2022 Innovative Medical Devices White Paper: Medical New Infrastructure Drives Market Recovery, Cardiovascular and Surgical Robotics Remain Hotspots

The novel coronavirus has posed severe challenges to healthcare systems worldwide, exposing deficiencies in medical resources across countries and making it imperative to strengthen public health infrastructure. At the national, societal, and individual levels, new demands and higher expectations have been placed on China’s healthcare service system. As a critical product on the supply side of the healthcare system, medical devices have become a highly scrutinized industry. Achieving self-reliance and control over core technologies has emerged as a defining challenge for the development of the medical device sector.

In recent years, domestic substitution and technological innovation have been the main themes driving the development of the medical device industry, giving rise to numerous outstanding medical device companies. The establishment of the STAR Market, the Hong Kong Stock Exchange’s Chapter 18A listing regime, and the Beijing Stock Exchange has provided more development platforms and opportunities for leading medical device enterprises, while also offering greater exit opportunities for institutions that have long supported the sector, significantly enhancing industry vitality.

Amid the rapid growth of the medical device industry, the sector is also upgrading toward high-quality development. Centralized volume-based procurement and health insurance payment reforms are continuously eliminating inefficiencies, accelerating market consolidation and upgrading, spurring the pursuit of greater cost-effectiveness, and fostering sound industry development.

In this context, Chinese medical device companies are continuously strengthening their independent R&D capabilities, with self-developed innovations taking root and gaining traction, while steadily catching up in foundational technologies and cross-disciplinary innovation.

In light of this, this white paper summarizes the major changes that occurred in the medical device industry during the challenging year of 2022.

Core Viewpoints

Policy: No Off-Limits Areas for Centralized Procurement, but Price Reductions Are ModeratingThe volume-based procurement (VBP) policy has entered a period of intensive implementation. Multiple high-volume, high-cost clinical products—including dental implants, orthopedic spinal implants, cardiac pacemakers, clear aligners, and ultrasonic surgical scalpels—as well as products in the consumer healthcare sector, have been included in centralized VBP programs. Although the scope of VBP coverage has expanded, recent rounds for several core products have signaled moderate price reductions, with procurement rules designed to leave greater room for companies to secure bids. The impact of VBP on market dynamics is primarily reflected in driving market consolidation, increasing market concentration, strengthening the position of industry leaders, and raising the market share of domestically produced products. As policy risks bottom out, market confidence in high-value medical device consumables is beginning to recover.

Investment: The medical device investment sector returns to rationality, with valuations of high-quality enterprises rebounding in the second half of the year.The healthcare investment market surged in 2021 before cooling rapidly in 2022, impacting the entire spectrum of innovative drugs, medical devices, and healthcare services. The decline in financing within the medical device sector is reflected not only in a reduced number of funding events but also in a slowdown in the growth of corporate valuations. Despite the overall market chill, the dynamic medical device landscape has seen several hot sub-sectors emerge, with numerous standout companies rising to prominence. In this challenging fundraising environment, enterprises that possess independent innovation capabilities, high technical barriers, and solutions addressing clinical needs continue to gain recognition from the capital markets.

The number of IPOs in the secondary market has declined, while new policies have diversified companies’ options for going public.The number of successful IPOs in the medical device sector also declined significantly in 2022. In terms of market performance, many companies saw their stock prices fall below the IPO price after listing, reflecting an overall trend of reduced fundraising scales, low trading volumes, and frequent instances of new shares breaking the issue price. Nevertheless, there were notable IPO successes in 2022; United Imaging Healthcare’s IPO became the largest medical-sector IPO on the STAR Market. Meanwhile, the opening of the fifth set of listing criteria on the STAR Market to medical device companies has provided more listing options for firms in this sector.

(Note: To obtain the full version of this report, please scan the QR code to add our assistant. If you have already added them, please initiate your inquiry.)

In 2022, a series of favorable policies were introduced to stimulate industry recovery. Policies were rolled out in three key areas—healthcare insurance payment reform, market access, and innovation incentives—to drive the development of China’s medical device industry.

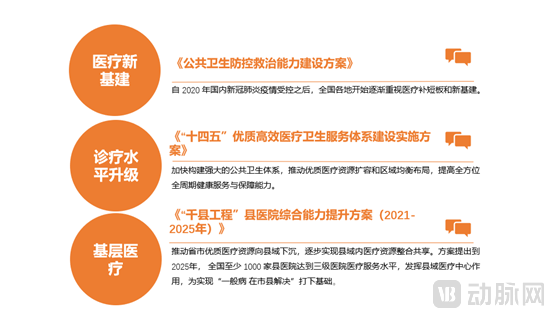

New Healthcare Infrastructure Drives Industry Recovery; Multiple Innovative Technologies Included in National Reimbursement Drug List

The ongoing implementation of the new wave of healthcare infrastructure development benefits leading domestic enterprises.Catalyzed by the COVID-19 pandemic, a global wave of new healthcare infrastructure development has surged, expanding the market size of medical devices. Among these drivers, fiscal interest-subsidized loans are expected to unlock hundreds of billions in demand for medical devices.

Multiple innovative medical technologies have been included in the national health insurance coverage, enabling innovative achievements to realize their commercial value in a shorter time.The commercial prospects for innovative technologies have become increasingly clear. A representative healthcare insurance policy promoting innovation in 2022 was Beijing’s inclusion of 53 assisted reproductive technology (ART) procedures in the basic medical insurance reimbursement scheme. Among these, 16 ART procedures, including intrauterine insemination, embryo transfer, and optimized sperm processing, were categorized under Class A reimbursement. The inclusion of ART in medical insurance benefits companies that master core ART technologies and products. Taking Reprocell Biotech as an example, although ART treatment has undergone significant development over the past three decades, key upstream products in this industry chain—namely reagents and consumables—have relied almost entirely on imports, creating a bottleneck for the development of China’s ART sector. Reprocell Biotech has successfully commercialized 36 products across four major series: sperm, oocyte, and embryo culture, as well as freezing and thawing. Its core products fill gaps in domestic production, lowering the cost barrier for ART. Driven by domestic substitution and favorable policies, the penetration rate in the ART sector is rising, leading to further industry expansion.

