2022 Innovative Drug White Paper: 30 Charts Overview of Frontier Layout and Differentiated Innovation Across More Than 10 Sub-sectors

Affected by the “capital winter” that began in the second half of 2021, the entire innovative drug sector in 2022 appeared somewhat “cold” compared to the “heat” of the previous two years. However, this coolness does not signify pessimism, but rather calmness and rationality.

For investors, 2022 saw a gradual shedding of the restlessness that had taken hold over the previous two years amid broader macroeconomic pressures. They began to calmly analyze what has changed and what has remained constant in the macro environment, rationally considering what types of innovation are truly suitable for the Chinese market, and focusing on how to balance investment returns and risks in the global marketplace. For innovative pharmaceutical companies, the sudden cooling of investor enthusiasm prompted them to calmly assess the competitive landscape, thoughtfully evaluate their team’s strengths, and determine how to leverage those advantages while mitigating weaknesses to maximize team potential. With renewed focus and determination, they are well-prepared to face any challenges.

The changes in the innovative drug sector in 2022 manifested in multiple ways: policy announcements, financing and investment activities, corporate product portfolio strategies, technological achievements, and business development (BD) transactions. At their core, however, these changes reflect the mindset of innovative pharmaceutical companies and investors—their strategic adjustments in response to current conditions, their insights into future trends, and the corresponding strategic initiatives they have undertaken.

VCBeat’s Eggshell Research Institute reviewed and analyzed the key changes in the innovative drug sector in 2022 and highlighted promising therapeutic areas to watch in 2023, compiling these insights into the “2022 Annual White Paper on Innovative Drugs.” We hope the following content will provide industry professionals with further food for thought as they embark on the new year. We are confident that 2023 will see more steady and solid progress, with the sector continuing to operate at full steam.

Table of Contents for the 2022 Annual White Paper on Innovative Drugs

(To obtain the full report, please scan the QR code to add our assistant, and initiate your inquiry after adding.)

The following is a brief summary of the white paper.

Policy: Further standardize the development of the innovative drug sector and guide innovative pharmaceutical companies to pursue differentiated innovation

According to VCBeat data, as of December 20, 2022, a total of 49 policies related to biopharmaceuticals were issued. These policies primarily focused on accelerating the high-quality development of the biopharmaceutical industry and regulating its growth. Additionally, specific policy guidelines were introduced to standardize and expedite development in areas such as gene and cell therapy, antibody drugs, CXO (contract research, manufacturing, and development organizations), and radiopharmaceuticals.

![UUD3U]1}@1WB_NSZG@RX3XT.png](http://cdn.vcbeat.top/upload/image/06/01/15/09/1673762991212234.png/dmw)

Figure 1: Selected Policies in 2022 to Accelerate the Development of the Biopharmaceutical Sector

(Data source: VCBeat Orange Database)

In 2022, to scientifically plan and systematically promote the high-quality development of China’s bioeconomy, the National Development and Reform Commission issued the “14th Five-Year Plan for Bioeconomic Development,” which is alsoChina’s First Top-Level Design for the Bioeconomy SectorProvinces and cities, including Shenzhen, Yunnan, Heilongjiang, and Guangzhou, have successively released development plans related to the 14th Five-Year Plan based on their local conditions, aiming to accelerate and promote the high-quality development of the bioeconomy in their respective regions. Specific targets and plans have been proposed for building biomedical industry clusters with an output value of hundreds of billions of yuan. Furthermore, detailed implementation rules for local policies have been assigned to specific executive departments, with clear task allocations and timelines.

Regions including Chongqing, Heilongjiang, Fujian, Zhejiang, and Shenzhen have also introduced specific policy measures to support and accelerate the high-quality development of the biopharmaceutical industry, among whichMultiple provinces and cities have rolled out an even larger “policy bonus rain” to support the R&D and industrialization of innovative drugs.As mentioned in the “Several Policy Measures on Accelerating the High-Quality Development of the Biopharmaceutical and Big Health Industries” issued by the Jinan Municipal People’s Government, the subsidy for each newly approved and marketed Class 1 new drug has been increased from RMB 20 million to RMB 30 million, and the financial support for Class 1 and Class 2 new drug projects in clinical trial stages has also been substantially enhanced.

Among the policies promoting the development of the biopharmaceutical industry, another significant measure was the release of the “Implementing Regulations of the Drug Administration Law of the People’s Republic of China (Revised Draft for Comment)” by the General Office of the National Medical Products Administration in May 2022, which established robust incentive policies to support areas including rare diseases and pediatric drugs.

![UOE%[9PNSA(7$5VB94S]9KJ.png](http://cdn.vcbeat.top/upload/image/06/01/15/11/1673763102304428.png/dmw)

Figure 2 Selected Policies Regulating the Development of the Biopharmaceutical Sector in 2022

(Data source: Artery Orange Database)

To further standardize the development of the biopharmaceutical industry, multiple departments, including the General Office of the National Medical Products Administration (NMPA), the Center for Drug Evaluation (CDE) under the NMPA, and the Inspection Center of the NMPA, issued a series of policies in 2022. The “Opinions on Strengthening the Governance of Science and Technology Ethics,” issued by the General Office of the Communist Party of China Central Committee and the General Office of the State Council in March 2022, isChina's First National-Level Guiding Document on the Governance of Scientific and Technological Ethics,This is another landmark event in China’s governance of scientific and technological ethics since the establishment of the National Science and Technology Ethics Committee.

In August 2022, the Center for Drug Evaluation of the National Medical Products Administration consecutively released three draft guidelines for public comment, once againEmphasize the inclusion of best supportive care (BSC) in clinical trial design to avoid suboptimal therapy as a control.Once these draft guidelines are finalized, it will mean that for a new drug to reach the market, sponsors must prospectively assess whether their product can demonstrate superiority over the standard of care at the time of marketing application submission; if not, they must evaluate the risk of rejection.

Figure 3: Specialized Policies Issued in 2022 for Segments Including CGT, Antibody Drugs, CXO, and Radiopharmaceuticals

(Data source: VCBeat Orange Database)

In 2022, more targeted policies were introduced for various subsectors of the biopharmaceutical industry, including cell and gene therapy (CGT), antibody drugs, CXO, and radiopharmaceuticals. Notably, the CGT sector received the highest number of policy initiatives, garnering significant attention and support. Additionally, to prevent the antibody drug sector from replicating the hyper-competitive “red ocean” scenario seen with PD-1 inhibitors, multiple policies were issued to guide companies in making rational decisions on R&D project initiation. Regions such as Shanghai and Hainan placed particular emphasis on the development of the CXO sector. In the niche field of radiopharmaceuticals, clinical guidelines were released prior to non-clinical ones, sending a positive signal for industrial development.

