Where Did Cardiovascular Innovation Head in 2022 Under Volume-Based Procurement?

ReviewIn 2022, we found that capital has never reduced its focus on the cardiovascular market.

According to statistics from the VCBeat database, five cardiovascular companies in China went public in 2022, while the early-stage cardiovascular market also saw a surge.In 2022, a total of 17 early-stage investment deals were completed in China’s cardiovascular sector, with total financing amounting to nearly RMB 1 billion.

So, what stories have unfolded in the early-stage cardiovascular market over the past year? Which frontier directions are drawing attention? VCBeat has compiled and organized data on early-stage financing in the cardiovascular sector to inform our readers.

Three Major Trends Among 15 Startups

In the early-stage healthcare market, startups are a focal point, as they to some extent foreshadow the future trajectory of the healthcare industry. Based on this, VCBeat’s Orange Fruit Desk has compiled a list of startups in the cardiovascular sector that completed early-stage financing in 2022 and provides a brief analysis of three major trending themes.

1Cardiovascular Devices Are the Mainstream

In 2022, a total of 15 early-stage companies in China’s cardiovascular sector received investment, with cardiovascular device companies being the most favored by capital. According to statistics, for R&D-focused enterprises in the cardiovascular device fieldA total of 11 companies, accounting for 73%。