Healthcare Policies Are Being Refined Around Three Key Directions

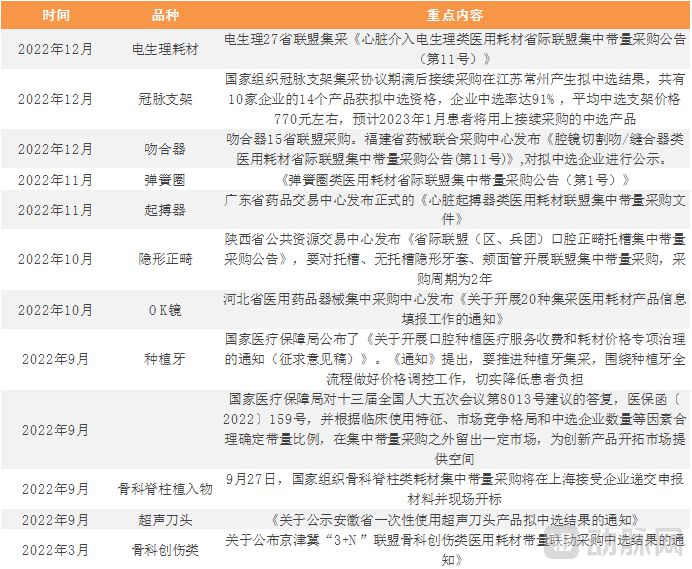

The intensity of price reductions in centralized procurement has moderated, while the influence of domestic enterprises is gradually increasing.

In 2022, the centralized volume-based procurement reform entered a phase of normalization and institutionalization. The price reductions from volume-based procurement have gradually moderated, which serves as a favorable development and protective measure for domestic enterprises.In 2022, volume-based procurement (VBP) was conducted nationwide for a variety of products characterized by high clinical usage, elevated market prices, and sufficient market competition. A review of the results from three national-level VBP initiatives—coronary stents (October 2020), artificial joints (September 2021), and spinal implants (September 2022)—reveals that average prices for coronary stents and artificial joints dropped by 93% and 82%, respectively, following procurement, while the estimated average price reduction for spinal implants ranged from 60% to 70%. From the perspective of national centralized procurement, the magnitude of price reductions has become more moderate. This narrowing of price cuts leaves greater profit margins for enterprises.

More rules protecting leading enterprises have also emerged in the setup of centralized procurement regulations., including the incorporation of ancillary services into centralized volume-based procurement (VBP), and the introduction of a guaranteed award rule in the VBP for spinal implants: enterprises can secure provisional winning bidder status as long as their bid prices reflect a reduction of at least 60% from the ceiling price (i.e., the bid price is no higher than 40% of the category-specific ceiling price). Based on the VBP shortlisting results, the number of enterprises shortlisted has also increased significantly.

2022 Policies on Centralized Procurement of Medical Devices

Early-Stage Financing Heats Up Amid the Winter Chill, with Gradual Recovery in H2 2022

In 2022, the overall transaction volume of medical device financing contracted, with multifaceted pressures leading to financing difficulties.In 2022, the overall investment and financing environment declined, with the healthcare investment sector shifting from a heated phase back to rationality. The total transaction volume in China’s healthcare industry failed to sustain its growth trajectory; particularly in the first half of 2022, influenced by various internal and external factors, the overall transaction volume contracted. The medical device sector also encountered bottlenecks.

The downturn in the financing market is driven by multiple factors. At the corporate level, homogenization has emerged within China’s medical device innovation ecosystem, consuming substantial innovation resources. Meanwhile, commercialization has fallen short of expectations across several sectors due to the prolonged training required for clinicians and the time-intensive establishment of distribution channels, posing challenges to market adoption and adding uncertainty to the commercialization of innovative medical devices. From a valuation perspective, the industry experienced a valuation bubble following the financing boom in 2021. In terms of external influences, the National Healthcare Security Administration has conducted multiple rounds of centralized procurement negotiations since its establishment, with the reality of “no excluded categories” in centralized procurement becoming evident in 2022. Policy uncertainties during the first half of the year have also exerted significant market and financing pressures on domestic medical device companies.

The long investment cycles in healthcare and the volatility of the primary market have driven away speculative “hot money” from this long-term sector. However, professional healthcare funds demonstrate greater patience toward cyclical fluctuations. Despite challenging external conditions, capital adhering to long-termism continued to support innovative technologies in 2022. In the second half of 2022, as pessimism eased and policy uncertainty diminished, healthcare investment gradually rebounded, with valuations of leading companies recovering and high-quality enterprises remaining well-regarded. Against this new market backdrop, early-stage investments and incubation-style deals began to increase.