Investment and Financing: Capital Clearly Favors Early-Stage and Small-Scale Investments, with CGT and CXO Being the Most Preferred Sectors

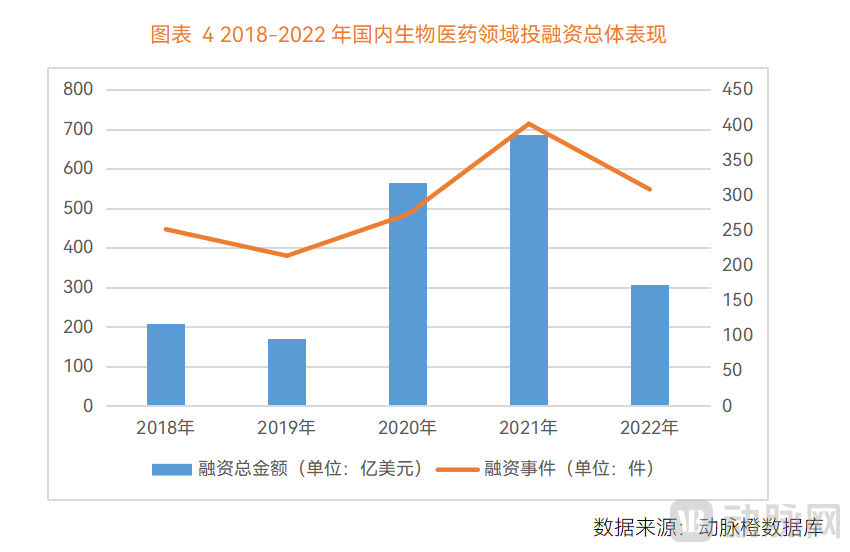

Overall financing activity has cooled, as evidenced by declines in both the total amount and the number of deals.In 2022, the biopharmaceutical sector experienced a significant decline in financing, with total funding amounting to $17.214 billion across 548 deals, compared to $38.604 billion across 714 deals in 2021, and also falling short of the 2020 figures of $31.862 billion across 485 deals.

The outbreak of COVID-19 in 2020 drew keen attention to the surging demand for growth in healthcare and biotechnology. However, by 2022, capital interest and sector enthusiasm had cooled due to weak commercial performance of innovative products, price reductions driven by medical insurance policies, and intense competition in R&D. Consequently, capital market expectations for innovative drugs declined. In the primary market, investors adopted a more cautious stance, with overall financing and investment activities falling significantly short of the previous year’s levels.

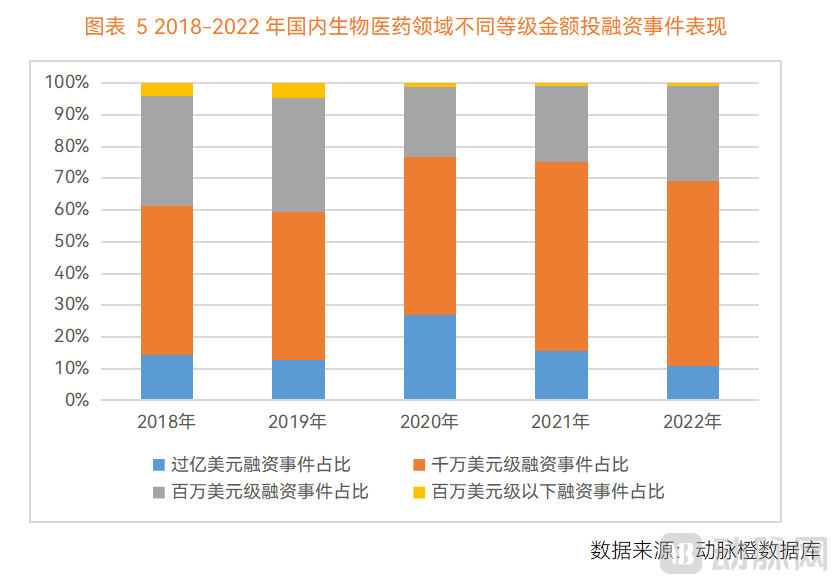

In 2022, the trend of capital investing in early-stage and small-scale ventures became increasingly pronounced.

Financing Deals in the Biopharmaceutical Sector Exceeding $100 Million Hit a Five-Year Low in 2022(accounting for 11% of all financing deals with disclosed amounts that year, totaling 47 deals),The proportion of financing rounds at or below the $1 million level hit a three-year high.(accounting for 31% of all disclosed financing events in that year, totaling 132 deals); this indicates that capital was more cautious about large-scale investments in 2022 and showed a stronger preference for smaller-ticket investments.

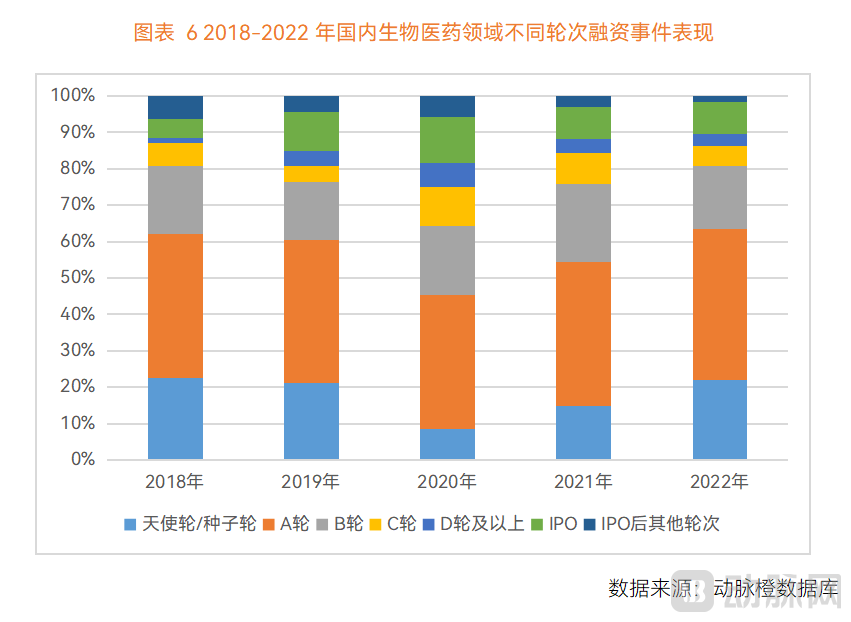

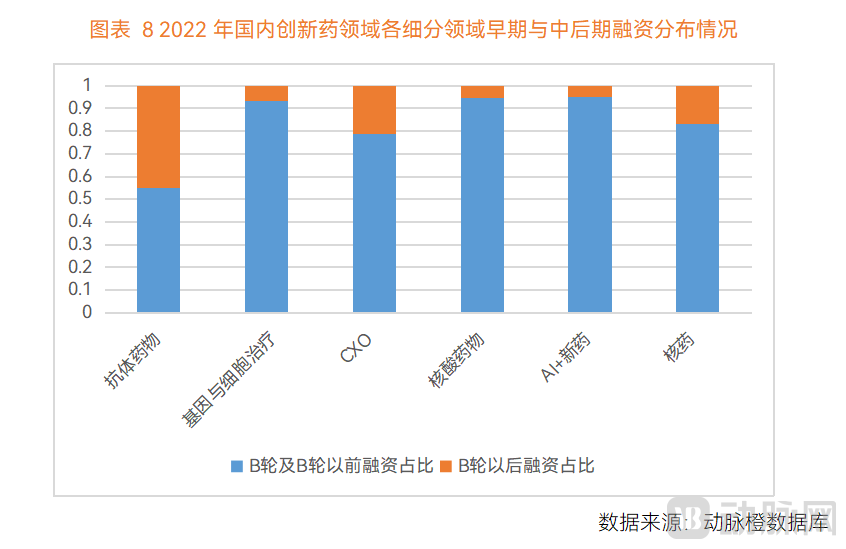

The Proportion of Financing Events in the Biomedical Field Before Series B Increased Significantly in 2022—Financing events accounted for 81% of all disclosed funding rounds, higher than in any year from 2018 to 2021, indicating that industrial capital is increasingly favoring early-stage investments.