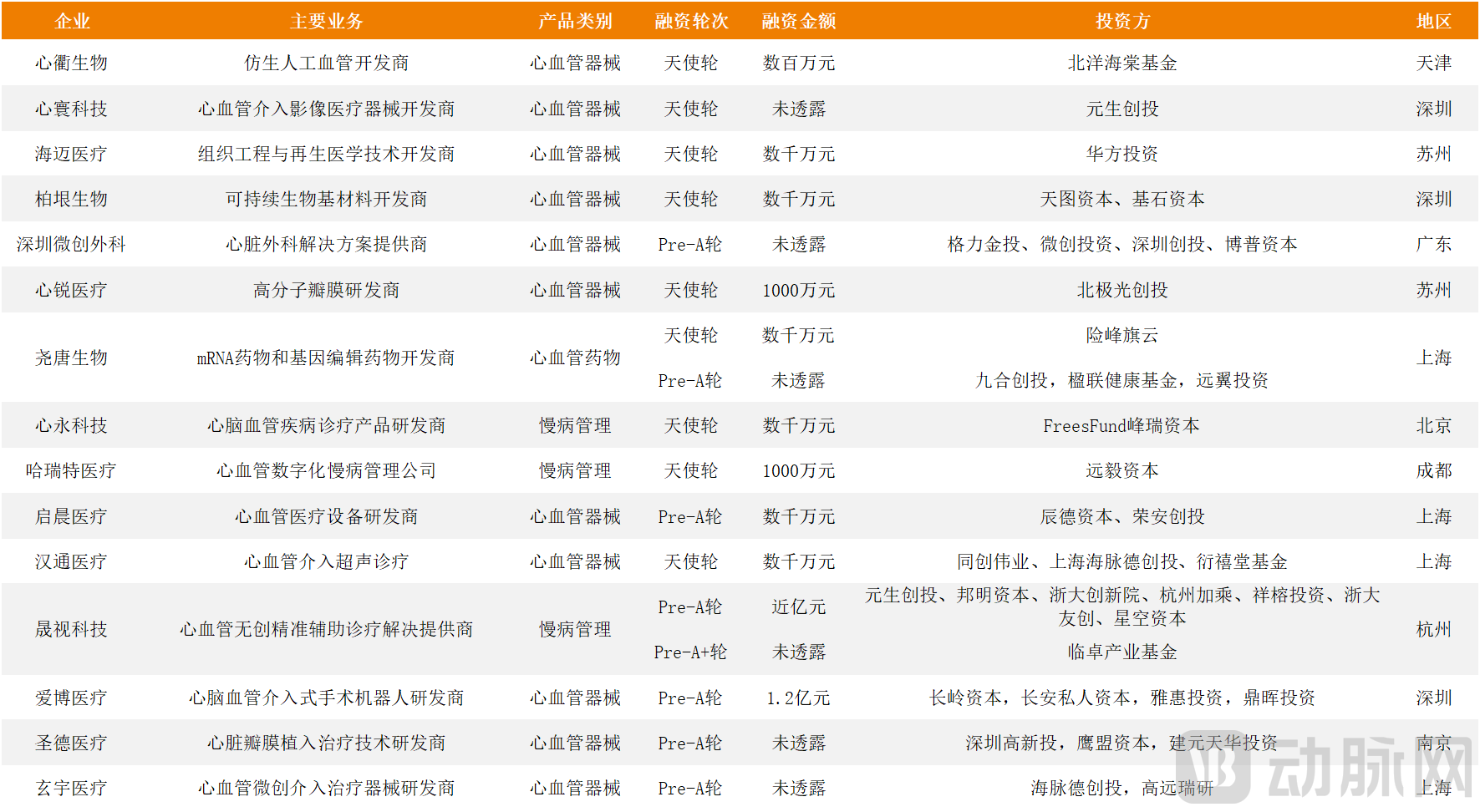

Early-Stage Cardiovascular Financing Events in China in 2022

Early-Stage Cardiovascular Financing Events in China in 2022

On the one hand,Medical devices face less innovation pressure than pharmaceuticals.. The development of innovative drugs is no easy task; it leans more toward technological leaps, which can lead to gaps and industry disruptors. Numerous challenges exist in terms of cost, complexity, clinical trial and registration requirements, as well as the difficulty of surpassing the efficacy of existing therapies. Meanwhile, public data shows that across all therapeutic areas globally, cardiovascular disease ranks second-to-last in success rates for Phase I, II, and III clinical trials of innovative drugs, with a mere 4% success rate in Phase I development. In contrast, the iteration and competition in the medical device sector belong to incremental innovation, placing greater emphasis on the accumulation of experience.

On the other hand,Cardiovascular diseases drive massive demand for medical devices. “In the medical device industry, cardiovascular conditions affect a larger population and carry higher fatality rates compared to other specialties, resulting in greater demand for medical products,” an investor specializing in cardiovascular devices told Chengguo Bureau.

According to data from AskCI Consulting, in 2021, the major segments of the medical device industry primarily included in vitro diagnostic reagents, cardiovascular devices and consumables, medical imaging equipment, orthopedic consumables, and ophthalmic consumables. Among these, cardiovascular devices and consumables ranked second, accounting for 11.3% of the global medical device market.

In fact, the field of cardiovascular devices is further divided into two categories: surgical devices and interventional devices. With technological advancements, guided by angiography systems,Minimally Invasive Interventional Therapy, due to its minimal invasiveness and low complication rate, it has gradually evolved into a more favored therapeutic approach for cardiovascular diseases.

This trend was also reflected in the early 2022 market, where 7 out of 11 companies engaged in R&D of cardiovascular drugs and devices were focused on interventional devices.

Having completed two rounds of financing in 2022,Shengde MedicalTake, for example, its focus on the research and development of transcatheter valve therapy (TAVR) products. TAVR is a minimally invasive valve replacement procedure that does not require open-heart surgery. Xcor, the first transcatheter aortic valve product under Shengde Medical, is used in TAVR procedures. It received approval from the first ethics committee in February 2022, and the first human implantation was performed in May by Professor Guo Yingqiang’s team at West China Hospital of Sichuan University.

2The Rise of Cardiovascular Chronic Disease Management and Monitoring

Among the 15 companies that completed early-stage financing in 2022, there are3 companiesStartups focusing on cardiovascular chronic disease management and monitoring include Xin Yong Technology, Haruit Medical, and Shengshi Technology.

Currently, artificial intelligence has facilitated medical advancements through big data sources such as electronic health records and cardiac imaging, with applications spanning lifestyle interventions, genetics, multi-omics, and wearable devices. In the field of cardiovascular medicine, AI encompasses disease screening, risk prediction, assisted diagnosis, treatment support, and follow-up monitoring.

Completed a $1.5 million angel round of financing in 2022Harit MedicalBy leveraging the new “Internet-based clinic + physical clinic” model and harnessing the advantages of digital connectivity, we integrate the four key stages of cardiovascular disease management—prevention, diagnosis, treatment, and rehabilitation—to build a professional, efficient, and standardized platform for managing chronic cardiovascular conditions. This enables a novel comprehensive management approach featuring “attending physician-led management, physician assistant support, patient self-management, and family supervision.”

For some patients with cardiovascular and cerebrovascular diseases, continuous blood pressure monitoring is of significant value. For instance, in cases of cerebral hemorrhage, excessively high blood pressure greatly increases the risk of recurrence. By continuously monitoring blood pressure and issuing alerts when levels become too high, the probability of recurrent cerebral hemorrhage can be substantially reduced. Having secured tens of millions of yuan in angel financing,Xinyong TechnologyThis approach utilizes hemodynamics combined with AI for continuous blood pressure monitoring, enabling individuals to conveniently access accurate blood pressure data anytime and anywhere, thereby preventing or mitigating the risks associated with cardiovascular and cerebrovascular diseases.