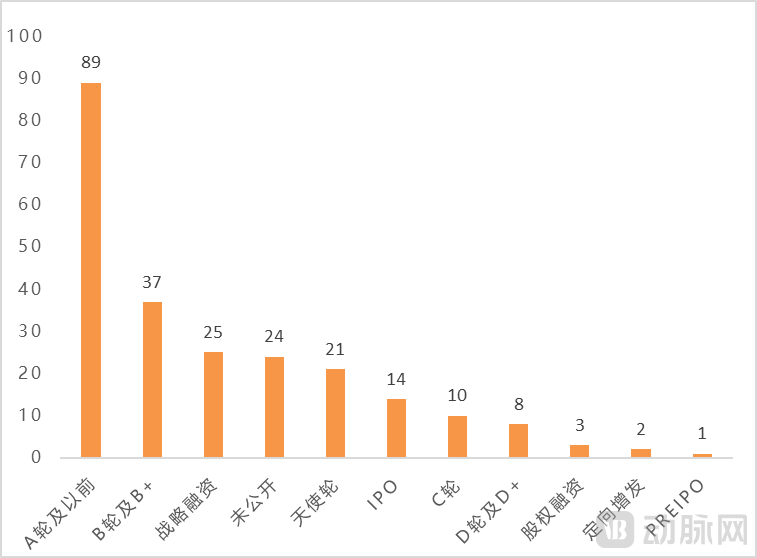

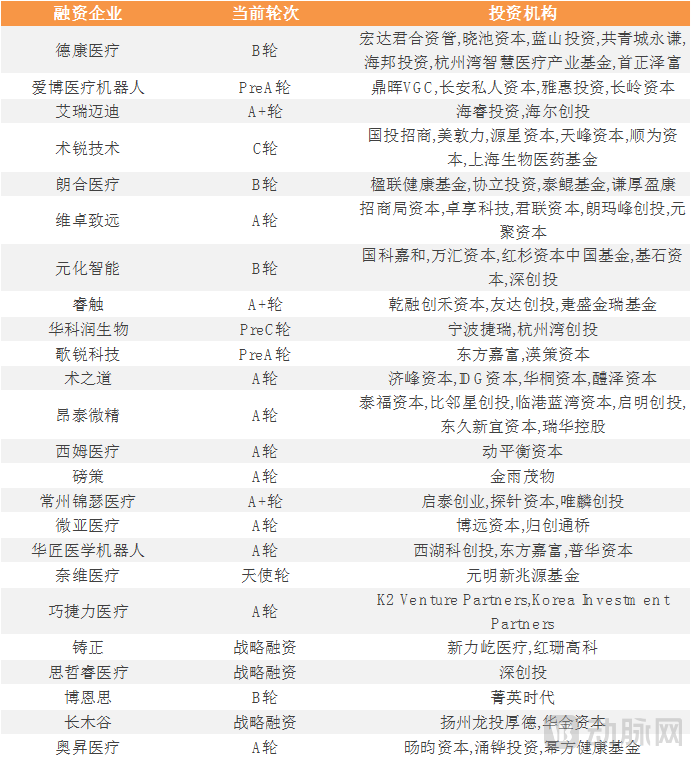

In terms of funding rounds, early-stage investment demonstrates higher activity compared to mid- and late-stage investment.More than half of the financing deals in the medical device sector occurred at Series A or earlier stages. In 2022, many large late-stage funds also established dedicated early-stage funds. The heightened enthusiasm for early-stage investments stems partly from the surge in innovative projects within the medtech field, as well as an overall acceleration in the pace of healthcare investment financing, with early-stage projects offering greater cost-effectiveness.

Distribution of Financing Rounds for Medical Device Companies in 2022

In 2022, a total of 17 medical device companies completed their initial public offerings (excluding in vitro diagnostic companies), among which 7 were listed on the Hong Kong Stock Exchange, 4 on the STAR Market, 5 on the ChiNext Board, and 1 on the Beijing Stock Exchange.

Compared with 12 medical device companies listing on the Hong Kong Stock Exchange and 16 on the A-share market in 2021, the pace of IPOs slowed in 2022, and the overall market sentiment cooled.

Hong Kong-listed healthcare companies remain in a period of adjustment, while Hong Kong’s healthcare technology sector continues to languish.

In 2022, the Hong Kong stock market remained sluggish, with poor liquidity for newly listed stocks.In 2022, medical device companies faced challenges in listing on the Hong Kong Stock Exchange (HKEX), with an overall trend of reduced fundraising scales, low trading volumes, and frequent instances of new stocks breaking their issue prices. Meanwhile, medical device companies listed on the HKEX in 2022 generally issued a relatively small proportion of free-float shares; even those with higher free-float ratios did not exceed 10%.

The Fifth Set of Listing Criteria for the STAR Market Has Been Introduced, Diversifying Financing Channels for Medical Device Companies Going Public.In the A-share market, a notable change in 2022 was the diversification of financing channels for medical device companies going public. In 2022, ten medical device companies listed on the A-share market, with five on the ChiNext Board, one on the Beijing Stock Exchange (BSE), and four on the STAR Market. Among these different trading venues, the STAR Market emphasizes scientific and technological innovation attributes and imposes high requirements on future profitability. In June 2021, the Shanghai Stock Exchange issued the "Guidelines for the Application of Review Rules for Issuance and Listing on the SSE STAR Market No. 7—Application of the Fifth Set of Listing Standards to Medical Device Companies," to support the listing of unprofitable innovative medical device enterprises. This initiative has provided a new listing channel for "hard-tech" companies in the medical device sector, creating additional listing opportunities for medical device firms that are still in the R&D phase and have not yet generated significant revenue. At the same time, it has imposed stricter requirements on applicant companies' R&D capabilities, development prospects, and compliance from various perspectives, including core technologies, phased achievements, market potential, technological advantages, sustainable operating capabilities, and information disclosure.

Previously, companies that successfully listed under the fifth set of listing standards were primarily innovative biopharmaceutical firms, with no innovative medical device enterprises having achieved a successful listing under these criteria. A key reason for this was the lack of clear operational guidelines for medical device companies applying under the fifth set of listing standards. The new regulations clarify the circumstances and requirements for medical device companies to qualify under the fifth set of listing standards, primarily benefiting medical device firms preparing for IPOs on the Hong Kong Stock Exchange, as well as innovative medical device companies that have encountered financing obstacles in the primary market.