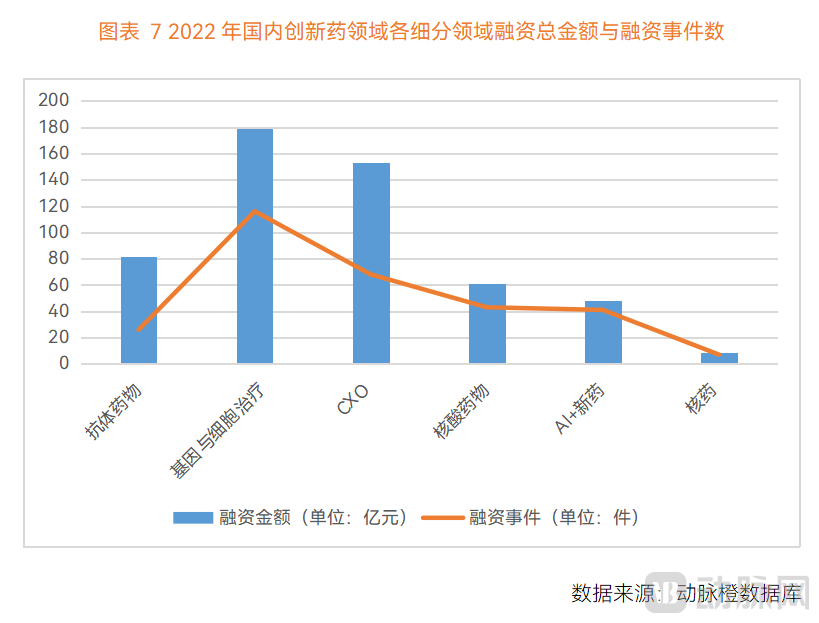

Sub-sectors: CGT and CXO are the most favored by capital; emerging technology tracks such as AI-driven drug discovery and nucleic acid therapeutics hold significant growth potential

In 2022, the cell and gene therapy (CGT) sector witnessed the highest level of investment and financing activity, with 116 financing deals totaling RMB 17.913 billion. The CXO sector maintained its strong momentum from previous years, ranking second with 68 financing deals amounting to RMB 15.328 billion. The antibody drug segment (including monoclonal antibodies, bispecific antibodies, ADCs, etc.) secured the third position in annual biomedical financing for 2022, with a total financing scale of RMB 8.175 billion.

Multiple companies in the antibody drug sector are launching IPOs, while emerging technology sectors such as AI-driven new drug discovery, nucleic acid therapeutics, and CGT remain in early-stage financing with significant growth potential.Funding rounds reflect, to some extent, the maturity of a sector: The antibody drug segment, with multiple listed companies such as RemeGen, Lepu Biopharma, and Mabwell, sees significantly more late-stage financing events (45% of financings occur after Series B). In contrast, emerging technology sectors—such as AI-driven drug discovery (95%), nucleic acid therapeutics (95%), gene and cell therapy (93%), and radiopharmaceuticals (83%)—have a higher number of early-stage financing events (Series B and earlier), indicating greater growth potential.

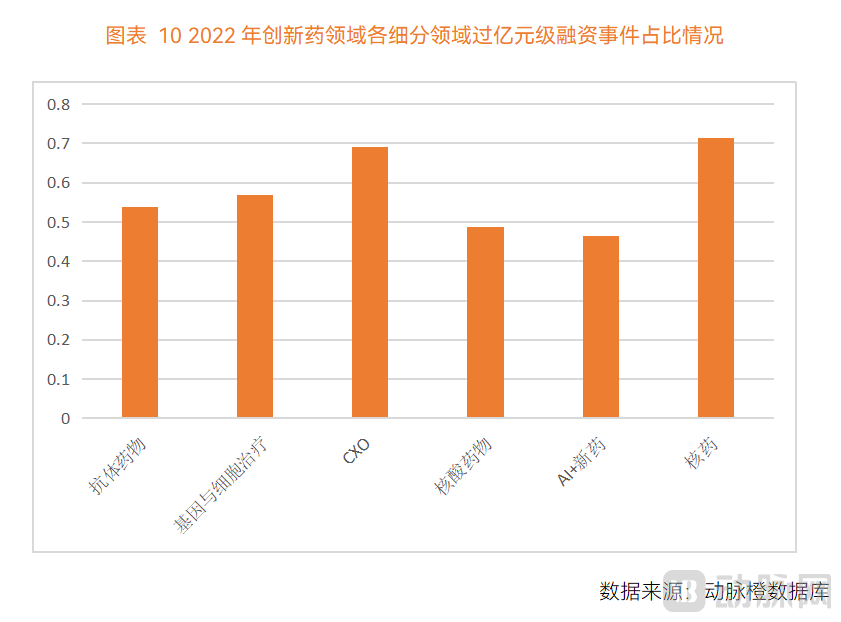

In capital-intensive sectors, radiopharmaceuticals and CXO companies are the most attractive to investors.In 2022, radiopharmaceuticals and CXO accounted for the largest proportion of financing rounds exceeding RMB 100 million (71% and 69%, respectively). Radiopharmaceuticals emerged as the most sought-after sub-sector, with the highest share of such large-scale financing events. The average single financing amount reached RMB 126 million, predominantly comprising early-stage deals (83% were Series B or earlier). Explaining the strong capital attraction in this sector, Ms. Wu Yixia, CFO of Fulian Pharma, noted that radiopharmaceuticals represent a cross-disciplinary field characterized by high industry barriers, scarcity of specialized talent, and capital-intensive operations, typically requiring substantial financial backing from enterprises.

Major Breakthrough: Peak Year for Global Approvals of Bispecific Antibodies and CGT; 12 New Clinical Assets Added to China’s AI-Driven Drug Discovery Pipeline

The concept of bispecific antibodies was first introduced in 1960,Due to its technical complexity, involving multidisciplinary and multi-technological fields such as genetic engineering, hybridoma technology, and recombinant biomacromolecules, 60Over the yearsThere are only four products worldwide.Approved(Catumaxomab, Blinatumomab, Emicizumab, Amivantamab), among which Catumaxomab was withdrawn from the market in 2017 due to poor sales performance.

After a prolonged period of exploration,2022 marked a boom period for the market launch of bispecific antibody products—with five bispecific antibodies launched in that single year, surpassing the total number approved over the previous several decades.In June 2022, the market launch of China’s first independently developed bispecific antibody drug (Cadonilimab; Chinese name: Kadunili Monoclonal Antibody) officially ushered in a wave of commercialization within the domestic market.

More than 30 companies in China are engaged in the development of bispecific antibodies, with over 300 drug candidates under investigation and nearly 100 having entered the Investigational New Drug (IND) stage. Representative players include Alphamab Oncology, BeiGene, Jiangsu Hengrui Medicine, Innovent Biologics, Beta Pharma, and Zai Lab.

In 2022, the total value of China’s top 10 license-out deals reached $14.5 billion, surpassing the total value of all such transactions in 2021 (30 deals, $13.3 billion).

Figure 12: Top 10 License-Out Drug Deals in China in 2022

(Data source: VCBeat)

Antibody drugs (including monoclonal antibodies, bispecific antibodies, and ADCs) are undoubtedly the protagonists, accounting for seven items.Notably, the ADC drug license-out transaction between Kelun-Biotech and Merck & Co. on December 22, 2022, and the bispecific antibody license-out deal between Akeso and Summit Therapeutics both set new records for overseas licensing of Chinese innovative drugs at the time.

Following the PD-1 wave, antibody-drug conjugates (ADCs) and bispecific antibodies are spearheading another surge in R&D activity, emerging as a new hotspot for competitive innovation.Medium and large enterprises in China have focused their efforts on these areas, capturing the majority of clinical pipelines. However, a small number of companies have carved out their own paths by leveraging distinctive competitive advantages and have gained recognition in the global market. For instance, Bio-Thera Solutions has developed more than 20 differentiated drug candidates (five of which have entered clinical trials) by relying on its proprietary H³ (High-throughput, High-content, High-efficiency) antibody discovery platform, SynTracer® high-throughput antibody internalization screening platform, and Flexibody™ bispecific antibody technology platform. The company has established 12 strategic global development collaborations with several leading pharmaceutical companies, including Pyxis, Celldex, OBI Pharma, ImmunoGen, and Chia Tai Tianqing Pharmaceutical Group.

