensor’s expertise and strengths to develop new products.

Interestingly, Meridian is the third company acquired by SD Biosensor since 2021.

As previously mentioned, SD’s revenue has surged significantly since 2020, driven by a sharp increase in overseas sales. Consequently, its substantial cash reserves have enabled SD to continuously pursue mergers and acquisitions within the industry over the past two years.

In November 2021, SD Biosensor completed the acquisition of the Brazilian company ECO Diagnóstica. ECO Diagnóstica is a leading supplier of rapid IgG and IgM antibody tests for Covid-19 in Brazil.Furthermore, it provides high-quality products and technologies for human diagnostics, veterinary medicine, and the food safety market.

March 2022,SD BiosensorAcquired the German in vitro diagnostics distributor Bestbion for KRW 16.1 billion (approximately USD 13.2 million). The company offers hundreds of immunoassay products, including those for rare diseases, microbiology, infectious diseases, and molecular diagnostics, and operates a distribution network in Germany and Austria capable of delivering products within 24 hours.

An SD Biosensor executive stated that the acquisition “saved us the time required to establish a local entity, enabling us to enter the European market more efficiently.”

To further strengthen its distribution network in Europe, SD acquired the Italian medical device distributor Relab SRL one month later for approximately KRW 61.9 billion (about USD 49.9 million).

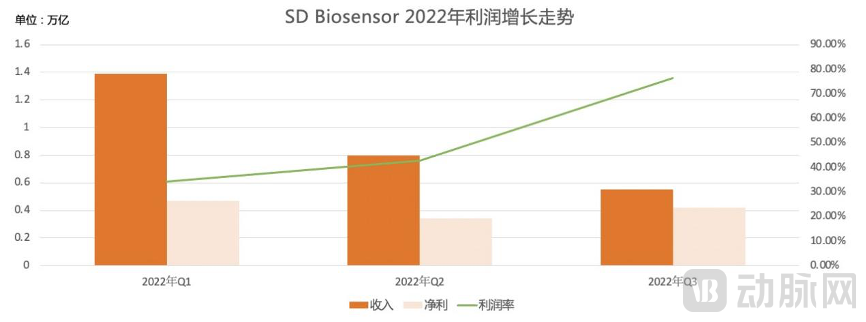

With such a global layout, SD’s profit margin maintained a relatively significant growth trend in the first three quarters of 2022.

SD’s Profit Growth Trend in 2022 | Chart by VCBeat

Strategic M&A is a fundamental strategy for participants in the IVD raw materials market to broaden their product portfolios and increase market share.

In addition to SD Biosensor’s acquisition of Meridian, Finnish IVD raw material company Medix Biochemica acquired 100% of the shares of U.S. leading IVD raw material supplier Bioresource Technology last June, to expand its base matrix capabilities and influence in the U.S. market.

From 2019 to 2022, Medix Biochemica successively acquired the U.S.-based companies Lee Biosolutions, EastCoast Bio, and Biostride, as well as the French company Diaclone and the German biotechnology firm myPOLS Biotec.

These companies are all IVD raw material suppliers, each possessing distinct R&D and manufacturing expertise, such as Lee Biosolutions’ protein purification capabilities and myPOLS Biotec’s strengths in molecular diagnostics. Consequently, this series of acquisitions will enable Medix to secure the most comprehensive portfolio of IVD raw materials and strengthen its business presence in North America and Western Europe.

SD BioscienceA series of M&A activities involving Medix Biochemica in recent years indicates that the upstream IVD market has witnessed a wave of mergers and acquisitions. A key driver behind this trend is the sustained rise in demand for diagnostic testing.

Apart from the impact of COVID-19 in recent years, population aging has consistently remained one of the primary drivers of market growth. In vitro diagnostics (IVD) can detect diseases and monitor an individual’s overall health status to facilitate disease cure, treatment, or prevention. Data from the National Health Commission in 2019 showed that over 180 million elderly people in China suffer from chronic diseases, with the prevalence of having one or more chronic conditions reaching as high as 75%. Therefore, even in the post-pandemic era, demand for testing remains widespread, and the key to strategic adjustment lies in reagents.

Thus, we can observe that numerous related startups have emerged in recent years. Meanwhile, independent laboratories have also experienced rapid development, particularly in developing countries. According to an analysis by Business Wire, pharmaceutical and biotechnology companies accounted for a dominant 62.19% share of the global IVD raw materials market in 2021, while independent laboratories are projected to achieve an absolute growth of 43.37% by 2027.

So, in a highly competitive and fragmented market, is it possible for China’s IVD raw materials industry to see the emergence of “acquisition giants” like SD Biosensor and Medix? In fact, some large domestic enterprises have already been capturing market share through frequent M&A activities.

The primary driver lies in a common characteristic of the global IVD raw materials market:SMEs often hold technical reserves for specialized projects or unique raw materials, while large enterprises possess numerous equipment patents, andPossesses robust distribution and manufacturing capabilities.Therefore, many larger companies choose to acquire other IVD raw material manufacturers to support their R&D and business networks, achieving complementary advantages.

Second, China’s IVD raw materials industry started relatively late, and there is an urgent need to enhance R&D and supply capabilities for raw materials.According to statistics from Guanyan Report Network, 88% of China’s raw material market was still dominated by imported products in 2019, and due to their extremely high gross profit margins, domestic midstream participants lacked bargaining power. Under the impact of the COVID-19 pandemic, most domestic enterprises and institutions only then began to focus on the upstream segment of the industrial chain.

For example, in recent years, some midstream IVD suppliers have chosen to extend upstream in the industrial chain through mergers and acquisitions. In May 2021, Shenzhen Mindray Bio-Medical Electronics Co., Ltd. acquired HyTest, one of the four major core raw material suppliers in the global IVD industry, for €545 million (approximately RMB 4.26 billion). According to Mindray’s financial report for that year, approximately 40% of the company’s revenue came from overseas markets, with its in vitro diagnostics business achieving an annual operating income of approximately RMB 8.4 billion, a year-on-year increase of 27.12%.

Upstream raw material manufacturers have also entered the fast lane amid this favorable trend. Hybribio’s IVD raw materials generated over RMB 900 million in revenue in the first half of 2021. In the second half of 2021, Sino Biological, ACROBiosystems, and Vazyme went public in succession.。In addition to these leading raw material manufacturers, companies such as Hanhai New Enzyme and Yinjia Biology are beginning to emerge in this field.

The Era of M&A in China’s IVD Raw Material Industry Has Begun. Although companies still have ample room for growth and the entire industry remains in a phase of market share fragmentation, certain IVD enterprises will inevitably enhance the specialization of their specialized testing portfolios by acquiring domestic and overseas raw material manufacturers. This strategy will alleviate pressures from the upstream market, secure core profit margins, and ultimately propel these companies to become IVD giants.