The Beijing Stock Exchange has attracted attention from small and medium-sized medical device companies.Since its establishment in 2021, the Beijing Stock Exchange (BSE) has brought significant benefits to medical device companies. On one hand, in terms of industry characteristics, the BSE’s focus on serving “specialized, refined, distinctive, and innovative” (SRDI) small and medium-sized enterprises (SMEs) and technology-based SMEs aligns well with the fragmented nature of niche segments within the medical device sector. The medical device industry features numerous subfields with high technical barriers and potential for import substitution, yet many have limited market ceilings, resulting in relatively small scales for leading players in certain niches. The establishment of the BSE provides earlier exit channels for investors in the healthcare industry, helping to attract more capital into the medical device sector. For medical device companies, diversified financing channels will further promote their fundraising and development, empowering niche market leaders to grow stronger and overcome critical technological bottlenecks.

On the other hand, compared with the STAR Market and the Hong Kong Stock Exchange (HKEX), the STAR Market imposes stricter requirements on innovation attributes. Specifically, it mandates that a company’s cumulative R&D expenditure as a percentage of revenue over the past three years be no less than 15%, whereas the Beijing Stock Exchange (BSE) requires only no less than 8% over the past two years. Furthermore, the BSE has lower thresholds for scientific and technological innovation indicators, such as R&D achievements, making it more suitable for start-ups. Against the backdrop of sluggish performance in the Hong Kong stock market and the stringent innovation attribute restrictions of the STAR Market, the BSE became the choice for many small and medium-sized medical device enterprises in China in 2022.

In the medical device investment ecosystem, mergers and acquisitions (M&A) have also become a key strategy. Volume-based procurement policies under healthcare cost containment have placed growth pressure on mature business lines. Given the rapid product iteration characteristic of the medical device industry, M&A offers a swift means to break through corporate growth ceilings and capture high-potential niche markets. Compounding this, the capital winter of 2022 led to declining enterprise valuations. These combined factors have imposed significant survival pressures on medical device companies. Consequently, M&A and license-in agreements have become essential fast-track pathways for their development. For medical device investors, M&A provides more diverse exit channels, shortens the capital circulation period within the industry, and enhances industrial vitality.

In 2022, the medical device sector witnessed several landmark mergers and acquisitions, with both cross-border M&A transactions and domestic M&A activities on the rise.

Major M&A Events in China's Medical Device Sector in 2022

2022 Global Mergers and Acquisitions in the Medical Device Industry

The primary types of mergers and acquisitions can be categorized into three groups.

First, small and medium-sized medical device product lines are being complementarily integrated to foster collective resilience and enhance competitiveness in the overall market.Strengthening Risk Resilience. The intensity of consolidation among small and medium-sized enterprises (SMEs) has also been influenced by volume-based procurement (VBP) policies. Although China’s medical device market continues to maintain a high-growth trajectory, VBP has compressed the market size in certain niche segments, reshaping the existing competitive landscape and driving mergers and acquisitions (M&A) among companies. A representative example of product-line complementary integration in the medical device sector in 2022 was the acquisition of neurointerventional company Puweisen Medical by peripheral interventional company Purui Medical.

Second, platform companies’ acquisitions of leaders in vertical sectors.In the medical device sector, there are no giants without mergers and acquisitions (M&A). M&A is a critical strategy for the growth of medical device companies. Compared to other subsectors within the healthcare industry, the medical device industry has a greater need for M&A. From a product perspective, the medical device industry is characterized by fragmentation and discrete manufacturing, with significant barriers between various subsegments. Product technologies are undergoing rapid iteration, and new technologies often have a disruptive impact on older ones. From a market perspective, the growth ceiling in each medical device subsegment is clearly defined. If companies fail to further expand their market share, intense external competition will quickly lead to a decline. Acquisitions can supplement product pipelines, ensuring that established enterprises maintain a competitive advantage in emerging technologies and markets.

A typical case of platform-type M&A acquiring a leader in a vertical sector in 2022 was Boston Scientific’s acquisition of Acotec, the leading domestic player in peripheral interventional devices.

Third, cross-industry M&A: medical device companies are intensifying their digital M&A efforts.As the scope of the medical device industry continues to expand, digital technologies are increasingly empowering traditional medical device products. This trend is particularly evident in overseas mergers and acquisitions, where global giants have directed their acquisition strategies toward the digital sector. In 2022, major companies such as GE HealthCare, Stryker, and BD (Becton, Dickinson and Company) acquired digitally focused enterprises. Meanwhile, a wave of digital health companies has emerged in the domestic market, driving innovation in traditional medical devices.Taking the niche of miniaturized ultrasound combined with AI-assisted remote diagnosis as an example, Shenzhen-based Deepwise Technology has targeted challenges in primary care medical imaging, such as complex operational procedures and high diagnostic thresholds. The company independently developed features including scan navigation, lesion detection, and integrated image-text reporting. By leveraging artificial intelligence models to enhance image quality and implementing intelligent settings to lower the barrier to entry for using miniaturized ultrasound devices, Deepwise has significantly improved accessibility. Within just two years, the company built an algorithmic model imaging database covering more than ten categories and over 30 disease types, along with an ultrasound imaging cloud center. This infrastructure enables AI-assisted screening and diagnosis for more than 20 disease conditions using miniaturized ultrasound. Furthermore, Deepwise has obtained or applied for over 151 domestic and international patents in areas such as ultrasound hardware, artificial intelligence systems, chips, and cloud computing.