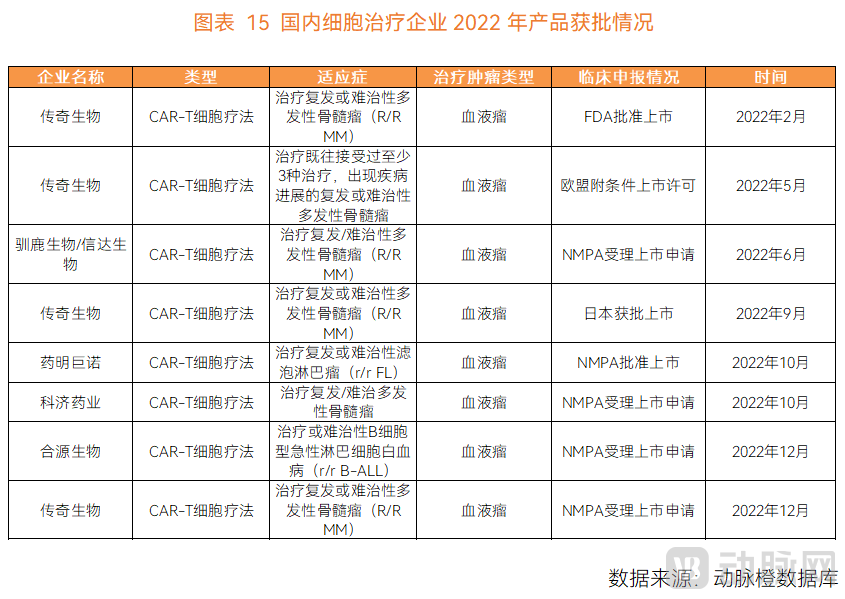

In 2022, a record-high eight cell and gene therapies were approved for market launch worldwide.

![6VO%9L8HW7{LR]L6UOYP@`Q.png](http://cdn.vcbeat.top/upload/image/06/01/15/43/1673765021446384.png/dmw)

Figure 13. Globally Approved CGT Therapies in 2022

(Data source: WuXi AppTec official WeChat account)

In terms of approved indications, gene therapies launched this year are primarily focused on rare diseases.Achieved groundbreaking milestones in certain disease areas, securing approval for the first gene therapies—including the first gene therapy administered via direct intracerebral injection and the first gene therapy for adult patients with hemophilia B.

In terms of cell therapy,Legend Biotech (NASDAQ: LEGN)’s self-developed cell therapy product ciltacabtagene autoleucel (brand name: CARVYKTI) has been successively approved for marketing in the United States, Europe, and Japan. In December,The World’s First “Off-the-Shelf” Allogeneic T-Cell Immunotherapy ApprovedRepresents a new breakthrough in the field of cell therapy.

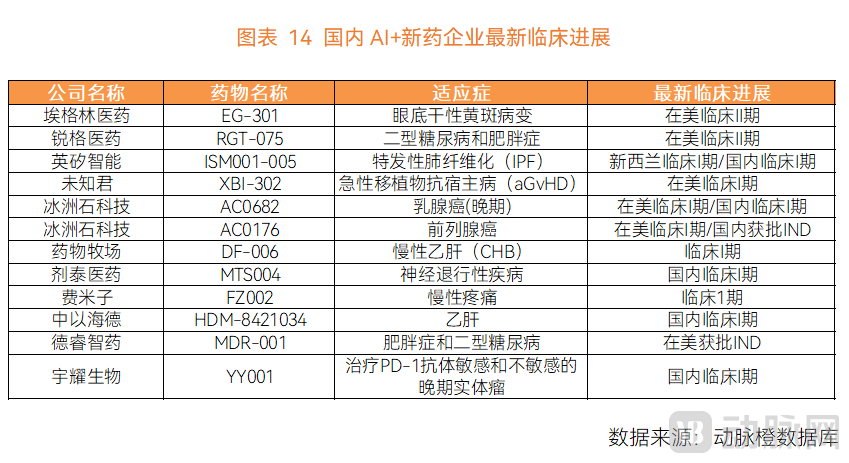

In terms of clinical progress, compared to 2021, when only a few AI-driven new drug companies advanced their pipelines into clinical trials, more domestic AI-driven new drug companies in China secured clinical assets from their AI-powered pipelines in 2022.

Some AI-driven pharmaceutical companies, despite their rapid growth, have maintained a relatively low profile. For instance, Aeglea Pharma has leveraged its proprietary AI drug discovery platform to develop two novel “AI Me-Only” drug candidates (EG-301 and EG-101). Among them, EG-301, an oral medication for the treatment of dry age-related macular degeneration (AMD), received FDA approval to enter Phase II clinical trials in February 2022. To achieve differentiated development and enhance the success rate of new drug development, the company previously conducted in-depth predictions on novel targets, disease mechanisms, intraocular efficacy, lysosomal pharmacokinetics, and development risks. Another company, Rigor Pharmaceuticals, announced in April 2022 that the first patient had been dosed in the United States in its Phase II clinical trial of RGT-075, a self-developed novel oral small-molecule GLP-1 receptor agonist.

Several well-established and renowned AI-driven pharmaceutical companies, such as IceStone Technology, announced in April and August 2022, respectively, that their products AC0682 and AC0176, which had already undergone Phase I clinical trials in the United States, received Investigational New Drug (IND) approval from the National Medical Products Administration (NMPA). Following the completion of Phase I patient dosing for its anti-fibrotic small molecule inhibitor ISM001-055 (for the treatment of idiopathic pulmonary fibrosis) in New Zealand in February 2022, Insilico Medicine completed Phase I patient dosing in China in July. In June 2022, MTI Pharmaceuticals’ independently developed Class 2.2 improved new drug, MTS004 orally disintegrating tablets, received IND approval from the Center for Drug Evaluation (CDE).

Several fast-growing industry newcomers, such as Zhongyi Haide, have initiated clinical trials for HDM-8421034, the first curative drug for hepatitis B developed using AI and big data technologies. Yuyao Biopharma’s investigational new drug application for its self-developed next-generation small-molecule EP4 receptor antagonist, YY001, has been approved by the NMPA. Fermion Technologies submitted IND applications in both China and the US for FZ002, a pipeline product efficiently developed based on its proprietary Drug Studio AI drug discovery platform for the treatment of chronic pain, in April 2022; the application was formally accepted by the NMPA in October 2022, with the first-in-human (FIH) Phase I clinical trial in China scheduled for February 2023. Reportedly, FZ002 targets a non-addictive analgesic mechanism and will become the second drug globally and the first in China to enter clinical trials targeting this specific pathway. MindDx’s self-developed small-molecule oral GLP-1 RA drug, MDR-001, has received clinical trial approval from the US FDA for the indication of obesity.

The release of AlphaFold2 has resolved the 50-year-old challenge in the biological community of predicting protein spatial structures, while also drawing greater industry attention to the AI-driven new drug sector and continuously attracting top-tier industrial talent to this field. For instance, in January 2022, Professor Jinbo Xu, a renowned computational biologist hailed by the industry as the “pioneer of AI-based protein folding technology,” founded Molecule Mind, which announced in April that it had completed tens of millions of US dollars in angel-round financing led by Sequoia Capital China. In September 2022, CarbonSilicon Intelligence completed RMB 50 million in angel-round financing jointly led by Lenovo Capital and Legend Star. The company was co-founded by Dr. Yafeng Deng, who brings twenty years of experience in artificial intelligence and previously served as CTO of DeepGlint and Vice President of 360 Group as well as Dean of its Artificial Intelligence Research Institute, and Professor Tingjun Hou, a Qiushi Distinguished Professor at the College of Pharmaceutical Sciences, Zhejiang University, who has over two decades of experience in computer-aided drug design.