3Cardiovascular Innovative Drugs: An Evergreen Theme and Hotspot

In the field of innovative drugs, research and development has consistently been a focal point for major diseases, with cardiovascular disease being no exception. Data publicly presented at the 71st American College of Cardiology (ACC) Scientific Session revealed that researchers in the cardiovascular field launched nine drug development pipelines in 2022, including DIAMOND, PACMAN-AMI, TRANSLATE-TIMI 70, and MITIGATE.

Also in the primary market,Yaotang BioHaving completed a tens-of-millions-level angel financing round in February 2022, this is a high-tech biotechnology company focused on combining mRNA in vivo delivery technology with gene editing technology to develop next-generation mRNA drugs and gene editing therapies. By continuously developing and optimizing CRISPR, base editing, and other next-generation gene editing tools, and through innovative improvements to next-generation mRNA production platforms and lipid nanoparticle assembly processes, the company is dedicated to developing in vivo gene editing therapeutics for genetic diseases and cardiovascular diseases.

Yaotang Biologics has completed its product pipeline planning for 2022 in the field of genetic diseases, as well asCardiovascular disease R&D layout, with the aim of advancing products to the clinical trial application stage as soon as possible.

What Further Breakthroughs Lie Ahead for the Maturing Cardiovascular Industry?

Under centralized procurement, the cardiovascular industry has gradually matured.

Since the launch of national volume-based procurement (VBP) for coronary stents, occluders, and defibrillators in 2020, pilot procurement schemes at the provincial level and above have been continuously introduced for products such as pacemakers, balloons, and electrophysiology consumables. Although VBP has compressed market space, clinical demand remains robust, and technological iteration continues.

This is mainly due to two reasons: first,The cardiovascular industry is not in a state of complete saturation.From a technological perspective, technologies in areas such as heart valves and heart failure remain immature. Even in relatively mature fields like coronary interventions, pacemakers, and occluders, clinical needs are not yet fully met, and products continue to undergo optimization. Taking coronary interventions as an example, calcification remains a prominent challenge; commonly used rotational atherectomy devices are difficult to operate, resulting in a utilization rate of less than 1%.

Second,Favorable Macro Environment, with a Vast and Continuously Growing Market

In this context, what “cutting-edge technologies” and new trends have emerged in the early-stage cardiovascular market? VCBeat’s Orange Fruit Bureau has summarized the following three points:

1Cardiac Rhythm Management: Pulsed Field Ablation Shows High Growth Potential

Currently, pulsed field ablation (PFA) is considered the next-generation disruptive ablation technology.

It is reported that the majority of China’s more than 10 million patients with atrial fibrillation are treated with medication. Catheter ablation has not been widely adopted in China due to its high cost, technical complexity, high recurrence rate, significant risk of complications, and scarcity of experienced physicians. Compared with radiofrequency ablation and cryoablation, pulsed field ablation technology presentsShort operative time, minimal trauma, and low recurrence ratesuch advantages will significantly drive the domestic electrophysiology market.

Meanwhile, domestic companies are also actively positioning themselves in the PFA sector. In the early investment market of 2022,Xuanyu MedicalThe delivery catheter for venous closure adhesive has been innovatively designed to facilitate physician visualization of catheter position and assist in accurate placement. Meanwhile, the materials R&D team has optimized the formulation of the venous closure adhesive to enhance its occlusion efficacy and improve the clinical procedural experience. Currently,Its pulsed field ablation system has been submitted for type testing and is about to commence multicenter registration clinical trials.。

2Heart Failure Management: Atrial Shunts Remain Controversial, Yet Their Value Persists

In the field of heart failure management, controversy surrounding atrial shunt devices has persisted. In particular, the failure of Corvia’s Phase III clinical trial for its atrial shunt device in February 2022 dealt a significant blow to the atrial shunt market.

However, clinical setbacks do not imply that atrial shunt technology is unfeasible; the atrial shunt device market continues to gain recognition from experts and investors. According to statistics from VCBeat Research Institute, there were nine R&D pipelines globally in 2022, with Corvia Medical, Israel’s V-WAVE, Occlutech, Edwards Lifesciences, Nuosheng Medical, Weike Medical, Lepu Medical, Qichen Medical, and Aoliu Medical all entering the field. Analysis of the failed clinical data reveals that implantation of atrial shunt devices can reduce the incidence of heart failure events and improve patients’ health status.

which completed a tens-of-millions-yuan Pre-A financing round in 2022Qichen Medicalas an example, its productsSIRIUS AFR Atrial Shunt SystemIt is the world’s first atrial shunt device with a multi-layer braided structure, as well as the first to utilize a compression bonding process. The SIRIUS AFR features secondary interventional retrieval capability, and its delivery sheath is pre-curved. Currently, some patients have completed six-month follow-ups, indicating successful clinical trials of the SIRIUS AFR.