>>>>

Vascular Intervention Accumulates Strength for Breakthroughs; Peripheral Intervention Sector Leads in Financing Deals

Diverse Demand for Peripheral Interventions, with Innovative Technologies Catalyzing Market Growth.Compared with coronary intervention, the peripheral intervention market boasts a large patient base and strong growth momentum; compared with neurointervention, it features diverse procedural techniques and broad market potential. The existing peripheral intervention market, encompassing both peripheral arterial and venous interventions, is dominated by multinational corporations, but Chinese enterprises are rising rapidly, strategically positioning themselves in frontier areas, with multiple core products nearing commercialization. Penetration rates for innovative products in the peripheral field—such as thrombectomy systems, TACE (Transarterial Chemoembolization) therapy, venous closure systems, peripheral drug-coated balloons, and venous stents—remain low. Domestic companies are poised to secure first-mover advantages in these emerging technological domains.

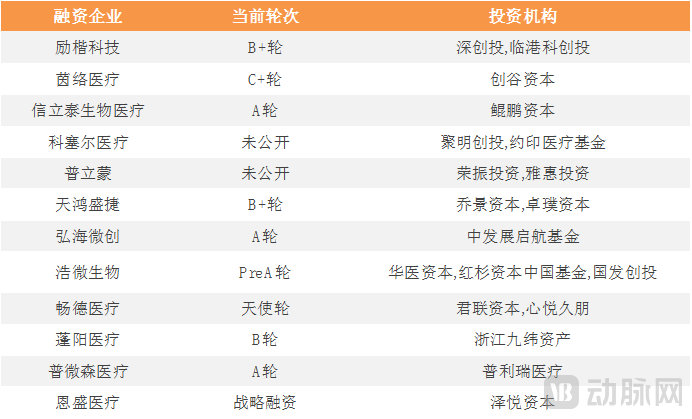

Major Financing Events in the Vascular Intervention Field in 2022

Taking the venous closure system for the treatment of varicose veins as an example, the prevalence of varicose veins in China ranges from 8.89% to 15%, with over 100 million patients. Endovenous closure is a cutting-edge approach for treating varicose veins. It involves injecting medical adhesive into the venous lumen to completely seal incompetent veins, thereby eliminating venous reflux. By sealing the great saphenous vein with venous closure adhesive, this method achieves a permanent cure for varicose veins. Unlike traditional open stripping surgery and thermal ablation, this therapy employs a minimally invasive technique using innovative specialized medical adhesives to precisely seal severely affected areas in the lower extremities of patients with varicose veins. This approach results in minimal surgical trauma and significantly reduces operative time.

This product has been widely proven effective and commercially valuable in the global market, yet no such product has been approved in China. Among domestic companies, Ensheng Medical’s self-developed venous closure system has completed enrollment of all study subjects and is poised to become the first approved product in the country. The venous closure system offers advantages including minimally invasive convenience, superior patient experience, softness after curing, and non-thermal operation, pioneering a new “non-thermal endovenous closure” technique for the treatment of varicose veins in clinical practice in China.

Structural Heart Disease Takes Center Stage in Innovation and Upgrading; Artificial Hearts Emerge as a Multi-Billion-Dollar Opportunity

The advent of new technologies in structural heart disease has ushered in and represents the fourth cardiac revolution in interventional cardiology. Since 2018, structural heart disease has become the central theme of innovation and upgrading in China’s cardiovascular medical device industry. Structural heart disease encompasses four major areas: treatment of congenital heart disease, treatment of valvular heart disease, prevention and treatment of atrial fibrillation, and adjunctive therapy for heart failure. The maturity levels vary across these subfields of interventional therapy for structural heart disease. Interventional treatment for congenital heart disease is the most mature; interventional valvular therapy is experiencing rapid development; atrial fibrillation prevention is in its early stages of development; and adjunctive therapy for heart failure remains in an early exploratory phase. In the primary market, the sectors attracting significant attention are valvular heart disease, electrophysiological therapy for atrial fibrillation, and heart failure treatment.

High R&D Difficulty for Interventional Mitral and Tricuspid Valves, with Large Market ExpectationsThe transcatheter heart valve market comprises interventional therapies for the aortic, mitral, and tricuspid valves. Among these, a major trend for TAVR (Transcatheter Aortic Valve Replacement) products is their expansion to younger patients, driven by improvements in anti-calcification properties and durability. For physicians, another key focus is enhancing implantation success rates through more precise device deployment. Beyond aortic valves, innovations in transcatheter mitral and tricuspid valve interventions are also garnering attention. Clinically, the patient population with mitral and tricuspid valve disease is larger than that with aortic valve disease; however, the development of interventional therapies for the mitral and tricuspid valves has lagged behind. The mitral and tricuspid valves are considered to be the primary components of the future structural heart disease market.

However, the research and development of mitral and tricuspid valve products present significant challenges. Taking the mitral valve as an example, its high anatomical complexity (including the annulus, leaflets, chordae tendineae, and papillary muscles), the diverse pathology and anatomy of mitral regurgitation, and the influence of atrial and ventricular function and size all contribute to this difficulty. Consequently, the design of mitral valve interventions must account for factors such as highly mobile leaflets, complex chordal apparatuses, and the three-dimensional structure of the annulus. Furthermore, the design of transfemoral venous delivery systems faces the challenge of navigating the longest and most tortuous pathways, while post-implantation fatigue durability remains a critical design hurdle and a severe test.

Among the many companies establishing a presence in the structural heart disease sector in China, Dejin Medical has risen to the challenge by developing multiple products targeting the therapeutic difficulties associated with mitral and tricuspid valve disorders. Dejin’s core product portfolio includes the MitralStitch Mitral Valve Repair System, the DragonFly Transfemoral Mitral Valve Clip System, and the DragonFly Transfemoral Tricuspid Valve Clip System. Notably, the MitralStitch Mitral Valve Repair System represents China’s first transapical interventional therapy technology, serving as a dual-purpose solution for both artificial chordae tendineae repair and edge-to-edge repair. The DragonFly® Mitral Valve Clip System is projected to be the first transfemoral TEER (Transcatheter Edge-to-Edge Repair) product to launch on the Chinese market.