In the coming years, more AI-designed drugs in China will enter clinical trials, and AI-driven drug candidates reaching the proof-of-concept (POC) stage for efficacy will no longer be isolated cases.In the short term, both successes and failures in AI-driven new drug pipelines are normal phenomena and will not alter the long-term trend of robust industry growth. The next three years will be a critical window for evaluating the output and R&D capabilities of various players in the AI-enabled drug discovery sector.

Based on VCBeat’s annual review of the innovative drug sector in 2022, this section focuses on two widely watched segments—CGT and CXO—covering four subsectors: cell therapy, gene therapy, CXO, and CGT CXO.

Cell Therapy: New Clinical Trends in Overcoming Solid Tumors and Developing Off-the-Shelf Products, Alongside Capital’s Strong Focus on Innovation and Differentiation

In terms of product approvals, the cell therapy products approved or submitted for New Drug Application (NDA) by domestic companies are still predominantly CAR-T therapies indicated for hematologic malignancies.

Yet the industry is already nurturing new changes.

Based on the clinical trial applications for cell therapy products,In terms of indications,In 2022, among the cell therapy products approved by Chinese companies to conduct clinical trials, 10 were developed for hematologic malignancies and 15 for solid tumors.Cell therapy products developed for solid tumors have overshadowed those for hematologic malignancies.

In terms of cell therapy types,In addition to the well-known CAR-T, there are also includingNovel cell therapy products, such as UCAR-T cell therapy, TCR-T cell therapy, TIL cell therapy, RAK cell therapy, STAR-T cell therapy, DNT cell therapy, MTCA-CTL cell therapy, and MASCT cell therapy, have begun to emerge.Successively entered clinical trials.

Figure 16. Clinical Approval Status of Products from Domestic Cell Therapy Companies in China in 2022

(Data source: VCBeat Orange Database)

In addition to the 23 companies that have already been approved to conduct clinical trials, there are alsoAdditionally, 11 other companies have submitted Investigational New Drug (IND) applications for their cell therapy products, which have been accepted by the National Medical Products Administration (NMPA); these products are also primarily cell therapies developed for solid tumors.(8 products, accounting for 73%),Cell Therapy Types Are Diverse.

In terms of investment and financing, capital has widely focused on innovative and differentiated projects, with the greatest willingness to invest in universal cell therapies.In 2022, there were 73 financing events in China’s cell therapy sector, with a total funding amount of RMB 7.191 billion. Among these, off-the-shelf cell therapies—such as UCAR-T, CAR-NK, iPSC-derived CAR-iNK, and in vivo CAR-T—have become the “darlings” of capital due to their potential to provide patients with more treatment options and their substantial future market prospects.

Specifically, in 2022, financing events in the cell therapy sector were predominantly concentrated in stem cell therapy (15 deals, totaling RMB 367 million), solid tumor treatment (13 deals, totaling RMB 1.25 billion), and universal/off-the-shelf cell therapy (12 deals, totaling RMB 1.529 billion), as well as niche areas such as NK cells (7 deals, RMB 820 million) and TILs (3 deals, RMB 917 million). There were virtually no investments focused on early-stage autologous CAR-T projects for hematologic malignancies. This indicates that following the period of homogeneous competition in domestic autologous CAR-T therapies for blood cancers and the subsequent funding winter in the biopharmaceutical market, capital has increasingly favored innovative and differentiated projects.

Supported by Policy H, China’s stem cell industry has entered a phase of rapid development in medical research and applications. Although stem cell therapy currently faces some skepticism, emerging technologies require time for validation. The field is transitioning from hematologic malignancies to solid tumors as the primary focus of immune cell therapies.Solid tumors, which account for more than 90% of all cancer cases, are undoubtedly the main battlefield for future efforts.

From the CAR-T Crowding to Diversified Development of Various Immune Cell Therapies, Addressing Clinical Needs and Cost Issues Is Core.Compared with autologous CAR-T cell therapy, which involves cumbersome and time-consuming manufacturing processes, high costs for personalized customization, and expensive pricing, universal cell therapies offer both potent anti-tumor activity and the potential for large-scale production. This significantly enhances the accessibility of cell therapies, making them a more ideal format for commercial application in the cell therapy sector. However, Fate Therapeutics, the leading company in CAR-NK/CAR-iNK therapies, sent a less-than-positive signal to the market at the beginning of 2023, which may dampen market enthusiasm for this therapeutic approach to some extent. Nevertheless, the fundamental advantages of CAR-NK cells, such as their favorable safety profile and suitability for allogeneic use, remain intact. Clinical exploration continues to be worthwhile, with expectations for major breakthroughs in efficacy. For a detailed analysis of specific subsectors within the cell therapy field, please refer to the white paper.

Gene Therapy: AAV Gene Therapy Dominates the Clinical Landscape, While the Potential of Gene Editing in Financing Is Beginning to Emerge

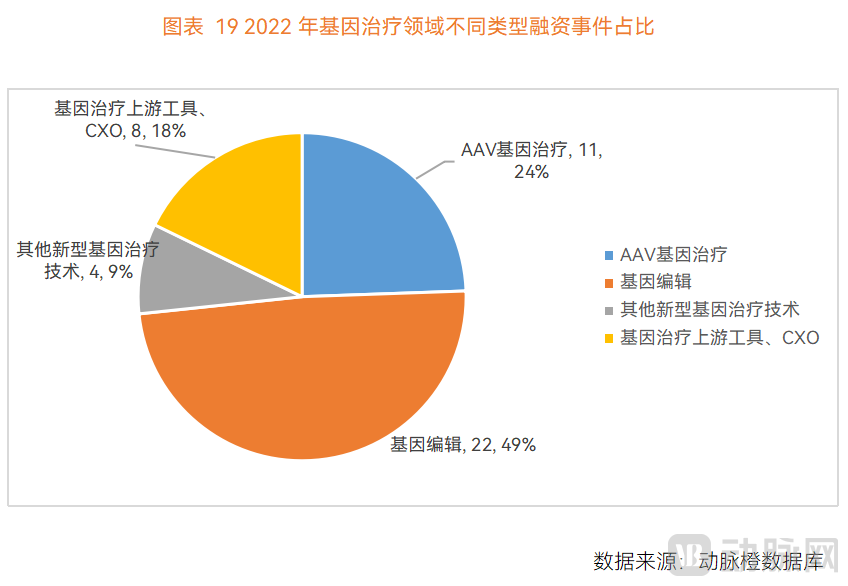

The successful commercialization of multiple AAV gene therapies worldwide has brought relatively high certainty to the AAV sector,AAV gene therapy also became the subfield with the largest number of domestic gene therapy companies advancing their pipelines into clinical trials in 2022.There are quite a few companies in China currently deploying gene-editing technologies, but relatively few drugs have entered clinical trials. This may be due to the higher technical challenges associated with gene editing and its later onset in China.

The situation in the primary market for investment and financing has shown differences compared to clinical trial applications.In 2022, companies investing in gene-editing technologies appeared to attract more capital favor than AAV gene therapy firms, representing a new trend in the industry’s future development.This is precisely similar to the current development of the gene therapy market abroad.