3Vascular Interventional Surgical Robots Emerge as “Star” Technologies

When it comes to the buzzwords in the healthcare industry in 2022, vascular interventional surgical robots certainly rank among them.

This is due to the volume and complexity of endovascular interventions. In terms of volume, in 2019, China performed over 1 million percutaneous coronary intervention (PCI) procedures and approximately 4 million coronary angiographies. With the deepening aging of the population, these numbers continue to rise. Regarding procedural complexity,Neurointerventional procedures are characterized by high technical difficulty, elevated risk, and prolonged duration....and other characteristics. Cerebral blood vessels are tortuous and fragile, requiring high precision in interventional procedures. These procedures are highly dependent on the physician’s individual experience and expertise, with a single neurointerventional surgery often taking more than twice as long as a coronary intervention.

Based on this, the vascular interventional surgical robotics sector is developing rapidly, with China's market expected to achieve a compound annual growth rate (CAGR) exceeding 90%. Industry giants such as Siemens and MicroPort have entered the field. Capital investment is also fueling this growth, with multiple financing rounds exceeding RMB 100 million injected into the sector, including a Pre-A round of RMB 120 million secured in March 2022 byAier Medical, as a pioneer in the field of pan-vascular interventional surgical robots, Aibo Medical completed China’s first neurointerventional clinical trial in 2017, making vascular intervention a powerful tool for treating cardiovascular and cerebrovascular diseases.

In fact, the advent of surgical robots has made the intelligent and automated performance of vascular interventional procedures possible. Acting as the eyes, hands, and brain of the physician, and leveraging a master-slave separation mode with precise force feedback, these systems enable medical personnel to perform surgical operations outside the catheterization laboratory using Aibo Medical’s vascular interventional surgical robot, not onlyEnabling more precise and efficient interventional procedures, reducing the incidence of postoperative complications in patients, and allowing physicians to stay away from the catheterization laboratory, thereby significantly reducing radiation exposure.。

De-homogenization: Say Goodbye to Involution

It is reported that China accounts for 14% of the global medical device market, making it the second-largest market worldwide. Meanwhile, population aging, along with improvements in residents’ quality of life and healthcare conditions, is jointly driving sustained growth in high-quality demand among cardiovascular patients.

The vast market potential has spurred a boom in the cardiovascular disease sector over the past two years, with numerous unprofitable companies listing on capital markets and becoming prime targets for investors seeking high returns. In reality, however, technological innovation in the current cardiovascular field is plagued by homogenization and intense internal competition.

Jiang Tianjiao, Dean of VCBeat Research Institute, pointed out at the 2022 Xiamen Cardiovascular Health Industry Innovation Forum, when looking solely at domestically listed valve companies, there is still a certain gap compared to the international giant Edwards.

Part of the reason is that domestic cardiovascular device innovation suffers from severe homogenization, lacking more granular segmentation. For instance, domestic valve development closely mirrors U.S. products. Additionally, in the transcatheter mitral valve (TMV) sector, a large number of Chinese enterprises have flooded the market, leading to certain bubbles and overheating in technological innovation.

To narrow the gap, say goodbye to involution, and achieveTechnological Upgrades and Diversified Innovation Are Key。

First, innovation must shift from mere "technical showmanship" to a balanced approach; it is not simply about increasing engineering complexity, but rather about achieving a balance among clinical efficacy, safety, and ease of use.

Secondly, beyond core products such as mitral and tricuspid valves, there are also opportunities for innovation; for instance, significant innovative potential exists in ancillary devices like clipping systems used for repair during severe aortic calcification.

Finally, it is essential to discard biases and overcome critical technological bottlenecks. Currently, in both domestic and international markets, innovation in valve replacement products is predominantly focused on transcatheter interventional therapies, while innovation in traditional surgical valves has been relatively slow, or even stagnant, particularly for mechanical valves. However, in September 2022, the innovative company Novostia launched a mechanical valve that does not require lifelong anticoagulation—the Triflo valve. This breakthrough mechanical valve, made from high-performance biocompatible materials, offers patients a unique, durable, anticoagulation-free, and noiseless heart valve option.

Product innovation across various sub-sectors of the cardiovascular field is highly active. To seize this wave of innovation, companies should continuously pursue cross-disciplinary innovation rather than mere imitation and replication. Whether for early-stage startups or publicly listed companies, technological upgrades must avoid homogenization and focus on original innovation.