Upgrades in Electrophysiology PFA Technology Spark a Wave of Domestic Substitution.

Although centralized procurement has been implemented in the field of cardiac electrophysiology, it has not dampened the sector’s popularity in the primary market. This is primarily driven by the development of Pulsed Field Ablation (PFA), a breakthrough technology. Traditional electrophysiological ablation includes two modalities: radiofrequency ablation (thermal ablation) and cryoablation (cold ablation), with radiofrequency ablation dominating the atrial fibrillation (AF) ablation market. Radiofrequency ablation for AF is technically complex, requiring initial 3D system modeling and mapping, followed by point-by-point circumferential or linear ablation using a radiofrequency catheter. The procedure often lasts up to two hours, significantly longer than percutaneous coronary intervention (PCI), and demands high operator expertise. Although the advent of cryoablation has addressed some limitations of radiofrequency ablation, both techniques are fundamentally non-selective. Consequently, the ablation process may inadvertently affect surrounding healthy tissues, potentially causing damage to the esophagus, coronary arteries, and phrenic nerve.

Pulsed Field Ablation (PFA) technology utilizes high-intensity electric field stimulation over an extremely short duration (10⁻⁹ to 10⁻⁶ seconds). By leveraging the coupling effect between the electric field and cells, it specifically disrupts the cell membrane structure of target cells, thereby disturbing their physiological balance and achieving selective ablation of specific tissues. In the context of atrial fibrillation (AF) ablation, PFA demonstrates significant technical advantages over radiofrequency and cryoablation, including higher success rates, enhanced safety (due to its non-thermal mechanism and tissue selectivity, resulting in minimal complications), reduced procedural complexity, and a shorter learning curve.

In this sector, numerous domestic companies have made strategic moves. Taking Ruidi Bio as an example, the company has developed a nanosecond pulsed tumor ablation system and a pulsed field ablation system for cardiac atrial fibrillation, based on its pulsed field ablation technology platform. This has expanded the application scenarios of pulsed field ablation technology to address unmet clinical needs in various fields, including oncology, cardiology, pulmonology, gastroenterology, and brain-computer interfaces.

The Surgical Robotics Sector Heats Up Amidst Intense Competition; Core Proprietary Technologies Remain Highly Favored

In 2022, despite the downturn in healthcare investment, the surgical robotics sector remained highly active.Completed over 24 financing rounds, with Jingfeng Medical and Sizerobotics racing toward IPOs.

Financing in the Surgical Robotics Sector in 2022

Domestic Robots Face Commercialization Challenges, with Original Breakthrough Technologies Poised to Break the Deadlock.The primary challenge facing surgical robots in China is commercialization; even leading companies struggle with revenue generation and high valuations. Different categories of surgical robots encounter distinct challenges in exploring their commercialization pathways. For laparoscopic surgical robots, given the high market recognition of the da Vinci Surgical System, the key to commercialization for Chinese manufacturers lies in demonstrating product reliability and efficacy while establishing differentiated advantages.

For orthopedic surgical robots, current models offer relatively limited functionality, assisting surgeons with only a portion of intraoperative tasks. In China, there is a shortage of more sophisticated surgical robots capable of supporting a wider range of surgical procedures. Meanwhile, the extent to which core components have been domestically mastered also constrains, to some degree, the development of surgical robots in China.

After years of development, domestic companies are also actively exploring new commercialization pathways for surgical robots. In the past, Chinese surgical robots followed a development path centered on imitating mature overseas products; in recent years, domestic enterprises have increasingly sought to address clinical needs through original technologies.

Taking the pelvic reduction surgical robot as an example, closed reduction of pelvic fractures is internationally recognized as one of the most challenging procedures in trauma orthopedics. On one hand, the extremely complex three-dimensional structure of the pelvis is difficult to fully visualize through intraoperative fluoroscopy, posing a significant challenge to clinicians' spatial imagination. On the other hand, closed reduction requires precise adjustments in position and orientation under high loads; however, it is difficult for the human body to simultaneously control speed and precise displacement while exerting force, which has long been a pain point in clinical practice. Noitom, a Chinese company, has developed the HoloSight ZhiJian Trauma Surgical Robot. This system leverages high-precision optical positioning and tracking technology combined with mixed reality technology to display bone position and posture in real time as 3D models on a computer terminal. Furthermore, by flexibly adjusting the position and angle of planning lines, the system assists physicians in surgical planning and formulating operative strategies, thereby helping them perform highly complex surgeries.

The Window of Policy Opportunity for CROs Arrives: Scale and Profitability Become Core Competencies

In 2022, driven by increased domestic investment in medical device R&D and the impetus of regulatory reforms, China’s medical device CRO and CDMO sectors entered a period of policy-driven opportunity and rapid growth. The high-speed development of China’s medical device CRO industry is propelled by two main factors: on one hand, Chinese medical device companies are placing greater emphasis on R&D, while capital market reforms—exemplified by the STAR Market and Chapter 18A of the Hong Kong Stock Exchange Listing Rules—have opened up financing channels for innovative medical device enterprises, channeling more funds into the R&D value chain; on the other hand, the continuous improvement and increasing stringency of global medical device regulatory frameworks have imposed higher requirements on product registration processes for medical device manufacturers.

In the rapidly growing medical device CRO market, three capabilities have become core competitive advantages for enterprises: specialization in serving the diversified needs of downstream device manufacturers; global service capabilities amid the accelerating international expansion of device products; and full lifecycle service offerings.