In the early years, before gene-editing companies went public, AAV platform companies were highly sought-after, butIn recent years, with the advancement of gene-editing technologies, gene editing has garnered enthusiastic investment interest. As the technology continues to evolve through successive generations, funding amounts have repeatedly reached new highs. Due toThe core foundational patents for gene-editing technologies are primarily held by certain foreign companies and academic institutions. As China’s gene-editing companies started later, there remains a gap in their current R&D capabilities compared with their foreign counterparts, necessitating further improvement.

Currently, China's gene therapy sector is in its early stages of development, offering substantial room for growth and numerous opportunities. 2023 marked a critical foundational phase, with the potential to reap rewards in 2024.

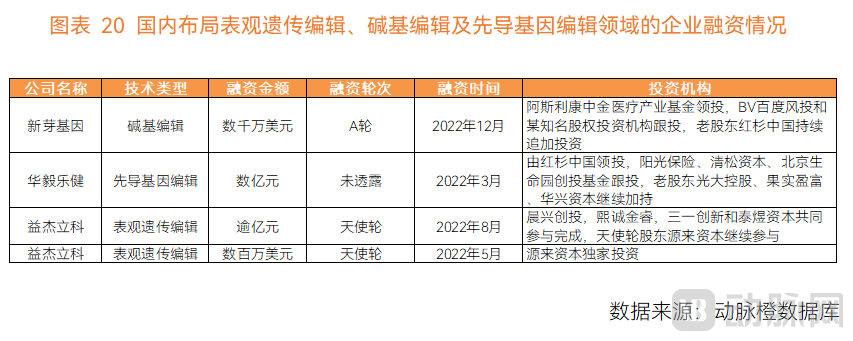

Epigenetic editing, base editing, and prime editing are novel gene-editing technologies that offer enhanced safety and higher efficiency. These technologies have gained significant momentum abroad in the past two years. Their emergence has unlocked substantial potential for the industry, making them a promising new sector worthy of attention in 2023.Currently, several Chinese companies are at the international forefront in terms of their technological pathways and have attracted significant capital attention. Multiple companies, including RayBiotech (Bangyao Biology), New Bud Gene, Huayi Lejian, and Yijie Like, have already begun to position themselves in this field, with several securing financing in 2022. This white paper provides a detailed analysis of the development of these cutting-edge technologies.

CXO: Specialization and Precision Are the Fundamentals for Attracting Capital, While Internationalization Has Become a Core Competitive Factor

As the “water vendors” of the industry, CXO companies have consistently enjoyed stable, recession-resilient revenues. Although the secondary market sector experienced significant volatility in 2022 due to the international environment, primary market enthusiasm for CXOs remained unabated. In 2022, CXOs secured the second-highest total financing amount in the innovative drug sector, raising RMB 15.328 billion across 68 financing deals.

Based on research interviews and desk research, the CXO sector remains highly active, primarily due to three factors (see the white paper for detailed analysis):

▷ The strategic shift of China's pharmaceutical industry from generic drugs to innovative drugs has fueled the rapid growth of the CXO industrial chain.

▷ In recent years, the difficulty of developing new drugs has continued to rise, accompanied by further increases in R&D costs and prolonged development cycles.

▷ The continuous enhancement of domestic CXO capabilities and the resource cost advantages in the Chinese market are attracting multinational pharmaceutical companies to shift their CXO orders to China.

The CXO Industry in 2022: Distinctively Characterized by Specialization, Precision, and Internationalization

The industry trend for CROs is an increasing demand for specialized expertise and a greater reliance on R&D strategy and top-level design.“Specialization and Precision” Become the Fundamental Criteria for Capital Investment in Innovative CROs.As domestic enterprises in China expand, their areas of involvement are becoming increasingly broad and diverse, with products growing more specialized. Given the significant technical disparities across various stages of pharmaceutical research and development, many large companies are unable to provide specialized guidance and services, thereby creating opportunities for growth and competition for emerging firms with strong professional expertise.

Going global is an unstoppable trend, with “internationalization” becoming a core competitive factor for the new generation of innovative CRO companies.

In recent years, the capabilities of China’s innovative pharmaceutical sector have strengthened, while pressure to reduce drug prices has persisted, creating an urgent need for domestic companies to expand into overseas markets. In 2022, the total value of license-out transactions reached a historic high, with the top ten license-out deals exceeding the combined value of all such transactions in 2021, demonstrating the R&D prowess of Chinese enterprises. As China’s basic medical insurance fund is the primary source of healthcare expenditure, the government holds core bargaining power, and new payment models capable of supporting high-risk innovative drug development remain unclear.Although China has a larger patient population, the size of its domestic market differs significantly from that of the global market.

To cite a specific example, in terms of the commercialization of two CAR-T therapies already approved in China, Fosun Kite’s Yikaida and JW Therapeutics’ Bei Nuoda are priced at RMB 1.2 million and RMB 1.29 million per dose, respectively. In contrast, overseas CAR-T therapies, such as Legend Biotech’s ciltacabtagene autoleucel, are priced at $465,000 (approximately RMB 3.2 million), nearly three times the price of domestic CAR-T therapies. However, ciltacabtagene autoleucel generated approximately $55 million in sales in a single quarter (Q3 2022), which already exceeded the combined annual sales of the two domestic CAR-T therapies in 2021 (Yikaida and Bei Nuoda achieved sales of approximately RMB 100 million and RMB 30.797 million, respectively, in 2021). Both in terms of product pricing and sales performance, domestic CAR-T products clearly lag behind their overseas counterparts.

Therefore, pursuing internationalization, enhancing global market competitiveness, adopting synchronized R&D in domestic and overseas markets, conducting international multi-center clinical trials, and ultimately achieving dual-market returns from “China + Overseas” have become the consistent choice for leading Chinese innovative pharmaceutical companies and a general trend in the industry. However, the challenges of going global are also evident. Given the significant differences in regulatory review and approval mechanisms across various regions worldwide, and facing the cumbersome and stringent new drug development and approval processes in the global market, Chinese innovative pharmaceutical companies require specialized and internationalized CXO (Contract X Organization) partners.

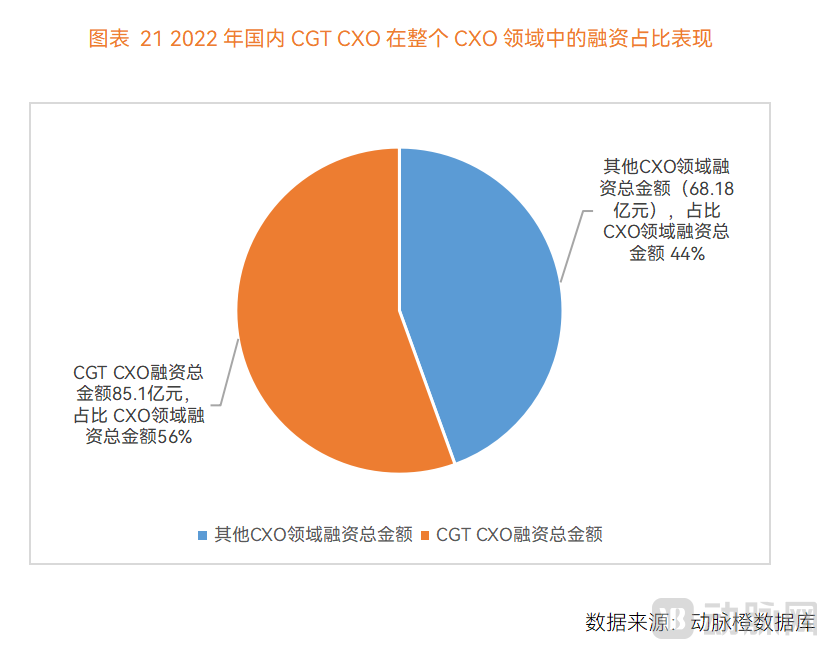

CGT CXO: High-Quality Capacity Remains Scarce, with Significant Growth Opportunities Still Emerging

Cell and Gene Therapy (CGT) CXO is a particularly noteworthy niche within the broader CXO sector. In 2022, there were 29 financing events in the CGT CXO segment, with a total amount reaching RMB 8.51 billion, accounting for 56% of the total financing in the CXO sector. The average financing amount per transaction was RMB 290 million.