Among domestic institutions investing in the medical device sector, Legend Capital invested in three medical device CRO/CDMO-related companies within a single year. Notably, Haihe Biology received an exclusive investment of over RMB 100 million from Legend Capital. As a full-lifecycle outsourced service provider for medical devices, Haihe Biology has been deeply engaged in the industry for nearly two decades. Its client base spans numerous multinational corporations, domestically listed companies, and innovative medical device enterprises, establishing it as a leading private-sector institution in China for medical device testing, inspection, and regulatory consulting.

Rehabilitation Sector Sees a Surge in Financing; Rehabilitation Robotics Is on the Rise

From Neglect to Rapid Growth: Intelligent Products Fill the Gap in the Rehabilitation Industry.Rehabilitation medicine, together with preventive medicine, clinical medicine, and healthcare medicine, is recognized by the World Health Organization as one of the “Four Pillars of Medicine.” China’s healthcare system has historically prioritized emergency care and treatment while neglecting prevention and rehabilitation, resulting in an insufficient overall supply and uneven distribution of rehabilitation resources. There is a severe shortage of rehabilitation professionals; China faces a deficit of approximately 300,000 rehabilitation therapists, and the quality of domestic rehabilitation training varies significantly. Over the past two decades, the majority of China’s rehabilitation products have relied on imitating overseas technologies, with innovation primarily originating from abroad. Consequently, China has mainly produced relatively low-end products.

China’s rehabilitation assistive device market has entered a new phase of development, with the trend toward intelligence leading the growth of the rehabilitation equipment sector and industry development shifting from policy-driven to market-driven.The core challenge to be addressed in the current wave of intelligent innovation is achieving intelligent human-computer interaction by integrating technologies such as smart sensors, the Internet of Things (IoT), and big data. Rehabilitation robots are leading the trend toward intelligent rehabilitation equipment, with the majority of rehabilitation companies that secured financing in 2022 being rehabilitation robot enterprises.

Taking Anjie Lai as an example, he has dedicated himself to studying the clinical rehabilitation mechanisms and logic for hemiplegia patients. By integrating neurorehabilitation theories based on brain plasticity, he independently developed the LiteStepper™ single-lower-limb exoskeleton rehabilitation robot. The LiteStepper™ collects gait data from the patient’s unaffected side during voluntary movement, identifies their motion intent, and drives the affected limb to perform rehabilitation training synchronized with the unaffected side. This establishes an interactive pattern between the unaffected and affected limbs, promoting the重塑 of neural control functions in the brain. Ultimately, it achieves seamless human-machine integration, delivering significant therapeutic effects while substantially shortening the rehabilitation period.

Capital markets always experience ups and downs, while medical technology continues to advance. Looking ahead to 2023, what are the investment themes in the medical device industry? VCBeat interviewed several senior investors in the field. These sectors have attracted attention.

Overall, domestic institutions continue to adhere to the investment logic of domestic substitution and high technical barriers, maintaining a positive outlook on China’s medical technology market. They are closely monitoring sectors such as surgical robots, endoscopes, implantable and interventional consumables, and cardiovascular and cerebrovascular devices. Although the competitive landscape continues to evolve, most investors remain actively and firmly optimistic about innovation opportunities in these key sectors, and the underlying rationale for this optimism remains solid. Identifying trends is not difficult; the real challenge lies in pinpointing the leading technologies and the right companies within these broader trends.

Neuromodulation Gained Momentum in 2022, with Promising Prospects for Integration with Brain-Computer Interfaces

In 2022, several Chinese companies in the neuromodulation sector, including Shenluo Medical, Jialiang Medical, Nuoer Medical, Ruishen’an, Jingyu Medical, MedPace, and Lingchuang Medical Valley, secured financing. Most of these funding rounds were still at early stages, reflecting the vitality and potential of the neuromodulation market.

The commercial value of neuromodulation has been validated globally, the application of neurostimulation in the global market is mature, and neuromodulation abroad has become an important clinical treatment for many refractory diseases.Major clinical applications include deep brain stimulation (DBS) for the treatment of Parkinson’s disease and depression; sacral nerve stimulation (SNS) for the treatment of urinary incontinence; vagus nerve stimulation (VNS) for the treatment of epilepsy; and spinal cord stimulation (SCS) for pain management. In 2018, global production of neurostimulators amounted to approximately 189,900 units, with sales reaching around USD 4 billion (equivalent to RMB 25.6 billion). China’s market production accounted for only about 1.63% of the global total, indicating substantial room for market expansion. The compound annual growth rate (CAGR) of the global neurostimulator market stands at 10%, and the market size is projected to reach USD 8.8 billion by 2025.

Innovations in Brain-Computer Interface Technology Are Poised to Unlock China’s Neuromodulation Market.With the continuous development and integration of technologies such as brain-computer interfaces, artificial intelligence, and robotics, the boundaries of the neuromodulation field are constantly expanding. Neuromodulation techniques, including deep brain stimulation (DBS), spinal cord stimulation (SCS), and vagus nerve stimulation (VNS), are not only effective treatments for functional brain disorders but also important tools for investigating disease mechanisms. The convergence of neuromodulation and brain-computer interface technology offers broad prospects for innovation. By combining neuromodulation with neurophysiological and neuroimaging approaches, researchers have abundant opportunities to explore the physiological basis of brain regulation, which holds significant importance for addressing refractory neurological diseases.

Taking insomnia disorder, a condition affecting approximately 300 million people in China, as an example, the majority of products on the market offer either monitoring alone or intervention alone. Leveraging brain-computer interface (BCI) technology, Sumian has developed the first insomnia disorder treatment system certified by the National Medical Products Administration (NMPA) that integrates real-time monitoring with dynamic intervention: the Pulsed Magnetic Therapy System. By utilizing artificial intelligence (AI) and big data to construct an adaptive neuromodulation model, the system provides digital, personalized treatment protocols for each patient. This approach effectively reduces the severity of insomnia, significantly shortens sleep latency, and facilitates the gradual reduction of sedative-hypnotic medications. As exploration into brain science and neurological disorders continues, along with in-depth research into neuromodulation technologies, Sumian will expand the application of its digital pulsed magnetic stimulation technology to other conditions, such as mild cognitive impairment and Parkinson’s syndrome.