The particular fervor surrounding CGT CXOs within the broader CXO landscape stems from two key factors: first, the rapid development of the CGT sector in recent years; and second, the paradox wherein CGT drugs face higher R&D and manufacturing barriers yet contend with a shortage of high-quality talent (see the white paper for detailed analysis).

Yet even as this field buzzes with activity, many industry insiders have stated thatHigh-quality manufacturing capacity in the cell and gene therapy (CGT) sector remains scarce.Rong Jing, Managing Director at BlueRun Ventures, also believes that the overall capabilities of companies in China’s cell and gene therapy (CGT) contract development and manufacturing organization (CDMO) sector are uneven, with very few high-quality talents coming from top-tier overseas CGT CDMOs.

Global expansion is an inevitable trend. For CGT CXO companies, securing overseas orders serves as proof of their capabilities and service standards, enabling them to gain industry influence and attract a substantial client base. However, the FDA’s stringent regulations and high requirements for CGT products make conducting business abroad particularly challenging.If teams with experience in developing FDA-approved CGT products enter China’s CGT CXO sector in the future, they will undoubtedly have significant opportunities.

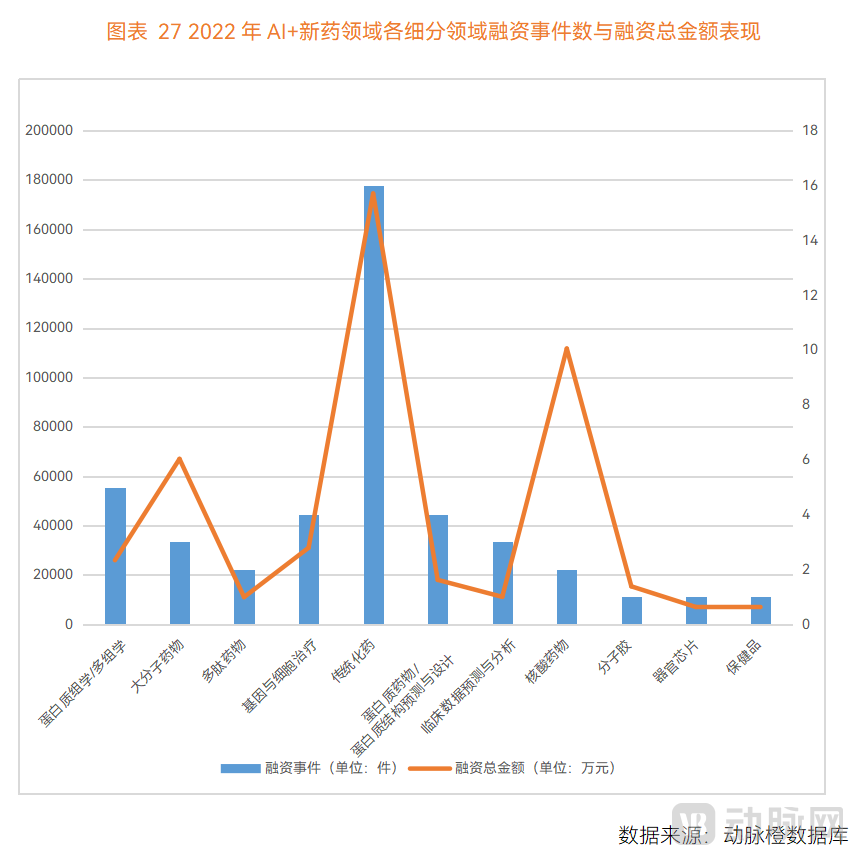

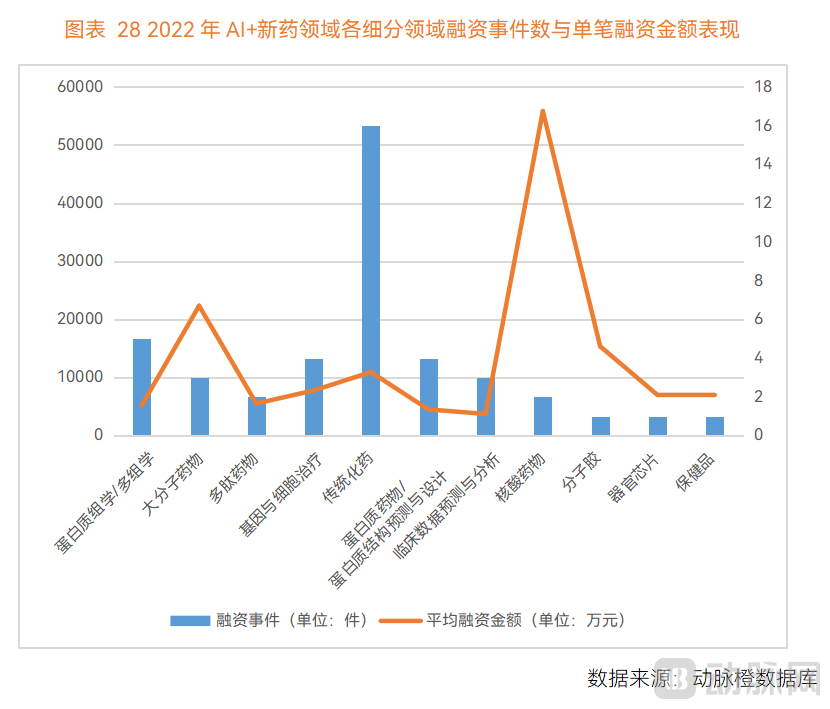

AI + New Drugs: AI-Driven Novel Therapies Hold Great Promise; AI-Empowered Clinical Trials for Cost Reduction and Efficiency Gains Deserve Attention

In terms of financing in sub-sectors in 2022, based on the advantages in three aspects: industrial development maturity, R&D risk, and industrial ecosystem support,Small-molecule drug discovery remains the most mature application area for AI. Meanwhile, as the technology continues to mature, companies leveraging AI to enable the development of novel therapeutic modalities are also emerging and attracting increasing attention from investors.

The frequency and total amount of capital deployment in the AI + novel therapeutics sector have surpassed those in the AI + traditional chemical drugs sector.——In 2022, there were 22 financing deals in the AI-enabled novel therapeutics sector, with a total funding amount of RMB 2.93 billion, surpassing both the number of deals (16) and the total funding amount (RMB 1.75 billion) in the AI-enabled traditional small-molecule drug sector. This clearly demonstrates investors’ strong preference for AI-enabled novel therapeutics.

The field of novel drug modalities harbors greater development opportunities. AI has begun to intervene at the early stages of development in this field, boasting broad prospects for future growth. In the future,With further advancements and breakthroughs in compound libraries, genomics, single-cell sequencing, proteomics, and other fields, the AI-enabled novel therapeutics sector is poised for stronger performance and greater opportunities.Worthy of the industry's attention.

Furthermore, as AI continues to extend its reach across the new drug development value chain, companies leveraging AI to empower clinical trials are increasingly attracting capital attention and investment.As clinical trial data become increasingly digitized, regulatory policies mature, and technology advances, AI is poised to significantly reduce costs and improve efficiency in the clinical development phase.

Nucleic Acid Drugs: Promising Frontline Innovations Such as Circular RNA Warrant Attention, While Nucleic Acid Delivery Systems Remain a Key Breakthrough

With the continuous advancement of biological technologies, nucleic acid therapeutics have garnered significant industry attention due to their immense potential in disease diagnosis and treatment. In 2022, there were 43 financing events in China’s nucleic acid therapeutics sector, with a total funding amount of RMB 6.1 billion. Financing rounds prior to Series B accounted for 95% of these events, indicating that this sector is in its early stages of development and holds substantial growth potential.

The launch of multiple mRNA vaccines, as well as several blockbuster antisense oligonucleotide (ASO) and small interfering RNA (siRNA) therapeutics, has largely mitigated the druggability risks associated with nucleic acid-based drugs. The emergence of lipid nanoparticles (LNPs) and N-acetylgalactosamine (GalNAc) conjugation technologies has also partially addressed delivery challenges. According to Rong Jing, Managing Director at BlueRun Ventures,If future delivery systems can be extended to specifically target other organs, it will further catalyze the development of nucleic acid drugs, bringing limitless possibilities to the industry.

Furthermore, from the perspectives of cost and clinical demand, nucleic acid drugs are particularly well-suited to the needs of the Chinese market. Taking the PCSK9 target as an example, the siRNA drug Inclisiran requires only one injection every six months, whereas monoclonal antibodies targeting PCSK9 necessitate two injections per month. Amgen’s PCSK9 monoclonal antibody, Evolocumab, was launched in 2015 and achieved annual sales of $1.1 billion in 2021.

Many investors have also paid close attention to cutting-edge innovations at the forefront, including circular RNA.Currently, several Chinese startups, including YuanYin Bio, HuanMa Bio, and CareMed, are focused on developing circular RNA therapeutics. Notably, YuanYin Bio and HuanMa Bio collectively secured over RMB 500 million in financing over the past two years, underscoring strong investor confidence in this sector. (For detailed analysis, please refer to the white paper.)

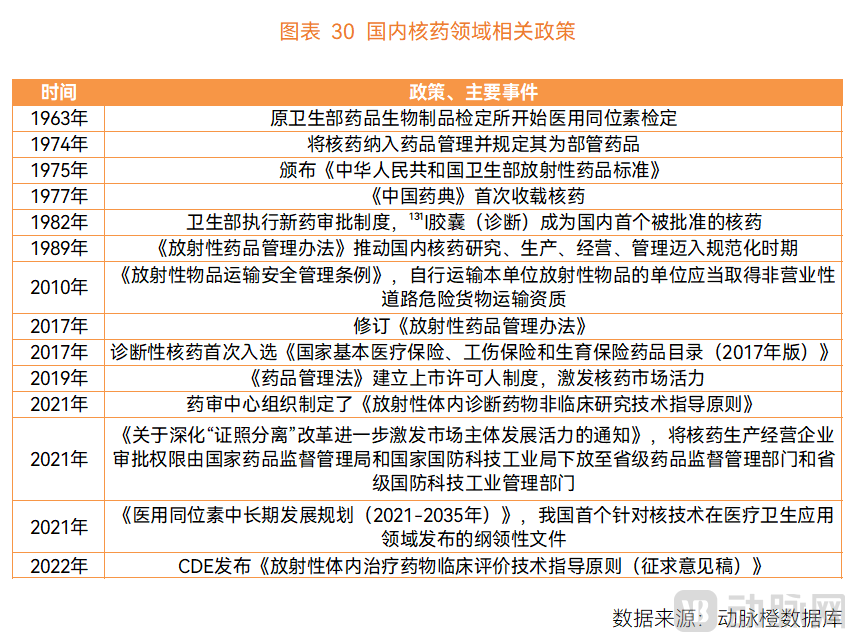

Nuclear Medicine: Policies Intensify, Top VCs Place Heavy Bets, and Production and Supply Challenges Present Both Obstacles and Opportunities

Driven by continuous technological advancements and supportive policies in recent years, nuclear medicine drugs have seen a surge in attention in 2022.

In March 2022, Novartis’ PSMA-targeting radiopharmaceutical Pluvicto received FDA approval for the treatment of prostate cancer, marking another significant milestone in the field of nuclear medicine. In 2022, multiple domestic innovative nuclear medicine companies announced the completion of new funding rounds in succession, with leading investment firms such as Sequoia China spearheading the two largest financing deals in the sector that year.

In November 2022, Focallink Pharma made another significant move that once again drew the attention of domestic industry professionals to the field of radiopharmaceuticals—announcing the acquisition of Focus-X Therapeutics for $245 million (approximately RMB 1.68 billion) to strengthen its pipeline of peptide ligand-based radiopharmaceuticals. Focus-X is an innovative company based in New Jersey, USA, that develops targeted radiopharmaceuticals for cancer treatment using its proprietary peptide engineering technology. By the end of 2022, industry interest and discussion in the radiopharmaceutical sector had far surpassed levels seen at the beginning of the year. For the biopharmaceutical industry, which remained shrouded in a “capital winter” throughout 2022, the radiopharmaceutical sector emerged as a “dark horse,” rapidly capturing public attention.

As an increasing number of radiopharmaceuticals become available, the nuclear medicine industry is gradually maturing. According to data from Medraysintell, the global nuclear medicine market was valued at approximately $6 billion in 2019. With more radiopharmaceuticals coming to market, the global nuclear medicine market is projected to reach around $30 billion by 2030.

China initiated the development of radioactive isotopes in 1956. The nuclear medicine market started relatively late, resulting in a significant gap compared with European and American countries. However, with continuous technological accumulation, China’s nuclear medicine sector has entered a period of rapid development. Moreover,The core production and supply challenges facing the radiopharmaceutical sector have instead created greater development opportunities and room for growth for Chinese radiopharmaceutical companies.In recent years, an increasing number of biotech companies have emerged in China’s radiopharmaceutical industry, while traditional pharmaceutical companies such as Hengrui Medicine and Grand Pharma have also entered the field.

With the continuous approval of an increasing number of radiopharmaceuticals, sustained R&D efforts by both established players and emerging innovators in China’s radiopharmaceutical sector, substantial financial backing from leading investors such as Sequoia Capital, and increasingly supportive policies, what surprises will unfold in the radiopharmaceutical field in 2023? It is a space worth watching and anticipating.

The above is an excerpt from the main content of the report,Scan the QR code to add the assistant and obtain the full report. Please initiate your inquiry after adding.

On Tuesday, January 31, at 8:00 PM, VCBeat New Medicine’s WeChat Channels account will host a live stream interpreting the report. Please refer to the poster at the end of this article and reserve your spot for the live broadcast. Stay tuned!

Report Reference Materials:

1. Outlook on the Breakthroughs in Gene Therapy at Home and Abroad Next Year. Fengshuo Venture Capital

2. CXO: Why Are Pharmaceutical “Shovel Sellers” So Sought After? | Xingtu Financial Research Institute

3. Leading CXOs Have All Entered the Fray, with 19 Companies Making Major Moves, but Is There Really a Need for So Many CGT CDMOs? – VCBeat New Medicine

4. [Exclusive] Jiyin Biology Secures Tens of Millions in Angel Funding to Accelerate Development of Universal Cell Therapies | VCBeat New Medicine

5. Approvals Hit Record High: A Comprehensive Guide to the Latest Trends in Cell and Gene Therapies – WuXi AppTec

6. Dual Antibodies at the Forefront, Advancing at Double Speed. Southwest Securities Research and Development Center

7. Multiple Companies Deploy Significant Resources with Innovative Technologies: Is the Duopoly in Radiopharmaceuticals About to Shift? – VCBeat New Medicine