Heart Failure and Cardiac Electrophysiology Remain Promising

Heart failure is regarded as the final frontier in the treatment of cardiovascular diseases. While humanity has made significant progress in treating most heart conditions, heart failure (HF) remains an exception, as its prevalence continues to rise and survival rates have seen only marginal improvement. In 2019, the global number of patients with heart failure reached 29.7 million, and it is projected to reach 38.7 million by 2030. The latest epidemiological survey on heart failure in China indicates that there are approximately 13.7 million patients, representing an increase of nearly 5 million compared to the survey conducted in 2000.

The primary reason for hospitalization in these patients was acute decompensation of chronic heart failure. As the condition progressed and pharmacological therapy became ineffective, existing domestic treatments for acute critical organ failure failed to achieve satisfactory clinical outcomes, resulting in a mortality rate exceeding 60%. In such cases, mechanical circulatory support (artificial heart) is the only viable option to assist blood circulation and perfusion, thereby maintaining normal function of systemic organs.

Artificial hearts can be classified into surgically implanted and interventional types based on the implantation method. According to their function, they are categorized into Ventricular Assist Devices (VADs) and Total Artificial Hearts (TAHs). Between the two, VADs are currently the most widely used artificial heart systems in clinical practice. VADs can be further divided into Left Ventricular Assist Devices (LVADs), Right Ventricular Assist Devices (RVADs), and Biventricular Assist Devices (BiVADs) based on the type of support provided, with LVADs being the most commonly used in clinical applications.

Three domestically produced left ventricular assist devices (LVADs) have been approved in China (Suzhou Tongxin Medical Technology Co., Ltd., Chongqing Yongrenxin Medical Device Co., Ltd., and Aerospace Taixin Technology Co., Ltd.).

From 2021 to 2022, interventional artificial hearts also garnered significant attention, with companies such as Magenta Medical (Xinqing Medical), Xinling Maide, Tongling Bionics, Fengkaili Medical, and Diyuan Medical securing financing. Artificial hearts have broad application potential, their product offerings are continuously expanding, and the future outlook is promising.

The journey is long, and only through persistent effort can we advance. Looking back at 2022, the medical device industry faced both challenges and achievements. As domestic epidemic prevention and control enters a new phase, the Chinese medical device market is poised for recovery. Having weathered the harsh winter, enterprises will emerge with greater resilience and accumulated strength, ready to unleash their potential. We look forward to what 2023 holds for the medical device industry.

"2022 Annual White Paper on Medical Device Innovation" Table of Contents

Chapter 1: Opportunities Amidst Crisis, Insights into the Medical Device Industry in 2022

1.1 Policy Uncertainty Cleared, Multiple Positive Factors Gradually Unfolding

1.2 Overall Decline in Primary Market Transactions; Early-Stage Investment Becomes More Selective

1.3 Secondary Market Undergoes Adjustment Period, IPO Companies Demonstrate Resilient Growth

1.4 The M&A Wave Rises, and the M&A Market Begins to Dance

Chapter 2 Forging Ahead: An Interpretation of Innovation in Niche Sectors

2.1 Cardiovascular Sector Continues to Lead in Financing, with Atrial Fibrillation and Heart Failure Garnering the Most Attention

2.2 The Surgical Robotics Sector Sees Surging Activity, with Core Proprietary Technologies Remaining Highly Promising

2.3 The Window of Policy Opportunity for CROs Is Opening, with Scale and Profitability Becoming Core Competencies

2.4 Financing in the Rehabilitation Sector Surges, with Rehabilitation Robotics Poised for Rapid Growth

Chapter 3: Forging Ahead in the Surge—Analysis of Innovative Cases in Medical Devices

3.1 Sumian: The First NMPA-Approved Digital Therapeutic System for Insomnia Disorder Integrating Monitoring and Treatment—Pulsed Magnetic Therapy System

3.2 Ensheng Medical: Pioneering a New Surgical Approach for Varicose Veins with “Non-Thermal Endoluminal Closure”

3.3 AngelExo: Single-Lower-Limb Exoskeleton Robot Approved for Market Launch, Ushering in a New Era of Intelligent Neurorehabilitation

3.4 Shenzhi Technology: Deepening Expertise in “Miniaturized Medical Imaging + AI-Assisted Remote Diagnosis”

3.5 Ruidi Bio: Internationally Original Nanosecond Pulsed Tumor Ablation System Breaks Through Industry Challenges

3.6 Noitom: HoloSight Intelligent Trauma Surgical Robot Achieves Full-Process 3D Visualization for Minimally Invasive Surgery

3.7 Haihe Biologics: Serving Globally, Providing High-Quality End-to-End Services for Medical Device Product Registration

3.8 Ruibo Biology: World-Class Expert Team Jointly Builds a Comprehensive Solution for High-Quality Embryo Culture Systems

3.9 Dejin Medical: Providing Excellent Integrated Interventional Treatment Solutions for Mitral and Tricuspid Valve Patients Worldwide

Chapter 4: Riding the Wind and Waves, Outlook for Subsectors in 2023

4.1 Neuromodulation Gained Momentum in 2022, with Promising Prospects for Integration with Brain-Computer Interfaces

4.2 The Rise of China’s Medical Device Industry Chain: Rapid Growth in Upstream Segments and CDMOs

4.3 Heart Failure and Cardiac Electrophysiology Remain Highly Promising

4.4 Seeing the Big Picture from Small Clues: The Ophthalmology Sector Is on the Rise